Homework Answers

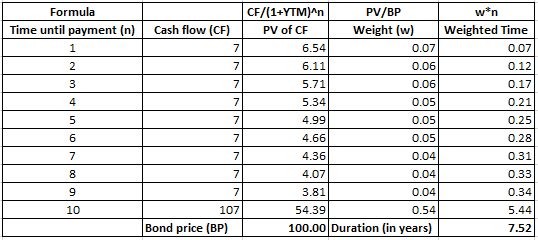

a). Duration = 7.515 years; Convexity = 64.933

Convexity calculation:

Convexity = 7,434.17/(Price*(1+y)^2) = 7,434.17/(100*(1+7%)^2) = 64.933

b). Actual price with YTM 8%: FV = 100; PMT = 70; N = 10; rate = 8%, solve for PV.

Price = 93.29

c). Modified duration (D*) = duration/(1+y) = 7.515/(1+0.07) = 7.02

Change in Price = - Price*(d*)*change in yield = -100*7.02*0.01 = -7.02

New price = 100 -7.02 = 92.98

%age price change = (new price/old price) -1 = (92.98/100) -1 = -7.02%

%age error = (predicted price-actual price)/actual price = (92.98/93.29)-1 = -0.34%

d). Change in price = Price*[(-D**change in yield) + 0.5*(Convexity*change in yield^2)]

= 100*[(-7.02*0.01) + 0.5*(64.933*0.01^2)] = -6.70

New price = 100 - 6.70 = 93.30

%age price change = (93.30/100) -1 = -6.70%

%age error = (93.30/93.29) -1 = 0.01%

Add Answer to:

A newly issued bond has a maturity of 10 years and pays a 7% coupon rate...

A newly issued bond has a maturity of 10 years and pays a 7.7% coupon rate...

A newly issued bond has a maturity of 10 years and pays a 7.7% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. (Round your answers to 3 decimal places.) Convexity - 61.810 Duration - 7.330 Years b. Find the actual price of the bond assuming that its yield to maturity immediately increases from 7.7% to...

A newly issued bond has a maturity of 10 years and pays a 7.4% coupon rate...

A newly issued bond has a maturity of 10 years and pays a 7.4% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. (Round your answers to 3 decimal places.) b. Find the actual price of the bond assuming that its yield to maturity immediately increases from 7.4% to 8.4% (with maturity still 10 years). Assume...

A newly issued bond has a maturity of 10 years and pays a 5.4% coupon rate...

A newly issued bond has a maturity of 10 years and pays a 5.4% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. (Round your answers to 3 decimal places.) b. Find the actual price of the bond assuming that its yield to maturity immediately increases from 5.4% to 6.4% (with maturity still 10 years). Assume...

A newly issued bond has a maturity of 10 years and pays a 5.5% coupon rate...

A newly issued bond has a maturity of 10 years and pays a 5.5% coupon rate (with coupon payments coming once annually). The bond sells at par value. a. What are the convexity and the duration of the bond? Use the formula for convexity in footnote 7. (Round your answers to 3 decimal places.) Answer is complete and correct. Convexity 724.31 Duration 7.95 years b. Find the actual price of the bond assuming that its yield to maturity immediately increases...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) F...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A 30-year maturity bond making annual coupon payments with a coupon rate of 7.5% has duration...

A 30-year maturity bond making annual coupon payments with a coupon rate of 7.5% has duration of 12.27 years and convexity of 216.28. The bond currently sells at a yield to maturity of 8%. a. Find the price of the bond if its yield to maturity falls to 7%. (Do not round intermediate calculations. Round your answers to 2 decimal places.) b. What price would be predicted by the duration rule? (Do not round intermediate calculations. Round your answers to...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield)...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 139.2 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years--but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? il...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 139.2 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years--but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? il...

Question 1 A 12.58-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective...

Question 1 A 12.58-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 146.5 and modified duration of 11.65 years. A 30-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration—-11.79 years—-but considerably higher convexity of 231.2. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each...

A 30-year maturity bond making annual coupon payments with a coupon rate of 7.5% has duration...

A 30-year maturity bond making annual coupon payments with a coupon rate of 7.5% has duration of 12.27 years and convexity of 216.28. The bond currently sells at a yield to maturity of 8%. e-1. Find the price of the bond if its yield to maturity increases to 9%. (Do not round intermediate calculations. Round your answers to 2 decimal places.) e-2. What price would be predicted by the duration rule? (Do not round intermediate calculations. Round your answers to...

A 13.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield)...

A 13.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 161.9 and modified duration of 12.27 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration-12.30 years-but considerabl higher convexity of 272.9 a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? What...

A 13.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 161.9 and modified duration of 12.27 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration-12.30 years-but considerabl higher convexity of 272.9 a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? What...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 139.2 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years--but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? il...

A 12.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 139.2 and modified duration of 11.34 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration--12.30 years--but considerably higher convexity of 272.9. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? il...

A 13.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 161.9 and modified duration of 12.27 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration-12.30 years-but considerabl higher convexity of 272.9 a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? What...

A 13.25-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 161.9 and modified duration of 12.27 years. A 40-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration-12.30 years-but considerabl higher convexity of 272.9 a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each bond? What...

Most questions answered within 3 hours.

-

The average length of time between arrivals at a turnpike

toll-booth is 26 seconds. What is...

asked 52 minutes ago -

(a) A piston at 6.1 atm contains a gas that occupies a volume of

3.5 L....

asked 2 hours ago -

Please answer true or false. Words

cannot be changed or added in to make it true...

asked 2 hours ago -

An empty test tube weighs 15.923 grams. Then,

MgCl2•6H2O is added into the test tube. After...

asked 2 hours ago -

Assume memory access is 10 units of time and disk access is

10000 units of time....

asked 2 hours ago -

1. Are all good samples random?

2. Magazines often report surveys giving statistics such as “63%...

asked 2 hours ago -

Under all the various types of market structures, firms

must eventually earn some economic profits for...

asked 2 hours ago -

Consider the following fitness regime for a single locus trait

with two co-dominant alleles: w11 =...

asked 2 hours ago -

A large cable company reports the following.

80% of its customers subscribe to its cable TV...

asked 2 hours ago -

Please answer the question in brief.

Discuss the role of ERP in organizations. Are ERP tools...

asked 2 hours ago -

Discuss the pros and cons of collaborative software such

as SameTime. Does it increase productivity? What...

asked 2 hours ago -

Buying your in-laws a gift because it’s expected is

due to the ____________ motive of gift-giving....

asked 2 hours ago