Homework Answers

Add Answer to:

The random variables X1, X2, - .. are independent and identically distributed with common pdf 0...

Question 4 15 marks] The random variables X1, ... , Xn random variables with common pdf...

Question 4 15 marks] The random variables X1, ... , Xn random variables with common pdf independent and identically distributed are 0 E fx (x;01) 0 independent of the random variables Y^,..., Y, which and are indepen are dent and identically distributed random variables with common pdf 0 fy (y; 02) 0 (a) Show that the MLE8 of 01 and 02 are 1 = X i=1 Y (b) Show that the MLE of 0 when 01 = 0, = 0...

Question 4 15 marks] The random variables X1, ... , Xn random variables with common pdf independent and identically distributed are 0 E fx (x;01) 0 independent of the random variables Y^,..., Y, which and are indepen are dent and identically distributed random variables with common pdf 0 fy (y; 02) 0 (a) Show that the MLE8 of 01 and 02 are 1 = X i=1 Y (b) Show that the MLE of 0 when 01 = 0, = 0...

Question 4 [15 marks] The random variables X1,... , Xn are independent and identically distributed with...

Question 4 [15 marks] The random variables X1,... , Xn are independent and identically distributed with probability function Px (1 -px)1 1-2 -{ 0,1 fx (x) ; otherwise, 0 while the random variables Yı,...,Yn are independent and identically dis- tributed with probability function = { p¥ (1 - py) y 0,1,2 ; otherwise fy (y) 0 where px and py are between 0 and 1 (a) Show that the MLEs of px and py are Xi, n PY 2n (b)...

Question 4 [15 marks] The random variables X1,... , Xn are independent and identically distributed with probability function Px (1 -px)1 1-2 -{ 0,1 fx (x) ; otherwise, 0 while the random variables Yı,...,Yn are independent and identically dis- tributed with probability function = { p¥ (1 - py) y 0,1,2 ; otherwise fy (y) 0 where px and py are between 0 and 1 (a) Show that the MLEs of px and py are Xi, n PY 2n (b)...

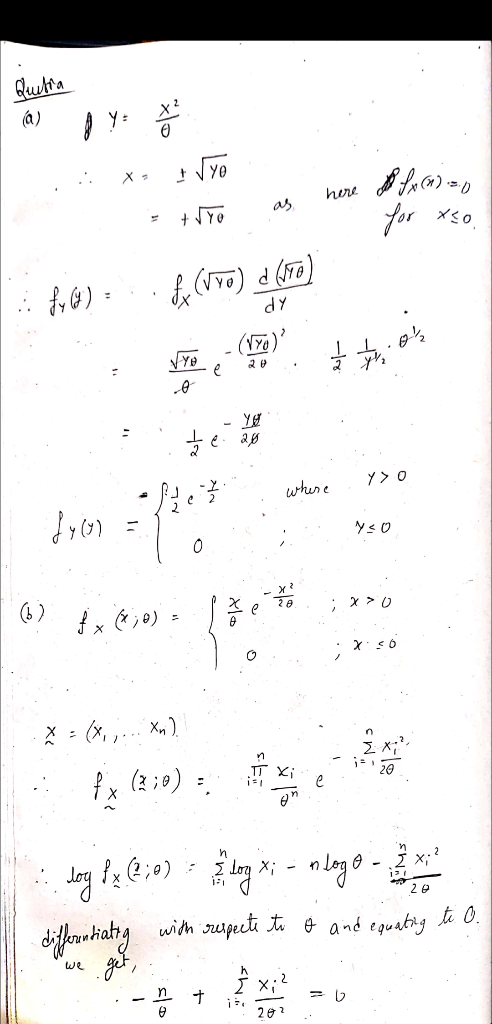

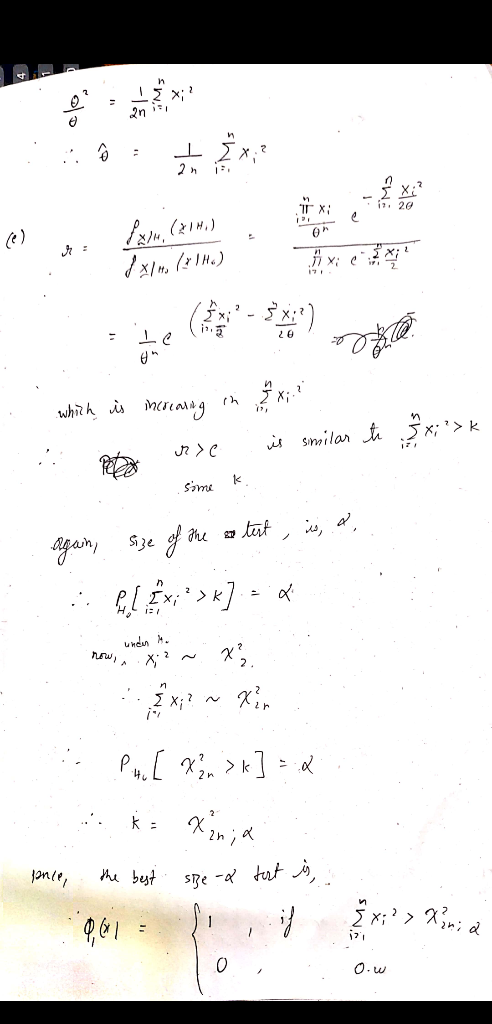

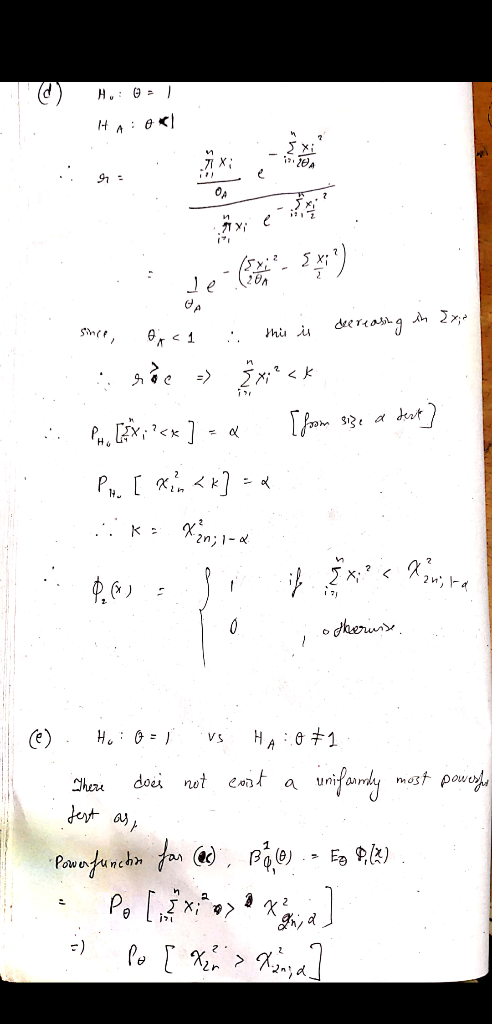

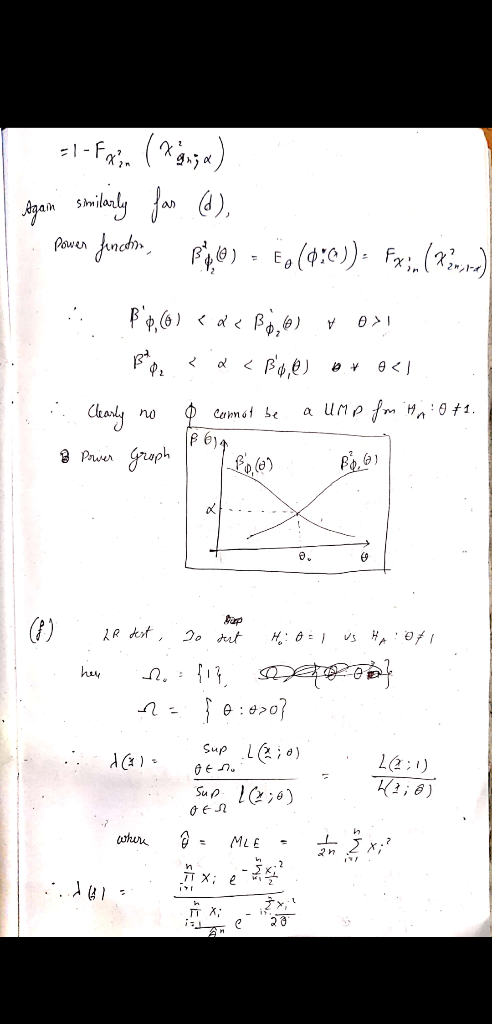

Question 3 15 marks] Let X1,..,X be independent identically distributed random variables with pdf common )...

Question 3 15 marks] Let X1,..,X be independent identically distributed random variables with pdf common ) = { (#)%2-1/64 0 fx (a;e) 0 where 0 >0 is an unknown parameter X-1. Show that Y ~ T (}, ); (a) Let Y (b) Show that 1 T n =1 is an unbiased estimator of 0-1 ewhere / (0; X) is the log- likeliho od function; (c) Compute U - (d) What functions T (0) have unbiased estimators that attain the relevant...

Question 3 15 marks] Let X1,..,X be independent identically distributed random variables with pdf common ) = { (#)%2-1/64 0 fx (a;e) 0 where 0 >0 is an unknown parameter X-1. Show that Y ~ T (}, ); (a) Let Y (b) Show that 1 T n =1 is an unbiased estimator of 0-1 ewhere / (0; X) is the log- likeliho od function; (c) Compute U - (d) What functions T (0) have unbiased estimators that attain the relevant...

13. Let X1, X2, ...,Xy be a sequence of independent and identically distributed discrete random variables,...

13. Let X1, X2, ...,Xy be a sequence of independent and identically distributed discrete random variables, each with probability mass function P(X = k)=,, for k = 0,1,2,3,.... emak (a) Find the expected value and the variance of the sample mean as = N&i=1X,. (b) Find the probability mass function of X. (c) Find an approximate pdf of X when N is very large (N −0).

13. Let X1, X2, ...,Xy be a sequence of independent and identically distributed discrete random variables, each with probability mass function P(X = k)=,, for k = 0,1,2,3,.... emak (a) Find the expected value and the variance of the sample mean as = N&i=1X,. (b) Find the probability mass function of X. (c) Find an approximate pdf of X when N is very large (N −0).

Consider n independent and identically distributed random variables X1,X2, following a uniform distribution on the interval...

Consider n independent and identically distributed random variables X1,X2, following a uniform distribution on the interval [0,1] ,Xn, each a) What is the pdf of Mmin(X1,X2, .. ,Xn)? b) Give the expectation and variance of XX 1-1лі.

Consider n independent and identically distributed random variables X1,X2, following a uniform distribution on the interval [0,1] ,Xn, each a) What is the pdf of Mmin(X1,X2, .. ,Xn)? b) Give the expectation and variance of XX 1-1лі.

Let X1 and X2 be independent random variables so X1~ N(u,1) and X2 N(u,4) Where u...

Let X1 and X2 be independent random variables so X1~ N(u,1) and X2 N(u,4) Where u R a) Show that the likelihood for , given that X1 = x1 and X2 = xz is 8 4T b) Show, that the maxium likelihood estimate for u is 4x1+ x2 и (х, х2) e) Show that СтN -("x"x) .я d) and enter a formula for the 95% confidence interval for

Let X1 and X2 be independent random variables so X1~ N(u,1) and...

Let X1 and X2 be independent random variables so X1~ N(u,1) and X2 N(u,4) Where u R a) Show that the likelihood for , given that X1 = x1 and X2 = xz is 8 4T b) Show, that the maxium likelihood estimate for u is 4x1+ x2 и (х, х2) e) Show that СтN -("x"x) .я d) and enter a formula for the 95% confidence interval for

Let X1 and X2 be independent random variables so X1~ N(u,1) and...

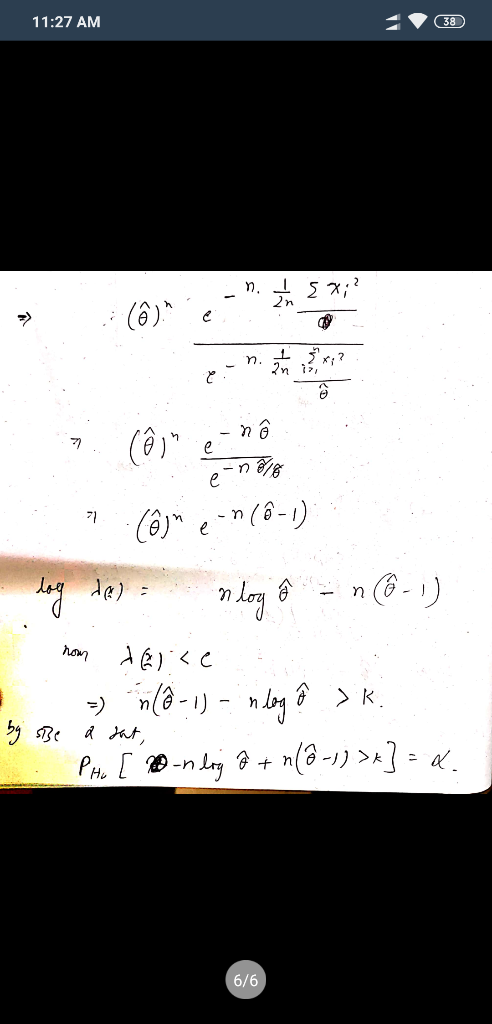

Suppose n independent, identically distributed observations are drawn from an exponential () distribution, with pdf given...

Suppose n independent, identically distributed observations are

drawn from an exponential ()

distribution, with pdf given by f(x,)=,

0 < x <

.

The data are x1, x2, .. , xn

Construct a likelihood ratio hypothesis test of Ho :

vs H1:

(where

and

are known constants, with

), where the critical value is taken to be a constant c

We were unable to transcribe this imageWe were unable to transcribe this imageWe were unable to transcribe this imageWe were...

Suppose n independent, identically distributed observations are

drawn from an exponential ()

distribution, with pdf given by f(x,)=,

0 < x <

.

The data are x1, x2, .. , xn

Construct a likelihood ratio hypothesis test of Ho :

vs H1:

(where

and

are known constants, with

), where the critical value is taken to be a constant c

We were unable to transcribe this imageWe were unable to transcribe this imageWe were unable to transcribe this imageWe were...

3. Let {X1, X2, X3, X4} be independent, identically distributed random variables with p.d.f. f(0) =...

3. Let {X1, X2, X3, X4} be independent, identically distributed random variables with p.d.f. f(0) = 2. o if 0<x< 1 else Find EY] where Y = min{X1, X2, X3, X4}.

3. Let {X1, X2, X3, X4} be independent, identically distributed random variables with p.d.f. f(0) = 2. o if 0<x< 1 else Find EY] where Y = min{X1, X2, X3, X4}.

Question 6 [15 marks] Let X1, X2,..., Xn be independent and identically distributed random vari- ables...

Question 6 [15 marks] Let X1, X2,..., Xn be independent and identically distributed random vari- ables with common probability function ()p(1-p) m m-a ; x 0,1,. ., m otherwise 0 where m is known and p is unknown (a) Obtain the Sequential Probability Ratio Test of Ho p = po versus HA p P, where pi > po, with significance level 0.01 and power 0.95. Describe the test precisely; (b) For the case where po 3/8,pı = 1/2, m =...

Question 6 [15 marks] Let X1, X2,..., Xn be independent and identically distributed random vari- ables with common probability function ()p(1-p) m m-a ; x 0,1,. ., m otherwise 0 where m is known and p is unknown (a) Obtain the Sequential Probability Ratio Test of Ho p = po versus HA p P, where pi > po, with significance level 0.01 and power 0.95. Describe the test precisely; (b) For the case where po 3/8,pı = 1/2, m =...

3. Suppose X1, X2, -- are independent identically distributed random variables with mean 0 and va...

3. Suppose X1, X2, -- are independent identically distributed random variables with mean 0 and variance 1.Let Sn denote the partial sum Let Fn denote the information contained in Xi, .X,. Suppoe m n. (1) Compute El(Sn Sm)lFm (2) Compute ESm(Sn Sm)|F (3) Compute ES|]. (Hint: Write S (4) Verify that S -n is a martingale. [Sm(Sn Sm))2)

3. Suppose X1, X2, -- are independent identically distributed random variables with mean 0 and variance 1.Let Sn denote the partial sum...

3. Suppose X1, X2, -- are independent identically distributed random variables with mean 0 and variance 1.Let Sn denote the partial sum Let Fn denote the information contained in Xi, .X,. Suppoe m n. (1) Compute El(Sn Sm)lFm (2) Compute ESm(Sn Sm)|F (3) Compute ES|]. (Hint: Write S (4) Verify that S -n is a martingale. [Sm(Sn Sm))2)

3. Suppose X1, X2, -- are independent identically distributed random variables with mean 0 and variance 1.Let Sn denote the partial sum...

Question 4 15 marks] The random variables X1, ... , Xn random variables with common pdf independent and identically distributed are 0 E fx (x;01) 0 independent of the random variables Y^,..., Y, which and are indepen are dent and identically distributed random variables with common pdf 0 fy (y; 02) 0 (a) Show that the MLE8 of 01 and 02 are 1 = X i=1 Y (b) Show that the MLE of 0 when 01 = 0, = 0...

Question 4 15 marks] The random variables X1, ... , Xn random variables with common pdf independent and identically distributed are 0 E fx (x;01) 0 independent of the random variables Y^,..., Y, which and are indepen are dent and identically distributed random variables with common pdf 0 fy (y; 02) 0 (a) Show that the MLE8 of 01 and 02 are 1 = X i=1 Y (b) Show that the MLE of 0 when 01 = 0, = 0...

Question 4 [15 marks] The random variables X1,... , Xn are independent and identically distributed with probability function Px (1 -px)1 1-2 -{ 0,1 fx (x) ; otherwise, 0 while the random variables Yı,...,Yn are independent and identically dis- tributed with probability function = { p¥ (1 - py) y 0,1,2 ; otherwise fy (y) 0 where px and py are between 0 and 1 (a) Show that the MLEs of px and py are Xi, n PY 2n (b)...

Question 4 [15 marks] The random variables X1,... , Xn are independent and identically distributed with probability function Px (1 -px)1 1-2 -{ 0,1 fx (x) ; otherwise, 0 while the random variables Yı,...,Yn are independent and identically dis- tributed with probability function = { p¥ (1 - py) y 0,1,2 ; otherwise fy (y) 0 where px and py are between 0 and 1 (a) Show that the MLEs of px and py are Xi, n PY 2n (b)...

Question 3 15 marks] Let X1,..,X be independent identically distributed random variables with pdf common ) = { (#)%2-1/64 0 fx (a;e) 0 where 0 >0 is an unknown parameter X-1. Show that Y ~ T (}, ); (a) Let Y (b) Show that 1 T n =1 is an unbiased estimator of 0-1 ewhere / (0; X) is the log- likeliho od function; (c) Compute U - (d) What functions T (0) have unbiased estimators that attain the relevant...

Question 3 15 marks] Let X1,..,X be independent identically distributed random variables with pdf common ) = { (#)%2-1/64 0 fx (a;e) 0 where 0 >0 is an unknown parameter X-1. Show that Y ~ T (}, ); (a) Let Y (b) Show that 1 T n =1 is an unbiased estimator of 0-1 ewhere / (0; X) is the log- likeliho od function; (c) Compute U - (d) What functions T (0) have unbiased estimators that attain the relevant...

13. Let X1, X2, ...,Xy be a sequence of independent and identically distributed discrete random variables, each with probability mass function P(X = k)=,, for k = 0,1,2,3,.... emak (a) Find the expected value and the variance of the sample mean as = N&i=1X,. (b) Find the probability mass function of X. (c) Find an approximate pdf of X when N is very large (N −0).

13. Let X1, X2, ...,Xy be a sequence of independent and identically distributed discrete random variables, each with probability mass function P(X = k)=,, for k = 0,1,2,3,.... emak (a) Find the expected value and the variance of the sample mean as = N&i=1X,. (b) Find the probability mass function of X. (c) Find an approximate pdf of X when N is very large (N −0).

Consider n independent and identically distributed random variables X1,X2, following a uniform distribution on the interval [0,1] ,Xn, each a) What is the pdf of Mmin(X1,X2, .. ,Xn)? b) Give the expectation and variance of XX 1-1лі.

Consider n independent and identically distributed random variables X1,X2, following a uniform distribution on the interval [0,1] ,Xn, each a) What is the pdf of Mmin(X1,X2, .. ,Xn)? b) Give the expectation and variance of XX 1-1лі.

Let X1 and X2 be independent random variables so X1~ N(u,1) and X2 N(u,4) Where u R a) Show that the likelihood for , given that X1 = x1 and X2 = xz is 8 4T b) Show, that the maxium likelihood estimate for u is 4x1+ x2 и (х, х2) e) Show that СтN -("x"x) .я d) and enter a formula for the 95% confidence interval for

Let X1 and X2 be independent random variables so X1~ N(u,1) and...

Let X1 and X2 be independent random variables so X1~ N(u,1) and X2 N(u,4) Where u R a) Show that the likelihood for , given that X1 = x1 and X2 = xz is 8 4T b) Show, that the maxium likelihood estimate for u is 4x1+ x2 и (х, х2) e) Show that СтN -("x"x) .я d) and enter a formula for the 95% confidence interval for

Let X1 and X2 be independent random variables so X1~ N(u,1) and...

Suppose n independent, identically distributed observations are

drawn from an exponential ()

distribution, with pdf given by f(x,)=,

0 < x <

.

The data are x1, x2, .. , xn

Construct a likelihood ratio hypothesis test of Ho :

vs H1:

(where

and

are known constants, with

), where the critical value is taken to be a constant c

We were unable to transcribe this imageWe were unable to transcribe this imageWe were unable to transcribe this imageWe were...

Suppose n independent, identically distributed observations are

drawn from an exponential ()

distribution, with pdf given by f(x,)=,

0 < x <

.

The data are x1, x2, .. , xn

Construct a likelihood ratio hypothesis test of Ho :

vs H1:

(where

and

are known constants, with

), where the critical value is taken to be a constant c

We were unable to transcribe this imageWe were unable to transcribe this imageWe were unable to transcribe this imageWe were...

3. Let {X1, X2, X3, X4} be independent, identically distributed random variables with p.d.f. f(0) = 2. o if 0<x< 1 else Find EY] where Y = min{X1, X2, X3, X4}.

3. Let {X1, X2, X3, X4} be independent, identically distributed random variables with p.d.f. f(0) = 2. o if 0<x< 1 else Find EY] where Y = min{X1, X2, X3, X4}.

Question 6 [15 marks] Let X1, X2,..., Xn be independent and identically distributed random vari- ables with common probability function ()p(1-p) m m-a ; x 0,1,. ., m otherwise 0 where m is known and p is unknown (a) Obtain the Sequential Probability Ratio Test of Ho p = po versus HA p P, where pi > po, with significance level 0.01 and power 0.95. Describe the test precisely; (b) For the case where po 3/8,pı = 1/2, m =...

Question 6 [15 marks] Let X1, X2,..., Xn be independent and identically distributed random vari- ables with common probability function ()p(1-p) m m-a ; x 0,1,. ., m otherwise 0 where m is known and p is unknown (a) Obtain the Sequential Probability Ratio Test of Ho p = po versus HA p P, where pi > po, with significance level 0.01 and power 0.95. Describe the test precisely; (b) For the case where po 3/8,pı = 1/2, m =...

3. Suppose X1, X2, -- are independent identically distributed random variables with mean 0 and variance 1.Let Sn denote the partial sum Let Fn denote the information contained in Xi, .X,. Suppoe m n. (1) Compute El(Sn Sm)lFm (2) Compute ESm(Sn Sm)|F (3) Compute ES|]. (Hint: Write S (4) Verify that S -n is a martingale. [Sm(Sn Sm))2)

3. Suppose X1, X2, -- are independent identically distributed random variables with mean 0 and variance 1.Let Sn denote the partial sum...

3. Suppose X1, X2, -- are independent identically distributed random variables with mean 0 and variance 1.Let Sn denote the partial sum Let Fn denote the information contained in Xi, .X,. Suppoe m n. (1) Compute El(Sn Sm)lFm (2) Compute ESm(Sn Sm)|F (3) Compute ES|]. (Hint: Write S (4) Verify that S -n is a martingale. [Sm(Sn Sm))2)

3. Suppose X1, X2, -- are independent identically distributed random variables with mean 0 and variance 1.Let Sn denote the partial sum...

Most questions answered within 3 hours.

-

If you were conducting a study involving twins regarding

genetics and/or upbringing, which would you use?...

asked 10 minutes ago -

Part 1- Inventory: You own a toy company and

you are producing wooden rocking horses. Assume...

asked 18 minutes ago -

What is aromaticity?

Identify aromatic molecules, especially those containing O, N,

S and B

asked 21 minutes ago -

A rubber solid circular wheel of uniform density spins about it

axis at rate of 60...

asked 33 minutes ago -

DNA evidence from an early human skeleton in Britain, shows that

early inhabitants of were blue...

asked 24 minutes ago -

Financial data for Joel de Paris, Inc., for last year

follow:

Joel de Paris, Inc.

Balance...

asked 33 minutes ago -

To practice Problem-Solving Strategy 19.1 Work in Ideal-gas

Processes.

A cylinder with initial volume V contains...

asked 41 minutes ago -

Depreciation for Partial Periods Bean Delivery Company purchased

a new delivery truck for $35,400 on April...

asked 45 minutes ago -

Q 5.23:

Jonathan has been doing calculations to determine a missing

component. So far he has...

asked 43 minutes ago -

Use indifference curve and the daily income-leisure choice model

to explain graphically the behavior of employees...

asked 1 hour ago -

Record the following transactions of Fashion Park in a

general journal. Fashion Park must charge 8...

asked 1 hour ago -

Chapter 08 Python Assignment: Question 1-5

Please I need help in my python course.

Question 1...

asked 1 hour ago