The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

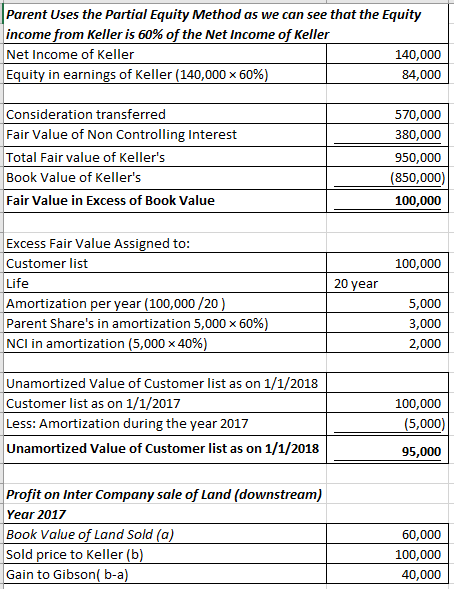

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $570,000. At the acquisition date, the fair value of the noncontrolling interest was $380,000 and Keller’s book value was $850,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $100,000. This intangible asset is being amortized over 20 years. Gibson sold Keller land with a book value of $60,000 on January 2, 2017, for $100,000. Keller still holds this land at the end of the current year. Keller regularly transfers inventory to Gibson. In 2017, it shipped inventory costing $100,000 to Gibson at a price of $150,000. During 2018, intra-entity shipments totaled $200,000, although the original cost to Keller was only $140,000. In each of these years, 20 percent of the merchandise was not resold to outside parties until the period following the transfer. Gibson owes Keller $40,000 at the end of 2018. Gibson Company Keller Company Sales $ (800,000) $ (500,000) Cost of goods sold 500,000 300,000 Operating expenses 100,000 60,000 Equity in earnings of Keller (84,000) –0– Net income $ (284,000) $ (140,000) Retained earnings, 1/1/18 $(1,116,000) $ (620,000) Net income (above) (284,000) (140,000) Dividends declared 115,000 60,000 Retained earnings, 12/31/18 $(1,285,000) $ (700,000) Cash $ 177,000 $ 90,000 Accounts receivable 356,000 410,000 Inventory 440,000 320,000 Investment in Keller 726,000 –0– Land 180,000 390,000 Buildings and equipment (net) 496,000 300,000 Total assets $ 2,375,000 $ 1,510,000 Liabilities $ (480,000) $ (400,000) Common stock (610,000) (320,000) Additional paid-in capital –0– (90,000) Retained earnings, 12/31/18 (1,285,000) (700,000) Total liabilities and equities $(2,375,000) $(1,510,000) Prepare a worksheet to consolidate the separate 2018 financial statements for Gibson and Keller. How would the consolidation entries in requirement (a) have differed if Gibson had sold a building with a $60,000 book value (cost of $140,000) to Keller for $100,000 instead of land, as the problem reports? Assume that the building had a 10-year remaining life at the date of transfer.

Homework Answers

![[A] 95,000 Customer List Investment in Keller (60%) Non Controlling Interest in Keller, 1/1/18 (40%) (to recognized the unamo](http://img.homeworklib.com/questions/e0733de0-7498-11ea-958c-17be264f0f5f.png?x-oss-process=image/resize,w_560)

![Investment in Keller Debit Credit 36,000 Entry [D] Entry [C] Entry [S] Entry [0] Entry [A] Total Adjustment 9,000 612,000 84,](http://img.homeworklib.com/questions/e19c93d0-7498-11ea-9905-e16a17d980c9.png?x-oss-process=image/resize,w_560)

Add Answer to:

The individual financial statements for Gibson Company and

Keller Company for the year ending December 31,...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $420,000. At the acquisition date, the fair value of the noncontrolling interest was $280,000 and Keller’s book value was $550,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $150,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $930,000. At the acquisition date, the fair value of the noncontrolling interest was $620,000 and Keller’s book value was $1,240,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $310,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $420,000. At the acquisition date, the fair value of the noncontrolling interest was $280,000 and Keller’s book value was $550,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $150,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $420,000. At the acquisition date, the fair value of the noncontrolling interest was $280,000 and Keller’s book value was $550,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $150,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $390,000. At the acquisition date, the fair value of the noncontrolling interest was $260,000 and Keller's book value was $510,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition date fair value of $140,000. This...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $390,000. At the acquisition date, the fair value of the noncontrolling interest was $260,000 and Keller's book value was $510,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition date fair value of $140,000. This...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $720,000. At the acquisition date, the fair value of the noncontrolling interest was $480,000 and Keller’s book value was $960,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $240,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $510,000. At the acquisition date, the fair value of the noncontrolling interest was $340,000 and Keller’s book value was $670,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $180,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $450,000. At the acquisition date, the fair value of the noncontrolling interest was $300,000 and Keller’s book value was $590,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $160,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $510,000. At the acquisition date, the fair value of the noncontrolling interest was $340,000 and Keller's book value was $670,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $180,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $510,000. At the acquisition date, the fair value of the noncontrolling interest was $340,000 and Keller's book value was $670,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $180,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31,...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $1,050,000. At the acquisition date, the fair value of the noncontrolling interest was $700,000 and Keller's book value was $1,400,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $350,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $1,050,000. At the acquisition date, the fair value of the noncontrolling interest was $700,000 and Keller's book value was $1,400,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $350,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $390,000. At the acquisition date, the fair value of the noncontrolling interest was $260,000 and Keller's book value was $510,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition date fair value of $140,000. This...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $390,000. At the acquisition date, the fair value of the noncontrolling interest was $260,000 and Keller's book value was $510,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition date fair value of $140,000. This...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $510,000. At the acquisition date, the fair value of the noncontrolling interest was $340,000 and Keller's book value was $670,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $180,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $510,000. At the acquisition date, the fair value of the noncontrolling interest was $340,000 and Keller's book value was $670,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $180,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $1,050,000. At the acquisition date, the fair value of the noncontrolling interest was $700,000 and Keller's book value was $1,400,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $350,000. This intangible...

The individual financial statements for Gibson Company and Keller Company for the year ending December 31, 2018, follow. Gibson acquired a 60 percent interest in Keller on January 1, 2017, in exchange for various considerations totaling $1,050,000. At the acquisition date, the fair value of the noncontrolling interest was $700,000 and Keller's book value was $1,400,000. Keller had developed internally a customer list that was not recorded on its books but had an acquisition-date fair value of $350,000. This intangible...

Most questions answered within 3 hours.

-

D. A student completed 20 courses in the School of Arts and

Sciences. Her grades in...

asked 1 hour ago -

teo

pucks moving on a frictionless air table are about to collide. the

1.5 kg puck...

asked 1 hour ago -

Problem #1

The area between Z = 0 and Z = 2.50

The area between Z...

asked 3 hours ago -

1. What is the meaning of the term communication style?

2. What are the benefits to...

asked 2 hours ago -

9.) You are buying a car that cost $26,500. You make payments of

$412 each month...

asked 2 hours ago -

. Suppose a discrete random variable has probability

distribution

P(x) = .2 if x = 0...

asked 4 hours ago -

Under the influence of its drive force, a snowmobile is moving

at a constant velocity along...

asked 4 hours ago -

Why do organizations decline? What steps can top

management take to halt, decline, and restore organizational...

asked 4 hours ago -

What mechanisms Drive speciation??

(I.e. what was Dawins theory on the orgin of species, and how...

asked 5 hours ago -

The manager at a car assembly plant believes that the mean

assembly time for a car...

asked 6 hours ago -

Which of the following is true of electron capture?

A) It decreases the nuclide's mass number...

asked 8 hours ago -

Assuming an efficiency of 43.10%, calculate the actual yield of

magnesium nitrate formed from 114.9 g...

asked 8 hours ago