Consider an industry with 7 identical competitive firms. The production function of a representat...

-

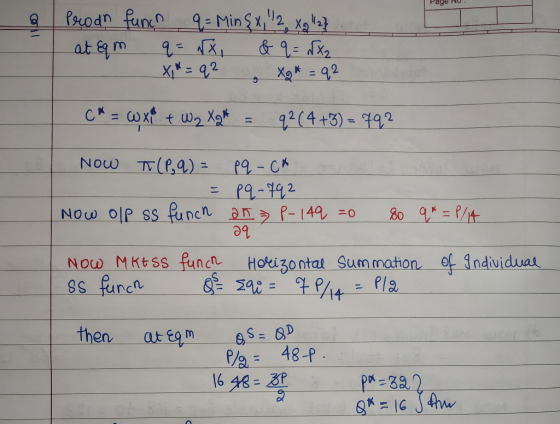

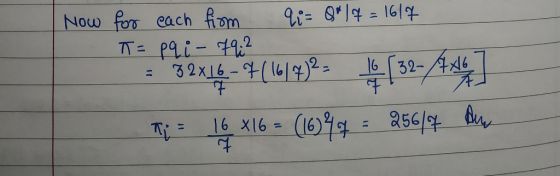

Consider an industry with 7 identical competitive firms. The production function of a representative firm is

q = min{√x1, √x2},

where x1 and x2 are the inputs that the firm uses to produce output q. Suppose that the input prices are w1 = 4 and w2 = 3. The demand function is q^D(p) = 48 − p. Assume that firms cannot enter or exit the market. Find the equilibrium price and quantity. Compute the profit of each firm.

Homework Answers

Add Answer to:

Consider an industry with 7 identical competitive firms. The production function of a representat...

Suppose there is a perfectly competitive industry where all the firms are identical with identical cost...

Suppose there is a perfectly competitive industry where all the firms are identical with identical cost curves. Furthermore, suppose that a representative firm’s total cost is given by the equation TC = 100 + q2 + q where q is the quantity of output produced by the firm. You also know that the market demand for this product is given by the equation P = 900 - 2Q where Q is the market quantity. In addition, you are told that...

2. A competitive industry has 12 identical firms, each one has a total variable cost function...

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

2. (1.5 p) Consider perfectly competitive industry with identical firms. The long run average cots function...

2. (1.5 p) Consider perfectly competitive industry with identical firms. The long run average cots function of a typical firm is given by AC(q)- 24 - 49 + q. Market demand is given by c p)=100-2p. (a) Find the long run supply curve of the typical firm. (b) Find the number of firms in the industry in the long run equilibrium.

2. (1.5 p) Consider perfectly competitive industry with identical firms. The long run average cots function of a typical firm is given by AC(q)- 24 - 49 + q. Market demand is given by c p)=100-2p. (a) Find the long run supply curve of the typical firm. (b) Find the number of firms in the industry in the long run equilibrium.

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q)...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q) = 4 +q? where q is the firm-specific level of production of the representative firm. The market demand function is Q(p) = 400 - 4p where Q(p) is the aggregate demand in the market (expressed as function of price) and p is the price a) Derive the firm-specific supply function of the representative firm as a function of price b) Assume there are N...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q) = 4 +q? where q is the firm-specific level of production of the representative firm. The market demand function is Q(p) = 400 - 4p where Q(p) is the aggregate demand in the market (expressed as function of price) and p is the price a) Derive the firm-specific supply function of the representative firm as a function of price b) Assume there are N...

Need as much details as possible. Microeconomics. A competitive industry consists of identical firms. Each firm...

Need as much details as possible. Microeconomics. A competitive industry consists of identical firms. Each firm has the long run total cost function TC(q)=18+½q2. If the market demand is Q(p)= 420 - p, what is the equilibrium quantity produced by each firm in the long run? a. 12 b. 18 c. 9 d. 6

1. (25 points) The market for study desks is characterized by perfect competition. Firms and consumers are price takers and in the long run there is free entry and exit of firms in this industry. Al...

1. (25 points) The market for study desks is characterized by perfect competition. Firms and consumers are price takers and in the long run there is free entry and exit of firms in this industry. All firms are identical in terms of their technological capabilities. Thus the cost function as given below for a representative firm can be assumed to function faced by each firm in the industry. The total cost and marginal cost functions t the representative firm are...

1. (25 points) The market for study desks is characterized by perfect competition. Firms and consumers are price takers and in the long run there is free entry and exit of firms in this industry. All firms are identical in terms of their technological capabilities. Thus the cost function as given below for a representative firm can be assumed to function faced by each firm in the industry. The total cost and marginal cost functions t the representative firm are...

1. Consider a competitive industry with a large number of firms, all of which have identical...

1. Consider a competitive industry with a large number of firms, all of which have identical cost functions c(y) = y^2 + 1. Suppose that initially the demand curve for this industry is given by D(p) = 52 - p: (The output of a firm does not have to be an integer number, but the number of firms does have to be an integer.) Answer part (c) through (e), and please show work? (c) What will be the equilibrium price?...

Question 27 A perfectly competitive industry is composed of 100 firms. Each firm has an identical...

Question 27 A perfectly competitive industry is composed of 100 firms. Each firm has an identical short-run marginal cost function SMC = 5+10q (where q is the firm's level of output). If Q denotes industry output, what is the short-run market supply curve for output? a) Q = -50 + 10p if p > 5 and 0 if p 5 5 α Q = -5 + TOP p if p > 5 and 0 if p < 5 + α...

Question 27 A perfectly competitive industry is composed of 100 firms. Each firm has an identical short-run marginal cost function SMC = 5+10q (where q is the firm's level of output). If Q denotes industry output, what is the short-run market supply curve for output? a) Q = -50 + 10p if p > 5 and 0 if p 5 5 α Q = -5 + TOP p if p > 5 and 0 if p < 5 + α...

Suppose that a firm has the production function (1) Draw an isoquant for f(x1,x2) = 10....

Suppose that a firm has the production function (1) Draw an isoquant for f(x1,x2) = 10. (5 points) (w1, w2) respec- (2) Suppose that the price of product is p, and that the prices of factors are tively. Find the factor demand function ri(w, w2, p), x1(w1, w2, P), the supply function y(w1, W2, P), and the profit function T(w1, w2, p). (10 points)

Suppose that a firm has the production function (1) Draw an isoquant for f(x1,x2) = 10....

Suppose that a firm has the production function (1) Draw an isoquant for f(x1,x2) = 10. (5 points) (w1, w2) respec- (2) Suppose that the price of product is p, and that the prices of factors are tively. Find the factor demand function ri(w, w2, p), x1(w1, w2, P), the supply function y(w1, W2, P), and the profit function T(w1, w2, p). (10 points)

Suppose that a firm has the production function (1) Draw an isoquant for f(x1,x2) = 10....

1.Consider an industry with only two firms that produce identical products. Each of the firms only...

1.Consider an industry with only two firms that produce identical products. Each of the firms only incurs a fixed cost of $1000 to produce and marginal cost is 20. The market demand function is as follows: Q=q1+q2=400-P a. Assuming that the firms form a cartel, calculate the profit-maximizing quantity of output, price and profits b. If the firms choose to behave as in the Cournot model, what would be the profit- maximizing quantities of output, price and profits? c. if...

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

2. (1.5 p) Consider perfectly competitive industry with identical firms. The long run average cots function of a typical firm is given by AC(q)- 24 - 49 + q. Market demand is given by c p)=100-2p. (a) Find the long run supply curve of the typical firm. (b) Find the number of firms in the industry in the long run equilibrium.

2. (1.5 p) Consider perfectly competitive industry with identical firms. The long run average cots function of a typical firm is given by AC(q)- 24 - 49 + q. Market demand is given by c p)=100-2p. (a) Find the long run supply curve of the typical firm. (b) Find the number of firms in the industry in the long run equilibrium.

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q) = 4 +q? where q is the firm-specific level of production of the representative firm. The market demand function is Q(p) = 400 - 4p where Q(p) is the aggregate demand in the market (expressed as function of price) and p is the price a) Derive the firm-specific supply function of the representative firm as a function of price b) Assume there are N...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q) = 4 +q? where q is the firm-specific level of production of the representative firm. The market demand function is Q(p) = 400 - 4p where Q(p) is the aggregate demand in the market (expressed as function of price) and p is the price a) Derive the firm-specific supply function of the representative firm as a function of price b) Assume there are N...

1. (25 points) The market for study desks is characterized by perfect competition. Firms and consumers are price takers and in the long run there is free entry and exit of firms in this industry. All firms are identical in terms of their technological capabilities. Thus the cost function as given below for a representative firm can be assumed to function faced by each firm in the industry. The total cost and marginal cost functions t the representative firm are...

1. (25 points) The market for study desks is characterized by perfect competition. Firms and consumers are price takers and in the long run there is free entry and exit of firms in this industry. All firms are identical in terms of their technological capabilities. Thus the cost function as given below for a representative firm can be assumed to function faced by each firm in the industry. The total cost and marginal cost functions t the representative firm are...

Question 27 A perfectly competitive industry is composed of 100 firms. Each firm has an identical short-run marginal cost function SMC = 5+10q (where q is the firm's level of output). If Q denotes industry output, what is the short-run market supply curve for output? a) Q = -50 + 10p if p > 5 and 0 if p 5 5 α Q = -5 + TOP p if p > 5 and 0 if p < 5 + α...

Question 27 A perfectly competitive industry is composed of 100 firms. Each firm has an identical short-run marginal cost function SMC = 5+10q (where q is the firm's level of output). If Q denotes industry output, what is the short-run market supply curve for output? a) Q = -50 + 10p if p > 5 and 0 if p 5 5 α Q = -5 + TOP p if p > 5 and 0 if p < 5 + α...

Suppose that a firm has the production function (1) Draw an isoquant for f(x1,x2) = 10. (5 points) (w1, w2) respec- (2) Suppose that the price of product is p, and that the prices of factors are tively. Find the factor demand function ri(w, w2, p), x1(w1, w2, P), the supply function y(w1, W2, P), and the profit function T(w1, w2, p). (10 points)

Suppose that a firm has the production function (1) Draw an isoquant for f(x1,x2) = 10....

Suppose that a firm has the production function (1) Draw an isoquant for f(x1,x2) = 10. (5 points) (w1, w2) respec- (2) Suppose that the price of product is p, and that the prices of factors are tively. Find the factor demand function ri(w, w2, p), x1(w1, w2, P), the supply function y(w1, W2, P), and the profit function T(w1, w2, p). (10 points)

Suppose that a firm has the production function (1) Draw an isoquant for f(x1,x2) = 10....

Most questions answered within 3 hours.

-

In Visual Basic 2017, Write a complete Main method that prints

Hello, world to the screen....

asked 52 seconds from now -

a) Find the pressure difference on an airplane wing if air flows

over the upper surface...

asked 5 minutes ago -

Write an assessment of the current business analysis of Hilton

Worldwide using Porters 5 Forces analysis.

asked 15 minutes ago -

i need help on this

Chapter 9 Section 3 Question 1:

Rudy puts this poster, with...

asked 24 minutes ago -

True or false Assembly x86

41. _____ The program counter is a pointer to the

instruction....

asked 25 minutes ago -

You have conducted an experiment to try to demonstrate that

growth factor receptor X protein (GFRX)...

asked 40 minutes ago -

The Gross Profit ratio for 2014 is 57.07%

Assume that Campbell's net sales for the first...

asked 39 minutes ago -

Thoroughly discuss the various current and proposed solutions to

anthropogenic influences resulting in Global Climate Change....

asked 44 minutes ago -

BLOG EXERCISE: You are writing a weekly intranet blog for the

CEO of a large Canadian...

asked 47 minutes ago -

calculate ΔGrxn at 36 ∘C. N2O4(g)→2NO2(g)

asked 47 minutes ago -

Present and Future Values of Single Cash Flows for Different

Periods

Find the following values, using...

asked 50 minutes ago -

Which types of mutations in DNA can lead to the translation of a

non-functional protein product?...

asked 49 minutes ago