Homework Answers

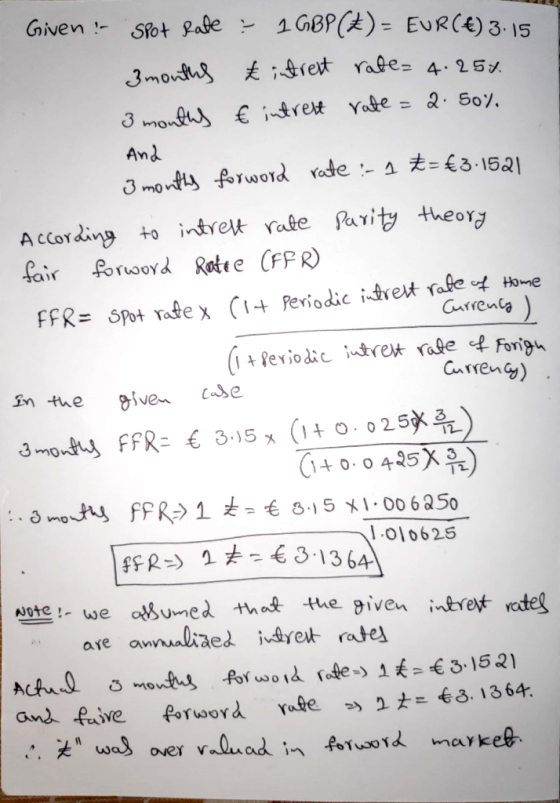

give problem was solved on the

basis of intrest rate parity theory.

give problem was solved on the

basis of intrest rate parity theory.

The fair forword rate calculated using intrest rate parity theory was lower than the actual available forward rate in the market,

This situation leads to possibility of an arbitrage

Accordingly an exposure of €10000 was taken and the arbitrage strategy was explained in the above posted images

Which stating an earning of €50.49 without any risk at the end of 3rd month

Add Answer to:

Map a three month currency (GBP/EUR) forward with the following features: GBP/EUR spot 3.15; 3 months...

Problem 5 The current spot rate is EUR/GBP 1.1600 and the six-month forward rate is EUR/...

Problem 5 The current spot rate is EUR/GBP 1.1600 and the six-month forward rate is EUR/ GBP 1.16300. The six-month interest rate in the UK is 0.40% and the six-month interest rate in the Eurozone is 0.44%. What would the British interest rate have to be per annum so that there would be no arbitrage opportunity? (round up your answer to the 4th digit)

Question: 2 following FX rates & interest rates CURRENCY SPOT RATES INTEREST RATES 3M (84...

Question: 2 following FX rates & interest rates CURRENCY SPOT RATES INTEREST RATES 3M (84 DAYS) (%) INTEREST RATES 6M (181 DAYS) (%) EURO/USD 1.0607/15 EUR 3 MONTH 0.02/0.04 EUR 6M 0.1/0.15 GBP/USD 1.5089/106 GBP 3 MONTH 0.25/0.30 GBP 6M 0.30/0.35 AUD/USD 0.7225/33 AUD 3 MONTH 1.05/10 AUD 6M 1.25/35 USD/JPY 122.55/72 JPY 3 MONTH 0.10/15 JPY 6M 0.15/20 USD/CNY 6.3920/45 CNY 3 MONTH 3.80/90 CNY 6M 4.10/20 USD/PKR 106.10/20 PKR 3 MONTH 5.90/00 PKR 6M 6.10/20 USD 3...

Calculate the following currency forward rates A) 1-year USD/CAD Spot rate: Risk-free USD rate: Risk-free CAD...

Calculate the following currency forward rates A) 1-year USD/CAD Spot rate: Risk-free USD rate: Risk-free CAD rate: 1.4040 2.37% p.a.d 0.92% pa.d B) 6-month CHF/JPY Spot rate: Risk-free CHF rate: Risk-free JPY rate: 121.61 -0.70% pa.d 0.19% p.a.d C) 3-month EUR/MXN Spot rate: Risk-free EUR rate: Risk-free MXN rate: 23.8 -0.61% 5.30%

Calculate the following currency forward rates A) 1-year USD/CAD Spot rate: Risk-free USD rate: Risk-free CAD rate: 1.4040 2.37% p.a.d 0.92% pa.d B) 6-month CHF/JPY Spot rate: Risk-free CHF rate: Risk-free JPY rate: 121.61 -0.70% pa.d 0.19% p.a.d C) 3-month EUR/MXN Spot rate: Risk-free EUR rate: Risk-free MXN rate: 23.8 -0.61% 5.30%

Problem 1 The following quotes are given for CAD/EUR: 1.4530/14535, 15-10, 22-14,30-20 for the spot, one...

Problem 1 The following quotes are given for CAD/EUR: 1.4530/14535, 15-10, 22-14,30-20 for the spot, one month, three months and six months forward contracts. a) calculate the outright quotations and the spread for the spot rate and the 3-month forward contract. b) how is the spread related to time to maturity of the forward contract? c) determine the percentage premium/ discount of the Canadian dollar with respect to the euro for the 3 months ask rates (annualized).

Exercise 1 There are the following quotations: Spot EUR/PLN 4,7200 Forward EUR/PLN 4,7500 Call EUR option...

Exercise 1 There are the following quotations: Spot EUR/PLN 4,7200 Forward EUR/PLN 4,7500 Call EUR option @ 4,7650 PLN - premium 0,0500 PLN/EUR Put EUR option @ 4,7650 PLN-premium 0,1550 PLN/EUR What will be your profit if you construct a synthetic forward and take the opposite position on the forward market

Exercise 1 There are the following quotations: Spot EUR/PLN 4,7200 Forward EUR/PLN 4,7500 Call EUR option @ 4,7650 PLN - premium 0,0500 PLN/EUR Put EUR option @ 4,7650 PLN-premium...

Exercise 1 There are the following quotations: Spot EUR/PLN 4,7200 Forward EUR/PLN 4,7500 Call EUR option @ 4,7650 PLN - premium 0,0500 PLN/EUR Put EUR option @ 4,7650 PLN-premium 0,1550 PLN/EUR What will be your profit if you construct a synthetic forward and take the opposite position on the forward market

Exercise 1 There are the following quotations: Spot EUR/PLN 4,7200 Forward EUR/PLN 4,7500 Call EUR option @ 4,7650 PLN - premium 0,0500 PLN/EUR Put EUR option @ 4,7650 PLN-premium...

points) Compute the forward premium for Spot rate Yen / USD - 85.25: Forward rate 3...

points) Compute the forward premium for Spot rate Yen / USD - 85.25: Forward rate 3 months forward premium (or discount with the following months = 83.60 Ground your (6) Spot rate USD/EUR - 1.13; Forward rate 6 months - 1. o months LTO (round your answer to 2 de

points) Compute the forward premium for Spot rate Yen / USD - 85.25: Forward rate 3 months forward premium (or discount with the following months = 83.60 Ground your (6) Spot rate USD/EUR - 1.13; Forward rate 6 months - 1. o months LTO (round your answer to 2 de

The current spot exchange rate is $1.55/€ and the three-month forward rate is $1.50/€. You are...

The current spot exchange rate is $1.55/€ and the three-month forward rate is $1.50/€. You are selling €1,000 forward for $. How much in $ are you receiving in three months? If the spot exchange rate is $1.60/€ in three months, how much is the gain or loss from the forward hedge?

The spot EUR/USD is 1.12 and the forward rate is 1.1. The interest rate in France...

The spot EUR/USD is 1.12 and the forward rate is 1.1. The interest rate in France is 3% and 4% in the US. a) Does the iRP hold? b) If not, how could you make a CIA profit by using 1000 EUR? Show your work. c) What is the forward rate that would make CIA disappear?

Calculate the forward premium on the dollar (the dollar is the home currency) if the spot...

Calculate the forward premium on the dollar (the dollar is the home currency) if the spot rate is €1.3300/$ and the 3-month forward rate is €1.3400/$. Note: Use a 360-day year. The forward premium on the dollar is _____________%. (Round to four decimal places).

QUESTION 1: Suppose that the current spot exchange rate is GBP1= €1.50 and the one-year forward...

QUESTION 1: Suppose that the current spot exchange rate is GBP1= €1.50 and the one-year forward exchange rate is GBP1=€1.60. One-year interest rate is 5.4% in euros and 5.2% in pounds. If you have EUR1,000,000, what is the Covered Interest arbitrage profit in EUR? QUESTION 2: Suppose that the current spot exchange rate is GBP1= €1.50 and the one-year forward exchange rate is GBP1=€1.60. One-year interest rate is 5.4% in euros and 5.2% in pounds. If you conduct covered interest...

Calculate the following currency forward rates A) 1-year USD/CAD Spot rate: Risk-free USD rate: Risk-free CAD rate: 1.4040 2.37% p.a.d 0.92% pa.d B) 6-month CHF/JPY Spot rate: Risk-free CHF rate: Risk-free JPY rate: 121.61 -0.70% pa.d 0.19% p.a.d C) 3-month EUR/MXN Spot rate: Risk-free EUR rate: Risk-free MXN rate: 23.8 -0.61% 5.30%

Calculate the following currency forward rates A) 1-year USD/CAD Spot rate: Risk-free USD rate: Risk-free CAD rate: 1.4040 2.37% p.a.d 0.92% pa.d B) 6-month CHF/JPY Spot rate: Risk-free CHF rate: Risk-free JPY rate: 121.61 -0.70% pa.d 0.19% p.a.d C) 3-month EUR/MXN Spot rate: Risk-free EUR rate: Risk-free MXN rate: 23.8 -0.61% 5.30%

Exercise 1 There are the following quotations: Spot EUR/PLN 4,7200 Forward EUR/PLN 4,7500 Call EUR option @ 4,7650 PLN - premium 0,0500 PLN/EUR Put EUR option @ 4,7650 PLN-premium 0,1550 PLN/EUR What will be your profit if you construct a synthetic forward and take the opposite position on the forward market

Exercise 1 There are the following quotations: Spot EUR/PLN 4,7200 Forward EUR/PLN 4,7500 Call EUR option @ 4,7650 PLN - premium 0,0500 PLN/EUR Put EUR option @ 4,7650 PLN-premium...

Exercise 1 There are the following quotations: Spot EUR/PLN 4,7200 Forward EUR/PLN 4,7500 Call EUR option @ 4,7650 PLN - premium 0,0500 PLN/EUR Put EUR option @ 4,7650 PLN-premium 0,1550 PLN/EUR What will be your profit if you construct a synthetic forward and take the opposite position on the forward market

Exercise 1 There are the following quotations: Spot EUR/PLN 4,7200 Forward EUR/PLN 4,7500 Call EUR option @ 4,7650 PLN - premium 0,0500 PLN/EUR Put EUR option @ 4,7650 PLN-premium...

points) Compute the forward premium for Spot rate Yen / USD - 85.25: Forward rate 3 months forward premium (or discount with the following months = 83.60 Ground your (6) Spot rate USD/EUR - 1.13; Forward rate 6 months - 1. o months LTO (round your answer to 2 de

points) Compute the forward premium for Spot rate Yen / USD - 85.25: Forward rate 3 months forward premium (or discount with the following months = 83.60 Ground your (6) Spot rate USD/EUR - 1.13; Forward rate 6 months - 1. o months LTO (round your answer to 2 de

Most questions answered within 3 hours.

-

Kylie is a single mom with two dependent children,

Tanner, age 7 and Olivia, age 11....

asked 7 minutes ago -

Phosphorous + bromine = phosphorous tribromide. If 35.0 g of

bromine are reacted and 27.9 grams...

asked 1 hour ago -

Derive the long wavelength limit of the Planck energy density

distribution

asked 1 hour ago -

Calculate the pH of each of the following solutions.

0.50 M HBr

3.1×10−4 M KOH

4.2×10−5...

asked 5 hours ago -

For the year ended December 31, Depot Max’s cost of merchandise

sold was $85,600. Inventory at the...

asked 5 hours ago -

Week 10 - Professional Memo Assignment

Professional Memo Assignment

Your mission for this week, should you...

asked 5 hours ago -

Write a Python program that stores the data for each

player on the team, and it...

asked 5 hours ago -

In

the last 3 months, mike never knows when he is going to get his

allowance...

asked 5 hours ago -

Is Ca(OH)2 a Bronsted base, Lewis base, or both? Why?

asked 5 hours ago -

1A- Why don’t voters complain about U.S. tariffs on imported

sugar?

Because sugar is only a...

asked 5 hours ago -

Cash Payback Period

Primera Banco is evaluating two capital investment proposals for

a drive-up ATM kiosk,...

asked 5 hours ago -

Create a button in Swift (Xcode) that will create a charge,

create a charge using Stripe's...

asked 5 hours ago