Homework Answers

Add Answer to:

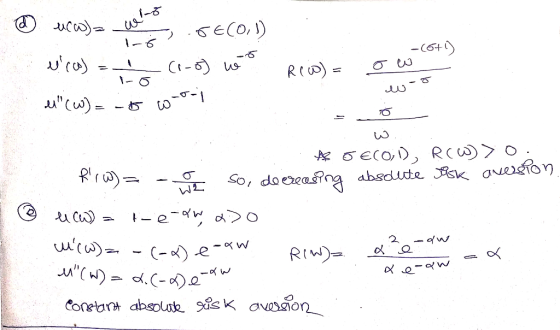

For each of the utility functions below, compute the Arrow-Pratt coefficients of risk-aversion. Say whether the utility...

Consider the utility function, defined for 1 = 0; w1-1-1 u(w) =- 1-) Compute the Arrow-Pratt...

Consider the utility function, defined for 1 = 0; w1-1-1 u(w) =- 1-) Compute the Arrow-Pratt coefficient of relative risk aversion for this func- tion.

Consider the utility function, defined for 1 = 0; w1-1-1 u(w) =- 1-) Compute the Arrow-Pratt coefficient of relative risk aversion for this func- tion.

(1) Ann has vNM utility u1 (x) = x, Bob has utility u2 (x) = √...

(1) Ann has vNM utility u1 (x) = x, Bob has utility u2 (x) = √ x and Carl has utility u3 (x) = x 3 . Who is risk neutral, risk averse and risk loving? (2) Consider the lottery P again. Find the dollar amount x such that each person is indifferent between the lottery P and $x (x is the certainty equivalent of P) (3) Calculate the Arrow-Pratt coefficients for everyone. How do they compare? Does this agree...

i) Suppose that Mary’s utility function is where W is wealth. Is she risk averse? Suppose...

i) Suppose that Mary’s utility function is where W is wealth. Is she risk averse? Suppose that Mary has initial wealth of $125,000. How much of a risk premium would she require to participate in a gamble that has a 50% probability of raising her wealth to $160,000 and a 50% probability of lowering her wealth to $90,000? ii) Suppose that Irma’s utility function with respect to wealth is U(W) = 100 + 80W − W2. Find her Arrow-Pratt risk...

1. For a utility function u(x) the measure of Absolute Risk Aversion is defined as Alca)...

1. For a utility function u(x) the measure of Absolute Risk Aversion is defined as Alca) = uchun Consider the utility function u(x)=1-e-axi where a is some positive parameter. Show that this utility function is for risk-averse consumer (concave utility/negative second derivative). Show that this utility function exhibits Constant Absolute Risk Aversion. Find the value of this constant.

1. For a utility function u(x) the measure of Absolute Risk Aversion is defined as Alca) = uchun Consider the utility function u(x)=1-e-axi where a is some positive parameter. Show that this utility function is for risk-averse consumer (concave utility/negative second derivative). Show that this utility function exhibits Constant Absolute Risk Aversion. Find the value of this constant.

Consider the utility function u(x) = ax + b e^cx where a, b, c are positive...

Consider the utility function u(x) = ax + b e^cx where a, b, c are positive scalars. (a) Compute the coefficient of absolute risk aversion. (b) Describe the risk attitude represented by u(x) and how it changes as x increases. (c) Write down the equations to determine the certainty equivalent and the risk premium of a gamble X for an individual with initial wealth w > 0. (d) What is the sign of the risk premium? How does the risk...

1. CRRA Utility Function: Constant relative risk aversion, or CRRA, utility function has been extensively used...

1. CRRA Utility Function: Constant relative risk aversion, or CRRA, utility function has been extensively used in macroeconomic analysis to represent consumer behavior. It takes the following general form u(x)- where σ is known as the curvature parameter. For the remainder of this question assume that σ>0. Assume that a representative household in a one-period model has the following preferences over consumption and leisure where l is leisure. The budget constraint is (in nominal terms) Pc nominal wage and n...

1. CRRA Utility Function: Constant relative risk aversion, or CRRA, utility function has been extensively used in macroeconomic analysis to represent consumer behavior. It takes the following general form u(x)- where σ is known as the curvature parameter. For the remainder of this question assume that σ>0. Assume that a representative household in a one-period model has the following preferences over consumption and leisure where l is leisure. The budget constraint is (in nominal terms) Pc nominal wage and n...

Problem Show that each of the follwing utility functions has a diminishing MRS but that they...

Problem Show that each of the follwing utility functions has a diminishing MRS but that they exhibit constant, increasing, and decreasing marginal utility, respectively. a) UE,y) = ry b) U(I,y) = rºy c) U(x,y) = ln I + Iny W Pyoblem A consumer is willing to trade 3 units of for 1 unit of y when she has 6 units of rand 5 units y. She is also willing to trade in 6 units of for 2 units of y...

Problem Show that each of the follwing utility functions has a diminishing MRS but that they exhibit constant, increasing, and decreasing marginal utility, respectively. a) UE,y) = ry b) U(I,y) = rºy c) U(x,y) = ln I + Iny W Pyoblem A consumer is willing to trade 3 units of for 1 unit of y when she has 6 units of rand 5 units y. She is also willing to trade in 6 units of for 2 units of y...

Problem 1 Consider the following two-period utility maximization problem. This utility function belongs to the CRRA...

Problem 1 Consider the following two-period utility maximization problem. This utility function belongs to the CRRA (Constant Relative Risk Aversion) class of functions which can be thought of as generalized logarithmic functions. An agent lives for two periods and in both receives some positive income. subject to +6+1 4+1 = 3+1 + (1 + r) ar+1 where a > 0,13 € (0, 1) and r>-1. (a) Rewrite the budget constraints into a single lifetime budget constraint and set up the...

Problem 1 Consider the following two-period utility maximization problem. This utility function belongs to the CRRA (Constant Relative Risk Aversion) class of functions which can be thought of as generalized logarithmic functions. An agent lives for two periods and in both receives some positive income. subject to +6+1 4+1 = 3+1 + (1 + r) ar+1 where a > 0,13 € (0, 1) and r>-1. (a) Rewrite the budget constraints into a single lifetime budget constraint and set up the...

1 [75 points; Chapter 5] You are to solve the consumer choice problem for three different...

1 [75 points; Chapter 5] You are to solve the consumer choice problem for three different consumers. Each consumer has $150 to spend (income) and faces prices Px = $2 and Py = $3 for goods X and Y. Consumers I, II, and III have utility functions U'(X, Y) = X? + Y, U"(X, Y) = X12 + Yl2, and UTM(X, Y) = X´Y, respectively. For each consumer, do the following steps. a [15 points] Carefully express the consumer's choice...

1 [75 points; Chapter 5] You are to solve the consumer choice problem for three different consumers. Each consumer has $150 to spend (income) and faces prices Px = $2 and Py = $3 for goods X and Y. Consumers I, II, and III have utility functions U'(X, Y) = X? + Y, U"(X, Y) = X12 + Yl2, and UTM(X, Y) = X´Y, respectively. For each consumer, do the following steps. a [15 points] Carefully express the consumer's choice...

Consider the utility function, defined for 1 = 0; w1-1-1 u(w) =- 1-) Compute the Arrow-Pratt coefficient of relative risk aversion for this func- tion.

Consider the utility function, defined for 1 = 0; w1-1-1 u(w) =- 1-) Compute the Arrow-Pratt coefficient of relative risk aversion for this func- tion.

1. For a utility function u(x) the measure of Absolute Risk Aversion is defined as Alca) = uchun Consider the utility function u(x)=1-e-axi where a is some positive parameter. Show that this utility function is for risk-averse consumer (concave utility/negative second derivative). Show that this utility function exhibits Constant Absolute Risk Aversion. Find the value of this constant.

1. For a utility function u(x) the measure of Absolute Risk Aversion is defined as Alca) = uchun Consider the utility function u(x)=1-e-axi where a is some positive parameter. Show that this utility function is for risk-averse consumer (concave utility/negative second derivative). Show that this utility function exhibits Constant Absolute Risk Aversion. Find the value of this constant.

1. CRRA Utility Function: Constant relative risk aversion, or CRRA, utility function has been extensively used in macroeconomic analysis to represent consumer behavior. It takes the following general form u(x)- where σ is known as the curvature parameter. For the remainder of this question assume that σ>0. Assume that a representative household in a one-period model has the following preferences over consumption and leisure where l is leisure. The budget constraint is (in nominal terms) Pc nominal wage and n...

1. CRRA Utility Function: Constant relative risk aversion, or CRRA, utility function has been extensively used in macroeconomic analysis to represent consumer behavior. It takes the following general form u(x)- where σ is known as the curvature parameter. For the remainder of this question assume that σ>0. Assume that a representative household in a one-period model has the following preferences over consumption and leisure where l is leisure. The budget constraint is (in nominal terms) Pc nominal wage and n...

Problem Show that each of the follwing utility functions has a diminishing MRS but that they exhibit constant, increasing, and decreasing marginal utility, respectively. a) UE,y) = ry b) U(I,y) = rºy c) U(x,y) = ln I + Iny W Pyoblem A consumer is willing to trade 3 units of for 1 unit of y when she has 6 units of rand 5 units y. She is also willing to trade in 6 units of for 2 units of y...

Problem Show that each of the follwing utility functions has a diminishing MRS but that they exhibit constant, increasing, and decreasing marginal utility, respectively. a) UE,y) = ry b) U(I,y) = rºy c) U(x,y) = ln I + Iny W Pyoblem A consumer is willing to trade 3 units of for 1 unit of y when she has 6 units of rand 5 units y. She is also willing to trade in 6 units of for 2 units of y...

Problem 1 Consider the following two-period utility maximization problem. This utility function belongs to the CRRA (Constant Relative Risk Aversion) class of functions which can be thought of as generalized logarithmic functions. An agent lives for two periods and in both receives some positive income. subject to +6+1 4+1 = 3+1 + (1 + r) ar+1 where a > 0,13 € (0, 1) and r>-1. (a) Rewrite the budget constraints into a single lifetime budget constraint and set up the...

Problem 1 Consider the following two-period utility maximization problem. This utility function belongs to the CRRA (Constant Relative Risk Aversion) class of functions which can be thought of as generalized logarithmic functions. An agent lives for two periods and in both receives some positive income. subject to +6+1 4+1 = 3+1 + (1 + r) ar+1 where a > 0,13 € (0, 1) and r>-1. (a) Rewrite the budget constraints into a single lifetime budget constraint and set up the...

1 [75 points; Chapter 5] You are to solve the consumer choice problem for three different consumers. Each consumer has $150 to spend (income) and faces prices Px = $2 and Py = $3 for goods X and Y. Consumers I, II, and III have utility functions U'(X, Y) = X? + Y, U"(X, Y) = X12 + Yl2, and UTM(X, Y) = X´Y, respectively. For each consumer, do the following steps. a [15 points] Carefully express the consumer's choice...

1 [75 points; Chapter 5] You are to solve the consumer choice problem for three different consumers. Each consumer has $150 to spend (income) and faces prices Px = $2 and Py = $3 for goods X and Y. Consumers I, II, and III have utility functions U'(X, Y) = X? + Y, U"(X, Y) = X12 + Yl2, and UTM(X, Y) = X´Y, respectively. For each consumer, do the following steps. a [15 points] Carefully express the consumer's choice...

Most questions answered within 3 hours.

-

For Dijkstra’s shortest path algorithm:

a. Give the Big-O time for Dijkstra’s shortest path algorithm

and...

asked 6 minutes ago -

Phosphorus violates the 'octet rule' in biological molecules,

forming more covalent bonds than expected based on...

asked 9 minutes ago -

A 1.3 eV electron has a 10-4 probability of tunneling

through a 2.4 eV potential barrier....

asked 27 minutes ago -

What is the one ingredient that is common to being successful

with all stakeholders?

profit

trust...

asked 26 minutes ago -

Write an assembly language 32 bit program that reads in lines of

text by a .txt...

asked 29 minutes ago -

what is the density ( in g/L) of hydrogen gas at 29 degrees C and a...

asked 37 minutes ago -

5-6. You are considering three investment alternatives for some

spare cash: Old Reliable Corporation stock (A1),...

asked 29 minutes ago -

Problem 16-02

Receivables Investment

Medwig Corporation has a DSO of 45 days. The company averages

$7,250...

asked 44 minutes ago -

Mr. Brown hired Lowe's Maintenance Services Limited to repair

and paint the exterior wall of his...

asked 45 minutes ago -

When might an index slow down the overall performance of the

database? Choose the best answer....

asked 50 minutes ago -

Due to a recession, expected inflation this year is only 2.25%.

However, the inflation rate in...

asked 51 minutes ago -

Write four functions: (IN PYTHON 3)

1) bound(l) - given a list of integers l, compute...

asked 53 minutes ago