Homework Answers

SEE THE IMAGE. ANY DOUBTS, FEEL FREE TO ASK. THUMBS UP

PLEASE

Add Answer to:

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term gove...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 7%. The probability distribution of the risky funds is as follows: Expected Return Standard Deviation Stock fund (S) 18 % 35 % Bond fund (B) 15 20 The correlation between the fund returns is 0.12. What is the Sharpe ratio of...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 7%. The probability distribution of the risky funds is as follows: Expected Return Standard Deviation Stock fund (S) 18 % 35 % Bond fund (B) 15 20 The correlation between the fund returns is 0.12. What is the Sharpe ratio of...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 6%. The probability distribution of the risky funds is as follows: Expected Return Standard Deviation Stock fund (S) 17 % 38 % Bond fund (B) 12 17 The correlation between the fund returns is 0.13. What is the Sharpe ratio of...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 5%. The probability distribution of the risky funds is as follows: Expected Return 19% 12 Standard Deviation 32% 15 Stock fund (5) Bond fund (B) The correlation between the fund returns is 0.11. What is the Sharpe ratio of the best...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 5%. The probability distribution of the risky funds is as follows: Expected Return 19% 12 Standard Deviation 32% 15 Stock fund (5) Bond fund (B) The correlation between the fund returns is 0.11. What is the Sharpe ratio of the best...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 6%. The probability distribution of the risky funds is as follows: Expected Return Standard Deviation Stock fund (S) 16 % 35 % Bond fund (B) 12 15 The correlation between the fund returns is 0.13. What is the Sharpe ratio of...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 6%. The probability distribution of the risky funds is as follows: Expected Return Standard Deviation Stock fund (S) 17 % 38 % Bond fund (B) 12 17 The correlation between the fund returns is 0.13. What is the Sharpe ratio of...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4%. The probability distribution of the risky funds is as follows: Expected Return 24% 12 Standard Deviation 30% Stock fund (S) Bond fund (B) 19 The correlation between the fund returns is 0.13. What is the Sharpe ratio of the best...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4%. The probability distribution of the risky funds is as follows: Expected Return 24% 12 Standard Deviation 30% Stock fund (S) Bond fund (B) 19 The correlation between the fund returns is 0.13. What is the Sharpe ratio of the best...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4%. The probability distribution of the risky funds is as follows: 10 points Expected Return 24% 12 Standard Deviation 30% 19 Stock fund (S) Bond fund (B) eBook The correlation between the fund returns is 0.13. What is the Sharpe ratio...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4%. The probability distribution of the risky funds is as follows: 10 points Expected Return 24% 12 Standard Deviation 30% 19 Stock fund (S) Bond fund (B) eBook The correlation between the fund returns is 0.13. What is the Sharpe ratio...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.2%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) 12% 33% Bond fund (B) 5% 26% The correlation between the fund returns is 0.0308. What is the Sharpe ratio of the best feasible...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

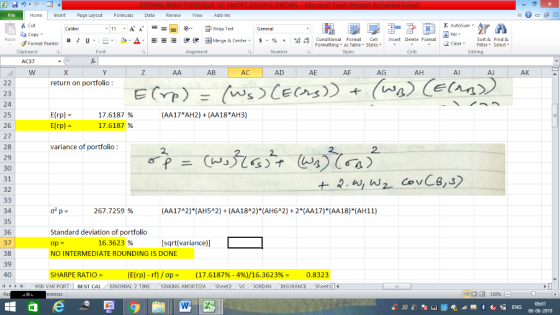

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 5%. The probability distribution of the risky funds is as follows: Expected Return Standard Deviation Stock fund (S) 19 % 32 % Bond fund (B) 12 15 The correlation between the fund returns is 0.11. What is the Sharpe ratio of...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 5%. The probability distribution of the risky funds is as follows: Expected Return 19% 12 Standard Deviation 32% 15 Stock fund (5) Bond fund (B) The correlation between the fund returns is 0.11. What is the Sharpe ratio of the best...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 5%. The probability distribution of the risky funds is as follows: Expected Return 19% 12 Standard Deviation 32% 15 Stock fund (5) Bond fund (B) The correlation between the fund returns is 0.11. What is the Sharpe ratio of the best...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4%. The probability distribution of the risky funds is as follows: Expected Return 24% 12 Standard Deviation 30% Stock fund (S) Bond fund (B) 19 The correlation between the fund returns is 0.13. What is the Sharpe ratio of the best...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4%. The probability distribution of the risky funds is as follows: Expected Return 24% 12 Standard Deviation 30% Stock fund (S) Bond fund (B) 19 The correlation between the fund returns is 0.13. What is the Sharpe ratio of the best...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4%. The probability distribution of the risky funds is as follows: 10 points Expected Return 24% 12 Standard Deviation 30% 19 Stock fund (S) Bond fund (B) eBook The correlation between the fund returns is 0.13. What is the Sharpe ratio...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4%. The probability distribution of the risky funds is as follows: 10 points Expected Return 24% 12 Standard Deviation 30% 19 Stock fund (S) Bond fund (B) eBook The correlation between the fund returns is 0.13. What is the Sharpe ratio...

Most questions answered within 3 hours.

-

Python Program: Design the logic for and implement a program

that merges the two files into...

asked 8 minutes ago -

Human relations refer to the way a company arranges people,

jobs, and communications so that work...

asked 10 minutes ago -

The specific radiocarbon activity of a sample of wood is 6.25

gms dpm/gm of carbon. The...

asked 13 minutes ago -

An aqueous magnesium chloride solution is made by dissolving

6.96 moles of MgCl2 in sufficient water...

asked 16 minutes ago -

Ken believes the average age of men who come to get a haircut at

his barber...

asked 38 minutes ago -

(Ratio Analysis): Last year Co. XYZ had sales of $ 400,000, with

“cost of goods sold”...

asked 46 minutes ago -

can someone please write the balanced chemical

equation for the synthesis of Bromoacetanilide

from;

aniline +...

asked 43 minutes ago -

1. If a corporation purchases land and building and subsequently

tears down the building and uses...

asked 54 minutes ago -

Consider a 23-year bond with 7 percent annual coupon payments.

The market rate (YTM) is 6.4...

asked 57 minutes ago -

a tuba creates a 4th harmonic of frequency 116.5 Hz. what is the

frequency of the...

asked 1 hour ago -

A coconut mass 2kg falls from a 30m tall tree. The coconut falls

and comes to...

asked 1 hour ago -

Group Policies

Research GROUP POLICY OBJECTS (GPO'S)

You can start in the Windows Server 2012 eBook...

asked 1 hour ago