|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Homework Answers

Job order Costing: It is a method of cost accounting, in which cost is collected and accumulated for each job, work order, or project separately. Especially the job order costing is followed in organizations where customized goods are produced.

Transaction: A transaction in business refers to any events that affect the financial position of the business that can be reliably measured in monetary terms.

Journal entry: It is the process of recording transactions in a chronological order. Normally double entry accounting system is used for recording accounting transactions. Under this method each transaction has two sides, debit side and credit side. Total amount of debit side must be equal to the total amount of credit side.

Direct materials: Direct materials are the raw materials which are directly related with the production of the goods.

Manufacturing overhead costs: The costs, which do not relate directly with the manufacturing of products, are referred to as manufacturing overhead costs or indirect costs.

Direct labor cost: the labor cost includes the wages or salaries paid to employees who physically produce goods or services. Labor refers to the actual work that the employees do to produce products. Labor costs refer to the amount of money that the employer pays the employees to complete the work.

Work-in-process: It is the total of all expenses put into the production process to manufacture products that are partially completed. Generally, work in process refers to labor, raw materials and overhead expenses incurred for products that are at several stages of the production procedure.

Finished goods: These are goods that have been completed by the manufacturing procedure, or purchase in a complete form, but are not yet sold to customers.

Cost of goods sold: Cost of goods sold is the direct costs incurred by the business for the merchandise that the business has sold. The amount includes the materials costs used to create the goods and direct labor costs used to produce the goods.

Gross profit: Gross profit is the excess of net sales revenue over cost of goods sold. Net sales revenue is the total sales less returns, allowances, and discounts. Cost of goods sold are the direct expenses incurred by the company to produce goods or services, including direct labor costs.

Rules for debit and credit:

• When asset increases debit it; asset decreases credit it.

• When liabilities increase credit it; liabilities decrease debit it.

• When stockholders’ equity increases credit it; stockholders’ equity decreases debit it.

• Expenses and losses increases debit it; expenses and losses decrease credit it.

• Incomes and gains increases credit it; incomes and gains decrease debit it.

Assets: Asset is the resource used by the company to generate income. Assets can be classified into different types, Current assets, long term assets and intangible assets. Assets that are expected to be converted into cash within one year are called as current assets. Assets that are expected to be converted into cash more than one year are called as long-term assets. Asset which cannot be touch and see is called as intangible asset. Goodwill, patents etc are the examples of intangible assets.

Stockholders’ equity: A Shareholders claim on the assets of a company is known as stockholders’ equity, which are assets minus liabilities. This is also a permanent account because these balances are carried forward from one financial year to the other. Stockholders’ equity also called as owners’ equity.

Liabilities: Liability is an amount of money owed to outsider of the company. Accounts payable, bank loans, personal loans etc are examples of liability. Liabilities that are expected to repay within one year are coming under the category of current liabilities. Liabilities that are expected to repay more than one year are coming under the category of long term liabilities.

Accounting equation: Accounting equation is the relationship among the assets, liabilities and stockholders’ equity. Total assets are equal to total liabilities and stockholders’ equity. According to this equation, when assets increase, corresponding increase will happen on either liabilities or owners’ equity. The following formula used for accounting equation.

Formula for actual manufacturing overhead costs as shown below:

Over (or) under applied overhead: The actual manufacturing overhead cost is debited, and the estimated manufacturing overhead cost is credited to the manufacturing overhead account. At the end of the reporting period, the debit balance of the manufacturing overhead account shows the under applied overhead, however, the credit balance of the manufacturing overhead account shows the over applied overhead i.e., if the actual overhead incurred is more than the overhead applied then it is under application of overheads and if the actual overhead incurred is less than the overhead applied, then it is over application of overheads.

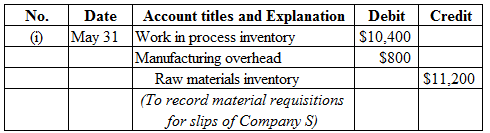

(i)

Prepare the journal entry to record the requisition bills for Company S as shown below:

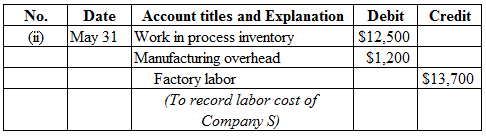

(ii)

Prepare the journal entry to record the time tickets for Company S as shown below:

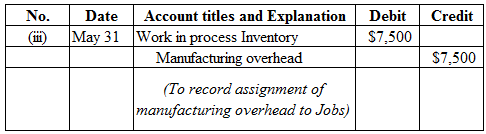

(iii)

Prepare the journal entry to record the assignment of manufacturing overhead to jobs for Company S as shown below:

Working note:

Calculation of manufacturing overhead as shown below:

Hence, manufacturing overhead cost for Company S is $7,500.

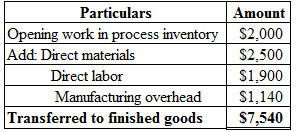

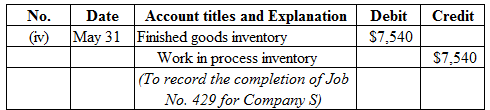

(iv)

Calculate the amount transferred to finished goods for Job No. 429 of Company S as shown below:

Therefore, transferred to finished goods for Job No. 429 of Company S is $7,540.

Working note:

Calculate manufacturing overhead for Job No. 429 as shown below:

Hence, manufacturing overhead cost for Job No. 429 is $1,140.

Prepare the journal entry to record the completion of job no. 429for Company S as shown below:

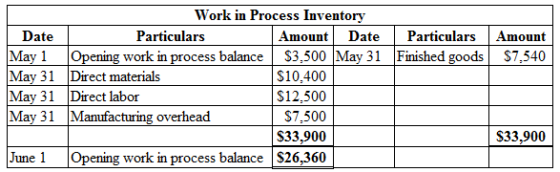

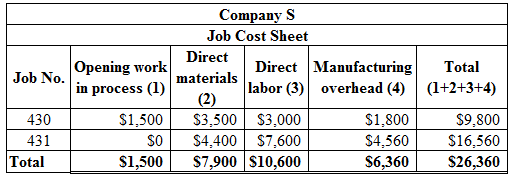

Post the transaction to post the entries to work in process inventory and prove the agreement of the control account with the Job cost sheets of Company S as shown below:

Add Answer to:

Exercise 16-2

Stine Company uses a job order cost system. On May 1, the company

has...

Stine Company uses a job order cost system. On May 1, the company has a balance...

Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,500 and two jobs in process: Job No. 429 $2,000, and Job No. 430 $1,500. During May, a summary of source documents reveals the following. Job Number Materials Requisition Slips Labor Time Tickets 429 $2,500 $1,900 430 3,500 3,000 431 4,400 $10,400 7,600 $12,500 General use 800 1,200 $11,200 $13,700 Stine Company applies manufacturing overhead to jobs at...

E16-2 Stine Company uses a job order cost system. On May 1, the company has a...

E16-2 Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,500 and two jobs in process: Job No. 429 $2,000, and Job No. 430 $1,500. During May, a summary of source documents reveals the following. Job Number 429 430 431 General use Materials Requisition Slips $2,500 3,500 4,400 $10,400 800 $11,200 Labor Time Tickets $1,900 3,000 7,600 $12,500 1,200 $13,700 Stine Company applies manufacturing overhead to jobs...

E16-2 Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,500 and two jobs in process: Job No. 429 $2,000, and Job No. 430 $1,500. During May, a summary of source documents reveals the following. Job Number 429 430 431 General use Materials Requisition Slips $2,500 3,500 4,400 $10,400 800 $11,200 Labor Time Tickets $1,900 3,000 7,600 $12,500 1,200 $13,700 Stine Company applies manufacturing overhead to jobs...

E2-2 Stine Company uses a job order cost system. On May 1, the company has a...

E2-2 Stine Company uses a job order cost system. On May 1, the company has a balance Prepare in Work in Process Inventory of $3,500 and two jobs in process: Job No. 429 $2,000, and manugfa Job No. 430 $1,500. During May, a summary of source documents reveals the following. (LO 1, 2 Materials Labor Time Tickets Job Number 429 430 431 General use Requisition Slips $2,500 3,500 4,400 $1,900 3,000 7,600 $10,400 800 $11,200 $12,500 1,200 $13,700 Stine Company...

E2-2 Stine Company uses a job order cost system. On May 1, the company has a balance Prepare in Work in Process Inventory of $3,500 and two jobs in process: Job No. 429 $2,000, and manugfa Job No. 430 $1,500. During May, a summary of source documents reveals the following. (LO 1, 2 Materials Labor Time Tickets Job Number 429 430 431 General use Requisition Slips $2,500 3,500 4,400 $1,900 3,000 7,600 $10,400 800 $11,200 $12,500 1,200 $13,700 Stine Company...

E15.2 (LO 1, 2, 3, 4) Stine Company uses a job order cost system. On May...

E15.2 (LO 1, 2, 3, 4) Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,500 and two jobs in process: Job No. 429 $2,000, and Job No. 430 $1,500. During May, a summary of source documents reveals the following. Materials Labor Job Number Requisition Slips Time Tickets 429 $2,500 3,500 4,400 $1,900 430 3,000 431 $10,400 $12,500 7,600 General use 800 1,200 $11,200 $13,700 Stine Company...

E15.2 (LO 1, 2, 3, 4) Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,500 and two jobs in process: Job No. 429 $2,000, and Job No. 430 $1,500. During May, a summary of source documents reveals the following. Materials Labor Job Number Requisition Slips Time Tickets 429 $2,500 3,500 4,400 $1,900 430 3,000 431 $10,400 $12,500 7,600 General use 800 1,200 $11,200 $13,700 Stine Company...

Exercise 2-2 Stine Company uses a job order cost system. On May 1, the company has...

Exercise 2-2 Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,920 and two jobs in process: Job No. 429 $2,600, and Job No. 430 $1,320. During May, a summary of source documents reveals the following. Materials Labor Time Job Number Requisition Slips Tickets 429 $3,040 $2,300 430 4,020 3,400 431/ 4,740 $11,800 7,900 $13,600 General use 900 1,310 $12,700 $14,910 Stine Company applies manufacturing overhead to...

Exercise 2-2 Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,920 and two jobs in process: Job No. 429 $2,600, and Job No. 430 $1,320. During May, a summary of source documents reveals the following. Materials Labor Time Job Number Requisition Slips Tickets 429 $3,040 $2,300 430 4,020 3,400 431/ 4,740 $11,800 7,900 $13,600 General use 900 1,310 $12,700 $14,910 Stine Company applies manufacturing overhead to...

Stine Company uses a job order cost system. On May 1, the company has a balance...

Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $4,240 and two jobs in process: Job No. 429 $2,580, and Job No. 430 $1,660. During May, a summary of source documents reveals the following Job Number 429 Materials Requisition Slips $3,040 3.680 4,710 $11.430 940 430 Labor Time Tickets $2,100 3,300 8,100 $13,500 1.360 $14,860 431 General use $12,370 Stine Company applies manufacturing overhead to jobs at...

Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $4,240 and two jobs in process: Job No. 429 $2,580, and Job No. 430 $1,660. During May, a summary of source documents reveals the following Job Number 429 Materials Requisition Slips $3,040 3.680 4,710 $11.430 940 430 Labor Time Tickets $2,100 3,300 8,100 $13,500 1.360 $14,860 431 General use $12,370 Stine Company applies manufacturing overhead to jobs at...

Stine Company uses a job order cost system. On May 1, the company has a balance...

Stine Company uses a job order cost system. On May 1, the

company has a balance in Work in Process Inventory of $4,240 and

two jobs in process: Job No. 429 $2,580, and Job No. 430 $1,660.

During May, a summary of source documents reveals the

following.

Job Number

Materials

Requisition Slips

Labor Time

Tickets

429

$3,040

$2,100

430

3,680

3,300

431

4,710

$11,430

8,100

$13,500

General use

940

1,360

$12,370

$14,860

Stine Company applies manufacturing overhead to jobs at...

Stine Company uses a job order cost system. On May 1, the

company has a balance in Work in Process Inventory of $4,240 and

two jobs in process: Job No. 429 $2,580, and Job No. 430 $1,660.

During May, a summary of source documents reveals the

following.

Job Number

Materials

Requisition Slips

Labor Time

Tickets

429

$3,040

$2,100

430

3,680

3,300

431

4,710

$11,430

8,100

$13,500

General use

940

1,360

$12,370

$14,860

Stine Company applies manufacturing overhead to jobs at...

Exercise 15-02 Stine Company uses a job order cost system. On May 1, the company has...

Exercise 15-02 Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $4,080 and two jobs in process: Job No. 429 $2,590, and Job No. 430 $1,490. During May, a summary of source documents reveals the following. Job Number 429 430 431 Materials Requisition Slips $2,870 3,660 4,500 $11,030 990 $12,020 Labor Time Tickets $2,100 3,600 7,700 $13,400 1,630 $15,030 General use Stine Company applies manufacturing overhead to...

Exercise 15-02 Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $4,080 and two jobs in process: Job No. 429 $2,590, and Job No. 430 $1,490. During May, a summary of source documents reveals the following. Job Number 429 430 431 Materials Requisition Slips $2,870 3,660 4,500 $11,030 990 $12,020 Labor Time Tickets $2,100 3,600 7,700 $13,400 1,630 $15,030 General use Stine Company applies manufacturing overhead to...

Exercise 20-2 Stine Company uses a job order cost system. On May 1, the company has...

Exercise 20-2 Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,650 and two jobs in process: Job No. 429 $2,290, and Job No. 430 $1,360. During May, a summary of source documents reveals the following. Materials Labor Time Tickets Job Number Requisition Slips 429 $2,950 $2,410 3,440 430 4,000 431 4,740 $11,690 8,080 $13,930 General use 900 1,750 $12,590 $15,680 Stine Company applies manufacturing overhead to...

Exercise 20-2 Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,650 and two jobs in process: Job No. 429 $2,290, and Job No. 430 $1,360. During May, a summary of source documents reveals the following. Materials Labor Time Tickets Job Number Requisition Slips 429 $2,950 $2,410 3,440 430 4,000 431 4,740 $11,690 8,080 $13,930 General use 900 1,750 $12,590 $15,680 Stine Company applies manufacturing overhead to...

Stine Company uses a job order cost system. On May 1, the company has a balance...

Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,510 and two jobs in process: Job No. 429 $2,150, and Job No. 430 $1,360. During May, a summary of source documents reveals the following. Job Number Labor Time Tickets 429 430 431 General use Materials Requisition Slips $2,970 4,100 4,540 $11,610 900 $12,510 $2,100 3,200 8,100 $13,400 1,590 $14,990 Stine Company applies manufacturing overhead to jobs at...

Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,510 and two jobs in process: Job No. 429 $2,150, and Job No. 430 $1,360. During May, a summary of source documents reveals the following. Job Number Labor Time Tickets 429 430 431 General use Materials Requisition Slips $2,970 4,100 4,540 $11,610 900 $12,510 $2,100 3,200 8,100 $13,400 1,590 $14,990 Stine Company applies manufacturing overhead to jobs at...

E16-2 Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,500 and two jobs in process: Job No. 429 $2,000, and Job No. 430 $1,500. During May, a summary of source documents reveals the following. Job Number 429 430 431 General use Materials Requisition Slips $2,500 3,500 4,400 $10,400 800 $11,200 Labor Time Tickets $1,900 3,000 7,600 $12,500 1,200 $13,700 Stine Company applies manufacturing overhead to jobs...

E16-2 Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,500 and two jobs in process: Job No. 429 $2,000, and Job No. 430 $1,500. During May, a summary of source documents reveals the following. Job Number 429 430 431 General use Materials Requisition Slips $2,500 3,500 4,400 $10,400 800 $11,200 Labor Time Tickets $1,900 3,000 7,600 $12,500 1,200 $13,700 Stine Company applies manufacturing overhead to jobs...

E2-2 Stine Company uses a job order cost system. On May 1, the company has a balance Prepare in Work in Process Inventory of $3,500 and two jobs in process: Job No. 429 $2,000, and manugfa Job No. 430 $1,500. During May, a summary of source documents reveals the following. (LO 1, 2 Materials Labor Time Tickets Job Number 429 430 431 General use Requisition Slips $2,500 3,500 4,400 $1,900 3,000 7,600 $10,400 800 $11,200 $12,500 1,200 $13,700 Stine Company...

E2-2 Stine Company uses a job order cost system. On May 1, the company has a balance Prepare in Work in Process Inventory of $3,500 and two jobs in process: Job No. 429 $2,000, and manugfa Job No. 430 $1,500. During May, a summary of source documents reveals the following. (LO 1, 2 Materials Labor Time Tickets Job Number 429 430 431 General use Requisition Slips $2,500 3,500 4,400 $1,900 3,000 7,600 $10,400 800 $11,200 $12,500 1,200 $13,700 Stine Company...

E15.2 (LO 1, 2, 3, 4) Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,500 and two jobs in process: Job No. 429 $2,000, and Job No. 430 $1,500. During May, a summary of source documents reveals the following. Materials Labor Job Number Requisition Slips Time Tickets 429 $2,500 3,500 4,400 $1,900 430 3,000 431 $10,400 $12,500 7,600 General use 800 1,200 $11,200 $13,700 Stine Company...

E15.2 (LO 1, 2, 3, 4) Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,500 and two jobs in process: Job No. 429 $2,000, and Job No. 430 $1,500. During May, a summary of source documents reveals the following. Materials Labor Job Number Requisition Slips Time Tickets 429 $2,500 3,500 4,400 $1,900 430 3,000 431 $10,400 $12,500 7,600 General use 800 1,200 $11,200 $13,700 Stine Company...

Exercise 2-2 Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,920 and two jobs in process: Job No. 429 $2,600, and Job No. 430 $1,320. During May, a summary of source documents reveals the following. Materials Labor Time Job Number Requisition Slips Tickets 429 $3,040 $2,300 430 4,020 3,400 431/ 4,740 $11,800 7,900 $13,600 General use 900 1,310 $12,700 $14,910 Stine Company applies manufacturing overhead to...

Exercise 2-2 Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,920 and two jobs in process: Job No. 429 $2,600, and Job No. 430 $1,320. During May, a summary of source documents reveals the following. Materials Labor Time Job Number Requisition Slips Tickets 429 $3,040 $2,300 430 4,020 3,400 431/ 4,740 $11,800 7,900 $13,600 General use 900 1,310 $12,700 $14,910 Stine Company applies manufacturing overhead to...

Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $4,240 and two jobs in process: Job No. 429 $2,580, and Job No. 430 $1,660. During May, a summary of source documents reveals the following Job Number 429 Materials Requisition Slips $3,040 3.680 4,710 $11.430 940 430 Labor Time Tickets $2,100 3,300 8,100 $13,500 1.360 $14,860 431 General use $12,370 Stine Company applies manufacturing overhead to jobs at...

Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $4,240 and two jobs in process: Job No. 429 $2,580, and Job No. 430 $1,660. During May, a summary of source documents reveals the following Job Number 429 Materials Requisition Slips $3,040 3.680 4,710 $11.430 940 430 Labor Time Tickets $2,100 3,300 8,100 $13,500 1.360 $14,860 431 General use $12,370 Stine Company applies manufacturing overhead to jobs at...

Stine Company uses a job order cost system. On May 1, the

company has a balance in Work in Process Inventory of $4,240 and

two jobs in process: Job No. 429 $2,580, and Job No. 430 $1,660.

During May, a summary of source documents reveals the

following.

Job Number

Materials

Requisition Slips

Labor Time

Tickets

429

$3,040

$2,100

430

3,680

3,300

431

4,710

$11,430

8,100

$13,500

General use

940

1,360

$12,370

$14,860

Stine Company applies manufacturing overhead to jobs at...

Stine Company uses a job order cost system. On May 1, the

company has a balance in Work in Process Inventory of $4,240 and

two jobs in process: Job No. 429 $2,580, and Job No. 430 $1,660.

During May, a summary of source documents reveals the

following.

Job Number

Materials

Requisition Slips

Labor Time

Tickets

429

$3,040

$2,100

430

3,680

3,300

431

4,710

$11,430

8,100

$13,500

General use

940

1,360

$12,370

$14,860

Stine Company applies manufacturing overhead to jobs at...

Exercise 15-02 Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $4,080 and two jobs in process: Job No. 429 $2,590, and Job No. 430 $1,490. During May, a summary of source documents reveals the following. Job Number 429 430 431 Materials Requisition Slips $2,870 3,660 4,500 $11,030 990 $12,020 Labor Time Tickets $2,100 3,600 7,700 $13,400 1,630 $15,030 General use Stine Company applies manufacturing overhead to...

Exercise 15-02 Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $4,080 and two jobs in process: Job No. 429 $2,590, and Job No. 430 $1,490. During May, a summary of source documents reveals the following. Job Number 429 430 431 Materials Requisition Slips $2,870 3,660 4,500 $11,030 990 $12,020 Labor Time Tickets $2,100 3,600 7,700 $13,400 1,630 $15,030 General use Stine Company applies manufacturing overhead to...

Exercise 20-2 Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,650 and two jobs in process: Job No. 429 $2,290, and Job No. 430 $1,360. During May, a summary of source documents reveals the following. Materials Labor Time Tickets Job Number Requisition Slips 429 $2,950 $2,410 3,440 430 4,000 431 4,740 $11,690 8,080 $13,930 General use 900 1,750 $12,590 $15,680 Stine Company applies manufacturing overhead to...

Exercise 20-2 Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,650 and two jobs in process: Job No. 429 $2,290, and Job No. 430 $1,360. During May, a summary of source documents reveals the following. Materials Labor Time Tickets Job Number Requisition Slips 429 $2,950 $2,410 3,440 430 4,000 431 4,740 $11,690 8,080 $13,930 General use 900 1,750 $12,590 $15,680 Stine Company applies manufacturing overhead to...

Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,510 and two jobs in process: Job No. 429 $2,150, and Job No. 430 $1,360. During May, a summary of source documents reveals the following. Job Number Labor Time Tickets 429 430 431 General use Materials Requisition Slips $2,970 4,100 4,540 $11,610 900 $12,510 $2,100 3,200 8,100 $13,400 1,590 $14,990 Stine Company applies manufacturing overhead to jobs at...

Stine Company uses a job order cost system. On May 1, the company has a balance in Work in Process Inventory of $3,510 and two jobs in process: Job No. 429 $2,150, and Job No. 430 $1,360. During May, a summary of source documents reveals the following. Job Number Labor Time Tickets 429 430 431 General use Materials Requisition Slips $2,970 4,100 4,540 $11,610 900 $12,510 $2,100 3,200 8,100 $13,400 1,590 $14,990 Stine Company applies manufacturing overhead to jobs at...

Most questions answered within 3 hours.

-

Write a program to solve the Josephus problem, with the following

modification:

Sample Input:

./a.out n...

asked 2 hours ago -

At the start of a CD it is spinning at a rate of 525 rpm

(revolutions...

asked 2 hours ago -

4. Without doing any calculations, predict whether the observed

∆T would increase, decrease or remain the...

asked 4 hours ago -

Based on the range, which of the following sets of scores has

the greatest variability? 3,...

asked 5 hours ago -

Ripples in a pond travel at a velocity of 3 m/s with one peak

passing a...

asked 5 hours ago -

A man stands on the roof of a building of height 13.0 mm and

throws a...

asked 5 hours ago -

The extent to which assets are financed by borrowed funds and

other liabilities is indicated by:...

asked 6 hours ago -

Explain in detail

Germany is the fifth largest economy

explain what goods and services Germany specializes...

asked 6 hours ago -

The density of platinum is 21.45 g/mL. If a cube of platinum

with a mass of...

asked 6 hours ago -

Accounts Receivable

Sales

A/R Posting

Extended Sales Invoice

Packing Slip

Compare invoice to packing slip 2...

asked 6 hours ago -

Michaella, age 23, is a full-time law student and is claimed by

her parents as a...

asked 6 hours ago -

Why are polymers not typically casted into products?

asked 6 hours ago