Consider a market free of government intervention and having a downward sloping demand curve and an...

Consider a market free of government intervention and having a downward sloping demand curve and an upward sloping supply curve intersecting at some price P0.

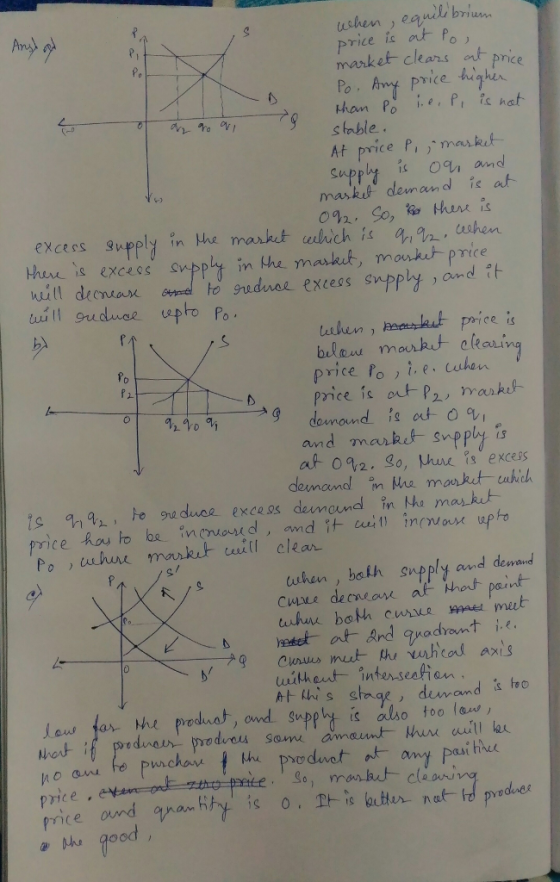

- Write a short explanation of why any price higher than P0cannot be a free market equilibrium.

- Write a shortexplanation of why any price lower than P0cannot be a free market equilibrium.

- Now decrease supply a great deal and decrease demand until the curves no longer intersect (that is, the curves meet the vertical axis without intersection). What is the free market equilibrium quantity?

Homework Answers

Answer-

Equilibrium price in a market of a particular product is determined through interaction between demand and supply curve in the market of that product. Equilibrium to be unique and stable it has to be in the 1st quadrant of the diagram i.e. intersection between supply and demand curve has to be in the 1st quadrant of the diagram.

Add Answer to:

Consider a market free of government intervention and having a downward sloping demand curve and an...

in a market with an upward sloping supply curve and a downward sloping demand curve, when...

in a market with an upward sloping supply curve and a downward sloping demand curve, when there is an excess supply, a. b. c. The actual price must be higher that the equilibrium price. The actual price must be lower that the equilibrium price. The quantity demanded is higher than the equilibrium quantity.

in a market with an upward sloping supply curve and a downward sloping demand curve, when there is an excess supply, a. b. c. The actual price must be higher that the equilibrium price. The actual price must be lower that the equilibrium price. The quantity demanded is higher than the equilibrium quantity.

Suppose there is a linear downward-sloping demand curve and a linear upward-sloping supply curve for some...

Suppose there is a linear downward-sloping demand curve and a linear upward-sloping supply curve for some good. The price of a substitute good decreases and the price of an input to the production process also decreases. Both changes occur simultaneously. Graph the original demand and supply curves, and then graph new curves after the substitute good and input prices decrease. How will the equilibrium price and quantity change after the substitute and input prices decrease? Explain your answer in English...

1) Consider a normal market with a downward-sloping demand curve and an upward-sloping supply curve. Which...

1) Consider a normal market with a downward-sloping demand curve and an upward-sloping supply curve. Which of the following cases would definitely result in a decrease in consumer surplus? For each case, assume that the market is initially in equilibrium and that everything else is held constant except for the change described in the case Case 1: The supply curve shifts to the left. Case 2: The supp Case 3: The government imposes a binding price ceiling. Case 4: The...

1) Consider a normal market with a downward-sloping demand curve and an upward-sloping supply curve. Which of the following cases would definitely result in a decrease in consumer surplus? For each case, assume that the market is initially in equilibrium and that everything else is held constant except for the change described in the case Case 1: The supply curve shifts to the left. Case 2: The supp Case 3: The government imposes a binding price ceiling. Case 4: The...

suppose that the market for product x is characterized by a typical, downward-sloping, linear demand curve...

suppose that the market for product x is characterized by a typical, downward-sloping, linear demand curve and a typical , upward-sloping, linear supply curve. suppose the price of supply is 0.7. will the dead weight loss form a $3 tax per unit be smaller if the absolute value of the price elasticity of demand is 0.6 or if the absolute value of the price elasticity of demand is 1.5?

please answer Question 4 2.6 pts Assuming Demand is downward sloping and Supply is upward sloping...

please answer

Question 4 2.6 pts Assuming Demand is downward sloping and Supply is upward sloping (as we usually do), what happens to equilibrium price (P) and quantity (Q) of a good when Demand decreases? P and Q should not change P increases; Q increases P increases; Q decreases. P decreases, decreases. P decreases; Q increases. Question 5 2.6 pts Suppose that the supply of Blu Ray players decreases (i.e., shifts to the left). Using our standard supply and demand...

please answer

Question 4 2.6 pts Assuming Demand is downward sloping and Supply is upward sloping (as we usually do), what happens to equilibrium price (P) and quantity (Q) of a good when Demand decreases? P and Q should not change P increases; Q increases P increases; Q decreases. P decreases, decreases. P decreases; Q increases. Question 5 2.6 pts Suppose that the supply of Blu Ray players decreases (i.e., shifts to the left). Using our standard supply and demand...

Given a downward-sloping aggregate demand (AD) curve and an upward-sloping short-run aggregate supply curve (SRAS), equilibrium...

Given a downward-sloping aggregate demand (AD) curve and an upward-sloping short-run aggregate supply curve (SRAS), equilibrium occurs where the two intersect. The value on the vertical axis is the equilibrium price level and the value on the horizontal axis is the equilibrium value of real GDP or output. What happens to the economy when AD shifts? It is useful to sketch a graph and show the shift. Suppose, for example, interest rates fall or wealth increases due to a stock...

In a competitive market with a linear upward-sloping supply curve and a linear downward-sloping demand curve, the government imposes a $10 tax per unit bought and sold. The tax causes the equilibrium quantity to fall from 113 units to 101 units. The deadw

In a competitive market with a linear upward-sloping supply curve and a linear downward-sloping demand curve, the government imposes a $10 tax per unit bought and sold. The tax causes the equilibrium quantity to fall from 113 units to 101 units. The deadweight loss of this tax is $______

DEMAND & SUPPLY: Consider the market for bananas which is known to be perfectly competitive. The...

DEMAND & SUPPLY: Consider the market for bananas which is known to be perfectly competitive. The market is characterized by the following relationships: QD = 10,000 – 140P QS = 7500 + 125P Plot the demand curve and the supply curve on a graph. Clearly label the axes and the intercepts. Why is the demand-curve downward-sloping? What is the slope of the demand curve? Why is the supply-curve upward-sloping? What is the slope of the supply curve? What is the...

Suppose that, in a perfect competitive market, an equilibrium point is generated by intersecting downward sloping...

Suppose that, in a perfect competitive market, an equilibrium point is generated by intersecting downward sloping market demand curve and upward sloping market supply curve. Explain step by step how to get this equilibrium point from the decision making of INDIVIDAL consumers and producers. In your answer individual consumer's decision making must start from preference ordering and utility maximizing process. Producer's decision making must start from budget constraint, production function and go to the process of cost minimization and profit...

Suppose that, in a perfect competitive market, an equilibrium point is generated by intersecting downward sloping market demand curve and upward sloping market supply curve. Explain step by step how to get this equilibrium point from the decision making of INDIVIDAL consumers and producers. In your answer individual consumer's decision making must start from preference ordering and utility maximizing process. Producer's decision making must start from budget constraint, production function and go to the process of cost minimization and profit...

Suppose that, in a perfect competitive market, an equilibrium point is generated by intersecting downward sloping...

Suppose that, in a perfect competitive market, an equilibrium point is generated by intersecting downward sloping market demand curve and upward sloping market supply curve. Explain step by step how to get this equilibrium point from the decision making of INDIVIDAL consumers and producers. In your answer, individual consumer’s decision making must start from preference ordering and utility maximizing process. Producer’s decision making must start from budget constraint, production function and go to the process of cost minimization and profit...

in a market with an upward sloping supply curve and a downward sloping demand curve, when there is an excess supply, a. b. c. The actual price must be higher that the equilibrium price. The actual price must be lower that the equilibrium price. The quantity demanded is higher than the equilibrium quantity.

in a market with an upward sloping supply curve and a downward sloping demand curve, when there is an excess supply, a. b. c. The actual price must be higher that the equilibrium price. The actual price must be lower that the equilibrium price. The quantity demanded is higher than the equilibrium quantity.

1) Consider a normal market with a downward-sloping demand curve and an upward-sloping supply curve. Which of the following cases would definitely result in a decrease in consumer surplus? For each case, assume that the market is initially in equilibrium and that everything else is held constant except for the change described in the case Case 1: The supply curve shifts to the left. Case 2: The supp Case 3: The government imposes a binding price ceiling. Case 4: The...

1) Consider a normal market with a downward-sloping demand curve and an upward-sloping supply curve. Which of the following cases would definitely result in a decrease in consumer surplus? For each case, assume that the market is initially in equilibrium and that everything else is held constant except for the change described in the case Case 1: The supply curve shifts to the left. Case 2: The supp Case 3: The government imposes a binding price ceiling. Case 4: The...

please answer

Question 4 2.6 pts Assuming Demand is downward sloping and Supply is upward sloping (as we usually do), what happens to equilibrium price (P) and quantity (Q) of a good when Demand decreases? P and Q should not change P increases; Q increases P increases; Q decreases. P decreases, decreases. P decreases; Q increases. Question 5 2.6 pts Suppose that the supply of Blu Ray players decreases (i.e., shifts to the left). Using our standard supply and demand...

please answer

Question 4 2.6 pts Assuming Demand is downward sloping and Supply is upward sloping (as we usually do), what happens to equilibrium price (P) and quantity (Q) of a good when Demand decreases? P and Q should not change P increases; Q increases P increases; Q decreases. P decreases, decreases. P decreases; Q increases. Question 5 2.6 pts Suppose that the supply of Blu Ray players decreases (i.e., shifts to the left). Using our standard supply and demand...

Suppose that, in a perfect competitive market, an equilibrium point is generated by intersecting downward sloping market demand curve and upward sloping market supply curve. Explain step by step how to get this equilibrium point from the decision making of INDIVIDAL consumers and producers. In your answer individual consumer's decision making must start from preference ordering and utility maximizing process. Producer's decision making must start from budget constraint, production function and go to the process of cost minimization and profit...

Suppose that, in a perfect competitive market, an equilibrium point is generated by intersecting downward sloping market demand curve and upward sloping market supply curve. Explain step by step how to get this equilibrium point from the decision making of INDIVIDAL consumers and producers. In your answer individual consumer's decision making must start from preference ordering and utility maximizing process. Producer's decision making must start from budget constraint, production function and go to the process of cost minimization and profit...

Most questions answered within 3 hours.

-

An MNE is this kind of industry when competition in one country

is essentially independent of...

asked 48 minutes ago -

. For this set of questions, determine what

proportion of a normal distribution is located betweeneach...

asked 1 hour ago -

A college student is employed as a door-to-door newspaper

salesman. Historical data suggests that the student...

asked 2 hours ago -

MATLAB HW 11 problem using Switch Case and Input commands

Write a script file that calculates...

asked 2 hours ago -

Considering gravitational time dilation, calculate the time that

passes in Earth’s surface while 1 hour passes...

asked 2 hours ago -

Minitab Problem: Take the Lake Hume June rainfall data and find

use the processes outlined in...

asked 3 hours ago -

X Company is trying to decide whether to continue using old

equipment to make Product A...

asked 3 hours ago -

IN PYTHON ONLY !! Program 2: Re-work

program #5 (WeeklyHours) from the previous assignment such that...

asked 4 hours ago -

The average length of time between arrivals at a turnpike

toll-booth is 26 seconds. What is...

asked 5 hours ago -

(a) A piston at 6.1 atm contains a gas that occupies a volume of

3.5 L....

asked 7 hours ago -

Please answer true or false. Words

cannot be changed or added in to make it true...

asked 7 hours ago -

An empty test tube weighs 15.923 grams. Then,

MgCl2•6H2O is added into the test tube. After...

asked 7 hours ago