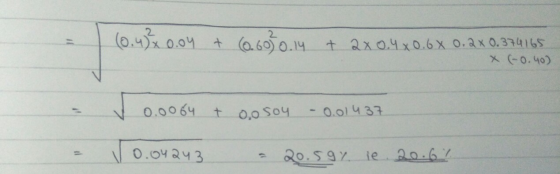

1.Stock X has an expected return of 12% and a variance of .04. Stock Y has...

1.Stock X has an expected return of 12% and a variance of .04. Stock Y has an expected return of 24% and a variance of .14. Stocks X and Y have a correlation coefficient of –.4. Calculate the expected return (in %) and standard deviation (in %) of a portfolio consisting of $20,000 invested in stock X and $30,000 invested in stock Y.

Unless stated otherwise, compounding is annual and payments occur at the end of the period.

Homework Answers

Add Answer to:

1.Stock X has an expected return of 12% and a variance of .04. Stock Y has...

Assume an investment manager is considering to invest in a portfolio composed of Stock (A) and Stock (B). Stock (A) has an expected return of 10% and a Variance of 100 (Standard Deviation=10), while Stock (B) has an expected return of

Assume an investment manager is considering to invest in a portfolio composed of Stock (A) and Stock (B). Stock (A) has an expected return of 10% and a Variance of 100 (Standard Deviation=10), while Stock (B) has an expected return of 20% and a Variance of 900 (Standard deviation=30).1- Calculate the expected return and variance of the portfolio if the proportion invested in Sock (A) is (0, .2, .3,.5. .6,.7,1) .The Correlation Coefficient is .4.2- If the Correlation Coefficient is...

these SUCI 8-19 KAND RETURN Stock X has a 10% expected return, a beta coefficient of...

these SUCI 8-19 KAND RETURN Stock X has a 10% expected return, a beta coefficient of EVALUATING 0.9. and a 35% standard deviation of expected returns. Stock Y has a 12.5% expected return a beta coefficient of 1.2, and a 25% standard deviation. The risk-free rate is 6%, and the market risk premium is 5%. a. Calculate each stock's coefficient of variation. b. Which stock is riskier for a diversified investor? c. Calculate each stock's required rate of return. d....

these SUCI 8-19 KAND RETURN Stock X has a 10% expected return, a beta coefficient of EVALUATING 0.9. and a 35% standard deviation of expected returns. Stock Y has a 12.5% expected return a beta coefficient of 1.2, and a 25% standard deviation. The risk-free rate is 6%, and the market risk premium is 5%. a. Calculate each stock's coefficient of variation. b. Which stock is riskier for a diversified investor? c. Calculate each stock's required rate of return. d....

Stock X has an expected return of 15%, standard deviation of 20%, beta of 0.8. Stock...

Stock X has an expected return of 15%, standard deviation of 20%, beta of 0.8. Stock Y has an expected return of 20%, a standard deviation of 40% and a beta of 0.3, and a correlation with stock X of 0.6. Assume the CAPM holds. a. If you are a typical, risk-averse investor with a well-diversified portfolio, which stock would you prefer? b. What are the expected return and standard deviation of a portfolio consisting of 30% of stock X...

Stock X has an expected return of 15%, standard deviation of 20%, beta of 0.8. Stock Y has an expected return of 20%, a standard deviation of 40% and a beta of 0.3, and a correlation with stock X of 0.6. Assume the CAPM holds. a. If you are a typical, risk-averse investor with a well-diversified portfolio, which stock would you prefer? b. What are the expected return and standard deviation of a portfolio consisting of 30% of stock X...

Two-stock Portfolio Stock A has an expected return of 12.50 percent and a standard deviation of...

Two-stock Portfolio Stock A has an expected return of 12.50 percent and a standard deviation of 25.50 percent. Stock B has an expected return of 7.25 percent and a standard deviation of 30.45 percent. The correlation coefficient between Stock A and B is 0.23. The optimal weight of Stock A in a portfolio consisting of these two stocks is estimated to be _ , and the standard deviation of this portfolio is estimated to be Select one: O a. 61.35%;...

Two-stock Portfolio Stock A has an expected return of 12.50 percent and a standard deviation of 25.50 percent. Stock B has an expected return of 7.25 percent and a standard deviation of 30.45 percent. The correlation coefficient between Stock A and B is 0.23. The optimal weight of Stock A in a portfolio consisting of these two stocks is estimated to be _ , and the standard deviation of this portfolio is estimated to be Select one: O a. 61.35%;...

EVALUATING RISK AND RETURN Stock X has a 10.5% expected return, a beta coefficient of 1.0,...

EVALUATING RISK AND RETURN Stock X has a 10.5% expected return, a beta coefficient of 1.0, and a 35% standard deviation of expected returns. Stock Y has a 12.5% expected return, a beta coefficient of 1.2, and a 30.0% standard deviation. The risk-free rate is 6%, and the market risk premium is 5%. Calculate each stock's coefficient of variation. Round your answers to two decimal places. Do not round intermediate calculations. Cvx= ?Cvy=? C.Calculate each stock's required rate of return.Rx=?...

5. Stock X has a 10% expected return, a Beta coefficient of .9, and a 35%...

5. Stock X has a 10% expected return, a Beta coefficient of .9, and a 35% standard deviation of expected return. Stock Y has a 12.5% expected return, a bet coefficient of 2, and a 25% standard deviation. The risk free rate is 2% and the market risk premium is 5% Calculate each stock’s coefficient of variation. Which stock is riskier? Calculate each stock’s required rate of return. Calculate the required rate of return of a portfolio that has $7,500...

QUESTION 54 Your portfolio consists of $50,000 invested in Stock X and $50,000 invested in Stock ...

please assist with excel function or calculator

QUESTION 54 Your portfolio consists of $50,000 invested in Stock X and $50,000 invested in Stock Y. Both stocks have return of 15%, betas of 1.6, and standard deviations of 30%-The returns ofthe two stocks are independent correlation coefficient between them, xy, is zero. Which of the following statements best describes the cl your 2-stock portfolio? Your portfolio has a beta greater than 1.6, and its expected return is greater than 15% Your...

please assist with excel function or calculator

QUESTION 54 Your portfolio consists of $50,000 invested in Stock X and $50,000 invested in Stock Y. Both stocks have return of 15%, betas of 1.6, and standard deviations of 30%-The returns ofthe two stocks are independent correlation coefficient between them, xy, is zero. Which of the following statements best describes the cl your 2-stock portfolio? Your portfolio has a beta greater than 1.6, and its expected return is greater than 15% Your...

EVALUATING RISK AND RETURN Stock X has a 9.5% expected return, a beta coefficient of 0.8,...

EVALUATING RISK AND RETURN Stock X has a 9.5% expected return, a beta coefficient of 0.8, and a 35% standard deviation of expected returns. Stock Y has a 12.5% expected return, a beta coefficient of 1.2, and a 20.0% standard deviation. The risk-free rate is 6%, and the market risk premium is 5%. Calculate each stock's coefficient of variation. Round your answers to two decimal places. Do not round intermediate calculations. CVx = CVy = Which stock is riskier for...

Stock X has a 9.5% expected return, a beta coefficient of 0.8, and a 30% standard...

Stock X has a 9.5% expected return, a beta coefficient of 0.8, and a 30% standard deviation of expected returns. Stock Y has a 12.0% expected return, a beta coefficient of 1.1, and a 30.0% standard deviation. The risk-free rate is 6%, and the market risk premium is 5%. Calculate the required return of a portfolio that has $7,500 invested in Stock X and $5,500 invested in Stock Y. Do not round intermediate calculations. Round your answer to two decimal...

Consider a portfolio that contains two stocks. Stock "A" has an expected return of 10% and...

Consider a portfolio that contains two stocks. Stock "A" has an expected return of 10% and a standard deviation of 20%. Stock "B" has an expected return of -10% and a standard deviation of 25%. The proportion of your wealth invested in stock "A" is 60%. The correlation between the two stocks is 0. What is the expected return of the portfolio? Enter your answer as a percentage. Do not include the percentage sign in your answer. Enter your response...

these SUCI 8-19 KAND RETURN Stock X has a 10% expected return, a beta coefficient of EVALUATING 0.9. and a 35% standard deviation of expected returns. Stock Y has a 12.5% expected return a beta coefficient of 1.2, and a 25% standard deviation. The risk-free rate is 6%, and the market risk premium is 5%. a. Calculate each stock's coefficient of variation. b. Which stock is riskier for a diversified investor? c. Calculate each stock's required rate of return. d....

these SUCI 8-19 KAND RETURN Stock X has a 10% expected return, a beta coefficient of EVALUATING 0.9. and a 35% standard deviation of expected returns. Stock Y has a 12.5% expected return a beta coefficient of 1.2, and a 25% standard deviation. The risk-free rate is 6%, and the market risk premium is 5%. a. Calculate each stock's coefficient of variation. b. Which stock is riskier for a diversified investor? c. Calculate each stock's required rate of return. d....

Stock X has an expected return of 15%, standard deviation of 20%, beta of 0.8. Stock Y has an expected return of 20%, a standard deviation of 40% and a beta of 0.3, and a correlation with stock X of 0.6. Assume the CAPM holds. a. If you are a typical, risk-averse investor with a well-diversified portfolio, which stock would you prefer? b. What are the expected return and standard deviation of a portfolio consisting of 30% of stock X...

Stock X has an expected return of 15%, standard deviation of 20%, beta of 0.8. Stock Y has an expected return of 20%, a standard deviation of 40% and a beta of 0.3, and a correlation with stock X of 0.6. Assume the CAPM holds. a. If you are a typical, risk-averse investor with a well-diversified portfolio, which stock would you prefer? b. What are the expected return and standard deviation of a portfolio consisting of 30% of stock X...

Two-stock Portfolio Stock A has an expected return of 12.50 percent and a standard deviation of 25.50 percent. Stock B has an expected return of 7.25 percent and a standard deviation of 30.45 percent. The correlation coefficient between Stock A and B is 0.23. The optimal weight of Stock A in a portfolio consisting of these two stocks is estimated to be _ , and the standard deviation of this portfolio is estimated to be Select one: O a. 61.35%;...

Two-stock Portfolio Stock A has an expected return of 12.50 percent and a standard deviation of 25.50 percent. Stock B has an expected return of 7.25 percent and a standard deviation of 30.45 percent. The correlation coefficient between Stock A and B is 0.23. The optimal weight of Stock A in a portfolio consisting of these two stocks is estimated to be _ , and the standard deviation of this portfolio is estimated to be Select one: O a. 61.35%;...

please assist with excel function or calculator

QUESTION 54 Your portfolio consists of $50,000 invested in Stock X and $50,000 invested in Stock Y. Both stocks have return of 15%, betas of 1.6, and standard deviations of 30%-The returns ofthe two stocks are independent correlation coefficient between them, xy, is zero. Which of the following statements best describes the cl your 2-stock portfolio? Your portfolio has a beta greater than 1.6, and its expected return is greater than 15% Your...

please assist with excel function or calculator

QUESTION 54 Your portfolio consists of $50,000 invested in Stock X and $50,000 invested in Stock Y. Both stocks have return of 15%, betas of 1.6, and standard deviations of 30%-The returns ofthe two stocks are independent correlation coefficient between them, xy, is zero. Which of the following statements best describes the cl your 2-stock portfolio? Your portfolio has a beta greater than 1.6, and its expected return is greater than 15% Your...

Most questions answered within 3 hours.

-

Write SQL queries to answer the following question: A. Which

students are enrolled in Database and...

asked 21 minutes ago -

Required:

How was Dell computer working capital policy as a competitive

advantage? Write at least 200...

asked 3 minutes ago -

Your eye is 2.5 m away from a 60W light bulb that emits light in

all...

asked 10 minutes ago -

Cars enter a car wash at a mean rate of 2 cars per half an hour....

asked 7 minutes ago -

As a human and using your own human Intelligent Analysis (IA),

you would have noted that...

asked 12 minutes ago -

Transverse waves on a string have wave speed 8 m/s, amplitude

0.071 m, and wavelength 0.33...

asked 26 minutes ago -

At −11°C a sample of carbon monoxide gas exerts a pressure of

0.45 atm. What is...

asked 26 minutes ago -

Aqueous hydrobromic acid HBr reacts with solid sodium hydroxide

NaOH to produce aqueous sodium bromide NaBr...

asked 40 minutes ago -

You dissolve 1.0 mole of a substance in water to a total volume

of 1,000 ml....

asked 45 minutes ago -

A company's total assets at the end of last year were 500,000

and its EBIT was...

asked 50 minutes ago -

Is it redundant to say that a pure substance is homogeneous, or

can it not be...

asked 53 minutes ago -

Already famous by the time he arrived at Princeton University in

1933, Einstein had suggested a...

asked 1 hour ago