E15-2 (Recording the Issuance of Common and Preferred Stock) Kathleen Battle Corporation was organized on January...

E15-2 (Recording the Issuance of Common and Preferred Stock) Kathleen Battle Corporation was organized on January 1, 2014. It is authorized to issue 10,000 shares of 8%, $100 par value preferred stock, and 500,000 shares of no-par common stock with a stated value of $1 per share. The following stock transactions were completed during the first year.

Jan. 10 Issued 80,000 shares of common stock for cash at $5 per share.

Mar.1 Issued 5,000 shares of preferred stock for cash at $108 per share.

Apr. 1 Issued24, 000shares of common stock for land. The asking price of the land was$90,000; the fair value of the land was $80,000.

May1 Issued 80,000 shares of common stock for cash at $7 per share.

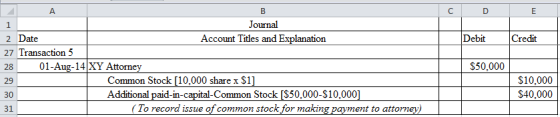

Aug.1 Issued 10,000 shares of common stock to attorneys in payment of their bill of $50,000 for services rendered in helping the company organizes.

Sept. 1 Issued 10,000 shares of common stock for cash at $9 per share.

Nov.1 Issued 1,000 shares of preferred stock for cash at $112 per share.

Instructions

Prepare the journal entries to record the above transactions

Homework Answers

Transaction: It is an agreement which creates a legal obligation between two or more parties for exchanging the goods or providing the services. The transactions which can be measured in money are to be recorded in financial books.

Journal Entry: It refers to an entry in the journal. It is a way to record the accounting transactions in a chronological way, which is when the transaction occurs.

Ledger: It is the account or graphical representation of general ledger account or its entries. The left side of T-account is debit side and the right side represents as credit side.

Rules of debit and credit have been followed for journalizing the various transactions and these are:

Debit the Receiver and Credit the Giver: It is used for personal accounts. It indicates when the organization receives something from anyone then, what is received would be debited and the giver would be credited.

Debit what comes in and Credit what goes out: It is used for real accounts. It indicates when the organization purchased or receives any asset then it would be debited and on the other side, when the asset is going out of the organization then, it would be credited.

Debit all expenses and losses, credit all incomes and gains: It is used in case of a nominal account, and according to this rule all the expenses and losses incurred by the organization would be debited and on the other side, all the incomes and gain of the organization would be credited. There are five categories of accounts:

Assets: It can be defined as the resources which are controlled and owned by the organization and which are capable of providing some future benefits for operating the core business of the organization. Whenever any asset has been purchased or any transaction which increases the amount of asset, the asset account will be debited.

Liabilities: These are referred as company’s financial obligation arising during the course of Business Cycle, which will be settled by the outflow of resources. Whenever any transaction raises the amount of liability, the liability account will be credited.

Revenues: It is income that an entity earns from its normal business operations. It reflects the amount which is received by the firm by manufacturing or providing goods and services. Whenever income has been earned or due, the revenue account will be credited.

Expenses: These are the gross outflows incurred by a business entity while carrying out their regular business operations like manufacturing and providing goods and services. Whenever any expense has been due to be incurred, the expense account has been debited.

Capital account: This account represents the balance of amount invested by the stockholders. It also includes the earnings which are due and not withdrawn by the stockholders. Whenever any transaction increases the amount of capital, the capital account will be credited.

KB issued 80,000 common stocks for cash at $5 per share

KB issued 5,000 preferred stocks for cash at $108 per share.

KB issue 24,000 common stock for the purchase of land and fair value for land was $80,000 asking price of land was $90,000.

KB issued 80,000 number of common stock for cash at $7 per share.

KB issued 10,000 common stock against attorney’s bill of $50,000 for their services to the company.

KB issued 10,000 in numbers common stock for cash at $9 per share.

KB issued 1,000 in numbers of preferred stock for cash at $112 per share.

Add Answer to:

E15-2 (Recording the Issuance of Common and Preferred Stock)

Kathleen Battle Corporation was organized on January...

Most questions answered within 3 hours.

-

Suppose the method of tree ring dating gave the following dates

A.D. for an archaeological excavation...

asked 22 minutes ago -

Network security

1. explain succinctly how a Denial of Service attack may occur

on an implementation...

asked 12 minutes ago -

Name two of the basic guidelines for business dress that women

should follow in cultures other...

asked 13 minutes ago -

How can organizations create value by implementing an advanced

information system solution paired with the appropriate...

asked 14 minutes ago -

You are designing a wastewater treatment system using a

constructed wetland. The inputs will be high...

asked 17 minutes ago -

A 43kg teen grabs onto a rope swing. The length of rope between

the teen and...

asked 25 minutes ago -

In a certain oscillating LC circuit, the total energy

is converted from electrical energy in the...

asked 28 minutes ago -

JAVA - OOP inheritance help please

I have a question,

I have 4 classes.

College, course,...

asked 28 minutes ago -

what is the distinction between the purpose of healthcare

management and the purpose od healthcare financial...

asked 42 minutes ago -

When disposable income is $1000, consumer spending is $950. The

value of the multiplier for this...

asked 51 minutes ago -

Calculate the pH of a buffer solution that is

0.116 M in

C2H5NH2

(ethylamine) and 0.403...

asked 51 minutes ago -

#include <iostream>

#include <vector>

using namespace std;

class Solution {

public:

vector<int> smallerNumbersThanCurrent(vector<int>&

nums) {

int...

asked 1 hour ago