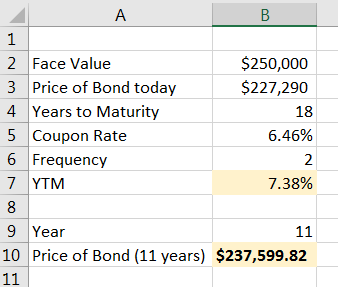

An 18-year semi-annual coupon bond has a face value of $250,000 and coupon rate of 6.46 percent. The price of the bond i...

An 18-year semi-annual coupon bond has a face value of $250,000 and coupon rate of 6.46 percent. The price of the bond is $227,290. If the yield to maturity of this bond does not change during the life of the bond, what will its price be 11 years from today?

Homework Answers

Add Answer to:

An 18-year semi-annual coupon bond has a face value of $250,000 and coupon rate of 6.46 percent. The price of the bond i...

A semi-annual coupon bond has a 6 percent coupon rate, a $1,000 face value, a current...

A semi-annual coupon bond has a 6 percent coupon rate, a $1,000 face value, a current value of $1,036.09, and 3 years until the first call date. What is the call price if the yield to call is 6.5 percent? A STRIPS has a yield to maturity of 6.2 percent, a par value of $25,000, and a time to maturity of 10 years. What is the price

Bond A is a semi-annual coupon bond that has a face value of $1000, a 10% coupon rate

Bond A is a semi-annual coupon bond that has a face value of $1000, a 10% coupon rate, a five year maturity, and a yield to maturity of 7%. At the maturity date, how much payment should the bond investor expect from the bond? (a) $50 (b) $100 (c) $1035 (d) $1050

A T-bond with semi-annual coupons has a coupon rate of 3%, face value of $1,000, and...

A T-bond with semi-annual coupons has a coupon rate of 3%, face value of $1,000, and 2 years to maturity. If its yield to maturity is 4%, what is its Macaulay Duration? Answer in years, rounded to three decimal places

A semi-annual bond has the following characteristics: Face value = Ksh 1,000 Coupon rate = 10%...

A semi-annual bond has the following characteristics: Face value = Ksh 1,000 Coupon rate = 10% per annum Time remaining till maturity = 15 years Bond price = Ksh 880 Required: From the characteristics given state the type of bond and why Estimate the yield to maturity for the bond

A 5.5%, 5-year bond with semi-annual coupon payments and a face value of $1,000 has a...

A 5.5%, 5-year bond with semi-annual coupon payments and a face value of $1,000 has a market price of $1,032.19. Assume that the next coupon payment is exactly six months away. a) What is the yield-to-maturity of the bond? b) What is the effective annual rate implied by this price?

A coupon bond with a face value of $1200 that pays an annual coupon of $400...

A coupon bond with a face value of $1200 that pays an annual coupon of $400 has a coupon rate equal to ? What is the approximate (closest whole number) yield to maturity on a coupon bond that matures one year from today, has a par value of $1010, pays an annual coupon of $75, and whose price today is $1004.50? A. 7% B. 4% C. 8% D 6% E. 5% If the yield to maturity on a bond exceeds...

A five-year 2.4% defaultable coupon bond is selling to yield 3% (Annual Percent Rate and semi-annual...

A five-year 2.4% defaultable coupon bond is selling to yield 3% (Annual Percent Rate and semi-annual compounding). The bond pays interest semi-annually. The risk-free yield is 2.4%. Therefore, its current credit spread is 3% -2.4% = 0.6%. Two years later its credit spread increases from 0.6% to 1% while the risk-free yield doesn’t change. Assuming the face value of the coupon bond and risk-free bond is 100. a)What is the return of investing in this bond over the two year?...

ABC issued 12-year bonds at a coupon rate of 8% with semi-annual payments. If the bond...

ABC issued 12-year bonds at a coupon rate of 8% with semi-annual payments. If the bond currently sells for $1050 of par value, what is the YTM? ABC issued 12-year bonds 2 years ago at a coupon rate of 8% with semi-annual payments. If the bond currently sells for 105% of par value, what is the YTM? A bond has a quoted price of $1,080.42. It has a face value of $1000, a semi-annual coupon of $30, and a maturity...

Today, a bond has a coupon rate of 8.86 percent, par value of 1,000 dollars, YTM...

Today, a bond has a coupon rate of 8.86 percent, par value of 1,000 dollars, YTM of 9.46 percent, and semi-annual coupons with the next coupon due in 6 months. One year ago, the bond's price was 1,069.83 dollars and the bond had 11 years until maturity. What is the current yield of the bond today? Answer as a rate in decimal format so that 12.34% would be entered as.1234 and 0.98% would be entered as .0098. Number One year...

Today, a bond has a coupon rate of 8.86 percent, par value of 1,000 dollars, YTM of 9.46 percent, and semi-annual coupons with the next coupon due in 6 months. One year ago, the bond's price was 1,069.83 dollars and the bond had 11 years until maturity. What is the current yield of the bond today? Answer as a rate in decimal format so that 12.34% would be entered as.1234 and 0.98% would be entered as .0098. Number One year...

A five-year 2.4% defaultable coupon bond is selling to yield 3% (Annual Percent Rate and semi-annual...

A five-year 2.4% defaultable coupon bond is selling to yield 3% (Annual Percent Rate and semi-annual compounding). The bond pays interest semi-annually. The risk-free yield is 2.4%. Therefore, its current credit spread is 3% -2.4% = 0.6%. Two years later its credit spread increases from 0.6% to 1% while the risk-free yield doesn’t change. Assuming the face value of the coupon bond and risk-free bond is 100. a)What is the return of investing in this bond over the two year?

Today, a bond has a coupon rate of 8.86 percent, par value of 1,000 dollars, YTM of 9.46 percent, and semi-annual coupons with the next coupon due in 6 months. One year ago, the bond's price was 1,069.83 dollars and the bond had 11 years until maturity. What is the current yield of the bond today? Answer as a rate in decimal format so that 12.34% would be entered as.1234 and 0.98% would be entered as .0098. Number One year...

Today, a bond has a coupon rate of 8.86 percent, par value of 1,000 dollars, YTM of 9.46 percent, and semi-annual coupons with the next coupon due in 6 months. One year ago, the bond's price was 1,069.83 dollars and the bond had 11 years until maturity. What is the current yield of the bond today? Answer as a rate in decimal format so that 12.34% would be entered as.1234 and 0.98% would be entered as .0098. Number One year...

Most questions answered within 3 hours.

-

Imagine you are driving around a horizontal circular track (such

as a roundabout at an intersection...

asked 5 minutes ago -

Draw the structures that correspond to the following names.

Correct any names that are not in...

asked 14 minutes ago -

Do elephants and cows present an interesting dichotomy when

viewed from the perspective of property rights?

asked 25 minutes ago -

USE an API

You have a drop down list of 4 cities.

Upon selecting a particular...

asked 25 minutes ago -

Which type of chemical reaction is regulated by altering an

enzyme's function?

a.) irreversible

b.) reversible

asked 29 minutes ago -

Supply management is a developing ____________ and an area of

management _______________.

1. discipline / responsibility...

asked 32 minutes ago -

Calculate the mass of acetic acid that must be mixed with

0.88moles of sodium acetate to...

asked 32 minutes ago -

Crown Corporation, a United States Company, made a sale to a

foreign customer on

September 15,...

asked 34 minutes ago -

The complete combustion of acetic acid, HC2H3O2(l) to form

H2O(l) and CO2(g) at constant pressure releases...

asked 46 minutes ago -

What is the effect of using MACRS rather than straight-line

depreciation?

It increases the NPV.

The...

asked 44 minutes ago -

Write a program to create a game map. A game map is a 2D array

of...

asked 53 minutes ago -

2. When a student ran an asymmetric dihydroxylation reaction

using cis-stilbene and the ligand (DHQ)2PHAL, the...

asked 52 minutes ago