1- Larry Davis borrows $73,000 at 12 percent interest toward the purchase of a home. His mortgage is for 30 years. Use Appendix D for an approximate answer, but calculate your final answer using the formula and financial calculator methods.

a. How much will his annual payments be? (Although home payments are usually on a monthly basis, we shall do our analysis on an annual basis for ease of computation. We will get a reasonably accurate answer.)

b. How much interest will he pay over the life of the loan?

c. How much should he be willing to pay to get out of a 12 percent mortgage and into a 10 percent mortgage with 30 years remaining on the mortgage? Assume current interest rates are 10 percent. Carefully consider the time value of money. Disregard taxes.

2- If you invest $9,300 per period for the following number of periods, how much would you have in each of the following instances? Use Appendix C for an approximate answer, but calculate your final answer using the formula and financial calculator methods.

a. In 11 years at 8 percent?

b. In 40 years at 7 percent?

3- Al Rosen invests $23,000 in a mint condition 1952 Mickey Mantle Topps baseball card. He expects the card to increase in value 11 percent per year for the next 12 years.

How much will his card be worth after 12 years? Use Appendix A for an approximate answer, but calculate your final answer using the formula and financial calculator methods.

4- Carrie Tune will receive $32,500 for the next 15 years as a payment for a new song she has written. Use Appendix D for an approximate answer, but calculate your final answer using the formula and financial calculator methods.

a. What is the present value of these payments if the discount rate is 17 percent?

5-Maxwell Communications paid a dividend of $0.80 last year. Over the next 12 months, the dividend is expected to grow at 10 percent, which is the constant growth rate for the firm (g). The new dividend after 12 months will represent D1. The required rate of return (Ke) is 17 percent.

Compute the price of the stock (P0)

(1+i"-1 Future value of an annuity of $1, FV/FA Appendix C FV=A Percent 3% 4% Period 1% 2% 5% 6% 7% 8% 9% 10% 11% 1.000 1,000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 2.010 2.020 2.030 2.040 2.050 2.060 2.070 2.080 2.090 2.100 2.110 3.060 3.091 3.122 3.153 3.184 3.215 3.246 3.278 3.310 3.342 3.030 4,060 4.122 4.184 4.246 4,310 4.375 4.440 4.506 4.573 4.641 4.710 5.204 5.309 5.416 5.526 5.637 5.867 6.228 5.101 5.751 5.985 6.105 6.152 6.308 6.468 6.633 6.975 7.153 7.336 7.523 7.716 7.913 6 6.802 7.214 7.434 7.662 7.898 8.142 8.394 8.654 8.923 9.200 9.487 9.783 8.286 8.583 8.892 9.897 10.637 11.859 9.214 9.549 10.260 11.028 11.436 9.369 10.159 10.583 11.978 12.488 14.164 9.755 11.027 11.491 13.021 13.579 1C 10.462 10.950 11.464 12.006 12.578 13.181 13.816 14.487 15.193 15.937 16.722 17.560 11 11.567 12.169 12.808 13.486 14.207 14.972 15.784 16.645 18.531 19.561 12 12.683 13.412 14.192 15.026 15.917 16.870 17.888 18.977 20.141 21.384 22.713 13 13.809 14.680 15.618 16.627 17.713 18.882 20.141 21.495 22.953 24.523 26.212 14 14.947 15.974 17.086 18.292 19.599 21.015 22.550 24.215 26.019 27.975 30.095 15 16.097 17.293 18.599 20.024 21.579 23.276 25.129 27.152 29.361 31.772 34,405 16 17.258 18.639 20.157 21.825 23.657 25.673 27.888 30.324 33.003 35.950 39.190 20.012 21.762 23.698 30.840 33.750 36.974 44,501 18.430 25.840 28.213 40.545 18 19.615 21.412 23.414 25.645 28.132 30.906 33.999 37.450 41.301 45.599 50.396 1C 20.811 22.841 25.117 27.671 30.539 33.760 37.379 41.446 46.018 51.159 56.939 20 29.778 51.160 22.019 24.297 26.870 33.066 36.786 40.995 45.762 57.275 64.203 25 63.249 73.106 114,41 28.243 32.030 36.459 41.646 47.727 54.865 84.701 98.347 113.28 30 34.785 40.588 47.575 56.085 66.439 79.058 94.461 136.31 164.49 199.02 ис 48.886 75.401 95.026 154.76 199.64 259.06 442.59 581.83 60.402 120.80 337.89 50 209.35 64.463 84.579 112.80 152.67 290.34 406.53 573.77 815.08 1,163.9 1,668.8

Appendix C (concluded) Future value of an annuity of $1 Percent Period 12% 13% 14% 15% 16% 17% 18% 19% 20% 25% 30% 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1 2.120 2.130 2.140 2.150 2.160 2.170 2.180 2.190 2.200 2.250 2.300 3.374 3.407 3.440 3.473 3.506 3.539 3.572 3.606 3.640 3.813 3.990 5.368 6.187 4.779 4.850 4.921 4.993 5.066 5.14 5.215 5.291 5.766 6.353 6.480 6.610 6.742 6.877 7.014 7.154 7.297 7.442 8.207 9.043 8.115 8.323 8.536 8.754 8.977 9.207 9.442 9.683 9.930 11.259 12.756 10.089 11.772 10.405 10.730 11,067 11.414 12.142 12.523 12.916 15.073 17.583 12.300 12.757 13.233 13.727 14.240 14.773 15.327 15.902 16.499 19.842 23.858 14.776 15.416 16.085 16.786 17.519 18.285 19.086 19.923 20.799 25.802 32.015 10 17.549 18.420 19.337 20.304 21,321 22.393 23.521 24.701 25.959 33.253 42.619 11 20.655 21.814 23.045 24,349 25.733 27.200 28.755 30.404 32.150 42.566 56.405 12 24.133 25.650 27.271 29.002 30.850 32.824 34.931 37.180 39.581 54.208 74.327 28.029 34,352 48.497 13 29.985 32.089 36.786 39.404 42.219 45.244 68.760 97.625 14 32.393 34,883 37.581 40.505 43.672 47.103 50.818 54.841 59.196 86.949 127.91 15 37.280 40.417 43.842 47.580 51.660 56.110 60.965 66.261 72.035 109.69 167.29 87.442 16 42.753 46.672 50.980 55.717 60.925 66.649 72.939 79.850 138.11 218.47 17 71.673 48.884 53.739 59.118 65.075 78.979 87.068 96,022 105.93 173.64 285.01 18 55.750 61.725 68.394 75.836 84.141 93.406 103.74 115.27 128.12 218.05 371.52 19 63.440 70.749 78.969 88.212 98.603 110.29 123.41 138.17 154,74 273.56 483.97 20 72.052 80.947 91.025 102.44 115.38 130.03 146.63 165.42 186.69 342.95 630.17 25 133.33 155.62 181.87 212.79 249.21 292.11 342.60 402.04 471.98 1,054.8 2,348.80 30 241.33 293.20 356.79 434.75 530.31 647,44 790.95 966.7 1,181,9 3,227.2 8,730.0 40 767.09 1,013.7 1,342.0 1,779.1 2,360.8 3.134,5 4,163.21 5,529.8 7,343.9 30,089.0 120,393.0 50 2,400.0 3,459.5 4,994.5 7,217.7 10,436.0 15,090,0 21,813.0 31,515.0 45,497.0 280,256,0 1,659,76,0

FV PV(1+i" Future value of $1, FV,1F Appendix A Percent Period 1% 2% 3% 4% 5% 6% 79% 8% 9% 10% 11% 1,050 1.080 1 1,010 1.020 1.030 1.040 1.060 1,070 1.090 1.100 1.110 1.020 1.040 1.061 1.082 1.103 1.124 1.166 1.188 1.210 1.232 1.145 1.260 3 1.030 1.061 1.093 1.125 1.158 1.191 1.225 1.295 1.331 1.368 4 1.412 1.464 1.04 1.082 1.126 1.170 1.216 1.262 1.311 1.360 1.518 1.539 1.051 1.104 1.159 1.217 1.276 1.338 1.403 1.469 1.611 1.685 6 1.062 1.126 1.194 1.265 1.340 1.419 1.501 1.587 1.677 1.772 1.870 1.606 1.828 7 1.072 1.149 1.230 1.316 1.407 1.504 1.714 1.949 2.076 8 1.083 1.172 1.267 1.369 1.477 1.594 1.718 1.851 1.993 2.144 2.305 9 1.094 1.195 1.305 1.423 1.55 1.689 1.838 1.999 2.172 2.558 2.358 10 1.105 1.344 1.629 1.967 2.159 2.367 2.839 1.219 1.480 1.791 2.594 1.116 1.243 1.384 1.539 1.710 1.898 2.105 2.332 2.580 2.853 3.152 11 1.268 1,426 1.796 2.012 2.518 2.813 3.138 3.498 12 1.127 1.601 2.252 13 1.138 1.294 1.469 1.665 1.886 2.133 2.410 2.720 3.066 3.452 3.883 1.513 2.261 3.342 4.310 14 1.149 1.319 1.732 1.980 2.579 2.937 3.797 1.80 1.346 2.397 2.759 3.172 3.642 4.785 15 1.161 1.558 2.079 4.177 16 1.873 2.540 3.426 1.173 1.373 1.605 2.183 2.952 3.970 4.595 5.311 3.700 4.328 17 1.184 1.400 1.653 1.948 2.292 2.693 3.159 5.054 5.895 18 1.196 1.428 2.026 2.407 3.380 3.996 5.560 6.544 1.702 2.854 4.717 19 1.208 1.457 1.754 2.107 2.527 3.026 3.617 4.316 5.142 6.116 7.263 2.653 20 1.220 1.486 1.806 2.191 3.207 3.870 4.661 5.604 6.727 8.062 2.666 3.386 8.623 10.835 25 1.282 1,641 2.094 4.292 5.427 6.848 13.585 5.743 30 1,348 1.811 2.427 3.243 4.322 7.612 10.063 13.268 17.449 22.892 40 1,489 2.208 3.262 4,801 7.040 10.286 14.974 21.725 31.409 45,259 65.001 7.107 11.467 18.420 46.902 117.39 184.57 50 1,645 2.692 4.384 29.457 74.358

Appendix A (concluded) Future value of $1 Percent 30% Period 12% 13% 14% 15% 16% 17% 18% 19% 20% 25% 1.130 1.140 1.150 1.160 1.170 1.180 1.190 1.200 1.250 1.300 1.120 2 1.254 1.277 1.300 1.563 1.323 1.346 1.369 1.392 1.416 1,440 1.690 3 1.405 1.443 1.482 1.521 1.561 1.602 1.643 1.685 1.728 1.953 2.197 4 1.574 1.630 1.689 1.749 1.939 2.005 2.856 1.811 1.874 2.074 2.44 5 1.762 1.842 1.925 2.386 3.713 2.011 2.100 2.192 2.288 2.488 3.052 1.974 2.082 2.195 2.313 2.436 2.565 2.700 2.840 2.986 3.815 4.827 2.211 2.353 2.502 2.660 2.826 3.185 3.379 3.583 4.768 3.001 6.276 8 2.476 4.021 2.658 2.853 3.059 3.278 3.511 3.759 4.300 5.960 8.157 9. 2.773 3.004 3.252 3.518 3.803 4.108 4.435 4.785 5.160 7.45 10.604 10 3.106 3.395 3.707 4,046 5.234 5.696 6,192 9.313 13.786 4,411 4,807 3.479 11 3.836 4.226 4.652 5.117 5.624 6.176 6.777 7.430 11.642 17.922 12 3.896 4.335 4.818 5.350 5.936 6.580 7.288 8.064 8.916 14.552 23.298 13 4.363 4.898 5.492 6.153 6.886 7.699 8.599 9.596 10.699 18.190 30.288 14 4.887 6.26 7.988 9.007 10.147 12.839 22.737 39.374 5.535 7.076 11.420 15 5.474 6.254 7.138 8.137 9.266 10.539 11.974 13.590 15.407 28.422 51.186 16 6.130 7.067 8.137 9.358 12.330 16.172 35.527 10.748 14.129 18.488 66.542 17 6.866 7.986 9.276 10.761 12.468 14.426 16.672 19.244 22.186 44.409 86.504 18 7,690 10.575 12.375 16.879 19.673 26.623 9.024 14.463 22.091 55.511 112.46 19 8.613 19.748 10.197 12.056 14.232 16.777 23.214 27.252 31.948 69.389 146.19 20 9.646 11.523 13.743 16.367 19.461 23.106 27.393 32.429 38.338 86.736 190.05 40.874 25 17.000 26.462 32.919 50.658 77.388 95.396 705.64 21.231 62.669 264.70 30 29.960 39.116 50.950 66.212 85.850 111.07 143.37 184.68 237.38 807.79 2,620.0 40 93.051 132.78 188.88 267.86 378.72 533.87 750.38 1,051.7 1,469.8 7,523.2 36,119.0 50 289.00 450.74 1,083.7 1,670.7 2,566.2 9,100.4 497,929.0 700.23 3,927.4 5,988.9 70,065.0

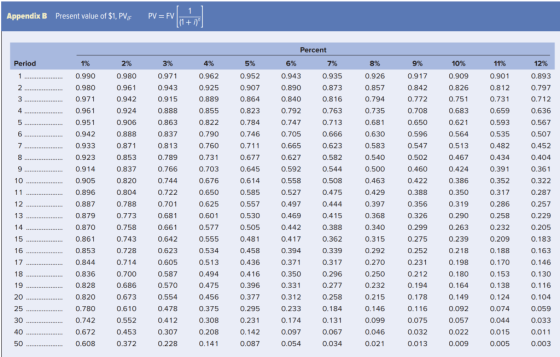

1 PV= FV Appendix B Present value of $1, PV/ (1+i Percent Period 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 0.980 0.971 0.926 0.909 0.990 0.962 0.952 0.943 0.935 0.917 0.901 0.893 0.980 0.890 0.873 0.857 0.842 0.826 0.797 2 0.961 0.943 0.925 0.907 0.812 0.971 0.942 0.915 0.889 0.864 0.840 0.816 0.794 0.772 0.751 0.731 0.712 4 0.961 0.924 0.888 0.855 0.823 0.792 0.763 0.735 0.708 0.683 0.659 0.636 0.951 0.906 0.863 0.822 0.784 0.747 0.713 0.681 0.650 0.621 0.593 0.567 0.942 0.888 0.837 0.790 0.746 0.705 0.666 0.630 0.596 0.564 0.535 0.507 0.760 0.623 0.583 0.933 0.871 0.813 0.711 0.665 0.547 0.513 0.482 0.452 0.923 0.853 0.789 0.731 0.677 0.627 0.582 0.540 0.502 0.467 0.434 0.404 0.914 0.837 0.766 0.703 0.645 0.592 0.544 0.500 0.460 0.424 0.391 0.361 0.463 10 0.905 0.820 0.744 0.676 0.614 0.558 O.508 0.422 0.386 0.352 0.322 0.527 11 0.896 0.804 0.722 0.650 0.585 0.475 0.429 0.388 0.350 0.317 0.287 12 0.887 0.788 0.701 0.625 0.557 0.497 0.444 0.397 0.356 0.319 0.286 0.257 13 0.681 0.368 0.879 0.773 0.601 0.530 0.469 0.415 0.326 0.290 0.258 0.229 0.758 0.577 0.505 0.388 0.232 14 0.870 0.661 0.442 0.340 0.299 0.263 0.205 0.861 0.642 0.481 0.417 0.315 0.209 0.183 15 0.743 0.555 0.362 0.275 0.239 16 0.292 0.252 0.853 0.728 0.623 0.534 0.458 0.394 0.339 0.218 0.188 0.163 17 0.844 0.714 0.605 0.513 0.436 0.371 0.317 0.270 0.231 0.198 0.170 0.146 18 0.836 0.700 0.587 0.494 0.416 0.350 0.296 0.250 0.212 0.180 0.153 0.130 19 0.686 0.570 0.475 0.396 0.331 0.277 0.232 0.194 0.138 0.116 0.828 0.164 20 0.820 0.673 0.554 0.456 0.377 0.312 0.258 0.215 0.178 0.149 O.124 0.104 25 0.610 0.375 0.233 0.146 0.116 0.780 0.478 0.295 0.184 0.092 0.074 0.059 30 0.742 O.552 0.412 0.308 0.231 0.174 0.131 0.099 0.075 0.057 0.044 0.033 40 0.672 0.453 0.307 0.208 0.142 0.097 0.067 0.046 O.032 0.022 0.015 0.011 50 0.608 0.372 0.228 0.141 0.087 0.034 0.021 0.013 0.009 0.005 0.003 0.054

Percent 20% 30% 40% 50% Period 13% 14% 15% 16% 17% 18% 19% 25% 35% 0.870 0.833 0.769 0.714 0.885 0.877 0.862 0.855 0.847 0.840 0.800 0.74 0.667 0.592 2 0.783 0.769 0.756 0.743 0.731 0.718 0.706 0.694 0.640 0.549 0.510 0.444 0.693 0.675 0.658 0.641 0.624 0.609 0.593 0.579 0.512 0.455 0.406 0.364 0.296 0.572 0.482 0.350 4 0.613 0.592 0.552 0.534 0.515 0.499 0.410 0.301 0.260 0.198 5 0.543 0.519 0.497 0.476 0.456 0.437 0.419 0.402 0.328 0.269 0.223 0.186 0.132 0.480 0.456 0.432 0.410 0.390 0.370 0.352 0.335 0.262 0.207 0.165 0.133 0.088 0.425 0.400 0.376 0.354 0.333 0.314 0.296 0.279 0.210 0.159 0.122 O.095 0.059 0.376 0.249 0.233 0.168 0.123 0.351 0.327 0.305 0.285 0.266 O.091 0.068 0.039 0.333 0.308 0.284 0.263 0.243 0.225 0.209 0.194 0.134 0.094 0.067 0.048 0.026 1C 0.247 0.162 0.073 0.035 0.295 0.270 0.227 0.208 0.191 0.176 0.107 0.050 0.017 0.261 0.178 0.086 11 0.237 0.215 0.195 0.162 0.148 0.135 0.056 O.037 0.025 0.012 12 0.231 0.208 0.187 0.168 0.152 O.137 0.124 0.112 0.069 0.043 0.027 0.018 0.008 13 0.204 0.182 0.163 O.145 0.130 0.116 0.104 0.093 O.055 0.033 0.020 0.013 0.005 0.099 0.078 14 0.125 0.088 O.015 0.009 0.181 0.160 0.141 0.111 0.044 O.025 0.003 15 0.160 0.140 0.123 0.108 0.095 0.084 0.074 0.065 O.035 0.020 0.011 0.006 0.002 16 0.107 0.054 0.015 0.008 0.005 0.141 0.123 0.093 0.08 0.071 0.062 0.028 0.002 0.060 17 0.108 0.093 0.080 0.069 0.052 0.023 0.125 O.045 0.012 O.006 O.003 0.001 18 0.059 0.009 0.002 0.111 0.095 0.081 0.069 O.051 O.044 0.038 0.018 0.005 O.001 1C 0.007 0.002 0.098 0.083 0.070 0.060 0.051 0.043 0.037 0.031 0.014 O.003 20 O.087 0.073 O.061 0.051 0.043 0.037 O.031 O.026 0.012 0.005 0.002 0.001 C 0.001 25 0.047 0.038 0.030 0.024 0.020 O.016 0.013 0.010 0.004 0.001 C 0.012 0.007 30 0,026 0.015 0.004 0.020 0.009 0.005 0.001 C 0 A0 0.008 0.005 O.004 0.003 0.002 0.001 0.001 0.001 C C C C 50 0.001 0.002 0.001 0.001 C O

Homework Answers

1a).Loan amount (PV) = 73,000

Interest p.a. (r) = 12%

Number of payments (N) = 30

Annual payments (PMT) =

PV = PMT*[1 - (1+r)^-n]/r

(PV factor from the appendix = 8.055)

PMT = PV/PV factor(12%, 30)

= 73,000/8.055 = 9,062.69 (Approximate annual payment)

Using financial calculator: PV = -73,000; N = 30; rate = 12%, CPT PMT.

PMT = 9,062.49 (Exact annual payment)

(Note: there will be slight differences in the answers calculated using financial calculator and PV factor values due to rounding off.)

1b). Total amount paid in 30 installments = 30*PMT = 30*9,062.49 = 2,71,874.61

Total interest paid = Total amount - Loan amount

= 271,874.61 - 73,000 = 198,874.61

1c). If interest rate p.a. is 10% then annual payment (PMT) will be PV/PV factor(10%, 30)

= 73,000/9.427 = 7,743.71 (Approximate annual payment)

Exact annual payment: PV = 73,000; N = 30; rate = 10%, CPT PMT.

PMT = 7,743.49

Difference in annual payments = 9,062.49 - 7,743.49 = 1,318.70

PV of this difference = Difference * PV factor (10%,30) = 1,318.70*9.427 = 12,431.40 (Approximate PV)

Exact PV: PMT = 1,318.70; N = 30; rate = 10%, CPT PV. PV = 12,431.29

Larry can pay $12,431.29 to get out of the 12% mortgage to a 10% mortgage.

2a). We have to calculate the Future Values (FV):

Approximate FV: FV factor(8%,11) = 16.645

FV = Annual payment*FV factor

= 9,300*16.645 = 1,54,798.50

Exact FV: PMT = -9,300; N = 11; rate = 8%, CPT FV.

FV = 154,803.03

2b). Approximate FV: FV factor(7%,40) = 199.64

FV = Annual payment*FV factor

= 9,300*199.64 = 1,856,652.00

Exact FV: PMT = -9,300; N = 40; rate = 7%, CPT FV.

FV = 1,856,606.54

3). PV = 23,000; N = 12; rate = 11%

Approximate FV: FV(11%,12) = 3.498

FV = PV*FV(11%.12)

= 23,000*3.498 = 80,454.00

Exact FV: PV = -23,000; PMT = 0; N = 12; rate = 11%, CPT FV.

FV = 80,464.36

Card will be worth $80,464.36 after 12 years.

4). PMT = 32,500; N = 15; rate = 17%

Approximate PV: PV = PMT*PV factor(17%, 15)

= 32,500*5.324 = 173,030.00

Exact PV: PMT = -32,5000; N = 15; rate = 17%, CPT PV.

PV = 173,036.09

5). D0 = 0.80

Growth rate g = 10%

D1 = D0*(1+g) = 0.80*(1+10%) = 0.88

Current share price P0 = D1/(Ke - g)

= 0.88/(17%-10%) = 12.57

Add Answer to:

1- Larry Davis borrows $73,000 at 12 percent interest toward the purchase of a home. His...

1 Appendix B Present value of $1. PVF PV=FV Percent Period 1% 5% 8% 9% 12%...

1 Appendix B Present value of $1. PVF PV=FV Percent Period 1% 5% 8% 9% 12% 1 2. 3 0.893 0.797 012 4 6 7 8 9 10 .............. 11 12 0.990 0.980 0.971 0.961 0.951 0.942 0.933 0.923 0.914 0.905 0.896 0.887 0.879 0.870 0.861 0.853 0.844 0.836 0.828 0.820 0.780 0.742 0.672 0.608 2% 0.980 0.961 0.942 0.924 0.906 0.888 0.871 0.853 0.837 0.820 0.804 0.788 0.773 0.758 0.743 0.728 0.714 0.700 0.686 0.673 0.610 0.552 0.453 0.372...

1 Appendix B Present value of $1. PVF PV=FV Percent Period 1% 5% 8% 9% 12% 1 2. 3 0.893 0.797 012 4 6 7 8 9 10 .............. 11 12 0.990 0.980 0.971 0.961 0.951 0.942 0.933 0.923 0.914 0.905 0.896 0.887 0.879 0.870 0.861 0.853 0.844 0.836 0.828 0.820 0.780 0.742 0.672 0.608 2% 0.980 0.961 0.942 0.924 0.906 0.888 0.871 0.853 0.837 0.820 0.804 0.788 0.773 0.758 0.743 0.728 0.714 0.700 0.686 0.673 0.610 0.552 0.453 0.372...

1 Appendix B Present value of $1. PVF PV=FV Percent Period 1% 5% 8% 9% 12%...

1 Appendix B Present value of $1. PVF PV=FV Percent Period 1% 5% 8% 9% 12% 1 2. 3 0.893 0.797 012 4 6 7 8 9 10 .............. 11 12 0.990 0.980 0.971 0.961 0.951 0.942 0.933 0.923 0.914 0.905 0.896 0.887 0.879 0.870 0.861 0.853 0.844 0.836 0.828 0.820 0.780 0.742 0.672 0.608 2% 0.980 0.961 0.942 0.924 0.906 0.888 0.871 0.853 0.837 0.820 0.804 0.788 0.773 0.758 0.743 0.728 0.714 0.700 0.686 0.673 0.610 0.552 0.453 0.372...

1 Appendix B Present value of $1. PVF PV=FV Percent Period 1% 5% 8% 9% 12% 1 2. 3 0.893 0.797 012 4 6 7 8 9 10 .............. 11 12 0.990 0.980 0.971 0.961 0.951 0.942 0.933 0.923 0.914 0.905 0.896 0.887 0.879 0.870 0.861 0.853 0.844 0.836 0.828 0.820 0.780 0.742 0.672 0.608 2% 0.980 0.961 0.942 0.924 0.906 0.888 0.871 0.853 0.837 0.820 0.804 0.788 0.773 0.758 0.743 0.728 0.714 0.700 0.686 0.673 0.610 0.552 0.453 0.372...

1 Appendix B Present value of $1. PVF PV=FV Percent Period 1% 5% 8% 9% 12%...

1 Appendix B Present value of $1. PVF PV=FV Percent Period 1% 5% 8% 9% 12% 1 2. 3 0.893 0.797 012 4 6 7 8 9 10 .............. 11 12 0.990 0.980 0.971 0.961 0.951 0.942 0.933 0.923 0.914 0.905 0.896 0.887 0.879 0.870 0.861 0.853 0.844 0.836 0.828 0.820 0.780 0.742 0.672 0.608 2% 0.980 0.961 0.942 0.924 0.906 0.888 0.871 0.853 0.837 0.820 0.804 0.788 0.773 0.758 0.743 0.728 0.714 0.700 0.686 0.673 0.610 0.552 0.453 0.372...

1 Appendix B Present value of $1. PVF PV=FV Percent Period 1% 5% 8% 9% 12% 1 2. 3 0.893 0.797 012 4 6 7 8 9 10 .............. 11 12 0.990 0.980 0.971 0.961 0.951 0.942 0.933 0.923 0.914 0.905 0.896 0.887 0.879 0.870 0.861 0.853 0.844 0.836 0.828 0.820 0.780 0.742 0.672 0.608 2% 0.980 0.961 0.942 0.924 0.906 0.888 0.871 0.853 0.837 0.820 0.804 0.788 0.773 0.758 0.743 0.728 0.714 0.700 0.686 0.673 0.610 0.552 0.453 0.372...

Loan Payment Larry Davis borrows $80.000 at 14 percent interest toward the purchase of a home...

Loan Payment

Larry Davis borrows $80.000 at 14 percent interest toward the purchase of a home is mortgages for 25 years. Use Accent calculator methods for an approximan but calculate your finan s ing the formula and ranca a. How much wilis annual payments be? Athough home payments are usually on a monthly basis, we shall do our round intermediate calculations. Round your final answer to 2 decimal places.) sis on an annual boss for ease of computation. We we...

Loan Payment

Larry Davis borrows $80.000 at 14 percent interest toward the purchase of a home is mortgages for 25 years. Use Accent calculator methods for an approximan but calculate your finan s ing the formula and ranca a. How much wilis annual payments be? Athough home payments are usually on a monthly basis, we shall do our round intermediate calculations. Round your final answer to 2 decimal places.) sis on an annual boss for ease of computation. We we...

Keller Construction is considering two new investments. Project E calls for the purchase of earthmoving equipment....

Keller Construction is

considering two new investments. Project E calls for the purchase

of earthmoving equipment. Project H represents an investment in a

hydraulic lift. Keller wishes to use a net present value profile in

comparing the projects. The investment and cash flow patterns are

as follows: Use Appendix B for an approximate answer but calculate

your final answer using the formula and financial calculator

methods.

Project E

Project H

($40,000 Investment)

($36,000 Investment)

Year

Cash Flow

Year

Cash Flow...

Keller Construction is

considering two new investments. Project E calls for the purchase

of earthmoving equipment. Project H represents an investment in a

hydraulic lift. Keller wishes to use a net present value profile in

comparing the projects. The investment and cash flow patterns are

as follows: Use Appendix B for an approximate answer but calculate

your final answer using the formula and financial calculator

methods.

Project E

Project H

($40,000 Investment)

($36,000 Investment)

Year

Cash Flow

Year

Cash Flow...

Cascade Mining Company expects its earnings and dividends to increase by 8 percent per year over...

Cascade Mining Company expects its earnings and dividends to

increase by 8 percent per year over the next 6 years and then to

remain relatively constant thereafter. The firm currently (that is,

as of year 0) pays a dividend of $4.5 per share. Determine the

value of a share of Cascade stock to an investor with a 11 percent

required rate of return. Use Table II to answer the question. Round

your answer to the nearest cent.

TABLE II Present...

Cascade Mining Company expects its earnings and dividends to

increase by 8 percent per year over the next 6 years and then to

remain relatively constant thereafter. The firm currently (that is,

as of year 0) pays a dividend of $4.5 per share. Determine the

value of a share of Cascade stock to an investor with a 11 percent

required rate of return. Use Table II to answer the question. Round

your answer to the nearest cent.

TABLE II Present...

Larry Davis borrows $75,000 at 11 percent interest toward the purchase of a home. His mortgage...

Larry Davis borrows $75,000 at 11 percent interest toward the purchase of a home. His mortgage is for 25 years. Use Appendix D for an approximate answer, but calolate your final answer using the formula and francial calculator methods. a. How much will his annual payments be? (Although home payments are usually on a monthly basis, we shal do our analysis on an annual basis for ease of computation. We will get a reasonably accurate answer.) (Do not round Intermediate...

Larry Davis borrows $75,000 at 11 percent interest toward the purchase of a home. His mortgage is for 25 years. Use Appendix D for an approximate answer, but calolate your final answer using the formula and francial calculator methods. a. How much will his annual payments be? (Although home payments are usually on a monthly basis, we shal do our analysis on an annual basis for ease of computation. We will get a reasonably accurate answer.) (Do not round Intermediate...

Larry Davis borrows $75,000 at 11 percent interest toward the purchase of a home. His mortgage...

Larry Davis borrows $75,000 at 11 percent interest toward the purchase of a home. His mortgage is for 25 years. Use Appendix D for an approximate answer, but caloulate your final answer using the formula and financial calculator methods. a. How much will his annual payments be? (Athough home payments are usually on a monthly basis, we shall do our analysis on an annual basis for ease of computation. We will get a reasonably accurate answer (Do not round Intermediate...

Larry Davis borrows $75,000 at 11 percent interest toward the purchase of a home. His mortgage is for 25 years. Use Appendix D for an approximate answer, but caloulate your final answer using the formula and financial calculator methods. a. How much will his annual payments be? (Athough home payments are usually on a monthly basis, we shall do our analysis on an annual basis for ease of computation. We will get a reasonably accurate answer (Do not round Intermediate...

Larry Davis borrows $74,000 at 10 percent Interest toward the purchase of a home. His mortgage...

Larry Davis borrows $74,000 at 10 percent Interest toward the purchase of a home. His mortgage is for 20 years. a. If Larry decides to make annual payments, how much will they be? (Enter your answer as a positive number rounded to 2 decimal places.) Annual payments b. How much Interest will he pay over the life of the loan? (Do not round Intermediate calculations. Round your final answer to 2 declmal places.) Total interest

Larry Davis borrows $74,000 at 10 percent Interest toward the purchase of a home. His mortgage is for 20 years. a. If Larry decides to make annual payments, how much will they be? (Enter your answer as a positive number rounded to 2 decimal places.) Annual payments b. How much Interest will he pay over the life of the loan? (Do not round Intermediate calculations. Round your final answer to 2 declmal places.) Total interest

X-treme Vitamin Company is considering two investments, both of which cost $20,000. The cash flows are...

X-treme Vitamin Company is considering two investments, both of which cost $20,000. The cash flows are as follows: Year Project A Project B $23,000 $20,000 2 10,000 9,000 3 10,000 15,000 1 Use Appendix B for an approximate answer but calculate your final answer using the formula and financial calculator methods. a-1. Calculate the payback period for Project A and Project B. (Round your answers to 2 decimal places.) Project A Project B Payback Period year(s) year(s) b-1. Calculate the...

X-treme Vitamin Company is considering two investments, both of which cost $20,000. The cash flows are as follows: Year Project A Project B $23,000 $20,000 2 10,000 9,000 3 10,000 15,000 1 Use Appendix B for an approximate answer but calculate your final answer using the formula and financial calculator methods. a-1. Calculate the payback period for Project A and Project B. (Round your answers to 2 decimal places.) Project A Project B Payback Period year(s) year(s) b-1. Calculate the...

1 Appendix B Present value of $1. PVF PV=FV Percent Period 1% 5% 8% 9% 12% 1 2. 3 0.893 0.797 012 4 6 7 8 9 10 .............. 11 12 0.990 0.980 0.971 0.961 0.951 0.942 0.933 0.923 0.914 0.905 0.896 0.887 0.879 0.870 0.861 0.853 0.844 0.836 0.828 0.820 0.780 0.742 0.672 0.608 2% 0.980 0.961 0.942 0.924 0.906 0.888 0.871 0.853 0.837 0.820 0.804 0.788 0.773 0.758 0.743 0.728 0.714 0.700 0.686 0.673 0.610 0.552 0.453 0.372...

1 Appendix B Present value of $1. PVF PV=FV Percent Period 1% 5% 8% 9% 12% 1 2. 3 0.893 0.797 012 4 6 7 8 9 10 .............. 11 12 0.990 0.980 0.971 0.961 0.951 0.942 0.933 0.923 0.914 0.905 0.896 0.887 0.879 0.870 0.861 0.853 0.844 0.836 0.828 0.820 0.780 0.742 0.672 0.608 2% 0.980 0.961 0.942 0.924 0.906 0.888 0.871 0.853 0.837 0.820 0.804 0.788 0.773 0.758 0.743 0.728 0.714 0.700 0.686 0.673 0.610 0.552 0.453 0.372...

1 Appendix B Present value of $1. PVF PV=FV Percent Period 1% 5% 8% 9% 12% 1 2. 3 0.893 0.797 012 4 6 7 8 9 10 .............. 11 12 0.990 0.980 0.971 0.961 0.951 0.942 0.933 0.923 0.914 0.905 0.896 0.887 0.879 0.870 0.861 0.853 0.844 0.836 0.828 0.820 0.780 0.742 0.672 0.608 2% 0.980 0.961 0.942 0.924 0.906 0.888 0.871 0.853 0.837 0.820 0.804 0.788 0.773 0.758 0.743 0.728 0.714 0.700 0.686 0.673 0.610 0.552 0.453 0.372...

1 Appendix B Present value of $1. PVF PV=FV Percent Period 1% 5% 8% 9% 12% 1 2. 3 0.893 0.797 012 4 6 7 8 9 10 .............. 11 12 0.990 0.980 0.971 0.961 0.951 0.942 0.933 0.923 0.914 0.905 0.896 0.887 0.879 0.870 0.861 0.853 0.844 0.836 0.828 0.820 0.780 0.742 0.672 0.608 2% 0.980 0.961 0.942 0.924 0.906 0.888 0.871 0.853 0.837 0.820 0.804 0.788 0.773 0.758 0.743 0.728 0.714 0.700 0.686 0.673 0.610 0.552 0.453 0.372...

1 Appendix B Present value of $1. PVF PV=FV Percent Period 1% 5% 8% 9% 12% 1 2. 3 0.893 0.797 012 4 6 7 8 9 10 .............. 11 12 0.990 0.980 0.971 0.961 0.951 0.942 0.933 0.923 0.914 0.905 0.896 0.887 0.879 0.870 0.861 0.853 0.844 0.836 0.828 0.820 0.780 0.742 0.672 0.608 2% 0.980 0.961 0.942 0.924 0.906 0.888 0.871 0.853 0.837 0.820 0.804 0.788 0.773 0.758 0.743 0.728 0.714 0.700 0.686 0.673 0.610 0.552 0.453 0.372...

1 Appendix B Present value of $1. PVF PV=FV Percent Period 1% 5% 8% 9% 12% 1 2. 3 0.893 0.797 012 4 6 7 8 9 10 .............. 11 12 0.990 0.980 0.971 0.961 0.951 0.942 0.933 0.923 0.914 0.905 0.896 0.887 0.879 0.870 0.861 0.853 0.844 0.836 0.828 0.820 0.780 0.742 0.672 0.608 2% 0.980 0.961 0.942 0.924 0.906 0.888 0.871 0.853 0.837 0.820 0.804 0.788 0.773 0.758 0.743 0.728 0.714 0.700 0.686 0.673 0.610 0.552 0.453 0.372...

Loan Payment

Larry Davis borrows $80.000 at 14 percent interest toward the purchase of a home is mortgages for 25 years. Use Accent calculator methods for an approximan but calculate your finan s ing the formula and ranca a. How much wilis annual payments be? Athough home payments are usually on a monthly basis, we shall do our round intermediate calculations. Round your final answer to 2 decimal places.) sis on an annual boss for ease of computation. We we...

Loan Payment

Larry Davis borrows $80.000 at 14 percent interest toward the purchase of a home is mortgages for 25 years. Use Accent calculator methods for an approximan but calculate your finan s ing the formula and ranca a. How much wilis annual payments be? Athough home payments are usually on a monthly basis, we shall do our round intermediate calculations. Round your final answer to 2 decimal places.) sis on an annual boss for ease of computation. We we...

Keller Construction is

considering two new investments. Project E calls for the purchase

of earthmoving equipment. Project H represents an investment in a

hydraulic lift. Keller wishes to use a net present value profile in

comparing the projects. The investment and cash flow patterns are

as follows: Use Appendix B for an approximate answer but calculate

your final answer using the formula and financial calculator

methods.

Project E

Project H

($40,000 Investment)

($36,000 Investment)

Year

Cash Flow

Year

Cash Flow...

Keller Construction is

considering two new investments. Project E calls for the purchase

of earthmoving equipment. Project H represents an investment in a

hydraulic lift. Keller wishes to use a net present value profile in

comparing the projects. The investment and cash flow patterns are

as follows: Use Appendix B for an approximate answer but calculate

your final answer using the formula and financial calculator

methods.

Project E

Project H

($40,000 Investment)

($36,000 Investment)

Year

Cash Flow

Year

Cash Flow...

Cascade Mining Company expects its earnings and dividends to

increase by 8 percent per year over the next 6 years and then to

remain relatively constant thereafter. The firm currently (that is,

as of year 0) pays a dividend of $4.5 per share. Determine the

value of a share of Cascade stock to an investor with a 11 percent

required rate of return. Use Table II to answer the question. Round

your answer to the nearest cent.

TABLE II Present...

Cascade Mining Company expects its earnings and dividends to

increase by 8 percent per year over the next 6 years and then to

remain relatively constant thereafter. The firm currently (that is,

as of year 0) pays a dividend of $4.5 per share. Determine the

value of a share of Cascade stock to an investor with a 11 percent

required rate of return. Use Table II to answer the question. Round

your answer to the nearest cent.

TABLE II Present...

Larry Davis borrows $75,000 at 11 percent interest toward the purchase of a home. His mortgage is for 25 years. Use Appendix D for an approximate answer, but calolate your final answer using the formula and francial calculator methods. a. How much will his annual payments be? (Although home payments are usually on a monthly basis, we shal do our analysis on an annual basis for ease of computation. We will get a reasonably accurate answer.) (Do not round Intermediate...

Larry Davis borrows $75,000 at 11 percent interest toward the purchase of a home. His mortgage is for 25 years. Use Appendix D for an approximate answer, but calolate your final answer using the formula and francial calculator methods. a. How much will his annual payments be? (Although home payments are usually on a monthly basis, we shal do our analysis on an annual basis for ease of computation. We will get a reasonably accurate answer.) (Do not round Intermediate...

Larry Davis borrows $75,000 at 11 percent interest toward the purchase of a home. His mortgage is for 25 years. Use Appendix D for an approximate answer, but caloulate your final answer using the formula and financial calculator methods. a. How much will his annual payments be? (Athough home payments are usually on a monthly basis, we shall do our analysis on an annual basis for ease of computation. We will get a reasonably accurate answer (Do not round Intermediate...

Larry Davis borrows $75,000 at 11 percent interest toward the purchase of a home. His mortgage is for 25 years. Use Appendix D for an approximate answer, but caloulate your final answer using the formula and financial calculator methods. a. How much will his annual payments be? (Athough home payments are usually on a monthly basis, we shall do our analysis on an annual basis for ease of computation. We will get a reasonably accurate answer (Do not round Intermediate...

Larry Davis borrows $74,000 at 10 percent Interest toward the purchase of a home. His mortgage is for 20 years. a. If Larry decides to make annual payments, how much will they be? (Enter your answer as a positive number rounded to 2 decimal places.) Annual payments b. How much Interest will he pay over the life of the loan? (Do not round Intermediate calculations. Round your final answer to 2 declmal places.) Total interest

Larry Davis borrows $74,000 at 10 percent Interest toward the purchase of a home. His mortgage is for 20 years. a. If Larry decides to make annual payments, how much will they be? (Enter your answer as a positive number rounded to 2 decimal places.) Annual payments b. How much Interest will he pay over the life of the loan? (Do not round Intermediate calculations. Round your final answer to 2 declmal places.) Total interest

X-treme Vitamin Company is considering two investments, both of which cost $20,000. The cash flows are as follows: Year Project A Project B $23,000 $20,000 2 10,000 9,000 3 10,000 15,000 1 Use Appendix B for an approximate answer but calculate your final answer using the formula and financial calculator methods. a-1. Calculate the payback period for Project A and Project B. (Round your answers to 2 decimal places.) Project A Project B Payback Period year(s) year(s) b-1. Calculate the...

X-treme Vitamin Company is considering two investments, both of which cost $20,000. The cash flows are as follows: Year Project A Project B $23,000 $20,000 2 10,000 9,000 3 10,000 15,000 1 Use Appendix B for an approximate answer but calculate your final answer using the formula and financial calculator methods. a-1. Calculate the payback period for Project A and Project B. (Round your answers to 2 decimal places.) Project A Project B Payback Period year(s) year(s) b-1. Calculate the...

Most questions answered within 3 hours.

-

(63

#14)

which of the following statments best describes how chamging

the concentration of the substances...

asked 2 hours ago -

In the following reaction, which element is undergoing

oxidation: Na2SO3 + N2O --> N2 + Na2SO4...

asked 2 hours ago -

Which of the following pairs of ions have the same electron

configuration?

I: Br− and Se2−...

asked 5 hours ago -

The Foremost Composite Materials Company is planning a two-day

sales conference for October 19-20. The conference...

asked 5 hours ago -

3) Illustrate the observed pattern of relatedness of organisms

versus adaptations to specific conditions. This means...

asked 6 hours ago -

In winter a lake has a 0.35 m thick ice layer over 1.10 m of

water....

asked 7 hours ago -

Assuming the following has been encrypted with a Vigenere cipher

below, use the method(s) and assumptions...

asked 7 hours ago -

How would I use switch statements to write a program that will

take an input of...

asked 7 hours ago -

Imagine a reaction in which methane gas combusts at a constant

pressure of 1 atm and...

asked 7 hours ago -

Two parallel wires (each 12 m in length) are separated by a

distance of 0.065 m...

asked 7 hours ago -

Suppose there were three masses at the corner of uniform

equilateral triangle. The masses are m1...

asked 7 hours ago -

Situation: A building that is 618 m above the ground floor. How

many times would a...

asked 7 hours ago