Homework Answers

Attached below is the spreadsheet showing all the calculations involved in arriving at the answer

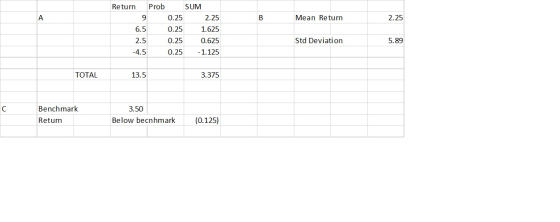

a) Expected Return 3.375% which is the arrived at by assigning a probability of 0.25 to each growth possibility

b) Calculating the Std Deviation of the four returns leads us to 5.89 as SD

c) Assuming equal probability the return as per A is 3.375% which is below the benchmark 3.5% by (0.125%)

d) A Securities performance can be measured in absolute terms or relative performance against a benchmark . The benchmark represents the broader market implying the average performance should be ideally equal to this. In this case actual performance is not yet known but by assigning equal probabilities to the 4 possible outcomes the expected return is 3.375%. Unfortunately the benchmark remains constant at 3.5% which is higher . So this mathematically calculated expected performance is actually below average. .

Addendum spreadsheet attached

Add Answer to:

QUESTION FOUR you are given the following data about expected returns on a security on the...

investment analysis you are given the following data about expected returns on a security on the lusa where differen...

investment analysis

you are given the following data about expected

returns on a security on the lusa where different states of the

economy have the same probability of occurrence

QUESTION FOUR You are given the folowing data about expected retums on a security on the LUSE where different states of the economy have the same probability of occurrencs State Retun Strong growth 9.0% Normal growth 6.5% Weak growth 2.5% 4.5 % Recession Required: Compute and fully interpret the following for...

investment analysis

you are given the following data about expected

returns on a security on the lusa where different states of the

economy have the same probability of occurrence

QUESTION FOUR You are given the folowing data about expected retums on a security on the LUSE where different states of the economy have the same probability of occurrencs State Retun Strong growth 9.0% Normal growth 6.5% Weak growth 2.5% 4.5 % Recession Required: Compute and fully interpret the following for...

QUESTION 4 You are given the following data about expected returns on a security on the...

QUESTION 4 You are given the following data about expected returns on a security on the LUSE where different states of the economy have the same probability of occurrence: State Return Strong growth 9.0% Normal growth 6.5% Weak growth 2.5% Recession -4.5% Required: Compute and fully interpret the following for the investment: The Expected return for the security. [3 Marks] The volatility of the security returns using the semi deviation. [6 Marks] Evaluate the security’s performance assuming a...

QUESTION THREE a) A colleague of yours has a K100,000-00, 2 years treasury Bond matunng in...

QUESTION THREE a) A colleague of yours has a K100,000-00, 2 years treasury Bond matunng in ons, issued at a fixed coupon of 10%, payable annually. He informs you that he has an urgent need of money and wants to sell you the Bond. What's the maximum price you would offer assuming the yield on a 12 months treasury bill is currently at 12%? [4 Marks] Briefly discuss how you may be affected by inflation over the holding period to...

QUESTION THREE a) A colleague of yours has a K100,000-00, 2 years treasury Bond matunng in ons, issued at a fixed coupon of 10%, payable annually. He informs you that he has an urgent need of money and wants to sell you the Bond. What's the maximum price you would offer assuming the yield on a 12 months treasury bill is currently at 12%? [4 Marks] Briefly discuss how you may be affected by inflation over the holding period to...

QUESTION 4 You are given the following data about expected returns on a Bank security on...

QUESTION 4 You are given the following data about expected returns on a Bank security on the LUSE where different states of the economy have the same probability of occurrence: State Return Strong growth 7.5% Normal growth 5.0% Weak growth 1.5% Recession -2.5% Required: Compute and fully interpret the following for the investment: The Expected return for the security. [5 Marks] The volatility of the security returns using the standard deviation. [6 Marks] The Sharpe ratio of...

You have been given information about the performance of two securities, a Telecoms stock and a...

You have been given information about the performance of two securities, a Telecoms stock and a Bank stock, over the past ten years in the table below. Based on this information, you have been requested to undertake a performance analysis with a view to forming a two-security portfolio. Year Telecoms Bank % % 2000 0.1 -4.5 2001 -16.1 42.7 2002 -28.3 14.5 2003 20.1 1.7 3.7 2004 21.5 2005 0.2 2.4 53.2 20.7 2006 2007 20.6 -18.9 2008 -28.0 -63.1...

You have been given information about the performance of two securities, a Telecoms stock and a Bank stock, over the past ten years in the table below. Based on this information, you have been requested to undertake a performance analysis with a view to forming a two-security portfolio. Year Telecoms Bank % % 2000 0.1 -4.5 2001 -16.1 42.7 2002 -28.3 14.5 2003 20.1 1.7 3.7 2004 21.5 2005 0.2 2.4 53.2 20.7 2006 2007 20.6 -18.9 2008 -28.0 -63.1...

investment analysis

you are given the following data about expected

returns on a security on the lusa where different states of the

economy have the same probability of occurrence

QUESTION FOUR You are given the folowing data about expected retums on a security on the LUSE where different states of the economy have the same probability of occurrencs State Retun Strong growth 9.0% Normal growth 6.5% Weak growth 2.5% 4.5 % Recession Required: Compute and fully interpret the following for...

investment analysis

you are given the following data about expected

returns on a security on the lusa where different states of the

economy have the same probability of occurrence

QUESTION FOUR You are given the folowing data about expected retums on a security on the LUSE where different states of the economy have the same probability of occurrencs State Retun Strong growth 9.0% Normal growth 6.5% Weak growth 2.5% 4.5 % Recession Required: Compute and fully interpret the following for...

QUESTION THREE a) A colleague of yours has a K100,000-00, 2 years treasury Bond matunng in ons, issued at a fixed coupon of 10%, payable annually. He informs you that he has an urgent need of money and wants to sell you the Bond. What's the maximum price you would offer assuming the yield on a 12 months treasury bill is currently at 12%? [4 Marks] Briefly discuss how you may be affected by inflation over the holding period to...

QUESTION THREE a) A colleague of yours has a K100,000-00, 2 years treasury Bond matunng in ons, issued at a fixed coupon of 10%, payable annually. He informs you that he has an urgent need of money and wants to sell you the Bond. What's the maximum price you would offer assuming the yield on a 12 months treasury bill is currently at 12%? [4 Marks] Briefly discuss how you may be affected by inflation over the holding period to...

You have been given information about the performance of two securities, a Telecoms stock and a Bank stock, over the past ten years in the table below. Based on this information, you have been requested to undertake a performance analysis with a view to forming a two-security portfolio. Year Telecoms Bank % % 2000 0.1 -4.5 2001 -16.1 42.7 2002 -28.3 14.5 2003 20.1 1.7 3.7 2004 21.5 2005 0.2 2.4 53.2 20.7 2006 2007 20.6 -18.9 2008 -28.0 -63.1...

You have been given information about the performance of two securities, a Telecoms stock and a Bank stock, over the past ten years in the table below. Based on this information, you have been requested to undertake a performance analysis with a view to forming a two-security portfolio. Year Telecoms Bank % % 2000 0.1 -4.5 2001 -16.1 42.7 2002 -28.3 14.5 2003 20.1 1.7 3.7 2004 21.5 2005 0.2 2.4 53.2 20.7 2006 2007 20.6 -18.9 2008 -28.0 -63.1...

Most questions answered within 3 hours.

-

. For this set of questions, determine what

proportion of a normal distribution is located betweeneach...

asked 18 minutes ago -

A college student is employed as a door-to-door newspaper

salesman. Historical data suggests that the student...

asked 1 hour ago -

MATLAB HW 11 problem using Switch Case and Input commands

Write a script file that calculates...

asked 58 minutes ago -

Considering gravitational time dilation, calculate the time that

passes in Earth’s surface while 1 hour passes...

asked 1 hour ago -

Minitab Problem: Take the Lake Hume June rainfall data and find

use the processes outlined in...

asked 2 hours ago -

X Company is trying to decide whether to continue using old

equipment to make Product A...

asked 2 hours ago -

IN PYTHON ONLY !! Program 2: Re-work

program #5 (WeeklyHours) from the previous assignment such that...

asked 3 hours ago -

The average length of time between arrivals at a turnpike

toll-booth is 26 seconds. What is...

asked 4 hours ago -

(a) A piston at 6.1 atm contains a gas that occupies a volume of

3.5 L....

asked 5 hours ago -

Please answer true or false. Words

cannot be changed or added in to make it true...

asked 5 hours ago -

An empty test tube weighs 15.923 grams. Then,

MgCl2•6H2O is added into the test tube. After...

asked 5 hours ago -

Assume memory access is 10 units of time and disk access is

10000 units of time....

asked 6 hours ago