y is output, pi is inflation, pi^e is expected inflation, i is interest rate

Homework Answers

a)

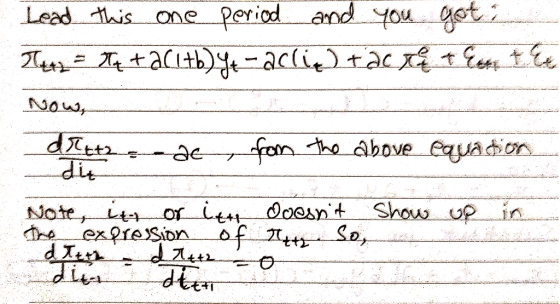

You can show this by showing that t period interest rate only t+2 period inflation. It doesn't influence t period or t+1 period inflation.

This way you show that t period inflation doesn't influence any t+i period inflation for i not equal to 2.

Now, we can write the Loss function as follows (by just opening the bracket):

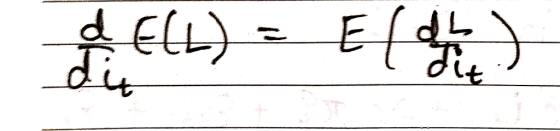

To minimize, you'll have to differentiate the loss function with respect to t period interest rate. By properties of expectations, you have:

To get your final result, just differentiate the loss function.

Notice something. The derivative all other terms except the one that has t+2 period inflation, when differentiated with respect to t period interest rate, become 0. So whether you minimize the whole loss function, or whether you minimize only that term of the loss function that has t+2 period inflation, it won't make a difference. Your final result will be the same. Hence, you can write the optimization problem with just the term corresponding to t+2 period inflation (as has been written in part a of the question).

b) The optimal interest rate ensures that

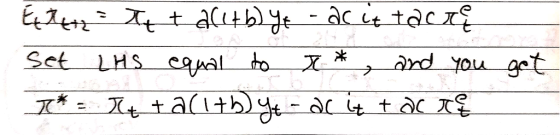

Now, look at the final solution for t+2 period inflation in part a. You had:

Take expectations on both sides, and you'll get:

A central bank knows all the all the terms in the RHS of the

expression for interest rate. This is because we've taken t period

expectations- that means they used all the information available

with them as of the end of period t. They know the actual inflation

at time t:

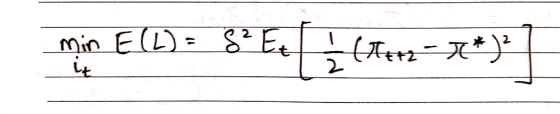

c) From part a) you found that the optimization problem can be written as follows:

Now just use basic calculus to minimize this expression with respect to t period interest rate.

The final expression shows that the solution to the optimization problem requires that the two period ahead forecast of inflation equal the inflation target.

Add Answer to:

y is output, pi is inflation, pi^e is expected inflation, i is interest rate Consider the dynamic IS-AS model presented by Svensson (1999) where all the symbols have the usual meaning. The monetar...

Most questions answered within 3 hours.

-

Using C++ :

A Pascals triangle row is constructed by looking at the previous

row and...

asked 3 minutes ago -

With what speed will the fastest photoelectrons be emitted from

a surface whose threshold wavelength is...

asked 3 minutes ago -

The following slope distances and differences in elevations

between the tape ends were recorded for a...

asked 4 minutes ago -

1. Assuming random walk markets and normally distributed

returns, if a one day VaR on an...

asked 14 minutes ago -

(a) With a variable life insurance policy, the rate of return on

the investment (the death...

asked 24 minutes ago -

By applying what you know about Grignard reagents and the

mechanism by which benzoic acid is...

asked 47 minutes ago -

For thermoplastics, explain the effects of increasing of each of

the following properties on a polymer’s...

asked 49 minutes ago -

Make a menu for the user to use in python 3 that can search and

replace...

asked 39 minutes ago -

1) An aqueous solution contains 0.280 M

NaHS and 0.128 M

H2S.

The pH of this...

asked 54 minutes ago -

Situational Leadership

is based on interplay of all of the following except:

The amount of guidance...

asked 55 minutes ago -

Consider the following problem: given n positive integers,

separate them into two groups such that adding...

asked 59 minutes ago -

Briefly discuss the following statements:

2.1 A partner never has the right to claim compensation for...

asked 1 hour ago