Homework Answers

Add Answer to:

4. (5 pts.) Draw the tree for a put option on $20,000 with a strike price of £10,000. The current...

The premium on a June 17 British pound call option with a strike price of $1.2560...

The premium on a June 17 British pound call option with a strike price of $1.2560 when the spot rate is $1.2620 is quoted as $0.02. The time value of this option is. The premium on a June 17 British pound call option with a strike price of $1.2750 when the spot rate is $1.2620 is quoted as $0.025. The intrinsic value of this option is. Your firm has an accounts receivable worth C$200,000 due in six months. The firm...

Consider a put option written on €100,000. The strike price is $1.50 = €1.00 and the...

Consider a put option written on €100,000. The strike price is $1.50 = €1.00 and the option premium is $0.02. At what exchange rate will the buyer of this put option break even? Grupo de opciones de respuesta $1.50 = €1.00 $1.48 = €1.00 $1.00 = €.667 $1.52 = €1.00

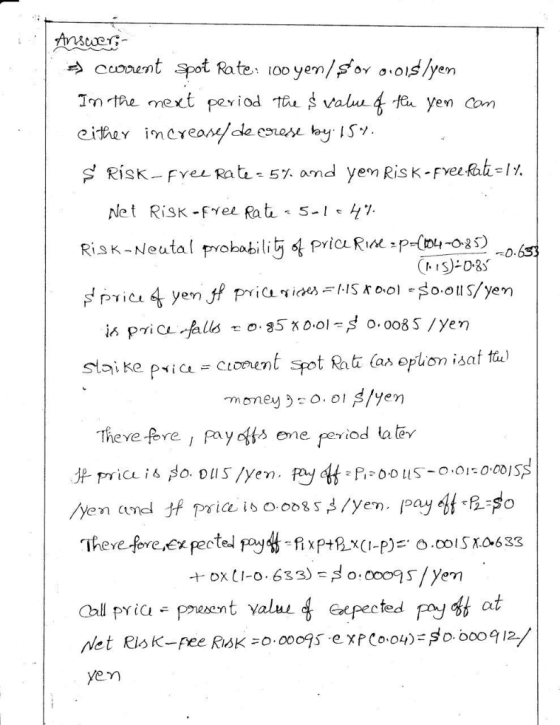

Calculate the value of an eight-month European put option on a currency with a strike price...

Calculate the value of an eight-month European put option on a currency with a strike price of 0.50. The current exchange rate is 0.52, the volatility of the exchange rate is 12%, the domestic risk-free interest rate is 4% per annum, and the foreign risk-free interest rate is 8% per annum.

Long currency straddle Call option premium = $0.05/€, Put option premium = $0.05/€ Strike price =...

Long currency straddle Call option premium = $0.05/€, Put option premium = $0.05/€ Strike price = $1.10/€, Option contract size = €62,500 Draw graphs of call option, put option, and straddle Mark BE point and Strike prices Mark each premium Spot exchange rate $1.00/€ $1.05/€ $1.10/€ $1.15/€ $1.20/€ $1.25/€ Long call option Exercise (N/Y) Holder’s net profit per unit Long put option Exercise (N/Y) Holder’s net profit per unit Net profit Net profit per unit (graph) Short currency straddle Call...

The current price of a stock is $75. A put option with a strike price of...

The current price of a stock is $75. A put option with a strike price of $70 is purchased along with the stock. If the breakeven point for this hedge is at a stock price of $82, then the value of the put option at the time of purchase was (a) $5 (b) $7 (c) $12 (d) $14 (e) None of the above

The current price of a stock is $75. A put option with a strike price of $70 is purchased along with the stock. If the breakeven point for this hedge is at a stock price of $82, then the value of the put option at the time of purchase was (a) $5 (b) $7 (c) $12 (d) $14 (e) None of the above

The current price of a stock is $75. A put option with a strike price of...

The current price of a stock is $75. A put option with a strike price of $70 is purchased along with the stock. If the breakeven point for this hedge is at a stock price of $82, then the value of the put option at the time of purchase was (a) $5 (b) $7 (c) $12 (d) $14 (e) None of the above FIN

The current price of a stock is $75. A put option with a strike price of $70 is purchased along with the stock. If the breakeven point for this hedge is at a stock price of $82, then the value of the put option at the time of purchase was (a) $5 (b) $7 (c) $12 (d) $14 (e) None of the above FIN

Using a binomial tree, what is the price of a $40 strike 6-month American put option,...

Using a binomial tree, what is the price of a $40 strike 6-month American put option, using 3-month intervals as the time period? Assume the following data: S=$37.90, r=5.0%, 5=35%, =0.

Using a binomial tree, what is the price of a $40 strike 6-month American put option, using 3-month intervals as the time period? Assume the following data: S=$37.90, r=5.0%, 5=35%, =0.

4. Consider six months European put option with a strike price of $100 on a stock...

4. Consider six months European put option with a strike price of $100 on a stock with current price $100. There are two time steps and in each time step the stock price either moves up by 10% or moves down by 10%. Risk-free interest rate is Y-5% (on 3 months (a) Find the current option price. (b) Compute the number of shares of stock which should be held by the replicating portfolio at time 0 and 1 (after 3...

4. Consider six months European put option with a strike price of $100 on a stock with current price $100. There are two time steps and in each time step the stock price either moves up by 10% or moves down by 10%. Risk-free interest rate is Y-5% (on 3 months (a) Find the current option price. (b) Compute the number of shares of stock which should be held by the replicating portfolio at time 0 and 1 (after 3...

Consider an option to buy £10,000 for €12,500. In the next period, if the pound appreciates...

Consider an option to buy £10,000 for €12,500. In the next period, if the pound appreciates against the dollar by 37.5 percent then the euro will appreciate against the dollar by ten percent. On the other hand, the euro could depreciate against the pound by 20 percent. Big hint: don't round, keep exchange rates out to at least 4 decimal places. Spot Rates Risk-free Rates S0($/€) $1.60 = €1.00 i$ 3.00% S0($/£) $2.00 = £1.00 i€ 4.00% S0(€/£) €1.25 =...

Consider a six-month call option written on €100,000 with a strike price of $1.00 = €1.00. The current exchange rate is...

Consider a six-month call option written on €100,000 with a strike price of $1.00 = €1.00. The current exchange rate is $1.25 = €1.00; The U.S. risk-free rate is 5% over the period and the euro-zone risk-free rate is 4%. Assume that N(d1)=0.9989, and N(d2)=0.9985. What is the option value using the Black-Scholes model? The answer is $25005 How do i get that?

The current price of a stock is $75. A put option with a strike price of $70 is purchased along with the stock. If the breakeven point for this hedge is at a stock price of $82, then the value of the put option at the time of purchase was (a) $5 (b) $7 (c) $12 (d) $14 (e) None of the above

The current price of a stock is $75. A put option with a strike price of $70 is purchased along with the stock. If the breakeven point for this hedge is at a stock price of $82, then the value of the put option at the time of purchase was (a) $5 (b) $7 (c) $12 (d) $14 (e) None of the above

The current price of a stock is $75. A put option with a strike price of $70 is purchased along with the stock. If the breakeven point for this hedge is at a stock price of $82, then the value of the put option at the time of purchase was (a) $5 (b) $7 (c) $12 (d) $14 (e) None of the above FIN

The current price of a stock is $75. A put option with a strike price of $70 is purchased along with the stock. If the breakeven point for this hedge is at a stock price of $82, then the value of the put option at the time of purchase was (a) $5 (b) $7 (c) $12 (d) $14 (e) None of the above FIN

Using a binomial tree, what is the price of a $40 strike 6-month American put option, using 3-month intervals as the time period? Assume the following data: S=$37.90, r=5.0%, 5=35%, =0.

Using a binomial tree, what is the price of a $40 strike 6-month American put option, using 3-month intervals as the time period? Assume the following data: S=$37.90, r=5.0%, 5=35%, =0.

4. Consider six months European put option with a strike price of $100 on a stock with current price $100. There are two time steps and in each time step the stock price either moves up by 10% or moves down by 10%. Risk-free interest rate is Y-5% (on 3 months (a) Find the current option price. (b) Compute the number of shares of stock which should be held by the replicating portfolio at time 0 and 1 (after 3...

4. Consider six months European put option with a strike price of $100 on a stock with current price $100. There are two time steps and in each time step the stock price either moves up by 10% or moves down by 10%. Risk-free interest rate is Y-5% (on 3 months (a) Find the current option price. (b) Compute the number of shares of stock which should be held by the replicating portfolio at time 0 and 1 (after 3...

Most questions answered within 3 hours.

-

Assume Kw = 1.01 ✕ 10−14

For pure water, we can calculate [H3O+ ] = [OH...

asked 14 minutes ago -

Suppose that on a temperature scale X, water boils at 203.0°X

and freezes at -105.7°X. What...

asked 1 hour ago -

BaS crystallizes in a cubic unit cell with S2- ions on each

corner and each face....

asked 1 hour ago -

A. 0≤P(Oi)≤10≤P(Oi)≤1 for each i

B. P(Oi)≤0P(Oi)≤0

C. P(Oi)=1+P(OCi)P(Oi)=1+P(OiC)

D. P(Oi)≥1P(Oi)≥1

If an experiment consists of...

asked 3 hours ago -

A battery has an emf of 9.20V and an internal resistance of 1.20

ohm. a)What resistance...

asked 3 hours ago -

The area of an elastic circular loop decreases at a constant

rate, dA/dt = −6.60×10−3 m2/s...

asked 4 hours ago -

The denaturation of proteins can be described by the

equilibrium

F⇌U

where F and U represent...

asked 5 hours ago -

Please answer what the maximum and minimum force is, and the

angle on the ion is...

asked 5 hours ago -

implement a program that reads a number of rows and a symbol.

The program will draw...

asked 5 hours ago -

Assume that when adults with smartphones are randomly selected,

45% use them in meetings or classes....

asked 5 hours ago -

Determine the number of formula units of

Na2SO4 and moles of oxygen contained in 8.11

moles...

asked 6 hours ago -

Explain in steps on the following code

What would be the output when executed

using System;...

asked 6 hours ago