1.Equipment that cost $674000 and has accumulated depreciation of $292000 is exchanged for equipment with a...

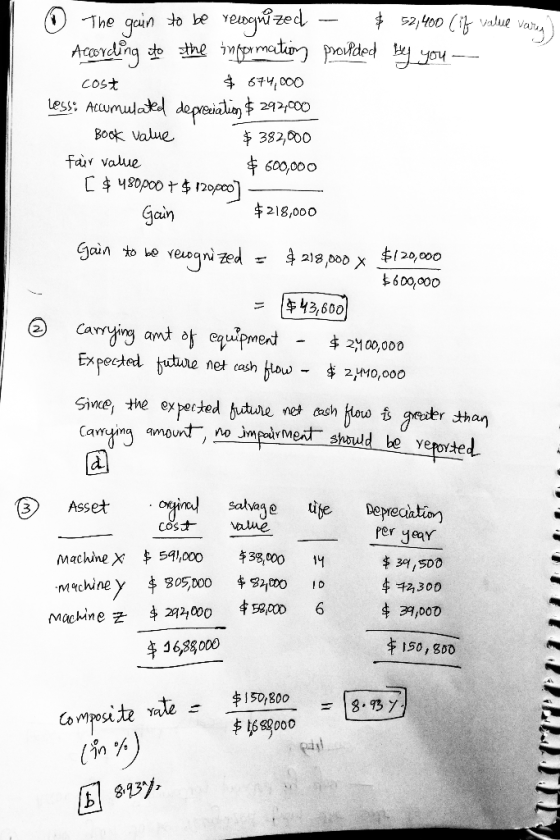

1.Equipment that cost $674000 and has accumulated depreciation of $292000 is exchanged for equipment with a fair value of $480000 and $120000 cash is received. The exchange lacked commercial substance. The gain to be recognized from the exchange is

a.$188000

b.$52400

c.$90000

d.$278000

2. Crane Company has equipment with a carrying amount of $2400000. The expected future net cash flows from the equipment are $2440000, and its fair value is $2035000. The equipment is expected to be used in operations in the future. What amount (if any) should Crane report as an impairment to its equipment?

|

a |

$365000. |

|

b |

$40000. |

|

c |

$405000. |

|

d |

No impairment should be reported |

3. A schedule of machinery owned by Concord Corporation is

presented below:

|

Estimated |

Estimated |

||||

|

Total Cost |

Salvage Value |

Life in Years |

|||

| Machine X |

$591000 |

$38000 |

14 |

||

| Machine Y |

805000 |

82000 |

10 |

||

| Machine Z |

292000 |

58000 |

6 |

Concord computes depreciation by the composite method.

The composite rate of depreciation (in percent) for these assets

is

|

a |

8.36. |

|

b |

8.93. |

|

c |

13.79. |

|

d |

10.36. |

Homework Answers

Add Answer to:

1.Equipment that cost $674000 and has accumulated depreciation

of $292000 is exchanged for equipment with a...

9. Equipment that cost $660,000 and has accumulated depreciation of $300.000 is exchanged for equipment with...

9. Equipment that cost $660,000 and has accumulated depreciation of $300.000 is exchanged for equipment with a fair value of $480,000 and $120,000 cash is received The exchange lacked commercial substance. The gain to be recognized from the exchange is A) $48,000 B) $60,000 C) $180,000 D) $240,000

9. Equipment that cost $660,000 and has accumulated depreciation of $300.000 is exchanged for equipment with a fair value of $480,000 and $120,000 cash is received The exchange lacked commercial substance. The gain to be recognized from the exchange is A) $48,000 B) $60,000 C) $180,000 D) $240,000

Equipment that cost $390,300 and has accumulated depreciation of $313,600 is exchanged for equipment with a...

Equipment that cost $390,300 and has accumulated depreciation of $313,600 is exchanged for equipment with a fair value of $160,000 and $40,000 cash is received. The exchange lacked commercial substance. Calculate the gain to be recognized from the exchange. Gain recognized SHOW LIST OF ACCOUNTS the entry for the exchange. Show a check of the amount recorded for the new equipment. (Credit account titles are automatically indented when the amount is entered. Do not indent manually.) Account Titles and Explanation...

Equipment that cost $390,300 and has accumulated depreciation of $313,600 is exchanged for equipment with a fair value of $160,000 and $40,000 cash is received. The exchange lacked commercial substance. Calculate the gain to be recognized from the exchange. Gain recognized SHOW LIST OF ACCOUNTS the entry for the exchange. Show a check of the amount recorded for the new equipment. (Credit account titles are automatically indented when the amount is entered. Do not indent manually.) Account Titles and Explanation...

Equipment that cost $390,300 and has accumulated depreciation of $313,600 is exchanged for equipment with a...

Equipment that cost $390,300 and has accumulated depreciation of $313,600 is exchanged for equipment with a fair value of $160,000 and $40,000 cash is received. The exchange lacked commercial substance. Calculate the gain to be recognized from the exchange. Gain recognized SHOW LIST OF ACCOUNTS Prepare the entry for the exchange. Show a check of the amount recorded for the new equipment. (Credit account titles are automatically indented when the amount is entered. Do not indent manually.) Account Titles and...

Equipment that cost $390,300 and has accumulated depreciation of $313,600 is exchanged for equipment with a fair value of $160,000 and $40,000 cash is received. The exchange lacked commercial substance. Calculate the gain to be recognized from the exchange. Gain recognized SHOW LIST OF ACCOUNTS Prepare the entry for the exchange. Show a check of the amount recorded for the new equipment. (Credit account titles are automatically indented when the amount is entered. Do not indent manually.) Account Titles and...

Current Attempt in Progress Equipment that cost $778800 and has accumulated depreciation of $354000 is exchanged...

Current Attempt in Progress Equipment that cost $778800 and has accumulated depreciation of $354000 is exchanged for equipment with a fair value of $566400 and $141600 cash is received. The exchange lacked commercial substance, The new equipment should be recorded at $339840 $283200 $566400 $354000

Current Attempt in Progress Equipment that cost $778800 and has accumulated depreciation of $354000 is exchanged for equipment with a fair value of $566400 and $141600 cash is received. The exchange lacked commercial substance, The new equipment should be recorded at $339840 $283200 $566400 $354000

Ex. 10-135—Nonmonetary exchange. Equipment that cost $240,000 and has accumulated depreciation of $189,000 is exchanged for...

Ex. 10-135—Nonmonetary exchange. Equipment that cost $240,000 and has accumulated depreciation of $189,000 is exchanged for equipment with a fair value of $96,000 and $24,000 cash is received. The exchange lacked commercial substance. Instructions (a) Show the calculation of the gain to be recognized from the exchange. (b) Prepare the entry for the exchange. Show a check of the amount recorded for the new equipment.

Ex. 10-135—Nonmonetary exchange. Equipment that cost $240,000 and has accumulated depreciation of $189,000 is exchanged for equipment with a fair value of $96,000 and $24,000 cash is received. The exchange lacked commercial substance. Instructions (a) Show the calculation of the gain to be recognized from the exchange. (b) Prepare the entry for the exchange. Show a check of the amount recorded for the new equipment.

A machine cost $228,600, has annual depreciation expense of $45,720, and has accumulated depreciation of $114,300...

A machine cost $228,600, has annual depreciation expense of $45,720, and has accumulated depreciation of $114,300 on December 31, 2020. On April 1, 2021, when the machine has a fair value of $89,470, it is exchanged for a similar machine with a fair value of $280,700 and the proper amount of cash is paid. The exchange lacked commercial substance. Prepare all entries that are necessary at April 1, 2021. (Credit account titles are automatically indented when the amount is entered....

A machine cost $228,600, has annual depreciation expense of $45,720, and has accumulated depreciation of $114,300 on December 31, 2020. On April 1, 2021, when the machine has a fair value of $89,470, it is exchanged for a similar machine with a fair value of $280,700 and the proper amount of cash is paid. The exchange lacked commercial substance. Prepare all entries that are necessary at April 1, 2021. (Credit account titles are automatically indented when the amount is entered....

Current Attempt in Progress Equipment that cost $554400 and has accumulated depreciation of 5252000 is exchanged...

Current Attempt in Progress Equipment that cost $554400 and has accumulated depreciation of 5252000 is exchanged for equipment with a fair value of $403200 and $100300 cash is received. The exchange backed commercial substand The new equipment should be recorded at $241920 $403200 $252000 $201600

Current Attempt in Progress Equipment that cost $554400 and has accumulated depreciation of 5252000 is exchanged for equipment with a fair value of $403200 and $100300 cash is received. The exchange backed commercial substand The new equipment should be recorded at $241920 $403200 $252000 $201600

A machine cost $255,200, has annual depreciation expense of $51,040, and has accumulated depreciation of $127,600...

A machine cost $255,200, has annual depreciation expense of $51,040, and has accumulated depreciation of $127,600 on December 31, 2020. On April 1, 2021, when the machine has a fair value of $102,490, it is exchanged for a similar machine with a fair value of $286,500 and the proper amount of cash is paid. The exchange lacked commercial substance. Prepare all entries that are necessary at April 1, 2021. (Credit account titles are automatically indented when the amount is entered....

A machine cost $255,200, has annual depreciation expense of $51,040, and has accumulated depreciation of $127,600 on December 31, 2020. On April 1, 2021, when the machine has a fair value of $102,490, it is exchanged for a similar machine with a fair value of $286,500 and the proper amount of cash is paid. The exchange lacked commercial substance. Prepare all entries that are necessary at April 1, 2021. (Credit account titles are automatically indented when the amount is entered....

Ex. 10-134-Nonmonetary exchange cost $140,000, has annual depreciation A machine expense of $28,000, and has accumulated...

Ex. 10-134-Nonmonetary exchange cost $140,000, has annual depreciation A machine expense of $28,000, and has accumulated depreciation of $70,000 on December 31, 2012. On April 1, 2013, when the machine has a fair value of $56,000, it is exchanged for a similar machine with a fair value of $168,0000 and the proper amount of cash is paid. The exchange lacked commercial substance. Instructions Prepare all entries that are necessary at April 1, 2013

Ex. 10-134-Nonmonetary exchange cost $140,000, has annual depreciation A machine expense of $28,000, and has accumulated depreciation of $70,000 on December 31, 2012. On April 1, 2013, when the machine has a fair value of $56,000, it is exchanged for a similar machine with a fair value of $168,0000 and the proper amount of cash is paid. The exchange lacked commercial substance. Instructions Prepare all entries that are necessary at April 1, 2013

Ex. 10-134-Nonmonetary exchange. A machine cost $140,000, has annual depreciation expense of $28,000, and has accumulated...

Ex. 10-134-Nonmonetary exchange. A machine cost $140,000, has annual depreciation expense of $28,000, and has accumulated depreciation of $70,000 on December 31, 2012. On April 1, 2013, when the machine has a fair value of $56,000, it is exchanged for a similar machine with a fair value of $168,000 and the proper amount of cash is paid. The exchange lacked commercial substance. Instructions Prepare all entries that are necessary at April 1, 2013.

Ex. 10-134-Nonmonetary exchange. A machine cost $140,000, has annual depreciation expense of $28,000, and has accumulated depreciation of $70,000 on December 31, 2012. On April 1, 2013, when the machine has a fair value of $56,000, it is exchanged for a similar machine with a fair value of $168,000 and the proper amount of cash is paid. The exchange lacked commercial substance. Instructions Prepare all entries that are necessary at April 1, 2013.

9. Equipment that cost $660,000 and has accumulated depreciation of $300.000 is exchanged for equipment with a fair value of $480,000 and $120,000 cash is received The exchange lacked commercial substance. The gain to be recognized from the exchange is A) $48,000 B) $60,000 C) $180,000 D) $240,000

9. Equipment that cost $660,000 and has accumulated depreciation of $300.000 is exchanged for equipment with a fair value of $480,000 and $120,000 cash is received The exchange lacked commercial substance. The gain to be recognized from the exchange is A) $48,000 B) $60,000 C) $180,000 D) $240,000

Equipment that cost $390,300 and has accumulated depreciation of $313,600 is exchanged for equipment with a fair value of $160,000 and $40,000 cash is received. The exchange lacked commercial substance. Calculate the gain to be recognized from the exchange. Gain recognized SHOW LIST OF ACCOUNTS the entry for the exchange. Show a check of the amount recorded for the new equipment. (Credit account titles are automatically indented when the amount is entered. Do not indent manually.) Account Titles and Explanation...

Equipment that cost $390,300 and has accumulated depreciation of $313,600 is exchanged for equipment with a fair value of $160,000 and $40,000 cash is received. The exchange lacked commercial substance. Calculate the gain to be recognized from the exchange. Gain recognized SHOW LIST OF ACCOUNTS the entry for the exchange. Show a check of the amount recorded for the new equipment. (Credit account titles are automatically indented when the amount is entered. Do not indent manually.) Account Titles and Explanation...

Equipment that cost $390,300 and has accumulated depreciation of $313,600 is exchanged for equipment with a fair value of $160,000 and $40,000 cash is received. The exchange lacked commercial substance. Calculate the gain to be recognized from the exchange. Gain recognized SHOW LIST OF ACCOUNTS Prepare the entry for the exchange. Show a check of the amount recorded for the new equipment. (Credit account titles are automatically indented when the amount is entered. Do not indent manually.) Account Titles and...

Equipment that cost $390,300 and has accumulated depreciation of $313,600 is exchanged for equipment with a fair value of $160,000 and $40,000 cash is received. The exchange lacked commercial substance. Calculate the gain to be recognized from the exchange. Gain recognized SHOW LIST OF ACCOUNTS Prepare the entry for the exchange. Show a check of the amount recorded for the new equipment. (Credit account titles are automatically indented when the amount is entered. Do not indent manually.) Account Titles and...

Current Attempt in Progress Equipment that cost $778800 and has accumulated depreciation of $354000 is exchanged for equipment with a fair value of $566400 and $141600 cash is received. The exchange lacked commercial substance, The new equipment should be recorded at $339840 $283200 $566400 $354000

Current Attempt in Progress Equipment that cost $778800 and has accumulated depreciation of $354000 is exchanged for equipment with a fair value of $566400 and $141600 cash is received. The exchange lacked commercial substance, The new equipment should be recorded at $339840 $283200 $566400 $354000

Ex. 10-135—Nonmonetary exchange. Equipment that cost $240,000 and has accumulated depreciation of $189,000 is exchanged for equipment with a fair value of $96,000 and $24,000 cash is received. The exchange lacked commercial substance. Instructions (a) Show the calculation of the gain to be recognized from the exchange. (b) Prepare the entry for the exchange. Show a check of the amount recorded for the new equipment.

Ex. 10-135—Nonmonetary exchange. Equipment that cost $240,000 and has accumulated depreciation of $189,000 is exchanged for equipment with a fair value of $96,000 and $24,000 cash is received. The exchange lacked commercial substance. Instructions (a) Show the calculation of the gain to be recognized from the exchange. (b) Prepare the entry for the exchange. Show a check of the amount recorded for the new equipment.

A machine cost $228,600, has annual depreciation expense of $45,720, and has accumulated depreciation of $114,300 on December 31, 2020. On April 1, 2021, when the machine has a fair value of $89,470, it is exchanged for a similar machine with a fair value of $280,700 and the proper amount of cash is paid. The exchange lacked commercial substance. Prepare all entries that are necessary at April 1, 2021. (Credit account titles are automatically indented when the amount is entered....

A machine cost $228,600, has annual depreciation expense of $45,720, and has accumulated depreciation of $114,300 on December 31, 2020. On April 1, 2021, when the machine has a fair value of $89,470, it is exchanged for a similar machine with a fair value of $280,700 and the proper amount of cash is paid. The exchange lacked commercial substance. Prepare all entries that are necessary at April 1, 2021. (Credit account titles are automatically indented when the amount is entered....

Current Attempt in Progress Equipment that cost $554400 and has accumulated depreciation of 5252000 is exchanged for equipment with a fair value of $403200 and $100300 cash is received. The exchange backed commercial substand The new equipment should be recorded at $241920 $403200 $252000 $201600

Current Attempt in Progress Equipment that cost $554400 and has accumulated depreciation of 5252000 is exchanged for equipment with a fair value of $403200 and $100300 cash is received. The exchange backed commercial substand The new equipment should be recorded at $241920 $403200 $252000 $201600

A machine cost $255,200, has annual depreciation expense of $51,040, and has accumulated depreciation of $127,600 on December 31, 2020. On April 1, 2021, when the machine has a fair value of $102,490, it is exchanged for a similar machine with a fair value of $286,500 and the proper amount of cash is paid. The exchange lacked commercial substance. Prepare all entries that are necessary at April 1, 2021. (Credit account titles are automatically indented when the amount is entered....

A machine cost $255,200, has annual depreciation expense of $51,040, and has accumulated depreciation of $127,600 on December 31, 2020. On April 1, 2021, when the machine has a fair value of $102,490, it is exchanged for a similar machine with a fair value of $286,500 and the proper amount of cash is paid. The exchange lacked commercial substance. Prepare all entries that are necessary at April 1, 2021. (Credit account titles are automatically indented when the amount is entered....

Ex. 10-134-Nonmonetary exchange cost $140,000, has annual depreciation A machine expense of $28,000, and has accumulated depreciation of $70,000 on December 31, 2012. On April 1, 2013, when the machine has a fair value of $56,000, it is exchanged for a similar machine with a fair value of $168,0000 and the proper amount of cash is paid. The exchange lacked commercial substance. Instructions Prepare all entries that are necessary at April 1, 2013

Ex. 10-134-Nonmonetary exchange cost $140,000, has annual depreciation A machine expense of $28,000, and has accumulated depreciation of $70,000 on December 31, 2012. On April 1, 2013, when the machine has a fair value of $56,000, it is exchanged for a similar machine with a fair value of $168,0000 and the proper amount of cash is paid. The exchange lacked commercial substance. Instructions Prepare all entries that are necessary at April 1, 2013

Ex. 10-134-Nonmonetary exchange. A machine cost $140,000, has annual depreciation expense of $28,000, and has accumulated depreciation of $70,000 on December 31, 2012. On April 1, 2013, when the machine has a fair value of $56,000, it is exchanged for a similar machine with a fair value of $168,000 and the proper amount of cash is paid. The exchange lacked commercial substance. Instructions Prepare all entries that are necessary at April 1, 2013.

Ex. 10-134-Nonmonetary exchange. A machine cost $140,000, has annual depreciation expense of $28,000, and has accumulated depreciation of $70,000 on December 31, 2012. On April 1, 2013, when the machine has a fair value of $56,000, it is exchanged for a similar machine with a fair value of $168,000 and the proper amount of cash is paid. The exchange lacked commercial substance. Instructions Prepare all entries that are necessary at April 1, 2013.

Most questions answered within 3 hours.

-

Rice Products in Bangladesh

Business behavior is derived in large part from the basic cultural

environment...

asked 1 hour ago -

The following base sequence is found for a mRNA fragment from

wild-type E. coli: 5'- UAUCAGUAGAUAAUGUAACC-3'...

asked 1 hour ago -

For this exercise, round all regression parameters to three

decimal places.

One of the two tables...

asked 1 hour ago -

What is the 5% level of significance for mean = 3.60, standard

deviation = 0.94, and...

asked 1 hour ago -

Prior to beginning work on this discussion, please read the

article by Hayley Peterson, 15 Companies...

asked 2 hours ago -

Which pair of aqueous solutions, when mixed, will form a

precipitate?

A) NaNO3 and AgC2H3O2

B)...

asked 2 hours ago -

1-Write an algorithm to get two numbers from the user (as

inputs) and calculate the sum...

asked 5 hours ago -

Define white-collar crime. What is the difference between

offender and offense-based definitions of white-collar crime? What...

asked 6 hours ago -

Consider a reaction which is 1st order with respect to A and 1st

order with respect...

asked 6 hours ago -

c++

The length of the hypotenuse of a right-angled triangle is the

square root of the...

asked 6 hours ago -

When a metal rod is heated, not only its resistance but also its

length and cross‐sectional...

asked 7 hours ago -

write a c++ program that computes the L^1 - Norm of a given

vector (L^1 norm...

asked 7 hours ago