Homework Answers

a.

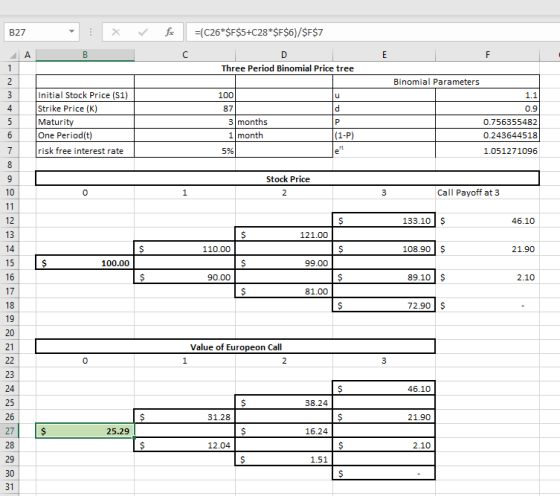

Factors of Option Binomial Model –

There are three parameters of Option Binomial Pricing Model

- up factor (u)

- down factor (d)

- probability (P)

up factor and down factor used to calculate rise in price and fall in price of underlying assets in one period. Probability is measure probability of rise in price and (1-P) is probability of price fall.

As per Risk-Neutral Probability

where,

r = rate of interest

t= time in each period

d = Price down factor

u = Price up factor

P = Probability of Price going up

(1-P) = probability of Price going down

We have following information -

Step (N) = 3

Spot Price of Stock (S0) = 100

Strike Price (K) = 87

r = 0.05

u = 1.1

d = 0.9

For calculation please refer to below spread sheet.

Formula Reference-

Value of European Call (V0) = $ 25.29

b.

European call option under binomial pricing theorem is $ 25.29 and current market price of same option is $ 25. This shows current market price of call option is not in equilibrium. Hence, There is arbitrage opportunity exist. Arbitrage an opportunity where arbitrager earn certain profit without making any investment and taking risk.

Arbitrage Strategy in above case -

In above case, Market Price of Call option is under-priced. Hence, to gain profit arbitrage follow below strategy

Today-

- Sale the stock at Spot price i.e $ 100

- Buy Call option at Market Price i.e $ 25

- Deposit Proceed from sale from stock to Bank at risk free interest rate i.e 0.05 & t=3

On Maturity-

- withdraw money from bank with interest

- Exercise the call option and buy the stock at strike price i.e 87

- Arbitrage Profit = Strike Price - Proceed from bank at maturity

C.

To earn $ 100,000 arbitrage Profit - Position of Assets,call option,cash

It is assumed that call option has size of 1 stock.

Firstly, calculate the arbitrage profit for one call option-

For one call option premium to be paid = $ 25

Sale Proceed from selling one stock at spot price = $ 100

After paying call premium from sale proceed deposit remaining amount to bank = $ 75

Interest factor (0.05,3) = ert = e0.05*3 = 1.1618

Amount received from bank at the end of period = $ 75 * 1.1618 = $ 87.135

Exercise the call option and pay to buy stock i.e strike price = $ 87

Remaining Amount would be Arbitrage Profit = 87.135 - 87 = $ 0.135

Thus, Size of Position to earn $ 100,000 arbitrage - as under

Long Call option = 100,000/0.135 = 740,741 (rounded)

Short Stock = 740,741

Cash in Bank = (740,741*100) - (740,741*25)

= 74,074,100 - 18,518,525

= $ 55,555,575

With above position, Arbitrage profit would be -

= (55,555,575*1.1618) - (740,741*87)

= 64,544,467 - 64,444,467

= $ 100,000

Add Answer to:

2. Consider the N-step binomial asset pricing model with 0 < d<1< u (a) Assume N-3....

I. Consider the N-step binomial asset pricing model with 0 < d < 1 + r...

I. Consider the N-step binomial asset pricing model with 0 < d < 1 + r < u. Assume N = 3, So 100, r = 0.05, u = 1.10, and d 0.90. Calculate the price at time zero of each of the following options using backward induction (a) A European put option expiring at time N 2 with strike price K-100 (b) A European put option expiring at time N 3 with strike price K- 100 (c) A European...

I. Consider the N-step binomial asset pricing model with 0 < d < 1 + r < u. Assume N = 3, So 100, r = 0.05, u = 1.10, and d 0.90. Calculate the price at time zero of each of the following options using backward induction (a) A European put option expiring at time N 2 with strike price K-100 (b) A European put option expiring at time N 3 with strike price K- 100 (c) A European...

Need helpp with both! 3. Consider the N-step binomial asset pricing model with 0 < d<1...

Need helpp with both!

3. Consider the N-step binomial asset pricing model with 0 < d<1 A European bear-spread option has payoff where Ki< K2 (a) Assume N- 3, So100, K-85, K2-100, 0.05,10, and d-0.90 Calculate the price at time zero, V, of the bear-spread option. (b) Specify how you can replicate the payoff of the European bear-spread option by investing in the stock and the bank account and verify that a short position in the European bear- spread option...

Need helpp with both!

3. Consider the N-step binomial asset pricing model with 0 < d<1 A European bear-spread option has payoff where Ki< K2 (a) Assume N- 3, So100, K-85, K2-100, 0.05,10, and d-0.90 Calculate the price at time zero, V, of the bear-spread option. (b) Specify how you can replicate the payoff of the European bear-spread option by investing in the stock and the bank account and verify that a short position in the European bear- spread option...

3. Consider the N-step binomial asset pricing model with 0 < d<1 A European bear-spread option...

3. Consider the N-step binomial asset pricing model with 0 < d<1 A European bear-spread option has payoff where Ki< K2 (a) Assume N- 3, So100, K-85, K2-100, 0.05,10, and d-0.90 Calculate the price at time zero, V, of the bear-spread option. (b) Specify how you can replicate the payoff of the European bear-spread option by investing in the stock and the bank account and verify that a short position in the European bear- spread option is hedged if the...

3. Consider the N-step binomial asset pricing model with 0 < d<1 A European bear-spread option has payoff where Ki< K2 (a) Assume N- 3, So100, K-85, K2-100, 0.05,10, and d-0.90 Calculate the price at time zero, V, of the bear-spread option. (b) Specify how you can replicate the payoff of the European bear-spread option by investing in the stock and the bank account and verify that a short position in the European bear- spread option is hedged if the...

1) consider a CRR model T = 2, S0= $100 , S1 = $200 or S1 = $50 an associated European call optio...

1) consider a CRR model T = 2, S0= $100 , S1 = $200 or S1 = $50 an associated European call option with strike price k = $80 and exercise time T = 2 assume that the risk free interest rate r = 0.1 a) draw the binary tree and compute the arbitrage free initial price of the European call option at time zero. b) Determine an explicit hedging strategy for this option c) Suppose that the option is...

PROBLEM 2. Consider a two-step Binomial model. In Figure 1 you are given an incomplete pricing...

PROBLEM 2. Consider a two-step Binomial model. In Figure 1 you are given an incomplete pricing tree, which corresponds to a European put option with strike price K = 65. (a) (5 Points) Compute the per period interest rate r and the risk-neutral probability p*. (b) (10 Points) Find the price of the put option at t = 0. Moreover, determine the complete binomial tree for the stock price. 2.6545 PE(O) 14.6 17.09 35.06 Figure 1: European put with K...

PROBLEM 2. Consider a two-step Binomial model. In Figure 1 you are given an incomplete pricing tree, which corresponds to a European put option with strike price K = 65. (a) (5 Points) Compute the per period interest rate r and the risk-neutral probability p*. (b) (10 Points) Find the price of the put option at t = 0. Moreover, determine the complete binomial tree for the stock price. 2.6545 PE(O) 14.6 17.09 35.06 Figure 1: European put with K...

3. Use a one step binomial option pricing model to value a 1 year at the...

3. Use a one step binomial option pricing model to value a 1 year at the money call option on AT&T. Assume interest rates are 2%. How does your value compare with the market price?

3. Use a one step binomial option pricing model to value a 1 year at the money call option on AT&T. Assume interest rates are 2%. How does your value compare with the market price?

Consider a two-period binomial model on an European put option. The stock is currently worth 48....

Consider a two-period binomial model on an European put option. The stock is currently worth 48. The exercise price is 52. The risk-free rate is 5% U = 1.15 and D=.9 . Price the European put option.

5. Consider a binomial tree model for a stock price, S(n) as above. Find a probability...

5. Consider a binomial tree model for a stock price, S(n) as above. Find a probability value p, in the case when the risk free assest has a continuous compounding rate of r. What are the bounds on e', that is, what is the smallest and largest value it can be in terms of u and d which prevent arbitrage? S(n) is a stock price where K1)u with probability p and K(1d with probability 1-p and K(1). K(n) are independent...

5. Consider a binomial tree model for a stock price, S(n) as above. Find a probability value p, in the case when the risk free assest has a continuous compounding rate of r. What are the bounds on e', that is, what is the smallest and largest value it can be in terms of u and d which prevent arbitrage? S(n) is a stock price where K1)u with probability p and K(1d with probability 1-p and K(1). K(n) are independent...

1. Consider the one period binomial model and assume 0 < So< 00, S1(H) -- uSo...

1. Consider the one period binomial model and assume 0 < So< 00, S1(H) -- uSo and Si (Τ)-dSo for some 0 〈 1 + r 〈 d 〈 u. P is an arbitrage oportunity. rove or disprove There

1. Consider the one period binomial model and assume 0 < So< 00, S1(H) -- uSo and Si (Τ)-dSo for some 0 〈 1 + r 〈 d 〈 u. P is an arbitrage oportunity. rove or disprove There

1. Consider the one period binomial model and assume 0 < So< 00, S1(H) -- uSo...

1. Consider the one period binomial model and assume 0 < So< 00, S1(H) -- uSo and Si (Τ)-dSo for some 0 〈 1 + r 〈 d 〈 u. P is an arbitrage oportunity. rove or disprove There

1. Consider the one period binomial model and assume 0 < So< 00, S1(H) -- uSo and Si (Τ)-dSo for some 0 〈 1 + r 〈 d 〈 u. P is an arbitrage oportunity. rove or disprove There

I. Consider the N-step binomial asset pricing model with 0 < d < 1 + r < u. Assume N = 3, So 100, r = 0.05, u = 1.10, and d 0.90. Calculate the price at time zero of each of the following options using backward induction (a) A European put option expiring at time N 2 with strike price K-100 (b) A European put option expiring at time N 3 with strike price K- 100 (c) A European...

I. Consider the N-step binomial asset pricing model with 0 < d < 1 + r < u. Assume N = 3, So 100, r = 0.05, u = 1.10, and d 0.90. Calculate the price at time zero of each of the following options using backward induction (a) A European put option expiring at time N 2 with strike price K-100 (b) A European put option expiring at time N 3 with strike price K- 100 (c) A European...

Need helpp with both!

3. Consider the N-step binomial asset pricing model with 0 < d<1 A European bear-spread option has payoff where Ki< K2 (a) Assume N- 3, So100, K-85, K2-100, 0.05,10, and d-0.90 Calculate the price at time zero, V, of the bear-spread option. (b) Specify how you can replicate the payoff of the European bear-spread option by investing in the stock and the bank account and verify that a short position in the European bear- spread option...

Need helpp with both!

3. Consider the N-step binomial asset pricing model with 0 < d<1 A European bear-spread option has payoff where Ki< K2 (a) Assume N- 3, So100, K-85, K2-100, 0.05,10, and d-0.90 Calculate the price at time zero, V, of the bear-spread option. (b) Specify how you can replicate the payoff of the European bear-spread option by investing in the stock and the bank account and verify that a short position in the European bear- spread option...

3. Consider the N-step binomial asset pricing model with 0 < d<1 A European bear-spread option has payoff where Ki< K2 (a) Assume N- 3, So100, K-85, K2-100, 0.05,10, and d-0.90 Calculate the price at time zero, V, of the bear-spread option. (b) Specify how you can replicate the payoff of the European bear-spread option by investing in the stock and the bank account and verify that a short position in the European bear- spread option is hedged if the...

3. Consider the N-step binomial asset pricing model with 0 < d<1 A European bear-spread option has payoff where Ki< K2 (a) Assume N- 3, So100, K-85, K2-100, 0.05,10, and d-0.90 Calculate the price at time zero, V, of the bear-spread option. (b) Specify how you can replicate the payoff of the European bear-spread option by investing in the stock and the bank account and verify that a short position in the European bear- spread option is hedged if the...

PROBLEM 2. Consider a two-step Binomial model. In Figure 1 you are given an incomplete pricing tree, which corresponds to a European put option with strike price K = 65. (a) (5 Points) Compute the per period interest rate r and the risk-neutral probability p*. (b) (10 Points) Find the price of the put option at t = 0. Moreover, determine the complete binomial tree for the stock price. 2.6545 PE(O) 14.6 17.09 35.06 Figure 1: European put with K...

PROBLEM 2. Consider a two-step Binomial model. In Figure 1 you are given an incomplete pricing tree, which corresponds to a European put option with strike price K = 65. (a) (5 Points) Compute the per period interest rate r and the risk-neutral probability p*. (b) (10 Points) Find the price of the put option at t = 0. Moreover, determine the complete binomial tree for the stock price. 2.6545 PE(O) 14.6 17.09 35.06 Figure 1: European put with K...

3. Use a one step binomial option pricing model to value a 1 year at the money call option on AT&T. Assume interest rates are 2%. How does your value compare with the market price?

3. Use a one step binomial option pricing model to value a 1 year at the money call option on AT&T. Assume interest rates are 2%. How does your value compare with the market price?

5. Consider a binomial tree model for a stock price, S(n) as above. Find a probability value p, in the case when the risk free assest has a continuous compounding rate of r. What are the bounds on e', that is, what is the smallest and largest value it can be in terms of u and d which prevent arbitrage? S(n) is a stock price where K1)u with probability p and K(1d with probability 1-p and K(1). K(n) are independent...

5. Consider a binomial tree model for a stock price, S(n) as above. Find a probability value p, in the case when the risk free assest has a continuous compounding rate of r. What are the bounds on e', that is, what is the smallest and largest value it can be in terms of u and d which prevent arbitrage? S(n) is a stock price where K1)u with probability p and K(1d with probability 1-p and K(1). K(n) are independent...

1. Consider the one period binomial model and assume 0 < So< 00, S1(H) -- uSo and Si (Τ)-dSo for some 0 〈 1 + r 〈 d 〈 u. P is an arbitrage oportunity. rove or disprove There

1. Consider the one period binomial model and assume 0 < So< 00, S1(H) -- uSo and Si (Τ)-dSo for some 0 〈 1 + r 〈 d 〈 u. P is an arbitrage oportunity. rove or disprove There

1. Consider the one period binomial model and assume 0 < So< 00, S1(H) -- uSo and Si (Τ)-dSo for some 0 〈 1 + r 〈 d 〈 u. P is an arbitrage oportunity. rove or disprove There

1. Consider the one period binomial model and assume 0 < So< 00, S1(H) -- uSo and Si (Τ)-dSo for some 0 〈 1 + r 〈 d 〈 u. P is an arbitrage oportunity. rove or disprove There

Most questions answered within 3 hours.

-

Explain the differences between FIND and FINDSTR command in

windows:

[write in a few sentences]

asked 5 minutes ago -

A 200g block attached to a horizontal spring is oscillating with

an amplitude of 2.0cm and...

asked 9 minutes ago -

When solving for an optimal bundle using the Hicksian and

Marshallian demand, should you get the...

asked 9 minutes ago -

1. The standard width between rails on North American and most

European railroads is 5 ft...

asked 6 minutes ago -

Which of these is a pure compound, which is an element, and

which is neither?

helium...

asked 13 minutes ago -

How much energy is required to vaporize 175 g of butane at its

boiling point? The...

asked 23 minutes ago -

X has a normal distribution with the given mean and

standard deviation. Find the indicated probability....

asked 25 minutes ago -

Calculate the probability that a particle will be found in a

tiny slice of space between...

asked 28 minutes ago -

Developed countries with some of the highest GDPs per

capita:

a)are not found outside of Europe...

asked 30 minutes ago -

draw a diagram illustrating the three ways of genetic

information flow

asked 46 minutes ago -

CASE 3-1 YOU CAN’T GET THERE FROM HERE: UBER SLOW ON

DIVERSITY

Established in 2009, Uber...

asked 45 minutes ago -

A local AM radio station broadcasts at an energy of

4.39×10-31 kJ/photon.

Calculate the frequency at...

asked 1 hour ago