Assume that you are auditing Paradox, Inc., a manufacturer of hand-held personal digital assistants (PDAs). The...

Assume that you are auditing Paradox, Inc., a manufacturer of hand-held personal digital assistants (PDAs). The following is information that you have extracted from the audit working papers. • The market for PDAs is very competitive with several companies battling for market share, which in turn has put downward pressure on profit margins. • Rapid advances in technology have further reduced the product life cycle. In the race to remain competitive a number of companies, including Paradox, have significantly increased their research and development efforts. • Funding the increased R&D has been a growing concern for Paradox. The company currently is actively seeking capital. • Paradox is a public company listed on the NASDAQ exchange. Top management’s compensation is heavily tied to the company’s profitability. • The company does not have an internal audit function and the audit committee has not been very diligent in the past.

1. What are your responsibilities to make sure the financial statements are free from material misstatement?

2. How will SAS No. 99 affect the procedures you will perform for this audit?

3. SAS No. 99 requires you to conduct a discussion among engagement team personnel. Based on the background information provided, what “insights” would you share with the other audit team members? Describe your insights in terms of the three characteristics of fraud, incentive, and rationalization.

4. When performing field work, you find that in responding to an accounts receivable confirmation, a customer notes that the receivable relates to a purchase that was made under the company’s “new extended return policy” and the customer is still deciding whether to keep the items purchased. How does this new information affect your fraud risk assessments? How should you respond to this situation?

Homework Answers

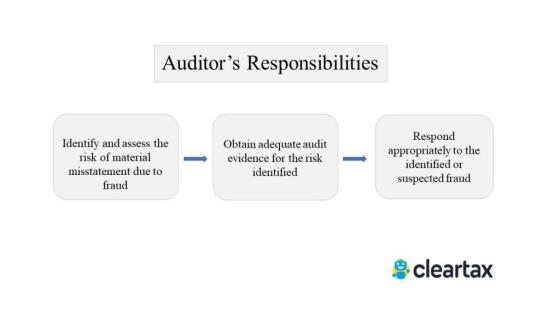

SA 240 – The Auditor’s Responsibility Relating to Fraud In An Audit Of Financial Statements

SA 240 deals with the auditor’s responsibilities towards frauds in the financial statement audits. It explains how the material misstatements in the financials due to fraud can be identified, assessed and appropriate procedures to detect can be implemented.

Auditor’s objectives with respect to the financial statements misstatements are as follows:

Following are the Auditor’s responsibilities here:

- Obtain reasonable assurance that the financial statements are free from material misstatements

- Maintain professional skepticism throughout the audit

- Should know that Risk of non-detection of management fraud is greater than of employee fraud

- Must be aware Risk of non-detection of fraudulent material misstatement is higher than the misstatement due to error.

2. SAS NO 99

Describes fraud and its characteristics.Edit

SAS 99 defines fraud as an intentional act that results in a material misstatement in financial statements. There are two types of fraud considered: misstatements arising from fraudulent financial reporting (e.g. falsification of accounting records) and misstatements arising from misappropriation of assets (e.g. theft of assets or fraudulent expenditures). The standard describes the fraud triangle. Generally, the three 'fraud triangle' conditions are present when fraud occurs. First, there is an incentive or pressure that provides a reason to commit fraud. Second, there is an opportunity for fraud to be perpetrated (e.g. absence of controls, ineffective controls, or the ability of management to override controls.) Third, the individuals committing the fraud possess an attitude that enables them to rationalize the fraud.

Requires 'brainstorming' sessions to discuss how and where the entity's financial statements might be susceptible to material misstatement due to fraud.Edit

This requirement is a new concept in audit standards and it has two primary objectives. The first objective is so the engagement team will have an opportunity for the seasoned team members to share their experiences with the client and how a fraud might be perpetrated and concealed. The second objective is to set the proper "tone at the top" for conducting the engagement. The brainstorming session is to be conducted in a manner that models the proper degree of professional skepticism and sets the culture for the entire audit.

Requires the auditor to gather information necessary to identify risks of material misstatement due to fraud by the followingEdit

- Making inquiries of management and others within the entity

- Considering the results of analytical procedures performed in planning the audit.

- Considering fraud risk factors.

- Considering certain other information

SAS 99 requires auditors to ask management questions about their awareness and understanding of fraud. Auditors will then make a decision as to whether they need to 'educate' management about fraud and the types of controls that will deter and detect fraud. The standard also requires auditors to make inquiries of the audit committee, internal audit personnel and others within the entity.

Requires the auditor to use the information gathered to identify risks that may result in a material misstatement.Edit

This section provides guidance and support on how to identify and assess risks. It challenges auditors to change the way they think about assessing fraud risks. Auditors should identify risks and synthesize how those risks could lead to a material misstatement. This section specifically requires that improper revenue recognition and management override of controls be considered.

Requires the auditor to evaluate the entity's programs and controls that address the identified risks of material misstatement.Edit

SAS 99 provides specific examples of programs and controls for both large and small businesses. The auditor should consider which controls mitigate the identified fraud risks.

Requires the auditor to assess the risks of material misstatement due to fraud throughout the audit and to evaluate at the completion of the audit whether the accumulated results of auditing procedures and other observations affect the assessment.Edit

The standard provides examples of conditions that may be identified during the audit that might indicate fraud. One example is management denying the auditors access to key IT operations staff including security, operations, and systems development personnel. The auditors must determine whether the results of their tests affect their assessment.

Provides guidance regarding the auditor's communications about fraud to management, the audit committee, and others.Edit

The standard requires that any evidence that fraud may exist must be communicated to management and others. The level of severity is insignificant.

Describes documentation requirements.Edit

SAS 99 significantly extends the documentation requirements of the previous standard. Auditors must document: (1) how and when the brainstorming session occurred and who participated, (2) procedures performed to obtain information to identify and assess fraud risk, (3) specific risks of material misstatement due to fraud (must specifically include discussion of revenue recognition) and the auditor's response to those risks, (4) results of the procedures performed to address the risk of management override of controls, (5) conditions and analytical relationships that led to additional audit procedures or other responses, and (6) nature of communications about fraud made to management and others.

3.

SAS no. 99 requires the audit team to discuss the potential for a material misstatement in the financial statements due to fraud before and during the information-gathering process. This required “brainstorming” is a new concept in auditing literature, and early in the adoption process firms will need to decide how best to implement this requirement in practice. Keep in mind that brainstorming is a required procedure and should be applied with the same degree of due care as any other audit procedure.

There are two primary objectives of the brainstorming session. The first is strategic in nature, so the engagement team will have a good understanding of information that seasoned team members have about their experiences with the client and how a fraud might be perpetrated and concealed.

| The second objective of the session is to set the proper “tone

at the top” for conducting the engagement. The requirement that

brainstorming be conducted with an attitude that “includes a

questioning mind” is an attempt to model the proper degree of

professional skepticism and “set” the culture for the engagement.

The belief is that such an audit engagement culture will infuse the

entire engagement, making all audit procedures that much

more effective.

The mere fact the engagement team has a serious discussion about the entity’s susceptibility to fraud also serves to remind auditors that the possibility does exist in every engagement—in spite of any history or preconceived biases about management’s honesty and integrity. 4. In this case the customer must be provided with adequate information about the new requirements of the company in order to avoid fraud. If he is not aware of new return policy he made transactions in a manner which leafs to fraud. So in order to avoid this customers must be informed about all information regarding the purchases made by them. |

Add Answer to:

Assume that you are auditing Paradox, Inc., a manufacturer of hand-held personal digital assistants (PDAs). The...

Case 14-6 Making Connections Social Konnections Inc. (SKI or the “Company”) is a global Internet company...

Case 14-6 Making Connections Social Konnections Inc. (SKI or the “Company”) is a global Internet company that runs Social Konnections, a large social media networking Web site. SKI has experienced steep growth since its launch in 2005, and the Company went public in 2010. SKI currently has over 500 million active users who visit the site to connect with others, express themselves, and play games. Last year, substantially all of SKI’s revenue came from advertisers who market their products and...

ETHICAL DILEMMA You are the Controller for AJAX, Inc., a large regional manufacturer of widgets. The...

ETHICAL DILEMMA You are the Controller for AJAX, Inc., a large regional manufacturer of widgets. The CFO comes to you and says the earnings results for the quarter ending June 30, 2019, are 20 percent below financial analysts’ estimates. As a public company, you know the stock price is likely to decline, perhaps significantly, after public disclosure of the earnings reduction for the second straight quarter in 2019. Competitive pressures and a difficult economic environment have already placed great strain...

AUDITING & ASSURANCE SERVICES PAPER AdoreU Children Fashion Ltd – Mini Audit Project QUESTIONS Part A:...

AUDITING & ASSURANCE SERVICES PAPER AdoreU Children Fashion Ltd – Mini Audit Project QUESTIONS Part A: Professional Ethics and Audit Planning BACKGROUND INFORMATION Wallace & Davey Partners, Chartered Accountants is a medium size accounting firm located in Auckland with four audit partners, seven business advisory partners and four tax partners. The firm has been appointed to audit AdoreU Children Fashion Ltd for the year ended 31 December 2018. The former auditor has been rotated off the client. The engagement partner...

King Companies, Inc. (KCI) is a private company that owns five auto parts stores in urban...

King Companies, Inc. (KCI) is a private company that owns five auto parts stores in urban Los Angeles, California. KCI has expanded from two auto parts stores to five stores in the last three years, and it plans continued growth. Eric and Patricia King own the majority of the shares in KCI. Eric is the chairman of the board of directors and CEO of KCI, and Patricia is a director as well as the CFO. Shares not owned by Eric...

It is August 2018. You are the manager on the audit of The Sophisticated Listener, Inc....

It is August 2018. You are the manager on the audit of The Sophisticated Listener, Inc. (TSL) a company that until recently had operated a large retail store in Lindsay selling CDs and music accessories. George, the managing director and principal shareholder of TSI, has for some time held the view that the future of the retail trade lies in the potential offered by Internet shopping. Shortly after its year end, December 31, 2017, the company closed its retail store...

It is August 2018. You are the manager on the audit of The Sophisticated Listener, Inc. (TSL) a company that until recently had operated a large retail store in Lindsay selling CDs and music accessories. George, the managing director and principal shareholder of TSI, has for some time held the view that the future of the retail trade lies in the potential offered by Internet shopping. Shortly after its year end, December 31, 2017, the company closed its retail store...

It is August 2018. You are the manager on the audit of The Sophisticated Listener, Inc....

It is August 2018. You are the manager on the audit of The Sophisticated Listener, Inc. (TSL) a company that until recently had operated a large retail store in Lindsay selling CDs and music accessories. George, the managing director and principal shareholder of TSL, has for some time held the view that the future of the retail trade lies in the potential offered by Internet shopping. Shortly after its year end, December 31, 2017, the company closed its retail store...

It is August 2018. You are the manager on the audit of The Sophisticated Listener, Inc. (TSL) a company that until recently had operated a large retail store in Lindsay selling CDs and music accessories. George, the managing director and principal shareholder of TSL, has for some time held the view that the future of the retail trade lies in the potential offered by Internet shopping. Shortly after its year end, December 31, 2017, the company closed its retail store...

2019 Audit of Beta Industries: Summary Information Assume you are an audit manager, today is May...

2019 Audit of Beta Industries: Summary

Information

Assume you are an audit manager, today is May 15, 2019, and your

public accounting firm is currently planning the 2019 financial

statement audit of Beta Home Goods, a retailer in the home goods

and supply industry. Beta is a public company with a 12/31

year-end, and a new client for your firm. The audit partner has

asked you to help plan the audit for this new client using the

following information obtained...

2019 Audit of Beta Industries: Summary

Information

Assume you are an audit manager, today is May 15, 2019, and your

public accounting firm is currently planning the 2019 financial

statement audit of Beta Home Goods, a retailer in the home goods

and supply industry. Beta is a public company with a 12/31

year-end, and a new client for your firm. The audit partner has

asked you to help plan the audit for this new client using the

following information obtained...

Read the Janes' Electronics, Inc. case at the end of the exam and answer the following...

Read the Janes' Electronics, Inc. case at the end of the exam and answer the following questions. Assume that you are preparing to bid on the audit and are working on your client acceptance issues. Develop a checklist of five areas or issues that you would want to research before you accepted this firm as an audit client. For each area or issue, explain why you would want to research it and give an example of where you might go...

Unhealthy Accounting at HealthSouth PROBLEM In 1996, key executives of HealthSouth, one of the nation’s largest...

Unhealthy Accounting at HealthSouth PROBLEM In 1996, key executives of HealthSouth, one of the nation’s largest providers of health care services, began a massive fraud that eventually amounted to $2.7 billion. HealthSouth is a textbook case of unbridled greed combined with a lack of corporate governance, which illustrates the difficult situation that auditors face when clients perpetrate a massive, collusive fraud. HealthSouth was founded in 1984 by Richard Scrushy and coworkers at Lifemark, a Houston-based company that owned and managed...

Case Study Analysis: Fred Stern & Company, Inc. (Knapp): In the business world of the Roaring...

Case Study Analysis: Fred Stern & Company, Inc. (Knapp): In the business world of the Roaring Twenties, the schemes and scams of flimflam artists and confidence men were legendary. The absence of a strong regulatory system at the federal level to police the securities markets—the Securities and Exchange Commission was not established until 1934—aided, if not encouraged, financial frauds of all types. In all likelihood, the majority of individuals involved in business during the 1920s were scrupulously honest. Nevertheless, the...

It is August 2018. You are the manager on the audit of The Sophisticated Listener, Inc. (TSL) a company that until recently had operated a large retail store in Lindsay selling CDs and music accessories. George, the managing director and principal shareholder of TSI, has for some time held the view that the future of the retail trade lies in the potential offered by Internet shopping. Shortly after its year end, December 31, 2017, the company closed its retail store...

It is August 2018. You are the manager on the audit of The Sophisticated Listener, Inc. (TSL) a company that until recently had operated a large retail store in Lindsay selling CDs and music accessories. George, the managing director and principal shareholder of TSI, has for some time held the view that the future of the retail trade lies in the potential offered by Internet shopping. Shortly after its year end, December 31, 2017, the company closed its retail store...

It is August 2018. You are the manager on the audit of The Sophisticated Listener, Inc. (TSL) a company that until recently had operated a large retail store in Lindsay selling CDs and music accessories. George, the managing director and principal shareholder of TSL, has for some time held the view that the future of the retail trade lies in the potential offered by Internet shopping. Shortly after its year end, December 31, 2017, the company closed its retail store...

It is August 2018. You are the manager on the audit of The Sophisticated Listener, Inc. (TSL) a company that until recently had operated a large retail store in Lindsay selling CDs and music accessories. George, the managing director and principal shareholder of TSL, has for some time held the view that the future of the retail trade lies in the potential offered by Internet shopping. Shortly after its year end, December 31, 2017, the company closed its retail store...

2019 Audit of Beta Industries: Summary

Information

Assume you are an audit manager, today is May 15, 2019, and your

public accounting firm is currently planning the 2019 financial

statement audit of Beta Home Goods, a retailer in the home goods

and supply industry. Beta is a public company with a 12/31

year-end, and a new client for your firm. The audit partner has

asked you to help plan the audit for this new client using the

following information obtained...

2019 Audit of Beta Industries: Summary

Information

Assume you are an audit manager, today is May 15, 2019, and your

public accounting firm is currently planning the 2019 financial

statement audit of Beta Home Goods, a retailer in the home goods

and supply industry. Beta is a public company with a 12/31

year-end, and a new client for your firm. The audit partner has

asked you to help plan the audit for this new client using the

following information obtained...

Most questions answered within 3 hours.

-

Question 5

What effect would a decrease in

temperature have on pressure, assuming that volume

(T)...

asked 1 minute from now -

Jor-el throws a ball upward from the top of a 728 foot building

on the planet...

asked 1 minute ago -

Draw the Lewis dot structures for the following molecules. None

of the atoms have a formal...

asked 3 minutes ago -

What does it mean when an element is radioactive?

a.

It means the element is changing...

asked 3 minutes ago -

A company deposits $6,000 in a bank at the end of every year for

10 years....

asked 3 minutes ago -

What are some strategies for eliminating service barriers?

By using your knowledge of

behavioral styles, please...

asked 11 minutes ago -

What are the decimal numbers for 159, 150, 200, 113, 225, 87,

106, 81 when converted...

asked 19 minutes ago -

Calculate and plot the number and weight distributions of x-mers

found in a step-growth polymerization for...

asked 39 minutes ago -

The Baily Corporation has developed a specialized software

program that improves inventory control capability. The following...

asked 42 minutes ago -

Problem 5-4A (Part Level Submission) Wolford Department Store is

located in midtown Metropolis. During the past...

asked 43 minutes ago -

Preparation of Benzoic Acid using a Grignard Reagent URGENT

1. During your Grignard formation, a small...

asked 1 hour ago -

A uniform magnetic field is perpendicular to the plane of a wire

loop. If the loop...

asked 1 hour ago