What is competition like in the North American wholesale club industry? Which of the five competitive...

What is competition like in the North American wholesale club industry? Which of the five competitive forces is strongest and why? Use the information in Figures 3.4, 3.5, 3.6, 3.7, and 3.8 (and the related chapter discussions on pp. 57–70) to do a complete five–forces analysis of competition in the North American wholesale club industry.

Homework Answers

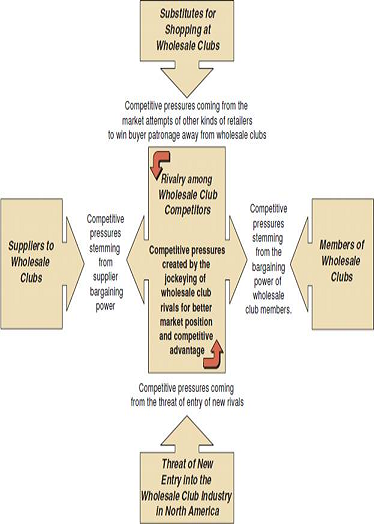

Below is a representative five-forces model of competition for the North American wholesale club industry:

■ Rivalry among wholesale club competitors— a strong to fierce competitive force

In assessing this competitive force, students should be draw upon the information in Figure 3.4 on p. 57 of Chapter 3 (and the related text discussion on pp. 56-58).

The rivalry among Costco, Sam’s Club, and BJ’s Wholesale is vigorous and likely to remain so. All 3 competitors are striving to attract more members and to offer merchandise selections and a shopping experience that will cause members to make more store visits and/or spend larger sums per visit. Rivalry is centered on two main factors:

• Low prices (consistently below retail price levels and the prices charged by retail discounters)—prices had to be at “bargain levels” in order to attract members and provide them with considerable cost savings (enough to more than cover membership fees)

• Product quality and selection

o Merchandise was generally of good to excellent quality and often included name brand products supplemented with an assortment of private-label products

o Warehouse clubs stocked 3,500 to 4,500 items, a portion of which were ever-changing as company purchasing personnel ran upon one-time buying opportunities. Typical supermarkets stocked about 40,000 items and a Wal-Mart Supercenter or SuperTarget might have as many as 150,000 items for shoppers to choose from.

o The product lineup included such items as appliances, electronics, office and restaurant supplies, auto supplies, toys and games, light bulbs, batteries, cookware, tools, apparel, DVDs, books, canned and frozen foods, fresh meats and seafood, fresh fruits and vegetables, bakery items, beverages, wines, vitamins and personal care products, cleaning supplies, and paper products.

o Selection within each category was limited (usually to fast-selling models, colors, and large-quantity sizes).

• To encourage members to shop more frequently and create a bit more of a one-stop shopping appeal, both Costco and Sam’s Club operated ancillary businesses within or next to most warehouses—gas stations, optical centers, photo centers, print and copy centers, pharmacies, food courts, and the like.

To a much lesser extent, rivalry also revolved around attracting members/shoppers by means of convenient store locations, fast checkout, and a comparatively pleasant big-box shopping environment.

Class members should cite several factors (displayed in Figure 4.3) as working to intensify rivalry among the three warehouse club competitors in North America:

• All 3 club rivals are aggressively pursuing top-line revenue growth (chiefly by opening new stores, attracting more members at both new and existing stores, and endeavoring to grow sales revenues and shopper traffic at existing stores). The industry is becoming somewhat mature (which strengthens rivalry); achieving fast revenue growth is heavily dependent on the speed with which rivals open new stores and grow sales at existing stores.

• Low switching costs on the part of consumers (membership fees were very similar from club to club). In large metropolitan areas with stores of two or more of the 3 competitors, it is easy for households and businesses to switch their memberships from one club to another (or to belong to both and then shop at whichever club had the best deals).

• Weak to modest degrees of product line differentiation from club to club. There is considerable similarity in the merchandise offerings of all three clubs (which enhances rivalry).

Factors that might be cited as making rivalry weaker include:

• The differentiation that does exist among the 3 warehouse club rivals —some bargain-hunting shoppers are definitely likely to prefer one club to another when they have multiple clubs to choose from in their shopping area. Preferences or loyalty to one club versus another makes members somewhat less prone to switch to rival clubs and thereby acts to weaken rivalry.

But this one factor is not powerful enough to overcome the combination of factors acting to strengthen rivalry.

■ Threat of entry into the warehouse club industry in North America— a weak competitive force

In assessing this competitive force, students should draw upon the information in Figure 3.5 on p. 62 of Chapter 3 (and the related text discussion on pp. 59-61.

From our perspective, the window for entering the North American warehouse club industry is pretty much closed—unless an outsider opted to acquire BJ’s Wholesale Club with the intention of rapidly expanding into areas and states where there are currently no BJ’s locations (Target might be a possible entry candidate).

The barriers to a new entrant are quite high:

• Costco and Sam’s have to be considered formidable competitors and enjoy sizable scale economies not easily accessed by a newcomer.

• Capital requirements are sizable—if an entrant wishes to compete on a scale comparable to the industry incumbents.

• The marketing and advertising costs to attract members and build a significant volume of sales (and otherwise overcome the loyalty of existing warehouse club members) would seem to be significant. Why, for example, would a Costco member want to switch to an industry newcomer? Overcoming member switching costs would be an uphill struggle of considerable proportions.

Moreover, the three industry incumbents are in a strong position to vigorously contest a newcomer’s entry.

Conclusions concerning the threat of entry. All things considered, a newcomer’s prospects for attractive profitability appear slim indeed. This is a low-margin business to begin with (with profits coming chiefly from membership fees). BJ’s Wholesale does not seem to be a very attractive acquisition candidate for an outsider. What outside company (besides perhaps Target---and that is a big perhaps) really would want to come in to this industry and do battle head-to-head with Costco and Sam’s in such a low-margin industry? It makes little or no business sense.

In short, the pool of candidates for fresh entry into warehouse club industry is small and the likelihood of entry in 2001 and beyond is equally small, making the competitive pressures from the threat of new entry virtually non-existent.

■ Competition from substitutes— a strong to fierce competitive force

In assessing this competitive force, students should draw upon in Figure 3.6 on p. 64 of Chapter 3 and also the related discussion on p. 63.

Students should quickly recognize that small business and individuals/households have hordes of substitutes for shopping at warehouse clubs. While the prices of substitute retailers may not be quite as low, the range of merchandise selection is far greater and the number of convenient store locations of these substitute retailers is overwhelming greater. Even the members of warehouse clubs buy a considerable fraction of what they need from other types of retail/discount outlets.

Students should conclude that the substitutes for being a member of and shopping at wholesale clubs are a relatively strong competitive force, given that

• Acceptable substitutes are readily available.

• Buyer costs to switch to substitutes are minimal (except for the higher prices that may have to be paid).

• Many consumers are familiar with and comfortable with shopping at substitute retailers/discounters.

• The merchandise that can be purchased at substitute retailers/discounters is quite comparable to the merchandise sold by wholesale clubs.

■ The bargaining power and leverage of suppliers to the warehouse club industry— a moderate to weakcompetitive force.

In assessing this competitive force, students should refer to Figure 3.7 and the related discussion on pp. 65-67 of Chapter 3.

The suppliers consist mainly of the manufacturers of the products that warehouse clubs elect to stock. While a big fraction of these manufacturers are undoubtedly large enterprises with well-recognized brand names and good reputations among consumers, they are not necessarily in a strong bargaining position that allows them to dictate the terms and conditions on which they will sell their wares to the warehouse clubs.

Costco and Sam’s, in particular, have considerable buying power and bargaining leverage in obtaining the merchandise they desire to stock. If a particular manufacturer chooses not to sell to the wholesale clubs at an attractively low price (such that the clubs can, in turn, charge what are perceived by members as “bargain prices” and save their members money), they can purchase goods for their stores from other more willing and price competitive sources. In Costco’s case, no single manufacturer supplied a large percentage of the merchandise that Costco stocked (which lessens any one manufacturer’s bargaining power). Moreover, because the items that the wholesale clubs stock produce high volumes of sales for manufacturers, manufacturers tend to be anxious to sell their goods to the wholesale clubs—in other words, the wholesale clubs are big volume buyers and thus have substantial bargaining clout with their suppliers. Costco management believed that if its current sources of supply became unavailable (for reasons of high supply prices or whatever), the company could switch its purchases to alternative manufacturers without experiencing a substantial disruption of its business—such ease of switching suppliers weakens supplier bargaining power and strengthens the bargaining power of a wholesale club.

Conclusion: The suppliers to the wholesale clubs tend to be a relatively weak competitive force—weak in the sense of being unable to put much pressure on their wholesale club customers in negotiating for better/higher prices and other more favorable terms of sale.

■ The bargaining power and leverage of customers (the members of wholesale clubs)— a very weak competitive force

In assessing this competitive force, students should refer to Figure 3.7 and the related discussion on pp. 67-70 of Chapter 3.

Wholesale club members buy in relatively small quantities; no single member accounts for a meaningful fractions of a wholesale club’s total sales. Consequently, individual members of wholesale clubs have essentially no power or leverage to bargain with a wholesale club over the prices they will pay or over other terms and conditions of sale. A member can certainly not purchase a particular item (and obtain it for another retailer/discounter) and can also choose not to renew their membership, but this does not convey any bargaining power of consequence (any customer of any company in any industry can always refuse to purchase and take their business elsewhere). So even though a member’s switching costs are relatively low, it does not result in having the clout to go to the Customer Service desk and bargain down a club’s posted price on an item or otherwise obtain any benefit beyond what their membership card provides.

In perusing all the factors that result in strong buyer bargaining power (discussed on pp. 67-70 and summarized in Figure 3.8), class members should conclude that wholesale clubs face little to no competitive pressure of any consequence stemming from the bargaining power of their members. In support of this position, they can argue that:

• Buyers/members are small, numerous, and buy in relatively small quantities.

• There’s no evidence indicating that clubs are frequently so overstocked with certain merchandise that a single member is able to bargain down the posted price of overstocked items.

■ Conclusions concerning the overall strength of competitive forces: Competitive pressures associated with rivalry and substitutes are definitely the two strongest of the five competitive forces. Competitive pressures from the other three competitive forces are weak. On the whole, competitive pressures confronting wholesale clubs are “normal” or reasonable—not so strong as to unduly crimp profit margins but certainly strong enough to prevent wholesale clubs from earning well above-average profits and attracting outsiders to entry the industry. To some large extent, the competitive market success of a wholesale club is a function of keeping its costs to buy goods and operate its stores low enough to be able to charge “bargain prices”, attract new members, and still achieve acceptable profitability.

Add Answer to:

What is competition like in the North American wholesale club industry? Which of the five competitive...

1. What core values or business principles did Jim Sinegal stress at Costco? 2. (In the event you have covered Chapter 3...

1. What core values or business principles did Jim Sinegal stress at Costco? 2. (In the event you have covered Chapter 3) What is competition like in the North American wholesale club industry? Which of the five competitive forces is strongest and why? Use the information in Figures 3.4, 3.5, 3.6, 3.7, and 3.8 (and the related discussions) in Chapter 3 to do a complete five-forces analysis of competition in the North American wholesale club industry. 3. How well is...

Chapter 3: Exercises for Simulation Participants If you are participating in a strategy simulation exercise during...

Chapter 3: Exercises for Simulation Participants If you are participating in a strategy simulation exercise during the academic term, you may be instructed to complete the following exercise. 1. Which of the five competitive forces is creating the strongest competitive pressures for your company? Multiple Choice There is not one competitive force that is strong enough to require a strategy change. Companies should not be concerned with entry barriers; these are always strong enough to prevent new entrants. Any one...

In The Five Competitive Forces That Shape Industry Competition, Porter identifies customer switching costs as one...

In The Five Competitive Forces That Shape Industry Competition, Porter identifies customer switching costs as one of the barriers to entry into an industry. The specific example that resonated with my work situation was about ERP software: “Enterprise resource planning (ERP) software is an example of a product with very high switching costs. Once a company has installed SAP’s ERP system, for example, the costs of moving to a new vendor are astronomical because of embedded data, the fact that...

ASSIGNMENT QUESTIONS 1. What is competition like in the North American wholesale club industry? Which of the five competitive forces is strongest and why? Use the information in Figures 3.3, 3.4, 3.5, 3.6, and 3.7 (and the related chapter discussions on p

Case work need answers xC

List the five primary dimensions of timely access. List external forces identified in the environmental scan...

List the five primary dimensions of timely access.

List external forces identified in the environmental scan of a

SWOT analysis.

In chapter 2, as you read the Bradley Park Hospital story,

consider question #2.4: Why do you think that by addressing quality

issues, you can positively impact the financial situation at BPH?

Why is Mike Chambers not attacking the other competitive

priorities?

Explain the principles of Lean.

In chapter 6, as you read the Bradley Park Hospital story,

consider question...

List the five primary dimensions of timely access.

List external forces identified in the environmental scan of a

SWOT analysis.

In chapter 2, as you read the Bradley Park Hospital story,

consider question #2.4: Why do you think that by addressing quality

issues, you can positively impact the financial situation at BPH?

Why is Mike Chambers not attacking the other competitive

priorities?

Explain the principles of Lean.

In chapter 6, as you read the Bradley Park Hospital story,

consider question...

What happened on United flight 3411?What service expectations do customers have of airlines such ...

What happened on United flight 3411?What service expectations

do customers have of airlines such as United and How did these

expectations develop over time?

Thank You!

In early April 2017, United Airlines (United), one of the largest airlines in the world, found itself yet again in the middle of a service disaster this time for forcibly dragging a passenger off an overbooked flight. The incident was to become a wake-up call for United, forcing it to ask itself what to...

What happened on United flight 3411?What service expectations

do customers have of airlines such as United and How did these

expectations develop over time?

Thank You!

In early April 2017, United Airlines (United), one of the largest airlines in the world, found itself yet again in the middle of a service disaster this time for forcibly dragging a passenger off an overbooked flight. The incident was to become a wake-up call for United, forcing it to ask itself what to...

Carlsberg in Emerging Markets A breeze of optimism blew through the office of Carlsberg A/S’s CEO,...

Carlsberg in Emerging Markets A breeze of optimism blew through the office of Carlsberg A/S’s CEO, Jørgen Buhl Rasmussen. After finally gaining 100 percent control over the giant Russian brewery Baltic Beverages Holding (BBH), and with the investments in Western China beginning to bear fruit, the newly appointed CEO was confident that the Danish brewing company’s intensified focus on emerging markets would pay off. The company was counting on tapping the massive potential in emerging markets in order to achieve...

Chapter overview 1. Reasons for international trade Resources reasons Economic reasons Other reasons 2. Difference between...

Chapter overview 1. Reasons for international trade Resources reasons Economic reasons Other reasons 2. Difference between international trade and domestic trade More complex context More difficult and risky Higher management skills required 3. Basic concept s relating to international trade Visible trade & invisible trade Favorable trade & unfavorable trade General trade system & special trade system Volume of international trade & quantum of international trade Commodity composition of international trade Geographical composition of international trade Degree / ratio of...

Discussion questions 1. What is the link between internal marketing and service quality in the ai...

Discussion questions

1. What is the link between internal marketing and service

quality in the airline industry?

2. What internal marketing programmes could British Airways

put into place to avoid further internal unrest? What potential is

there to extend auch programmes to external partners?

3. What challenges may BA face in implementing an internal

marketing programme to deliver value to its customers?

(1981)ǐn the context ofbank marketing ths theme has bon pururd by other, nashri oriented towards the identification of...

Discussion questions

1. What is the link between internal marketing and service

quality in the airline industry?

2. What internal marketing programmes could British Airways

put into place to avoid further internal unrest? What potential is

there to extend auch programmes to external partners?

3. What challenges may BA face in implementing an internal

marketing programme to deliver value to its customers?

(1981)ǐn the context ofbank marketing ths theme has bon pururd by other, nashri oriented towards the identification of...

4. Perform a SWOT analysis for Fitbit. Based on your assessment of these, what are some strategic options for Fitbit go...

4. Perform a SWOT analysis for Fitbit. Based on your

assessment of these, what are some strategic options for Fitbit

going forward?

5. Analyze the company’s financial performance. Do trends

suggest that Fitbit’s strategy is working?

6.What recommendations would you make to Fitbit management to

address the most important strategic issues facing the

company?

Fitbit, Inc., in 2017: Can Revive Its Strategy and It Reverse Mounting Losses? connect ROCHELLE R. BRUNSON Baylor University MARLENE M. REED Baylor University in the...

4. Perform a SWOT analysis for Fitbit. Based on your

assessment of these, what are some strategic options for Fitbit

going forward?

5. Analyze the company’s financial performance. Do trends

suggest that Fitbit’s strategy is working?

6.What recommendations would you make to Fitbit management to

address the most important strategic issues facing the

company?

Fitbit, Inc., in 2017: Can Revive Its Strategy and It Reverse Mounting Losses? connect ROCHELLE R. BRUNSON Baylor University MARLENE M. REED Baylor University in the...

List the five primary dimensions of timely access.

List external forces identified in the environmental scan of a

SWOT analysis.

In chapter 2, as you read the Bradley Park Hospital story,

consider question #2.4: Why do you think that by addressing quality

issues, you can positively impact the financial situation at BPH?

Why is Mike Chambers not attacking the other competitive

priorities?

Explain the principles of Lean.

In chapter 6, as you read the Bradley Park Hospital story,

consider question...

List the five primary dimensions of timely access.

List external forces identified in the environmental scan of a

SWOT analysis.

In chapter 2, as you read the Bradley Park Hospital story,

consider question #2.4: Why do you think that by addressing quality

issues, you can positively impact the financial situation at BPH?

Why is Mike Chambers not attacking the other competitive

priorities?

Explain the principles of Lean.

In chapter 6, as you read the Bradley Park Hospital story,

consider question...

What happened on United flight 3411?What service expectations

do customers have of airlines such as United and How did these

expectations develop over time?

Thank You!

In early April 2017, United Airlines (United), one of the largest airlines in the world, found itself yet again in the middle of a service disaster this time for forcibly dragging a passenger off an overbooked flight. The incident was to become a wake-up call for United, forcing it to ask itself what to...

What happened on United flight 3411?What service expectations

do customers have of airlines such as United and How did these

expectations develop over time?

Thank You!

In early April 2017, United Airlines (United), one of the largest airlines in the world, found itself yet again in the middle of a service disaster this time for forcibly dragging a passenger off an overbooked flight. The incident was to become a wake-up call for United, forcing it to ask itself what to...

Discussion questions

1. What is the link between internal marketing and service

quality in the airline industry?

2. What internal marketing programmes could British Airways

put into place to avoid further internal unrest? What potential is

there to extend auch programmes to external partners?

3. What challenges may BA face in implementing an internal

marketing programme to deliver value to its customers?

(1981)ǐn the context ofbank marketing ths theme has bon pururd by other, nashri oriented towards the identification of...

Discussion questions

1. What is the link between internal marketing and service

quality in the airline industry?

2. What internal marketing programmes could British Airways

put into place to avoid further internal unrest? What potential is

there to extend auch programmes to external partners?

3. What challenges may BA face in implementing an internal

marketing programme to deliver value to its customers?

(1981)ǐn the context ofbank marketing ths theme has bon pururd by other, nashri oriented towards the identification of...

4. Perform a SWOT analysis for Fitbit. Based on your

assessment of these, what are some strategic options for Fitbit

going forward?

5. Analyze the company’s financial performance. Do trends

suggest that Fitbit’s strategy is working?

6.What recommendations would you make to Fitbit management to

address the most important strategic issues facing the

company?

Fitbit, Inc., in 2017: Can Revive Its Strategy and It Reverse Mounting Losses? connect ROCHELLE R. BRUNSON Baylor University MARLENE M. REED Baylor University in the...

4. Perform a SWOT analysis for Fitbit. Based on your

assessment of these, what are some strategic options for Fitbit

going forward?

5. Analyze the company’s financial performance. Do trends

suggest that Fitbit’s strategy is working?

6.What recommendations would you make to Fitbit management to

address the most important strategic issues facing the

company?

Fitbit, Inc., in 2017: Can Revive Its Strategy and It Reverse Mounting Losses? connect ROCHELLE R. BRUNSON Baylor University MARLENE M. REED Baylor University in the...

Most questions answered within 3 hours.

-

Suppose that XX is a random variable with mean 16 and standard

deviation 5 . Also...

asked 25 minutes ago -

Calculate the number density of argon gas at a temperature of

24C and a pressure of...

asked 3 hours ago -

Alternative

Classification

How to Estimate

Probabilities from Data? ( For continuous Attributes)

And How to generate...

asked 3 hours ago -

An explosion breaks a 20.0-kg object into three parts. The

object is initially moving at a...

asked 4 hours ago -

Calculate the approximate number of residues of Rubisco, which

is involved in carbon fixation in plants,...

asked 5 hours ago -

Other decisions about scientific claims can have a much broader

impact.ENERGYarrow-10x10.png, environment, health, security - all...

asked 6 hours ago -

I need to write a research paper and work cited about this

topic: The United States...

asked 6 hours ago -

Hello! I was wondering if I could have some help?

If the vapor pressure of carvone...

asked 7 hours ago -

An economist wants to estimate the mean per capita income (in

thousands of dollars) for a...

asked 7 hours ago -

What would be the input/output characteristic of a circuit

obtained by putting two of your 2's-complementers...

asked 7 hours ago -

In Drosophila, the transition from the syncytial blastoderm

stage to the cellular blastoderm stage is a...

asked 7 hours ago -

Project management question:

Name 3 different types of resources (hint: humans are one

type)

asked 8 hours ago