Homework Answers

Please do rate me and mention doubts in the comments section

Add Answer to:

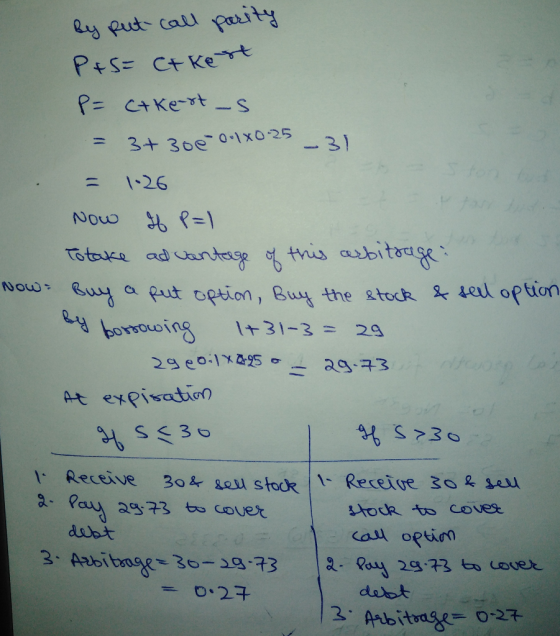

Arbitrage Opportunities . Suppose that So -31 T0.25 K -30 What are the arbitrage possibilities wh...

Suppose a security with a risk-free cash flow of $152 in one year trades for $137 today. If there are no arbitrage opportunities, what is the current risk-free interest rate?

Suppose a security with a risk-free cash flow of $152 in one year trades for $137 today. If there are no arbitrage opportunities, what is the current risk-free interest rate?

Show work, thanks. Let C(K) and P(K) be the call and the put premiums when the...

Show work, thanks.

Let C(K) and P(K) be the call and the put premiums when the strike price is A 8. Suppose C(50) 16,C(55) 10 and P(50) 7, P(55) 14. What no-arbitrage property is violated? If so, demonstrate arbitrage

Show work, thanks.

Let C(K) and P(K) be the call and the put premiums when the strike price is A 8. Suppose C(50) 16,C(55) 10 and P(50) 7, P(55) 14. What no-arbitrage property is violated? If so, demonstrate arbitrage

the futures price for a contract deliverable in four months is 520. What arbitrage opportunities does this create?...

the futures price for a contract deliverable in four months is 520. What arbitrage opportunities does this create? 8. (10 marks) The 6-month, 12-month, 18-month, and 24-month zero rates are 5%, 5.5%, 5.75%, and 6%, with semiannual compounding, (a) What are the rates with continuous compounding? (b) What is the forward rate for the 6-month period beginning in 18 months? (c) What is the value of an FRA that promises to pay you 6.5% (compounded semiannually) on a principal of...

the futures price for a contract deliverable in four months is 520. What arbitrage opportunities does this create? 8. (10 marks) The 6-month, 12-month, 18-month, and 24-month zero rates are 5%, 5.5%, 5.75%, and 6%, with semiannual compounding, (a) What are the rates with continuous compounding? (b) What is the forward rate for the 6-month period beginning in 18 months? (c) What is the value of an FRA that promises to pay you 6.5% (compounded semiannually) on a principal of...

2.2 Given: S(0)-50; r= 0.05, T-6 months; K = 49. What is a lower bound for...

2.2 Given: S(0)-50; r= 0.05, T-6 months; K = 49. What is a lower bound for an American Call Option on non-dividend paying stock? If an American Call option in the previous question (2.2) trades at $51, we have... O ANo arbitrage opportunities. O B An arbitrage opportunity by writing the call, buying the underlying stock and investing at a risk-free rate. O CAn arbitrage opportunity by writing the call and investing at a risk-free rate O D An arbitrage...

2.2 Given: S(0)-50; r= 0.05, T-6 months; K = 49. What is a lower bound for an American Call Option on non-dividend paying stock? If an American Call option in the previous question (2.2) trades at $51, we have... O ANo arbitrage opportunities. O B An arbitrage opportunity by writing the call, buying the underlying stock and investing at a risk-free rate. O CAn arbitrage opportunity by writing the call and investing at a risk-free rate O D An arbitrage...

according to the graph of the production possibilities frontier, what is the opportunity cost of the...

according to the graph of the production possibilities

frontier, what is the opportunity cost of the second widget?

ResourcesHint Check Answer K Question 5 of 26 Consider the graph. According to the graph of the production possibilities frontier, what is the opportunity cost of the second widget? 10 O about 3 gizmos O less than 0.5 gizmos O about 2 widgets O about 7 widgets 0123 45 6789 10 What best explains the shape of the production possibility frontier in...

according to the graph of the production possibilities

frontier, what is the opportunity cost of the second widget?

ResourcesHint Check Answer K Question 5 of 26 Consider the graph. According to the graph of the production possibilities frontier, what is the opportunity cost of the second widget? 10 O about 3 gizmos O less than 0.5 gizmos O about 2 widgets O about 7 widgets 0123 45 6789 10 What best explains the shape of the production possibility frontier in...

2. Suppose So 4, sl (H) 8, si (T)-2 and the risk-free interest rate is r...

2. Suppose So 4, sl (H) 8, si (T)-2 and the risk-free interest rate is r 0, Som eone is willing to buy or sell European Call options with strike price k = 10 for the price Vó 2. Explain why there exists an arbitrage opportunity; ie construct a portfolio which starts with nothing, has a positive chance of earning money and zero probability of losing money.

2. Suppose So 4, sl (H) 8, si (T)-2 and the risk-free interest rate is r 0, Som eone is willing to buy or sell European Call options with strike price k = 10 for the price Vó 2. Explain why there exists an arbitrage opportunity; ie construct a portfolio which starts with nothing, has a positive chance of earning money and zero probability of losing money.

9. Suppose the firm's production function is given by f(K,L) min (K",L" (a) For what values...

9. Suppose the firm's production function is given by f(K,L) min (K",L" (a) For what values of a will the firm exhibit decreasing returns to scale? Constant returns to scale? Increasing returns to scale? (b) Derive the long-run cost function and the optimal input choices. (c) Suppose the capital is fixed at R = 10,000 and a =. Assuming that the firm wants to produce less than 100 units, derive 10. Consider the production function: f(K, L) = KLi. Let...

9. Suppose the firm's production function is given by f(K,L) min (K",L" (a) For what values of a will the firm exhibit decreasing returns to scale? Constant returns to scale? Increasing returns to scale? (b) Derive the long-run cost function and the optimal input choices. (c) Suppose the capital is fixed at R = 10,000 and a =. Assuming that the firm wants to produce less than 100 units, derive 10. Consider the production function: f(K, L) = KLi. Let...

( 8) Suppose that: p stock). The put option expires in 1 year. Is there an...

( 8) Suppose that: p stock). The put option expires in 1 year. Is there an arbitrage opportunity? $37, T- 1.0, r-5%, X - $39, D-0, (non-dividend-paying $1.50, So

( 8) Suppose that: p stock). The put option expires in 1 year. Is there an arbitrage opportunity? $37, T- 1.0, r-5%, X - $39, D-0, (non-dividend-paying $1.50, So

According to the graph of the production possibilities frontier, what is the opportunity cost of the...

According to the graph of the production possibilities frontier, what is the opportunity cost of the third widget? Consider the graph 10 O about 6 widgets O about 3 gizmos O about 7.5 widgets O about 0.5 gizmos 0 1 2 3. 4 5 6 7 8 9 10 Widgets What best explains the shape of the production possibility frontier in the graph? O This economy has the capacity to produce different combinations of widgets and gizmos O Some resources...

According to the graph of the production possibilities frontier, what is the opportunity cost of the third widget? Consider the graph 10 O about 6 widgets O about 3 gizmos O about 7.5 widgets O about 0.5 gizmos 0 1 2 3. 4 5 6 7 8 9 10 Widgets What best explains the shape of the production possibility frontier in the graph? O This economy has the capacity to produce different combinations of widgets and gizmos O Some resources...

3. Suppose that y E C" is defined so that y(k-1 for 0 k-1 and y(k-0...

3. Suppose that y E C" is defined so that y(k-1 for 0 k-1 and y(k-0 for 2 k n-1. Derive a formula for (z )(j) and describe qualitatively what the filter y does.

3. Suppose that y E C" is defined so that y(k-1 for 0 k-1 and y(k-0 for 2 k n-1. Derive a formula for (z )(j) and describe qualitatively what the filter y does.

Show work, thanks.

Let C(K) and P(K) be the call and the put premiums when the strike price is A 8. Suppose C(50) 16,C(55) 10 and P(50) 7, P(55) 14. What no-arbitrage property is violated? If so, demonstrate arbitrage

Show work, thanks.

Let C(K) and P(K) be the call and the put premiums when the strike price is A 8. Suppose C(50) 16,C(55) 10 and P(50) 7, P(55) 14. What no-arbitrage property is violated? If so, demonstrate arbitrage

the futures price for a contract deliverable in four months is 520. What arbitrage opportunities does this create? 8. (10 marks) The 6-month, 12-month, 18-month, and 24-month zero rates are 5%, 5.5%, 5.75%, and 6%, with semiannual compounding, (a) What are the rates with continuous compounding? (b) What is the forward rate for the 6-month period beginning in 18 months? (c) What is the value of an FRA that promises to pay you 6.5% (compounded semiannually) on a principal of...

the futures price for a contract deliverable in four months is 520. What arbitrage opportunities does this create? 8. (10 marks) The 6-month, 12-month, 18-month, and 24-month zero rates are 5%, 5.5%, 5.75%, and 6%, with semiannual compounding, (a) What are the rates with continuous compounding? (b) What is the forward rate for the 6-month period beginning in 18 months? (c) What is the value of an FRA that promises to pay you 6.5% (compounded semiannually) on a principal of...

2.2 Given: S(0)-50; r= 0.05, T-6 months; K = 49. What is a lower bound for an American Call Option on non-dividend paying stock? If an American Call option in the previous question (2.2) trades at $51, we have... O ANo arbitrage opportunities. O B An arbitrage opportunity by writing the call, buying the underlying stock and investing at a risk-free rate. O CAn arbitrage opportunity by writing the call and investing at a risk-free rate O D An arbitrage...

2.2 Given: S(0)-50; r= 0.05, T-6 months; K = 49. What is a lower bound for an American Call Option on non-dividend paying stock? If an American Call option in the previous question (2.2) trades at $51, we have... O ANo arbitrage opportunities. O B An arbitrage opportunity by writing the call, buying the underlying stock and investing at a risk-free rate. O CAn arbitrage opportunity by writing the call and investing at a risk-free rate O D An arbitrage...

according to the graph of the production possibilities

frontier, what is the opportunity cost of the second widget?

ResourcesHint Check Answer K Question 5 of 26 Consider the graph. According to the graph of the production possibilities frontier, what is the opportunity cost of the second widget? 10 O about 3 gizmos O less than 0.5 gizmos O about 2 widgets O about 7 widgets 0123 45 6789 10 What best explains the shape of the production possibility frontier in...

according to the graph of the production possibilities

frontier, what is the opportunity cost of the second widget?

ResourcesHint Check Answer K Question 5 of 26 Consider the graph. According to the graph of the production possibilities frontier, what is the opportunity cost of the second widget? 10 O about 3 gizmos O less than 0.5 gizmos O about 2 widgets O about 7 widgets 0123 45 6789 10 What best explains the shape of the production possibility frontier in...

2. Suppose So 4, sl (H) 8, si (T)-2 and the risk-free interest rate is r 0, Som eone is willing to buy or sell European Call options with strike price k = 10 for the price Vó 2. Explain why there exists an arbitrage opportunity; ie construct a portfolio which starts with nothing, has a positive chance of earning money and zero probability of losing money.

2. Suppose So 4, sl (H) 8, si (T)-2 and the risk-free interest rate is r 0, Som eone is willing to buy or sell European Call options with strike price k = 10 for the price Vó 2. Explain why there exists an arbitrage opportunity; ie construct a portfolio which starts with nothing, has a positive chance of earning money and zero probability of losing money.

9. Suppose the firm's production function is given by f(K,L) min (K",L" (a) For what values of a will the firm exhibit decreasing returns to scale? Constant returns to scale? Increasing returns to scale? (b) Derive the long-run cost function and the optimal input choices. (c) Suppose the capital is fixed at R = 10,000 and a =. Assuming that the firm wants to produce less than 100 units, derive 10. Consider the production function: f(K, L) = KLi. Let...

9. Suppose the firm's production function is given by f(K,L) min (K",L" (a) For what values of a will the firm exhibit decreasing returns to scale? Constant returns to scale? Increasing returns to scale? (b) Derive the long-run cost function and the optimal input choices. (c) Suppose the capital is fixed at R = 10,000 and a =. Assuming that the firm wants to produce less than 100 units, derive 10. Consider the production function: f(K, L) = KLi. Let...

( 8) Suppose that: p stock). The put option expires in 1 year. Is there an arbitrage opportunity? $37, T- 1.0, r-5%, X - $39, D-0, (non-dividend-paying $1.50, So

( 8) Suppose that: p stock). The put option expires in 1 year. Is there an arbitrage opportunity? $37, T- 1.0, r-5%, X - $39, D-0, (non-dividend-paying $1.50, So

According to the graph of the production possibilities frontier, what is the opportunity cost of the third widget? Consider the graph 10 O about 6 widgets O about 3 gizmos O about 7.5 widgets O about 0.5 gizmos 0 1 2 3. 4 5 6 7 8 9 10 Widgets What best explains the shape of the production possibility frontier in the graph? O This economy has the capacity to produce different combinations of widgets and gizmos O Some resources...

According to the graph of the production possibilities frontier, what is the opportunity cost of the third widget? Consider the graph 10 O about 6 widgets O about 3 gizmos O about 7.5 widgets O about 0.5 gizmos 0 1 2 3. 4 5 6 7 8 9 10 Widgets What best explains the shape of the production possibility frontier in the graph? O This economy has the capacity to produce different combinations of widgets and gizmos O Some resources...

3. Suppose that y E C" is defined so that y(k-1 for 0 k-1 and y(k-0 for 2 k n-1. Derive a formula for (z )(j) and describe qualitatively what the filter y does.

3. Suppose that y E C" is defined so that y(k-1 for 0 k-1 and y(k-0 for 2 k n-1. Derive a formula for (z )(j) and describe qualitatively what the filter y does.

Most questions answered within 3 hours.

-

Assume memory access is 10 units of time and disk access is

10000 units of time....

asked 10 minutes ago -

1. Are all good samples random?

2. Magazines often report surveys giving statistics such as “63%...

asked 31 minutes ago -

Under all the various types of market structures, firms

must eventually earn some economic profits for...

asked 18 minutes ago -

Consider the following fitness regime for a single locus trait

with two co-dominant alleles: w11 =...

asked 22 minutes ago -

A large cable company reports the following.

80% of its customers subscribe to its cable TV...

asked 38 minutes ago -

Please answer the question in brief.

Discuss the role of ERP in organizations. Are ERP tools...

asked 23 minutes ago -

Discuss the pros and cons of collaborative software such

as SameTime. Does it increase productivity? What...

asked 36 minutes ago -

Buying your in-laws a gift because it’s expected is

due to the ____________ motive of gift-giving....

asked 39 minutes ago -

Calculate the expected value, the variance, and the standard

deviation of the given random variable X....

asked 1 hour ago -

A hospital performs 100 surgeries per week. The probability that

complications after surgery occur is 10%....

asked 1 hour ago -

1 point) Given the significance level α=0.01 find the following:

(a) left-tailed z value z= (b)...

asked 1 hour ago -

Assuming you are the head of the software development unit at

Cyber.Soft, explain and justify why...

asked 46 minutes ago