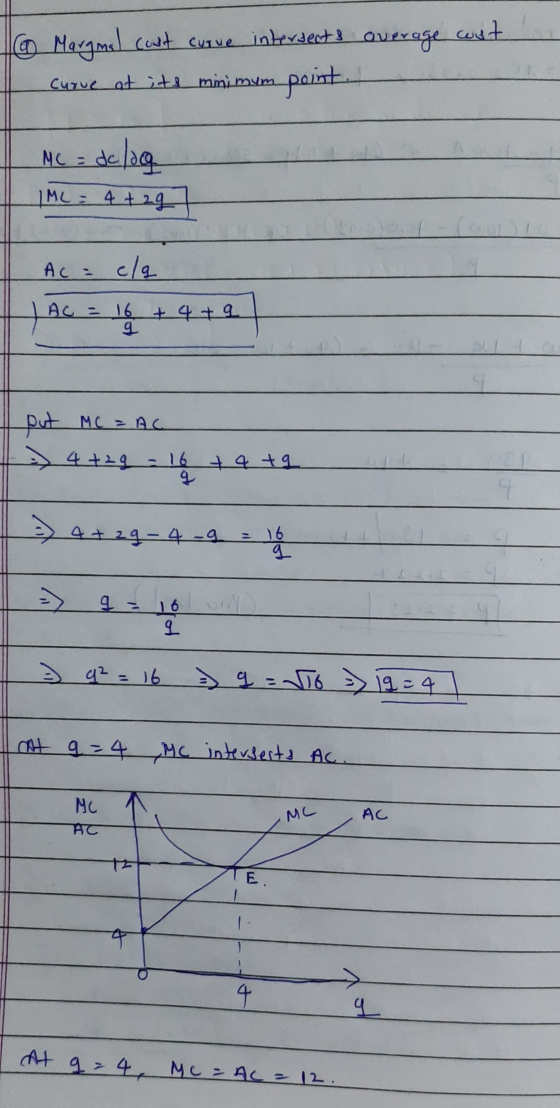

In a perfectly competitive market, a firm has the following short-run total cost function: C(q)=16+4q+q2 The...

In a perfectly competitive market, a firm has the following short-run total cost function:

C(q)=16+4q+q2

The market demand is

Q(p)=220-p

a. Show that marginal cost curve passes through the minimum point of average cost curve. Draw a figure to show it.

b. Find the firm’s individual short-run supply function. Draw it on the above figure. For the following questions, suppose that there are currently 10 identical firms in this market.

c. What is the market supply curve? What are the market equilibrium price and quantity?

d. In equilibrium, how much does each firm produce? How much is its profit? (It is short run, so it is possible for a firm to earn positive profit)

Homework Answers

Add Answer to:

In a perfectly competitive market, a firm has the following

short-run total cost function:

C(q)=16+4q+q2

The...

A firm in a perfectly competitive market has a short-run total cost curve of ST C(Q)...

A firm in a perfectly competitive market has a short-run total cost curve of ST C(Q) = 20 + 10Q + Q2. The market price is $10. a) What is the profit-maximizing quantity? b) What are the maximum profits? c) Find the short-run supply curve if all fixed costs are sunk. d) Find the short-run supply curve if all fixed costs are non-sunk. e) Suppose there are 100 identical firms in this market. What is the market supply curve if...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q)...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q) = 4 +q? where q is the firm-specific level of production of the representative firm. The market demand function is Q(p) = 400 - 4p where Q(p) is the aggregate demand in the market (expressed as function of price) and p is the price a) Derive the firm-specific supply function of the representative firm as a function of price b) Assume there are N...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q) = 4 +q? where q is the firm-specific level of production of the representative firm. The market demand function is Q(p) = 400 - 4p where Q(p) is the aggregate demand in the market (expressed as function of price) and p is the price a) Derive the firm-specific supply function of the representative firm as a function of price b) Assume there are N...

Exercise 1. Short-Run Industry Supply Curve In a perfectly competitive market there are n firms with...

Exercise 1. Short-Run Industry Supply Curve In a perfectly competitive market there are n firms with identical technology: yi=Li½Ki½. Each firm’s cost function is Ci=wLi+rKi where w=r=1. a) In the short run all firms have a fixed level of Ki=100, so that yi=10Li½ and Ci=Li+100. What is the cost function Ci(yi)? What is the short-run average cost function ACi(yi)? b) What is each firm’s marginal cost function MCi(yi)? What is each firm’s short-run supply function si(p)? Find the inverse of...

need help with 5 and 6 Suppose a perfectly competitive firm's cost function is C(q)-4q*+16. Marginal cost for the firm...

need help with 5 and 6

Suppose a perfectly competitive firm's cost function is C(q)-4q*+16. Marginal cost for the firm is given by MC=8q. 1) Find equations for variable cost, fixed cost, average total cost, average variable cost and average fixed cost for this firm. Illustrate on a graph the firm's average variable cost curve, average total cost curve, and marginal cost curve. 2) Find the outputs that minimize average total cost, average variable cost and average fixed cost. 3)...

need help with 5 and 6

Suppose a perfectly competitive firm's cost function is C(q)-4q*+16. Marginal cost for the firm is given by MC=8q. 1) Find equations for variable cost, fixed cost, average total cost, average variable cost and average fixed cost for this firm. Illustrate on a graph the firm's average variable cost curve, average total cost curve, and marginal cost curve. 2) Find the outputs that minimize average total cost, average variable cost and average fixed cost. 3)...

cardboard boxes are produced in a perfectly competitive market. each identical firm has a short run...

cardboard boxes are produced in a perfectly

competitive market. each identical firm has a short run total cost

curve of TC= 3Q^3 - 12Q^2 +16Q + 100, where Q is measured in

thousands of boxes per week. calculate the output for the price

below which a firm in the market will not produce any output in the

short run. ( i.e., the output for the shut down price)

a 2^1/2

b. 2

c. 1/2

d. 1/square root of 2

2)...

cardboard boxes are produced in a perfectly

competitive market. each identical firm has a short run total cost

curve of TC= 3Q^3 - 12Q^2 +16Q + 100, where Q is measured in

thousands of boxes per week. calculate the output for the price

below which a firm in the market will not produce any output in the

short run. ( i.e., the output for the shut down price)

a 2^1/2

b. 2

c. 1/2

d. 1/square root of 2

2)...

Short-run Equilibrium: Bumper sticker firms produce bumper stickers in a perfectly competitive market. Each identical firm...

Short-run Equilibrium: Bumper sticker firms produce bumper stickers in a perfectly competitive market. Each identical firm has a short-run total cost function equal to: STC (Q) = 3 + 2q + 2Q2. Suppose that there are 100 firms, and the market demand is D(P) = 100 - 5P where D(P) is the quantity consumed in the market when the market price is P. 1. What is the short-run equilibrium price? 2. How much does each firm produce? 3. Are they...

Short-run Equilibrium: Bumper sticker firms produce bumper stickers in a perfectly competitive market. Each identical firm has a short-run total cost function equal to: STC (Q) = 3 + 2q + 2Q2. Suppose that there are 100 firms, and the market demand is D(P) = 100 - 5P where D(P) is the quantity consumed in the market when the market price is P. 1. What is the short-run equilibrium price? 2. How much does each firm produce? 3. Are they...

Suppose a perfectly competitive firm has the short-run cost function C = 125 + q2. Use...

Suppose a perfectly competitive firm has the short-run cost function C = 125 + q2. Use the derivative formula or marginal cost to determine the firm’s output level and profit at prices of $30 and $20. At what price does the firm reach the shut-down point?

i) The long run cost function for each firm in a perfectly competitive market is c(q)...

i) The long run cost function for each firm in a perfectly competitive market is c(q) = 2^1.5+16q^0.5, LMC = 1.59^0.5+ 8q^-0.5, market demand curve is Q=1600-2p. Find price (p) of output and the level of output (q) produced by the firm in a long run equilibrium. Find the long run average cost curve for the firm. ii) what happens in the long run if the market demand curve shifts to Q=160-20p?/ -A competitive industry is in long run equilibrium....

i) The long run cost function for each firm in a perfectly competitive market is c(q) = 2^1.5+16q^0.5, LMC = 1.59^0.5+ 8q^-0.5, market demand curve is Q=1600-2p. Find price (p) of output and the level of output (q) produced by the firm in a long run equilibrium. Find the long run average cost curve for the firm. ii) what happens in the long run if the market demand curve shifts to Q=160-20p?/ -A competitive industry is in long run equilibrium....

Suppose there is a perfectly competitive industry where all the firms are identical with identical cost...

Suppose there is a perfectly competitive industry where all the firms are identical with identical cost curves. Furthermore, suppose that a representative firm’s total cost is given by the equation TC = 100 + q2 + q where q is the quantity of output produced by the firm. You also know that the market demand for this product is given by the equation P = 900 - 2Q where Q is the market quantity. In addition, you are told that...

A firm operates in a perfectly competitive industry. Suppose it has a short run total cost...

A firm operates in a perfectly competitive industry. Suppose it has a short run total cost function given by TC = 1200 + 2Q + 0.03Q2. If the market price is $38, what is the firm’s profit maximizing quantity?

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q) = 4 +q? where q is the firm-specific level of production of the representative firm. The market demand function is Q(p) = 400 - 4p where Q(p) is the aggregate demand in the market (expressed as function of price) and p is the price a) Derive the firm-specific supply function of the representative firm as a function of price b) Assume there are N...

Consider a perfectly competitive market comprised of identical firms each facing the following cost function: C(q) = 4 +q? where q is the firm-specific level of production of the representative firm. The market demand function is Q(p) = 400 - 4p where Q(p) is the aggregate demand in the market (expressed as function of price) and p is the price a) Derive the firm-specific supply function of the representative firm as a function of price b) Assume there are N...

need help with 5 and 6

Suppose a perfectly competitive firm's cost function is C(q)-4q*+16. Marginal cost for the firm is given by MC=8q. 1) Find equations for variable cost, fixed cost, average total cost, average variable cost and average fixed cost for this firm. Illustrate on a graph the firm's average variable cost curve, average total cost curve, and marginal cost curve. 2) Find the outputs that minimize average total cost, average variable cost and average fixed cost. 3)...

need help with 5 and 6

Suppose a perfectly competitive firm's cost function is C(q)-4q*+16. Marginal cost for the firm is given by MC=8q. 1) Find equations for variable cost, fixed cost, average total cost, average variable cost and average fixed cost for this firm. Illustrate on a graph the firm's average variable cost curve, average total cost curve, and marginal cost curve. 2) Find the outputs that minimize average total cost, average variable cost and average fixed cost. 3)...

cardboard boxes are produced in a perfectly

competitive market. each identical firm has a short run total cost

curve of TC= 3Q^3 - 12Q^2 +16Q + 100, where Q is measured in

thousands of boxes per week. calculate the output for the price

below which a firm in the market will not produce any output in the

short run. ( i.e., the output for the shut down price)

a 2^1/2

b. 2

c. 1/2

d. 1/square root of 2

2)...

cardboard boxes are produced in a perfectly

competitive market. each identical firm has a short run total cost

curve of TC= 3Q^3 - 12Q^2 +16Q + 100, where Q is measured in

thousands of boxes per week. calculate the output for the price

below which a firm in the market will not produce any output in the

short run. ( i.e., the output for the shut down price)

a 2^1/2

b. 2

c. 1/2

d. 1/square root of 2

2)...

Short-run Equilibrium: Bumper sticker firms produce bumper stickers in a perfectly competitive market. Each identical firm has a short-run total cost function equal to: STC (Q) = 3 + 2q + 2Q2. Suppose that there are 100 firms, and the market demand is D(P) = 100 - 5P where D(P) is the quantity consumed in the market when the market price is P. 1. What is the short-run equilibrium price? 2. How much does each firm produce? 3. Are they...

Short-run Equilibrium: Bumper sticker firms produce bumper stickers in a perfectly competitive market. Each identical firm has a short-run total cost function equal to: STC (Q) = 3 + 2q + 2Q2. Suppose that there are 100 firms, and the market demand is D(P) = 100 - 5P where D(P) is the quantity consumed in the market when the market price is P. 1. What is the short-run equilibrium price? 2. How much does each firm produce? 3. Are they...

i) The long run cost function for each firm in a perfectly competitive market is c(q) = 2^1.5+16q^0.5, LMC = 1.59^0.5+ 8q^-0.5, market demand curve is Q=1600-2p. Find price (p) of output and the level of output (q) produced by the firm in a long run equilibrium. Find the long run average cost curve for the firm. ii) what happens in the long run if the market demand curve shifts to Q=160-20p?/ -A competitive industry is in long run equilibrium....

i) The long run cost function for each firm in a perfectly competitive market is c(q) = 2^1.5+16q^0.5, LMC = 1.59^0.5+ 8q^-0.5, market demand curve is Q=1600-2p. Find price (p) of output and the level of output (q) produced by the firm in a long run equilibrium. Find the long run average cost curve for the firm. ii) what happens in the long run if the market demand curve shifts to Q=160-20p?/ -A competitive industry is in long run equilibrium....

Most questions answered within 3 hours.

-

An

Atwood's machine has one block of m1 = 0.370 kg and the other is of...

asked 1 minute ago -

Why is Kevlar a stronger fabric then dacron? Provide two reasons

involving structures.

asked 15 minutes ago -

Suppose you have a checkers board. (8 squares wide and 8

squares long) and you

have...

asked 35 minutes ago -

Given the following function: QD = 200 - 5.25P

7.1 Derive the Regular Demand Function

7.2...

asked 30 minutes ago -

The following results were obtained as

part of a multiple regression analysis involving 3 independent

variables:...

asked 1 hour ago -

The time to complete a standardized exam is approximately normal

with a mean of 70 minutes...

asked 3 hours ago -

Two thousand randomly selected adults were asked whether or not

they have ever shopped on the...

asked 3 hours ago -

Estimate the diffusion coefficient for methyl phenyl sulfide in

water at 25 degrees Celcius.

asked 2 hours ago -

10.g of a certain metal absorb 40. cal of heat and the temperature

is abserved to...

asked 3 hours ago -

How many milliliters of 0.0695 M Ca( OH)

2would be required to exactly neutralize 176 mL...

asked 4 hours ago -

A telephone survey uses a random digit dialing machine to call

subjects. The random digit dialing...

asked 4 hours ago -

How can having too little or too much of a certain

protein cause problems for an...

asked 6 hours ago