Homework Answers

Add Answer to:

5. Suppose that the market can be described by the following three sources of svstematic risk. Th...

9. Suppose that the market can be described by the following three sources of systematic risk...

9. Suppose that the market can be described by the following three sources of systematic risk with associated risk premiums. Factor Risk Premium Industrial production (I) 7% Interest rates (R) 2 Consumer confidence (C) 5 The return on a particular stock is generated according to the following equation: r = 19% + 0.8I + 0.4R + 0.50C + e a-1. Find the equilibrium rate of return on this stock using the APT. The T-bill rate...

Suppose that the market can be described by the following three sources of systematic risk with...

Suppose that the market can be described by the following three sources of systematic risk with associated risk premiums. Factor Risk Premium Industrial production (I) 7 % Interest rates (R) 4 % Consumer confidence (C) 5 % The return on a particular stock is generated according to the following equation: r = 12% + 1.2I + 0.8R + 1.00C + e a-1. Find the equilibrium rate of return on this stock using the APT. The T-bill rate is 8%. (Do...

Suppose that the market can be described by the following three sources of systematic risk with...

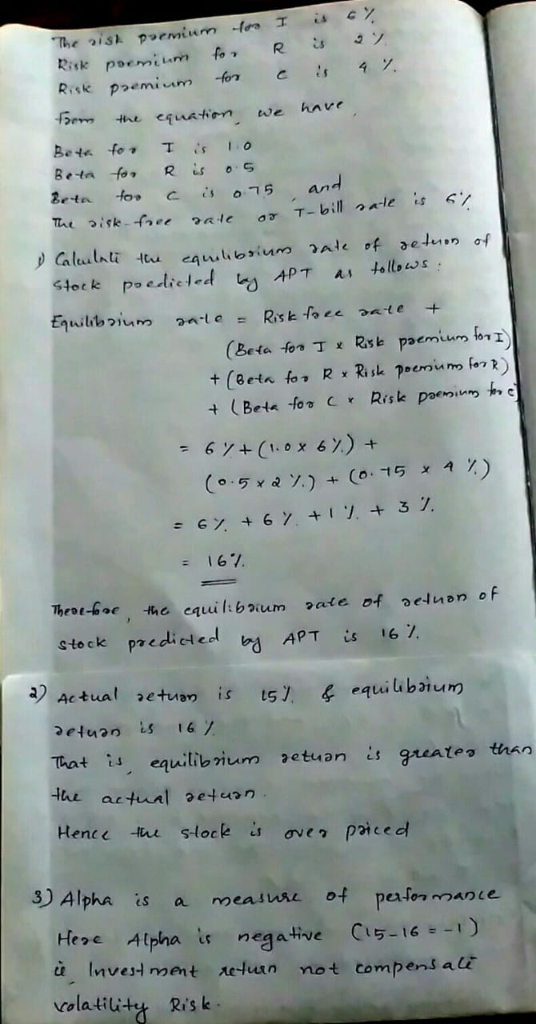

Suppose that the market can be described by the following three sources of systematic risk with associated risk premiums. Factor Industrial production (1) Interest rates (R) Consumer confidence (C) The return on a particular stock is generated according to the following equation: r=19% +0.71 +0.4R+ 0.60C+ e 0-1. Find the equilibrium rate of return on this stock using the APT. The T-bill rate is 8%. (Do not round intermediate calculations. Round your answer to 1 decimal place.) Equilibrium rate of...

Suppose that the market can be described by the following three sources of systematic risk with associated risk premiums. Factor Industrial production (1) Interest rates (R) Consumer confidence (C) The return on a particular stock is generated according to the following equation: r=19% +0.71 +0.4R+ 0.60C+ e 0-1. Find the equilibrium rate of return on this stock using the APT. The T-bill rate is 8%. (Do not round intermediate calculations. Round your answer to 1 decimal place.) Equilibrium rate of...

Consider the following information: Beta Portfolio Risk- free Market Expected Return 6 % 11.4 9.4 20...

Consider the following information: Beta Portfolio Risk- free Market Expected Return 6 % 11.4 9.4 20 a. Calculate the expected return of portfolio A with a beta of 20. (Round your answer to 2 decimal places.) Expected return b. What is the alpha of portfolio A (Negative value should be indicated by a minus sign. Round your answer to 2 decimal places.) Alpha c. If the simple CAPM is valid state whether the above situation is possible? Yes No 5....

Consider the following information: Beta Portfolio Risk- free Market Expected Return 6 % 11.4 9.4 20 a. Calculate the expected return of portfolio A with a beta of 20. (Round your answer to 2 decimal places.) Expected return b. What is the alpha of portfolio A (Negative value should be indicated by a minus sign. Round your answer to 2 decimal places.) Alpha c. If the simple CAPM is valid state whether the above situation is possible? Yes No 5....

Please answer Which of the following statements about the Arbitrage Pricing Theory (APT) are correct? Check...

Please answer

Which of the following statements about the Arbitrage Pricing Theory (APT) are correct? Check all that apply The APT is more general than the Capital Asset Pricing Model (CAPM) The APT maintains that the realized return on any stock depends on changes unique to the firm. The APT model maintains that the realized returns on stocks depend on unexpected changes in fundamental economic factors The APT identifies all relevant factors that affect the realized returns on stocks Imani,...

Please answer

Which of the following statements about the Arbitrage Pricing Theory (APT) are correct? Check all that apply The APT is more general than the Capital Asset Pricing Model (CAPM) The APT maintains that the realized return on any stock depends on changes unique to the firm. The APT model maintains that the realized returns on stocks depend on unexpected changes in fundamental economic factors The APT identifies all relevant factors that affect the realized returns on stocks Imani,...

9. The Arbitrage Pricing Theory Which of the following statements about the Arbitrage Pricing Theory (APT)...

9. The Arbitrage Pricing Theory Which of the following statements about the Arbitrage Pricing Theory (APT) are correct? Check all that apply. The APT is more restrictive than the Capital Asset Pricing Model (CAPM). The APT assumes that all investors hold the market portfolio The APT does not identify the relevant factors. The APT does not restrict the number or nature of the factors relevant to the determination of a stock's return. Karine, an analyst at Graffiti Aviation (GA), models...

9. The Arbitrage Pricing Theory Which of the following statements about the Arbitrage Pricing Theory (APT) are correct? Check all that apply. The APT is more restrictive than the Capital Asset Pricing Model (CAPM). The APT assumes that all investors hold the market portfolio The APT does not identify the relevant factors. The APT does not restrict the number or nature of the factors relevant to the determination of a stock's return. Karine, an analyst at Graffiti Aviation (GA), models...

Stock E(R) Standard Deviation Correlation between the stock and the market portfolio A 13% 12% 0.9...

Stock E(R) Standard Deviation Correlation between the stock and the market portfolio A 13% 12% 0.9 B 11% 16% 0.5 C 16% 23% 0.3 Standard Deviation for the market portfolio: 8% Risk free rate of return: 3% Market rate of return: 11% a. Calculate the alpha of three stocks above and determine if each stock is underpriced or overpriced. b. If you currently hold a market index portfolio, which stock is the best stock to add to your portfolio? c....

Consider the following information about three stocks: a. If your portfolio is invested 40 percent each...

Consider the following information about three stocks:

a. If your portfolio is invested 40 percent each in A and B and

20 percent in C, what is the portfolio expected return? The

variance? The standard deviation?

b.If the expected T-bill is is 3.80 percent, what is the

expected premium on the portfolio?

c. If the expected inflation rate is 3.50 percent, what are the

appropriate and exact expected real returns on the portfolio?What

are the approximate and exact expected real...

Consider the following information about three stocks:

a. If your portfolio is invested 40 percent each in A and B and

20 percent in C, what is the portfolio expected return? The

variance? The standard deviation?

b.If the expected T-bill is is 3.80 percent, what is the

expected premium on the portfolio?

c. If the expected inflation rate is 3.50 percent, what are the

appropriate and exact expected real returns on the portfolio?What

are the approximate and exact expected real...

12. Portfolio has beta=-0.5; its alpha is -2%, risk free rate is 5%; market expected return...

12. Portfolio has beta=-0.5; its alpha is -2%, risk free rate is 5%; market expected return is 8%. Find market risk premium R_mt, expected return r_portfolio and excess return R_portfolio. Use formula R_portfolio =beta portfolio *R_market]+alpha+e_portfolio; Where for each security, R=r-r_free is excess return; Is such portfolio over-, under- or fairly priced? Assume, portfolio is well diversified. Which term (s) should be negligible? Follow the guideline below to take the steps using a well- diversified portfolio to build an arbitrage...

12. Portfolio has beta=-0.5; its alpha is -2%, risk free rate is 5%; market expected return is 8%. Find market risk premium R_mt, expected return r_portfolio and excess return R_portfolio. Use formula R_portfolio =beta portfolio *R_market]+alpha+e_portfolio; Where for each security, R=r-r_free is excess return; Is such portfolio over-, under- or fairly priced? Assume, portfolio is well diversified. Which term (s) should be negligible? Follow the guideline below to take the steps using a well- diversified portfolio to build an arbitrage...

B2 Consider the following information on a portfolio of three stocks: State of Probabil f Stock...

B2 Consider the following information on a portfolio of three stocks: State of Probabil f Stock A Stock B Stock C Rate of Return Rate of Return Rate of Return 21 15 -22 Economy State of Ec Boom Normal Bust 15 80 05 .05 08 18 .07 The portfolio is invested 35 percent in each Stock A and Stock B and 30 percent in Stock C If the expected T-bill rate is 3.90 percent, what is the expected risk premium...

B2 Consider the following information on a portfolio of three stocks: State of Probabil f Stock A Stock B Stock C Rate of Return Rate of Return Rate of Return 21 15 -22 Economy State of Ec Boom Normal Bust 15 80 05 .05 08 18 .07 The portfolio is invested 35 percent in each Stock A and Stock B and 30 percent in Stock C If the expected T-bill rate is 3.90 percent, what is the expected risk premium...

Suppose that the market can be described by the following three sources of systematic risk with associated risk premiums. Factor Industrial production (1) Interest rates (R) Consumer confidence (C) The return on a particular stock is generated according to the following equation: r=19% +0.71 +0.4R+ 0.60C+ e 0-1. Find the equilibrium rate of return on this stock using the APT. The T-bill rate is 8%. (Do not round intermediate calculations. Round your answer to 1 decimal place.) Equilibrium rate of...

Suppose that the market can be described by the following three sources of systematic risk with associated risk premiums. Factor Industrial production (1) Interest rates (R) Consumer confidence (C) The return on a particular stock is generated according to the following equation: r=19% +0.71 +0.4R+ 0.60C+ e 0-1. Find the equilibrium rate of return on this stock using the APT. The T-bill rate is 8%. (Do not round intermediate calculations. Round your answer to 1 decimal place.) Equilibrium rate of...

Consider the following information: Beta Portfolio Risk- free Market Expected Return 6 % 11.4 9.4 20 a. Calculate the expected return of portfolio A with a beta of 20. (Round your answer to 2 decimal places.) Expected return b. What is the alpha of portfolio A (Negative value should be indicated by a minus sign. Round your answer to 2 decimal places.) Alpha c. If the simple CAPM is valid state whether the above situation is possible? Yes No 5....

Consider the following information: Beta Portfolio Risk- free Market Expected Return 6 % 11.4 9.4 20 a. Calculate the expected return of portfolio A with a beta of 20. (Round your answer to 2 decimal places.) Expected return b. What is the alpha of portfolio A (Negative value should be indicated by a minus sign. Round your answer to 2 decimal places.) Alpha c. If the simple CAPM is valid state whether the above situation is possible? Yes No 5....

Please answer

Which of the following statements about the Arbitrage Pricing Theory (APT) are correct? Check all that apply The APT is more general than the Capital Asset Pricing Model (CAPM) The APT maintains that the realized return on any stock depends on changes unique to the firm. The APT model maintains that the realized returns on stocks depend on unexpected changes in fundamental economic factors The APT identifies all relevant factors that affect the realized returns on stocks Imani,...

Please answer

Which of the following statements about the Arbitrage Pricing Theory (APT) are correct? Check all that apply The APT is more general than the Capital Asset Pricing Model (CAPM) The APT maintains that the realized return on any stock depends on changes unique to the firm. The APT model maintains that the realized returns on stocks depend on unexpected changes in fundamental economic factors The APT identifies all relevant factors that affect the realized returns on stocks Imani,...

9. The Arbitrage Pricing Theory Which of the following statements about the Arbitrage Pricing Theory (APT) are correct? Check all that apply. The APT is more restrictive than the Capital Asset Pricing Model (CAPM). The APT assumes that all investors hold the market portfolio The APT does not identify the relevant factors. The APT does not restrict the number or nature of the factors relevant to the determination of a stock's return. Karine, an analyst at Graffiti Aviation (GA), models...

9. The Arbitrage Pricing Theory Which of the following statements about the Arbitrage Pricing Theory (APT) are correct? Check all that apply. The APT is more restrictive than the Capital Asset Pricing Model (CAPM). The APT assumes that all investors hold the market portfolio The APT does not identify the relevant factors. The APT does not restrict the number or nature of the factors relevant to the determination of a stock's return. Karine, an analyst at Graffiti Aviation (GA), models...

Consider the following information about three stocks:

a. If your portfolio is invested 40 percent each in A and B and

20 percent in C, what is the portfolio expected return? The

variance? The standard deviation?

b.If the expected T-bill is is 3.80 percent, what is the

expected premium on the portfolio?

c. If the expected inflation rate is 3.50 percent, what are the

appropriate and exact expected real returns on the portfolio?What

are the approximate and exact expected real...

Consider the following information about three stocks:

a. If your portfolio is invested 40 percent each in A and B and

20 percent in C, what is the portfolio expected return? The

variance? The standard deviation?

b.If the expected T-bill is is 3.80 percent, what is the

expected premium on the portfolio?

c. If the expected inflation rate is 3.50 percent, what are the

appropriate and exact expected real returns on the portfolio?What

are the approximate and exact expected real...

12. Portfolio has beta=-0.5; its alpha is -2%, risk free rate is 5%; market expected return is 8%. Find market risk premium R_mt, expected return r_portfolio and excess return R_portfolio. Use formula R_portfolio =beta portfolio *R_market]+alpha+e_portfolio; Where for each security, R=r-r_free is excess return; Is such portfolio over-, under- or fairly priced? Assume, portfolio is well diversified. Which term (s) should be negligible? Follow the guideline below to take the steps using a well- diversified portfolio to build an arbitrage...

12. Portfolio has beta=-0.5; its alpha is -2%, risk free rate is 5%; market expected return is 8%. Find market risk premium R_mt, expected return r_portfolio and excess return R_portfolio. Use formula R_portfolio =beta portfolio *R_market]+alpha+e_portfolio; Where for each security, R=r-r_free is excess return; Is such portfolio over-, under- or fairly priced? Assume, portfolio is well diversified. Which term (s) should be negligible? Follow the guideline below to take the steps using a well- diversified portfolio to build an arbitrage...

B2 Consider the following information on a portfolio of three stocks: State of Probabil f Stock A Stock B Stock C Rate of Return Rate of Return Rate of Return 21 15 -22 Economy State of Ec Boom Normal Bust 15 80 05 .05 08 18 .07 The portfolio is invested 35 percent in each Stock A and Stock B and 30 percent in Stock C If the expected T-bill rate is 3.90 percent, what is the expected risk premium...

B2 Consider the following information on a portfolio of three stocks: State of Probabil f Stock A Stock B Stock C Rate of Return Rate of Return Rate of Return 21 15 -22 Economy State of Ec Boom Normal Bust 15 80 05 .05 08 18 .07 The portfolio is invested 35 percent in each Stock A and Stock B and 30 percent in Stock C If the expected T-bill rate is 3.90 percent, what is the expected risk premium...

Most questions answered within 3 hours.

-

(Expected rate of return and risk) Carter Inc. is evaluating a

security. Calculate the investment’s expected...

asked 2 hours ago -

What specific indicators can point to lack of progress for

African Americans in American society?

asked 3 hours ago -

1-The Electrons in a beam are moving at 2.7×108 m/s in an

electric field of 15000...

asked 3 hours ago -

A gas tank is a vertical cylinder. It has a radius of 1m, a

height of...

asked 4 hours ago -

Accent Software faces the following conditions. All of these

support Accent’s use of a market-penetration pricing...

asked 5 hours ago -

A mathematically inclined friend emails you the following

instructions: "Meet me in the cafeteria the first...

asked 5 hours ago -

A monopoly sells in two countries . The demand curves in the two

countries are p1...

asked 6 hours ago -

A .15kg rubber ball is bounced off a wall. Before hitting the

wall, the ball moves...

asked 6 hours ago -

A manufacturing company preparing to build a new plant is

considering three potential locations for it....

asked 6 hours ago -

B. If compound Y has approximately the same values of solubility

in toluene as compound X,...

asked 7 hours ago -

Oscar Inc. has inventory in Japan valued at 39,051,000 Yen one

year ago. One year ago...

asked 7 hours ago -

If Canada suffered from "fundamental disequilibrium," and its

government choose not to devalue its currency, a...

asked 7 hours ago