Consider a perfectly competitive industry in which each firm i has a total cost function given...

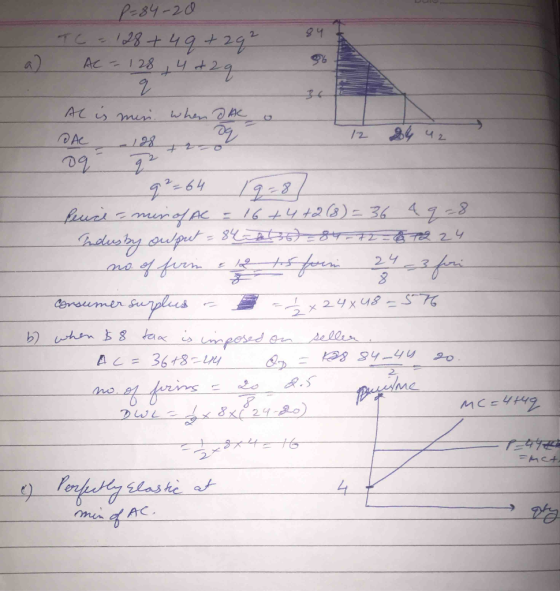

Consider a perfectly competitive industry in which each firm i has a total cost function given by the equation: TC= 128 + 4q+2q^2. Further assume that the industry demand function is given by the following: P = 84 – 2Q.

a) Describe the long run market equilibrium. That is, identify the equilibrium price and quantity, output for each firm, the number of firms in the industry and the level of producer and consumer surplus. What is the value of own price elasticity of demand at the market equilibrium? Is demand elastic or inelastic?

Show the outcome for individual firms in a well labelled diagram. Also, show the market equilibrium in a separate well labelled diagram

b) Assume now that the government imposes a specific tax of 8 on sellers. Find the new market equilibrium. That is, identify the equilibrium price and quantity, output for each firm, the number of firms in the industry and the deadweight loss associated with the tax.

Show the outcome for individual firms in a well labelled diagram. Also, show the market equilibrium in a separate well labelled diagram [4 marks]

c) What does this long run supply curve look like and why?

Homework Answers

Add Answer to:

Consider a perfectly competitive industry in which each firm i

has a total cost function given...

How to do this question ? B2-(13 MARKS) Consider a perfectly competitive industry in which each...

How to do this question ?

B2-(13 MARKS) Consider a perfectly competitive industry in which each firm i has a total cost function given by the equation: TC,- 128+ 4q+ 2q. Further, assume that the industry demand finction is given by the following: P = 84-20 a) Describe the long nun market equilibrium. That is, identify the equilibrium price and quantity output for each firm, the number of fims in the industry and the level of producer and consumer surplus....

How to do this question ?

B2-(13 MARKS) Consider a perfectly competitive industry in which each firm i has a total cost function given by the equation: TC,- 128+ 4q+ 2q. Further, assume that the industry demand finction is given by the following: P = 84-20 a) Describe the long nun market equilibrium. That is, identify the equilibrium price and quantity output for each firm, the number of fims in the industry and the level of producer and consumer surplus....

typical perfect competitive firm in the coffee market is given by the The cost curve for...

typical perfect competitive firm in the coffee market is given by the The cost curve for a following 1284qi + 2q% TC The market demand curve for coffee is given by the following P 84 2q (a) i) Find the long ru and quantity, output for each firm, the number of firms in the industry and the level of producer and consumer surplus. Show your answer in a clear well-labelled diagram (ii) What is the value of own price elasticity...

typical perfect competitive firm in the coffee market is given by the The cost curve for a following 1284qi + 2q% TC The market demand curve for coffee is given by the following P 84 2q (a) i) Find the long ru and quantity, output for each firm, the number of firms in the industry and the level of producer and consumer surplus. Show your answer in a clear well-labelled diagram (ii) What is the value of own price elasticity...

The cost curve for a typical perfect competitive firm in the coffee market is given by...

The cost curve for a typical perfect competitive firm in the coffee market is given by the following TC 128+4g+2q The market demand curve for coffee is given by the following P=84-2q (a) (i) Find the long run competitive equilibrium. That is, identify the equilibrium price and quantity, output for each firm, the number of firms in the industry and the level of producer and consumer surplus. Show your answer in a clear well-labelled diagram (ii) What is the value...

The cost curve for a typical perfect competitive firm in the coffee market is given by the following TC 128+4g+2q The market demand curve for coffee is given by the following P=84-2q (a) (i) Find the long run competitive equilibrium. That is, identify the equilibrium price and quantity, output for each firm, the number of firms in the industry and the level of producer and consumer surplus. Show your answer in a clear well-labelled diagram (ii) What is the value...

1. (20p) Suppose that, in a perfectly competitive industry, the technology for making the product (by...

1. (20p) Suppose that, in a perfectly competitive industry, the technology for making the product (by any single firm) has the total cost function c(q) = 200 + 4q+ Barriers to entry and exit the market are low and an unlimited number of firms could enter this industry, all with the same total cost function. (a) Compute the long-run equilibrium price in this industry, as well as the amount of output each firm would produce at this price. Explain the...

1. (20p) Suppose that, in a perfectly competitive industry, the technology for making the product (by any single firm) has the total cost function c(q) = 200 + 4q+ Barriers to entry and exit the market are low and an unlimited number of firms could enter this industry, all with the same total cost function. (a) Compute the long-run equilibrium price in this industry, as well as the amount of output each firm would produce at this price. Explain the...

A representative firm in a perfectly competitive, constant cost industry has a cost function T C...

A representative firm in a perfectly competitive, constant cost industry has a cost function T C = 100+4Q 2+ 100Q. (a) What are this firm fixed cost, variable cost and marginal cost? (b) What is the long-run equilibrium price for this industry? (c) If the market demand is Q = 1000 − P , how many firms will operate in this long-run equilibrium? (d) What is the most that this firm would be willing to pay for the exclusive right...

Suppose that each firm in a competitive industry has the following costs: Total Cost: TC= 50+1/2...

Suppose that each firm in a competitive industry has the following costs: Total Cost: TC= 50+1/2 q^2 Marginal Cost: MC= q where qq is an individual firm's quantity produced. The market demand curve for this product is Demand QD=160−4PQD=160−4P where PP is the price and QQ is the total quantity of the good. Each firm's fixed cost is $_____ What is each firm's variable cost? q 50+1/2 q 1/2q 1/2q^2 Which of the following represents the equation for each firm's...

Name Each producer in this perfectly competitive industry has a long-run MC function of: MC-40-120+ and...

Name Each producer in this perfectly competitive industry has a long-run MC function of: MC-40-120+ and long-run ATC function: ATC 40-60 (Q)/3. The market demand curve is: D-2200-100P a. What is the long-run equilibrium price in this industry? b. At this long-run equilibrium price, what is the quantity produced by an individual firm? c. How many firms are there in this industry (in the long-run)?

Name Each producer in this perfectly competitive industry has a long-run MC function of: MC-40-120+ and long-run ATC function: ATC 40-60 (Q)/3. The market demand curve is: D-2200-100P a. What is the long-run equilibrium price in this industry? b. At this long-run equilibrium price, what is the quantity produced by an individual firm? c. How many firms are there in this industry (in the long-run)?

2. A competitive industry has 12 identical firms, each one has a total variable cost function...

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

A firm produces a product in a competitive industry and has a total cost function (TC)...

A firm produces a product in a competitive industry and has a total cost function (TC) of TC(a) 60+4q+2q2 and a marginal cost function (MC) of MC(q) = 4 + 4q. At the given market price (P) of $20, the firm is producing 4.00 units of output. Is the firm maximizing profit?V What quantity of output should the firm produce in the long run? The firm should produce unit(s) of output. (Enter your response as an integer.)

A firm produces a product in a competitive industry and has a total cost function (TC) of TC(a) 60+4q+2q2 and a marginal cost function (MC) of MC(q) = 4 + 4q. At the given market price (P) of $20, the firm is producing 4.00 units of output. Is the firm maximizing profit?V What quantity of output should the firm produce in the long run? The firm should produce unit(s) of output. (Enter your response as an integer.)

How to do this question ?

B2-(13 MARKS) Consider a perfectly competitive industry in which each firm i has a total cost function given by the equation: TC,- 128+ 4q+ 2q. Further, assume that the industry demand finction is given by the following: P = 84-20 a) Describe the long nun market equilibrium. That is, identify the equilibrium price and quantity output for each firm, the number of fims in the industry and the level of producer and consumer surplus....

How to do this question ?

B2-(13 MARKS) Consider a perfectly competitive industry in which each firm i has a total cost function given by the equation: TC,- 128+ 4q+ 2q. Further, assume that the industry demand finction is given by the following: P = 84-20 a) Describe the long nun market equilibrium. That is, identify the equilibrium price and quantity output for each firm, the number of fims in the industry and the level of producer and consumer surplus....

typical perfect competitive firm in the coffee market is given by the The cost curve for a following 1284qi + 2q% TC The market demand curve for coffee is given by the following P 84 2q (a) i) Find the long ru and quantity, output for each firm, the number of firms in the industry and the level of producer and consumer surplus. Show your answer in a clear well-labelled diagram (ii) What is the value of own price elasticity...

typical perfect competitive firm in the coffee market is given by the The cost curve for a following 1284qi + 2q% TC The market demand curve for coffee is given by the following P 84 2q (a) i) Find the long ru and quantity, output for each firm, the number of firms in the industry and the level of producer and consumer surplus. Show your answer in a clear well-labelled diagram (ii) What is the value of own price elasticity...

The cost curve for a typical perfect competitive firm in the coffee market is given by the following TC 128+4g+2q The market demand curve for coffee is given by the following P=84-2q (a) (i) Find the long run competitive equilibrium. That is, identify the equilibrium price and quantity, output for each firm, the number of firms in the industry and the level of producer and consumer surplus. Show your answer in a clear well-labelled diagram (ii) What is the value...

The cost curve for a typical perfect competitive firm in the coffee market is given by the following TC 128+4g+2q The market demand curve for coffee is given by the following P=84-2q (a) (i) Find the long run competitive equilibrium. That is, identify the equilibrium price and quantity, output for each firm, the number of firms in the industry and the level of producer and consumer surplus. Show your answer in a clear well-labelled diagram (ii) What is the value...

1. (20p) Suppose that, in a perfectly competitive industry, the technology for making the product (by any single firm) has the total cost function c(q) = 200 + 4q+ Barriers to entry and exit the market are low and an unlimited number of firms could enter this industry, all with the same total cost function. (a) Compute the long-run equilibrium price in this industry, as well as the amount of output each firm would produce at this price. Explain the...

1. (20p) Suppose that, in a perfectly competitive industry, the technology for making the product (by any single firm) has the total cost function c(q) = 200 + 4q+ Barriers to entry and exit the market are low and an unlimited number of firms could enter this industry, all with the same total cost function. (a) Compute the long-run equilibrium price in this industry, as well as the amount of output each firm would produce at this price. Explain the...

Name Each producer in this perfectly competitive industry has a long-run MC function of: MC-40-120+ and long-run ATC function: ATC 40-60 (Q)/3. The market demand curve is: D-2200-100P a. What is the long-run equilibrium price in this industry? b. At this long-run equilibrium price, what is the quantity produced by an individual firm? c. How many firms are there in this industry (in the long-run)?

Name Each producer in this perfectly competitive industry has a long-run MC function of: MC-40-120+ and long-run ATC function: ATC 40-60 (Q)/3. The market demand curve is: D-2200-100P a. What is the long-run equilibrium price in this industry? b. At this long-run equilibrium price, what is the quantity produced by an individual firm? c. How many firms are there in this industry (in the long-run)?

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

A firm produces a product in a competitive industry and has a total cost function (TC) of TC(a) 60+4q+2q2 and a marginal cost function (MC) of MC(q) = 4 + 4q. At the given market price (P) of $20, the firm is producing 4.00 units of output. Is the firm maximizing profit?V What quantity of output should the firm produce in the long run? The firm should produce unit(s) of output. (Enter your response as an integer.)

A firm produces a product in a competitive industry and has a total cost function (TC) of TC(a) 60+4q+2q2 and a marginal cost function (MC) of MC(q) = 4 + 4q. At the given market price (P) of $20, the firm is producing 4.00 units of output. Is the firm maximizing profit?V What quantity of output should the firm produce in the long run? The firm should produce unit(s) of output. (Enter your response as an integer.)

Most questions answered within 3 hours.

-

Given input { 66, 28, 43, 29, 44, 69, 19 } and a hash function

h(x)...

asked 21 seconds ago -

A pebble with mass m is thrown straight up with an initial speed

v0 so that...

asked 4 minutes ago -

Let X be a discrete random variable that follows a

binomial distribution with n = 11...

asked 12 minutes ago -

The equilibrium constant, K, for the following reaction is

1.29×10-2 at 600

K.

COCl2(g) --->

CO(g)...

asked 25 minutes ago -

It is known that 72% of people have a favorable opinion of their

local police force....

asked 28 minutes ago -

A vertical straight wire carrying an upward 26-A current exerts

an attractive force per unit length...

asked 41 minutes ago -

For the purposes of this assignment, you are to choose an

adaptive trait common to more...

asked 50 minutes ago -

Two identical flutes can play middle C (262 Hz) at 20◦C. How

many beats per second...

asked 58 minutes ago -

Potassium phosphate and calcium chloride react in a double

replacement reaction. To produce 1.0 moles of...

asked 53 minutes ago -

Sparky, Co. purchased land as a factory site for $600,000.

Sparky paid $42,000 to tear down...

asked 1 hour ago -

A Chi-square distribution with 14 degrees of freedom is a

correct model for

Question 8 options:...

asked 1 hour ago -

In a group of 45 mice, there are 10 that have a certain genetic

character. suppose...

asked 1 hour ago