I need help with Part 6. Numbers 3 and 4

These are wrong and have a red mark next to them

Homework Answers

1) Budgeted Direct Labor Hours = Normal production*Direct labor hour per unit

= 100,000 units*2 hours = 200,000 hours

Standard Fixed Overhead rate = Budgeted Fixed Overhead/Budgeted Direct Labor Hours

= $770,000/200,000 hrs = $3.85 per hour

Standard Variable Overhead rate = Budgeted Variable Overhead/Budgeted Direct Labor Hours

= $444,000/200,000 hrs = $2.22 per hour

2) Applied Fixed Overhead = Std labor hours for actual production*Standard Fixed Overhead rate

= (97,000 units*2 hrs)*$3.85= $746,900

Applied Variable Overhead = Std labor hours for actual production*Standard Variable Overhead rate

= (97,000 units*2 hrs)*$2.22= $430,680

Total fixed overhead variance = Applied Fixed Overhead - Actual Fixed Overhead

= $746,900 - $780,000 = -$33,100 Unfavorable

Total variable overhead variance = Applied Variable Overhead - Actual Variable Overhead

= $430,680 - $435,600 = -$4,920 Unfavorable

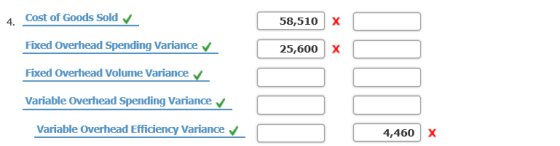

3) Fixed Overhead spending variance = Budgeted Fixed Overhead - Actual Fixed Overhead

= $770,000 - $780,000 = -$10,000 Unfavorable

Fixed overhead volume variance = Applied Fixed Overhead - Budgeted Fixed Overhead

= $746,900 - $770,000 = -$23,100 Unfavorable

4) Variable Overhead spending variance = (Actual labor hours*Std variable rate) - Actual Variable Overhead

= (196,000 hrs*$2.22) - $435,600 = -$480 Unfavorable

Variable overhead Efficiency variance = Applied Variable overhead - (Actual labor hours*Std variable rate)

= $430,680 - (196,000*2.22) = -$4,440 Unfavorable

5) Volume Variance = -$23,100 Unfavorable

Variable Overhead Efficiency Variance = -$4,440 Unfavorable

Spending Variance = -10,000-480 = -$10,480 Unfavorable

6) Journal Entries (Amounts in $)

| No | Account Titles | Debit | Credit |

| 1) | Work in Process (430,680+746,900) | 1,177,580 | |

| Variable Overhead Control (Applied) | 430,680 | ||

| Fixed Overhead Control (Applied) | 746,900 | ||

| 2) | Variable Overhead Control (Actual) | 435,600 | |

| Fixed Overhead Control (Actual) | 780,000 | ||

| Miscellaneous Accounts (435,600+780,000) | 1,215,600 | ||

| 3) | Fixed Overhead Spending Variance | 10,000 | |

| Fixed Overhead Volume Variance | 23,100 | ||

| Variable Overhead Spending Variance | 480 | ||

| Variable Overhead Efficiency Variance | 4,440 | ||

| Fixed Overhead Control (10,000+23,100) | 33,100 | ||

| Variable Overhead Control (480+4,440) | 4,920 | ||

| 4) | Cost of goods sold | 38,020 | |

| Fixed Overhead Spending Variance | 10,000 | ||

| Fixed Overhead Volume Variance | 23,100 | ||

| Variable Overhead Spending Variance | 480 | ||

| Variable Overhead Efficiency Variance | 4,440 |

Add Answer to:

I need help with Part 6. Numbers 3 and 4

These are wrong and have a...

need help with the journal Materials Direct Materials Price Variance Direct materials (5 lbs. @ $2.60)...

need help with the journal

Materials Direct Materials Price Variance Direct materials (5 lbs. @ $2.60) Accounts Payable $13.00 Work in Process Direct labor (0.75 hr. @ $18.00) 13.50 Direct Materials Usage Variance Materials Fixed overhead (0.75 hr. @ $4.00) 3.00 Variable overhead (0.75 hr. @ $3.00) 2.25 Work in Process Direct Labor Efficiency Variance Direct Labor Rate Variance Wages Payable Standard cost per unit $31.75 Work in Process Variable Overhead Control Fixed Overhead Control Algers computes its overhead rates...

need help with the journal

Materials Direct Materials Price Variance Direct materials (5 lbs. @ $2.60) Accounts Payable $13.00 Work in Process Direct labor (0.75 hr. @ $18.00) 13.50 Direct Materials Usage Variance Materials Fixed overhead (0.75 hr. @ $4.00) 3.00 Variable overhead (0.75 hr. @ $3.00) 2.25 Work in Process Direct Labor Efficiency Variance Direct Labor Rate Variance Wages Payable Standard cost per unit $31.75 Work in Process Variable Overhead Control Fixed Overhead Control Algers computes its overhead rates...

I have completed 1and 2, but I need help with number 3 (compute overhead controllable volume variances) Required...

I have completed 1and 2, but I need help with number 3

(compute overhead controllable volume variances)

Required information [The following information applies to the questions displayed below Trico Company set the following standard unit costs for its single product Direct materials (30 Ibs.$4.80 per Ib.) Direct labor (7 hrs. @ $14 per hr. Factory overhead-variable (7 hrs. $6 per hr.) Factory overhead-fixed (7 hrs.$9 per hr) Total standard cost $ 144.0 98.00 42.00 63.00 $ 347.00 The predetermined overhead...

I have completed 1and 2, but I need help with number 3

(compute overhead controllable volume variances)

Required information [The following information applies to the questions displayed below Trico Company set the following standard unit costs for its single product Direct materials (30 Ibs.$4.80 per Ib.) Direct labor (7 hrs. @ $14 per hr. Factory overhead-variable (7 hrs. $6 per hr.) Factory overhead-fixed (7 hrs.$9 per hr) Total standard cost $ 144.0 98.00 42.00 63.00 $ 347.00 The predetermined overhead...

Trico Company set the following standard unit costs for its single product. Direct materials (30 Ibs....

Trico Company set the following standard unit costs for its single product. Direct materials (30 Ibs. @ $5.10 per Ib.) Direct labor (8 hrs. @ $15 per hr.) Factory overhead-Variable (8 hrs. @ $6 per hr.) Factory overhead-Fixed (8 hrs. @ $9 per hr.) Total standard cost $ 153.00 120.00 48.00 72.00 $ 393.00 The predetermined overhead rate is based on a planned operating volume of 80% of the productive capacity of 65,000 units per quarter. The following flexible budget...

Trico Company set the following standard unit costs for its single product. Direct materials (30 Ibs. @ $5.10 per Ib.) Direct labor (8 hrs. @ $15 per hr.) Factory overhead-Variable (8 hrs. @ $6 per hr.) Factory overhead-Fixed (8 hrs. @ $9 per hr.) Total standard cost $ 153.00 120.00 48.00 72.00 $ 393.00 The predetermined overhead rate is based on a planned operating volume of 80% of the productive capacity of 65,000 units per quarter. The following flexible budget...

Overhead Variances, Four-Variance Analysis Oerstman, Inc., uses a standard costing system and develops its overhead rates...

Overhead Variances, Four-Variance Analysis Oerstman, Inc., uses a standard costing system and develops its overhead rates from the current annual budget. The budget is based on an expected annual output of 124,000 units requiring 496,000 direct labor hours. (Practical capacity is 516,000 hours.) Annual budgeted overhead costs total $828,320, of which $590,240 is fixed overhead. A total of 119,200 units using 494,000 direct labor hours were produced during the year. Actual variable overhead costs for the year were $261,300, and...

Can anybody help me with this? I have a little direction to go on, but I'm...

Can anybody help me with this? I have a

little direction to go on, but I'm not sure.

TIA

1 The following information has been provided for Abbott Company. 3 Standard Costs 4 Direct Materials 6 pounds per unit $ 5 Direct Manufacturing Labor 0.9595 hours per unit $ 6 Variable Manufacturing Overhead $ 7 8 Budgeted Fixed Manufacturing Overhe $1,000,000 $ 11.50 per pound 25.00 per hour 10.00 per direct labor hour 20.00 per direct labor hour 9 $...

Can anybody help me with this? I have a

little direction to go on, but I'm not sure.

TIA

1 The following information has been provided for Abbott Company. 3 Standard Costs 4 Direct Materials 6 pounds per unit $ 5 Direct Manufacturing Labor 0.9595 hours per unit $ 6 Variable Manufacturing Overhead $ 7 8 Budgeted Fixed Manufacturing Overhe $1,000,000 $ 11.50 per pound 25.00 per hour 10.00 per direct labor hour 20.00 per direct labor hour 9 $...

Overhead Variances, Four-Variance Analysis Oerstman, Inc., uses a standard costing system and develops its overhead rates...

Overhead Variances, Four-Variance Analysis Oerstman, Inc., uses a standard costing system and develops its overhead rates from the current annual budget. The budget is based on an expected annual output of 125,000 units requiring 500,000 direct labor hours. (Practical capacity is 520,000 hours.) Annual budgeted overhead costs total $840,000, of which $595,000 is fixed overhead. A total of 119,300 units using 498,000 direct labor hours were produced during the year. Actual variable overhead costs for the year were $262,000, and...

Overhead Application, Fixed and Variable Overhead Variances Zepol Company is planning to produce 600,000 power drills...

Overhead Application, Fixed and Variable Overhead Variances Zepol Company is planning to produce 600,000 power drills for the coming year. The company uses direct labor hours to assign overhead to products. Each drill requires 0.75 standard hour of labor for completion. The total budgeted overhead was $1,777,500. The total fixed overhead budgeted for the coming year is $832,500. Predetermined overhead rates are calculated using expected production, measured in direct labor hours. Actual results for the year are: Actual production (units)...

Overhead Application, Fixed and Variable Overhead Variances Zepol Company is planning to produce 600,000 power drills for the coming year. The company uses direct labor hours to assign overhead to products. Each drill requires 0.75 standard hour of labor for completion. The total budgeted overhead was $1,777,500. The total fixed overhead budgeted for the coming year is $832,500. Predetermined overhead rates are calculated using expected production, measured in direct labor hours. Actual results for the year are: Actual production (units)...

Overhead Application, Overhead Variances, Journal Entries Plimpton Company produces countertop ovens. Plimpton uses a standard costing...

Overhead Application, Overhead Variances, Journal Entries Plimpton Company produces countertop ovens. Plimpton uses a standard costing system. The standard costing system relies on direct labor hours to assign overhead costs to production. The direct labor standard indicates that two direct labor hours should be used for every oven produced. The normal production volume is 100,000 units. The budgeted overhead for the coming year is as follows: Fixed overhead $770,000 Variable overhead 446,000* *At normal volume. Plimpton applies overhead on the...

Static Plexible Volume Purchasing manager Favorable Unfavorable Debit Credit Fixed overhead budget Fixed overhead volune Spending...

Static Plexible Volume Purchasing manager Favorable Unfavorable Debit Credit Fixed overhead budget Fixed overhead volune Spending Production manager Variable overhead rate Variable overhead effieiency Fixed overhead spending Ixed overhead spending 1. A budget is based on a fixed estimate of sales volume. A volume 2. variance represents the difference between actual and expected levels of activity 3. The is typically responsible for the direct materials quantity variance The variable overhead rate variance is 4 when the actual variable overhead rate...

Static Plexible Volume Purchasing manager Favorable Unfavorable Debit Credit Fixed overhead budget Fixed overhead volune Spending Production manager Variable overhead rate Variable overhead effieiency Fixed overhead spending Ixed overhead spending 1. A budget is based on a fixed estimate of sales volume. A volume 2. variance represents the difference between actual and expected levels of activity 3. The is typically responsible for the direct materials quantity variance The variable overhead rate variance is 4 when the actual variable overhead rate...

Overhead Variances, Four-Variance Analysis Oerstman, Inc., uses a standard costing system and develops its overhead rates...

Overhead Variances, Four-Variance Analysis Oerstman, Inc., uses a standard costing system and develops its overhead rates from the current annual budget. The budget is based on an expected annual output of 126,000 units requiring 504,000 direct labor hours. (Practical capacity is 524,000 hours.) Annual budgeted overhead costs total $811,440, of which $584,640 is fixed overhead. A total of 119,000 units using 502,000 direct labor hours were produced during the year. Actual variable overhead costs for the year were $261,500, and...

need help with the journal

Materials Direct Materials Price Variance Direct materials (5 lbs. @ $2.60) Accounts Payable $13.00 Work in Process Direct labor (0.75 hr. @ $18.00) 13.50 Direct Materials Usage Variance Materials Fixed overhead (0.75 hr. @ $4.00) 3.00 Variable overhead (0.75 hr. @ $3.00) 2.25 Work in Process Direct Labor Efficiency Variance Direct Labor Rate Variance Wages Payable Standard cost per unit $31.75 Work in Process Variable Overhead Control Fixed Overhead Control Algers computes its overhead rates...

need help with the journal

Materials Direct Materials Price Variance Direct materials (5 lbs. @ $2.60) Accounts Payable $13.00 Work in Process Direct labor (0.75 hr. @ $18.00) 13.50 Direct Materials Usage Variance Materials Fixed overhead (0.75 hr. @ $4.00) 3.00 Variable overhead (0.75 hr. @ $3.00) 2.25 Work in Process Direct Labor Efficiency Variance Direct Labor Rate Variance Wages Payable Standard cost per unit $31.75 Work in Process Variable Overhead Control Fixed Overhead Control Algers computes its overhead rates...

I have completed 1and 2, but I need help with number 3

(compute overhead controllable volume variances)

Required information [The following information applies to the questions displayed below Trico Company set the following standard unit costs for its single product Direct materials (30 Ibs.$4.80 per Ib.) Direct labor (7 hrs. @ $14 per hr. Factory overhead-variable (7 hrs. $6 per hr.) Factory overhead-fixed (7 hrs.$9 per hr) Total standard cost $ 144.0 98.00 42.00 63.00 $ 347.00 The predetermined overhead...

I have completed 1and 2, but I need help with number 3

(compute overhead controllable volume variances)

Required information [The following information applies to the questions displayed below Trico Company set the following standard unit costs for its single product Direct materials (30 Ibs.$4.80 per Ib.) Direct labor (7 hrs. @ $14 per hr. Factory overhead-variable (7 hrs. $6 per hr.) Factory overhead-fixed (7 hrs.$9 per hr) Total standard cost $ 144.0 98.00 42.00 63.00 $ 347.00 The predetermined overhead...

Trico Company set the following standard unit costs for its single product. Direct materials (30 Ibs. @ $5.10 per Ib.) Direct labor (8 hrs. @ $15 per hr.) Factory overhead-Variable (8 hrs. @ $6 per hr.) Factory overhead-Fixed (8 hrs. @ $9 per hr.) Total standard cost $ 153.00 120.00 48.00 72.00 $ 393.00 The predetermined overhead rate is based on a planned operating volume of 80% of the productive capacity of 65,000 units per quarter. The following flexible budget...

Trico Company set the following standard unit costs for its single product. Direct materials (30 Ibs. @ $5.10 per Ib.) Direct labor (8 hrs. @ $15 per hr.) Factory overhead-Variable (8 hrs. @ $6 per hr.) Factory overhead-Fixed (8 hrs. @ $9 per hr.) Total standard cost $ 153.00 120.00 48.00 72.00 $ 393.00 The predetermined overhead rate is based on a planned operating volume of 80% of the productive capacity of 65,000 units per quarter. The following flexible budget...

Can anybody help me with this? I have a

little direction to go on, but I'm not sure.

TIA

1 The following information has been provided for Abbott Company. 3 Standard Costs 4 Direct Materials 6 pounds per unit $ 5 Direct Manufacturing Labor 0.9595 hours per unit $ 6 Variable Manufacturing Overhead $ 7 8 Budgeted Fixed Manufacturing Overhe $1,000,000 $ 11.50 per pound 25.00 per hour 10.00 per direct labor hour 20.00 per direct labor hour 9 $...

Can anybody help me with this? I have a

little direction to go on, but I'm not sure.

TIA

1 The following information has been provided for Abbott Company. 3 Standard Costs 4 Direct Materials 6 pounds per unit $ 5 Direct Manufacturing Labor 0.9595 hours per unit $ 6 Variable Manufacturing Overhead $ 7 8 Budgeted Fixed Manufacturing Overhe $1,000,000 $ 11.50 per pound 25.00 per hour 10.00 per direct labor hour 20.00 per direct labor hour 9 $...

Overhead Application, Fixed and Variable Overhead Variances Zepol Company is planning to produce 600,000 power drills for the coming year. The company uses direct labor hours to assign overhead to products. Each drill requires 0.75 standard hour of labor for completion. The total budgeted overhead was $1,777,500. The total fixed overhead budgeted for the coming year is $832,500. Predetermined overhead rates are calculated using expected production, measured in direct labor hours. Actual results for the year are: Actual production (units)...

Overhead Application, Fixed and Variable Overhead Variances Zepol Company is planning to produce 600,000 power drills for the coming year. The company uses direct labor hours to assign overhead to products. Each drill requires 0.75 standard hour of labor for completion. The total budgeted overhead was $1,777,500. The total fixed overhead budgeted for the coming year is $832,500. Predetermined overhead rates are calculated using expected production, measured in direct labor hours. Actual results for the year are: Actual production (units)...

Static Plexible Volume Purchasing manager Favorable Unfavorable Debit Credit Fixed overhead budget Fixed overhead volune Spending Production manager Variable overhead rate Variable overhead effieiency Fixed overhead spending Ixed overhead spending 1. A budget is based on a fixed estimate of sales volume. A volume 2. variance represents the difference between actual and expected levels of activity 3. The is typically responsible for the direct materials quantity variance The variable overhead rate variance is 4 when the actual variable overhead rate...

Static Plexible Volume Purchasing manager Favorable Unfavorable Debit Credit Fixed overhead budget Fixed overhead volune Spending Production manager Variable overhead rate Variable overhead effieiency Fixed overhead spending Ixed overhead spending 1. A budget is based on a fixed estimate of sales volume. A volume 2. variance represents the difference between actual and expected levels of activity 3. The is typically responsible for the direct materials quantity variance The variable overhead rate variance is 4 when the actual variable overhead rate...

Most questions answered within 3 hours.

-

At the start of a CD it is spinning at a rate of 525 rpm

(revolutions...

asked 33 minutes ago -

4. Without doing any calculations, predict whether the observed

∆T would increase, decrease or remain the...

asked 1 hour ago -

Based on the range, which of the following sets of scores has

the greatest variability? 3,...

asked 2 hours ago -

Ripples in a pond travel at a velocity of 3 m/s with one peak

passing a...

asked 2 hours ago -

A man stands on the roof of a building of height 13.0 mm and

throws a...

asked 2 hours ago -

The extent to which assets are financed by borrowed funds and

other liabilities is indicated by:...

asked 3 hours ago -

Explain in detail

Germany is the fifth largest economy

explain what goods and services Germany specializes...

asked 4 hours ago -

The density of platinum is 21.45 g/mL. If a cube of platinum

with a mass of...

asked 4 hours ago -

Accounts Receivable

Sales

A/R Posting

Extended Sales Invoice

Packing Slip

Compare invoice to packing slip 2...

asked 4 hours ago -

Michaella, age 23, is a full-time law student and is claimed by

her parents as a...

asked 4 hours ago -

Why are polymers not typically casted into products?

asked 4 hours ago -

When rolling a die 129 times, what is the probability of rolling

a 6 no more...

asked 4 hours ago