Homework Answers

Refer the below images for the above mentioned question , in a

detailed way of solution.

Add Answer to:

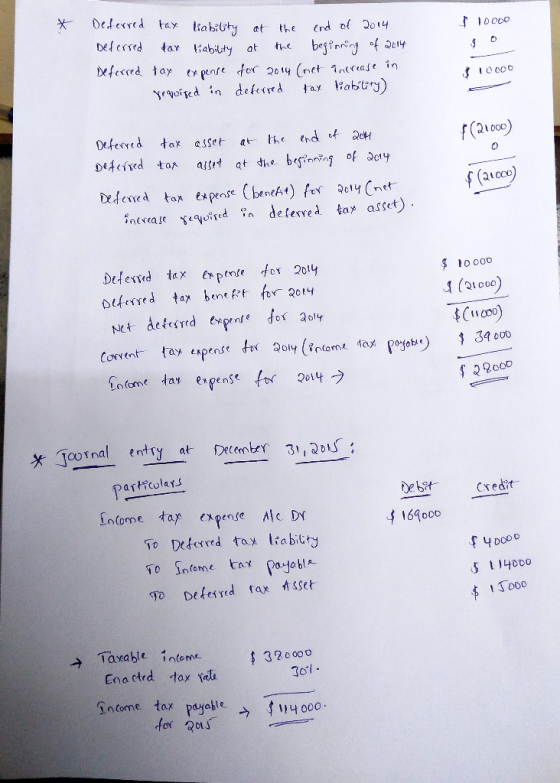

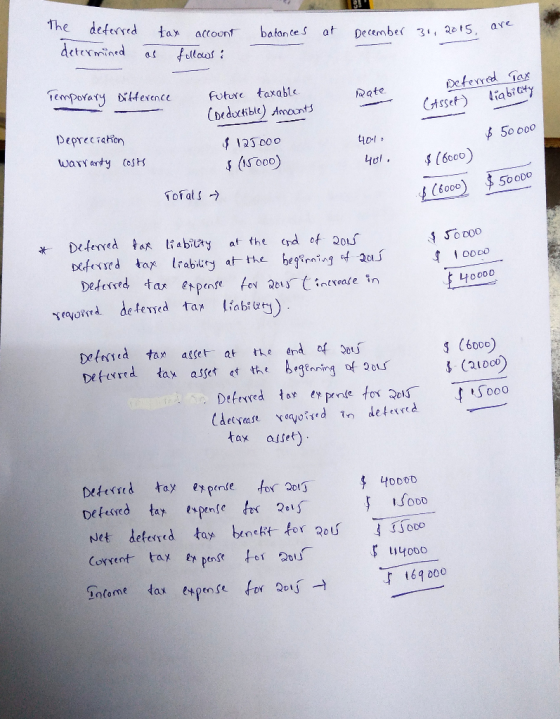

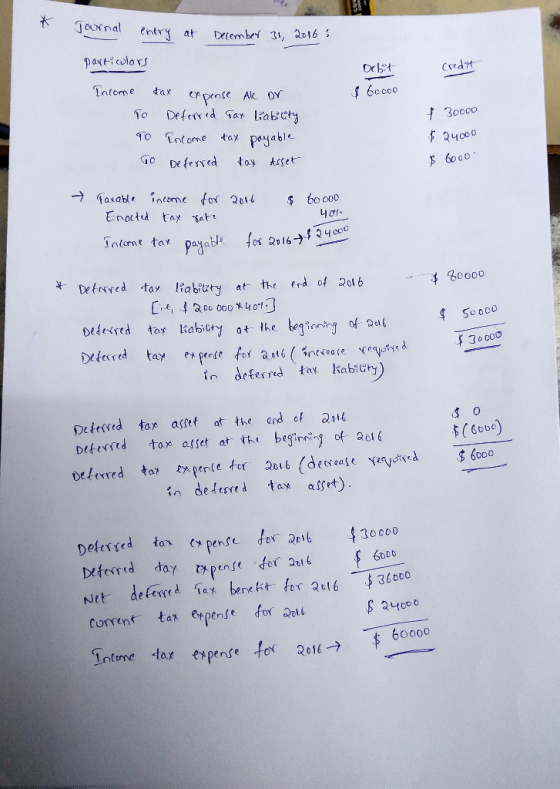

E19-17B (Two Temporary Differences, Tracked through 3 Years, Multiple Rates) Taxable income and pretax financial income...

Taxable income and pretax financial income would be identical for Bonita Co. except for its treatments...

Taxable income and pretax financial income would be identical for Bonita Co. except for its treatments of gross profit on installment sales and estimated costs of warranties The following income computations have been prepared Taxable income 2016 2017 2018 Excess of revenues over expenses (excluding two temporary differences) Installment gross profit collected $154,000 $191,000 $88,100 8,500 8,500 8.500 Expenditures for warranties (4,500) $158,000 (4,500) $195,000 (4,500) $92,100 Taxable income Pretax financial income 2016 2017 2018 Excess of revenues over expenses...

Taxable income and pretax financial income would be identical for Bonita Co. except for its treatments of gross profit on installment sales and estimated costs of warranties The following income computations have been prepared Taxable income 2016 2017 2018 Excess of revenues over expenses (excluding two temporary differences) Installment gross profit collected $154,000 $191,000 $88,100 8,500 8,500 8.500 Expenditures for warranties (4,500) $158,000 (4,500) $195,000 (4,500) $92,100 Taxable income Pretax financial income 2016 2017 2018 Excess of revenues over expenses...

Taxable income and pretax financial income would be identical for Crane Co. except for its treatments...

Taxable income and pretax financial income would be identical

for Crane Co. except for its treatments of gross profit on

installment sales and estimated costs of warranties. The following

income computations have been prepared.

Taxable income

2016

2017

2018

Excess of revenues over

expenses (excluding two temporary differences)

$154,000

$215,000

$93,500

Installment gross profit

collected

8,500

8,500

8,500

Expenditures for

warranties

(5,500

)

(5,500

)

(5,500

)

Taxable

income

$157,000

$218,000

$96,500

Pretax financial income

2016

2017

2018

Excess of...

Taxable income and pretax financial income would be identical

for Crane Co. except for its treatments of gross profit on

installment sales and estimated costs of warranties. The following

income computations have been prepared.

Taxable income

2016

2017

2018

Excess of revenues over

expenses (excluding two temporary differences)

$154,000

$215,000

$93,500

Installment gross profit

collected

8,500

8,500

8,500

Expenditures for

warranties

(5,500

)

(5,500

)

(5,500

)

Taxable

income

$157,000

$218,000

$96,500

Pretax financial income

2016

2017

2018

Excess of...

Taxable income and pretax financial income would be identical for Bramble Co. except for its treatments of gross p...

Taxable income and pretax financial income would be identical for Bramble Co. except for its treatments of gross profit on installment sales and estimated costs of warranties. The following income computations have been prepared. 2016 2017 2018 Taxable income Excess of revenues over expenses (excluding two temporary differences) Installment gross profit collected Expenditures for warranties Taxable income $83,200 7,300 $149,000 7,300 (5,000) $151,300 $218,000 7,300 (5,000) $220,300 (5,000) $85,500 2016 2017 2018 $149,000 $83,200 Pretax financial income Excess of revenues...

Taxable income and pretax financial income would be identical for Bramble Co. except for its treatments of gross profit on installment sales and estimated costs of warranties. The following income computations have been prepared. 2016 2017 2018 Taxable income Excess of revenues over expenses (excluding two temporary differences) Installment gross profit collected Expenditures for warranties Taxable income $83,200 7,300 $149,000 7,300 (5,000) $151,300 $218,000 7,300 (5,000) $220,300 (5,000) $85,500 2016 2017 2018 $149,000 $83,200 Pretax financial income Excess of revenues...

E19-1. (One Temporary Difference, Future Taxable Amounts, One Rate, No Beginning Deferred Taxes) 2 5 South...

E19-1.

(One Temporary Difference, Future Taxable Amounts, One Rate, No

Beginning Deferred Taxes)

2

5

South Carolina Corporation has one temporary difference at the end

of 2014 that will reverse and cause taxable amounts of $55,000 in

2015, $60,000 in 2016, and $65,000 in 2017. South Carolina's pretax

financial income for 2014 is $300,000, and the tax rate is 30% for

all years. There are no deferred taxes at the beginning of 2014.

Instructions

(a)

Compute taxable income and income...

E19-1.

(One Temporary Difference, Future Taxable Amounts, One Rate, No

Beginning Deferred Taxes)

2

5

South Carolina Corporation has one temporary difference at the end

of 2014 that will reverse and cause taxable amounts of $55,000 in

2015, $60,000 in 2016, and $65,000 in 2017. South Carolina's pretax

financial income for 2014 is $300,000, and the tax rate is 30% for

all years. There are no deferred taxes at the beginning of 2014.

Instructions

(a)

Compute taxable income and income...

Question 15 Taxable income and preta financial income would be computations have been prepared til for Grouper Co....

Question 15 Taxable income and preta financial income would be computations have been prepared til for Grouper Co. except for its treatments of gross profit on installment Sales and estimated costs of warranties. The following income 2016 2017 2018 Taxable income Excess of revenues over expenses (excluding two temporary Terences) Installment gross profit collected Expenditures for warranties Taxable income 5166,000 7,500 (4,800) $168,700 200.000 7.500 92.900 7.500 (4,800 ) $205,700 (4.800) 995,600 2016 2017 2018 Pretax financial income Excess of...

Question 15 Taxable income and preta financial income would be computations have been prepared til for Grouper Co. except for its treatments of gross profit on installment Sales and estimated costs of warranties. The following income 2016 2017 2018 Taxable income Excess of revenues over expenses (excluding two temporary Terences) Installment gross profit collected Expenditures for warranties Taxable income 5166,000 7,500 (4,800) $168,700 200.000 7.500 92.900 7.500 (4,800 ) $205,700 (4.800) 995,600 2016 2017 2018 Pretax financial income Excess of...

E19-4 (L01,2) (Three Differences, Compute Taxable income, Entry for Taxes) Zurich Company reports pretax financial income...

E19-4 (L01,2) (Three Differences, Compute Taxable income, Entry for Taxes) Zurich Company reports pretax financial income of $70,000 for 2017. The following items cause taxable income to be different than pretax financial income. 1. Depreciation on the tax return is greater than depreciation on the income statement by $16,000. 2. Rent collected on the tax return is greater than rent recognized on the income stalement by $22,000. 3. Fines for pollution appear as an expense of $11,000 on the income...

E19-4 (L01,2) (Three Differences, Compute Taxable income, Entry for Taxes) Zurich Company reports pretax financial income of $70,000 for 2017. The following items cause taxable income to be different than pretax financial income. 1. Depreciation on the tax return is greater than depreciation on the income statement by $16,000. 2. Rent collected on the tax return is greater than rent recognized on the income stalement by $22,000. 3. Fines for pollution appear as an expense of $11,000 on the income...

E19-4 (L01,2) (Three Differences, Compute Taxable income, Entry for Taxes) Zurich Company reports pretax financial income...

E19-4 (L01,2) (Three Differences, Compute Taxable income, Entry for Taxes) Zurich Company reports pretax financial income of $70,000 for 2017. The following items cause taxable income to be different than pretax financial income. 1. Depreciation on the tax return is greater than depreciation on the income statement by $16,000. 2. Rent collected on the tax return is greater than rent recognized on the income stalement by $22,000. 3. Fines for pollution appear as an expense of $11,000 on the income...

E19-4 (L01,2) (Three Differences, Compute Taxable income, Entry for Taxes) Zurich Company reports pretax financial income of $70,000 for 2017. The following items cause taxable income to be different than pretax financial income. 1. Depreciation on the tax return is greater than depreciation on the income statement by $16,000. 2. Rent collected on the tax return is greater than rent recognized on the income stalement by $22,000. 3. Fines for pollution appear as an expense of $11,000 on the income...

E19-4 (LO1,2) (Three Differences, Compute Taxable Income, Entry for Taxes) Zurich Company reports pretax financial...

E19-4 (LO1,2) (Three Differences, Compute Taxable Income, Entry for Taxes) Zurich Company reports pretax financial income of $70,000 for 2017. The following items cause taxable income to be different than pretax financial income. 1. Depreciation on the tax return is greater than depreciation on the income statement by $16,000. 2. Rent collected on the tax return is greater than rent recognized on the income sta.sment by $22,000. 3. Fines for pollution appear as an expense of $11,000 on the income...

E19-4 (LO1,2) (Three Differences, Compute Taxable Income, Entry for Taxes) Zurich Company reports pretax financial income of $70,000 for 2017. The following items cause taxable income to be different than pretax financial income. 1. Depreciation on the tax return is greater than depreciation on the income statement by $16,000. 2. Rent collected on the tax return is greater than rent recognized on the income sta.sment by $22,000. 3. Fines for pollution appear as an expense of $11,000 on the income...

Dart, Inc. began business on January 1, 2014. Its pretax financial income for the first 2...

Dart, Inc. began business on January 1, 2014. Its pretax financial income for the first 2 years was as follows: 2014 $240,000 2015 $560,000 The following items caused the only differences between pretax financial income and taxable income. In 2014, the company collected $240,000 of rent; of this amount, $80,000 was earned in 2014; the other $160,000 will be earned equally over the next two years. The full $240,000 was included in taxable income in 2014. Depreciation of property,...

Information for Kent Corp. for the year 2016: Reconciliation of pretax accounting income and taxable income:...

Information for Kent Corp. for the year 2016: Reconciliation of pretax accounting income and taxable income: Pretax accounting income $180,900 Permanent differences (15,500) 165,400 Temporary difference-depreciation (12,900) Taxable income $152,500 Cumulative future taxable amounts all from depreciation temporary differences: As of December 31, 2015 $13,400 As of December 31, 2016 $26,300 The enacted tax rate was 30% for 2015 and thereafter. What should be the balance in Kent's deferred tax liability account as of December 31, 2016? $5,360. $7,890. $26,300....

Taxable income and pretax financial income would be identical for Bonita Co. except for its treatments of gross profit on installment sales and estimated costs of warranties The following income computations have been prepared Taxable income 2016 2017 2018 Excess of revenues over expenses (excluding two temporary differences) Installment gross profit collected $154,000 $191,000 $88,100 8,500 8,500 8.500 Expenditures for warranties (4,500) $158,000 (4,500) $195,000 (4,500) $92,100 Taxable income Pretax financial income 2016 2017 2018 Excess of revenues over expenses...

Taxable income and pretax financial income would be identical for Bonita Co. except for its treatments of gross profit on installment sales and estimated costs of warranties The following income computations have been prepared Taxable income 2016 2017 2018 Excess of revenues over expenses (excluding two temporary differences) Installment gross profit collected $154,000 $191,000 $88,100 8,500 8,500 8.500 Expenditures for warranties (4,500) $158,000 (4,500) $195,000 (4,500) $92,100 Taxable income Pretax financial income 2016 2017 2018 Excess of revenues over expenses...

Taxable income and pretax financial income would be identical

for Crane Co. except for its treatments of gross profit on

installment sales and estimated costs of warranties. The following

income computations have been prepared.

Taxable income

2016

2017

2018

Excess of revenues over

expenses (excluding two temporary differences)

$154,000

$215,000

$93,500

Installment gross profit

collected

8,500

8,500

8,500

Expenditures for

warranties

(5,500

)

(5,500

)

(5,500

)

Taxable

income

$157,000

$218,000

$96,500

Pretax financial income

2016

2017

2018

Excess of...

Taxable income and pretax financial income would be identical

for Crane Co. except for its treatments of gross profit on

installment sales and estimated costs of warranties. The following

income computations have been prepared.

Taxable income

2016

2017

2018

Excess of revenues over

expenses (excluding two temporary differences)

$154,000

$215,000

$93,500

Installment gross profit

collected

8,500

8,500

8,500

Expenditures for

warranties

(5,500

)

(5,500

)

(5,500

)

Taxable

income

$157,000

$218,000

$96,500

Pretax financial income

2016

2017

2018

Excess of...

Taxable income and pretax financial income would be identical for Bramble Co. except for its treatments of gross profit on installment sales and estimated costs of warranties. The following income computations have been prepared. 2016 2017 2018 Taxable income Excess of revenues over expenses (excluding two temporary differences) Installment gross profit collected Expenditures for warranties Taxable income $83,200 7,300 $149,000 7,300 (5,000) $151,300 $218,000 7,300 (5,000) $220,300 (5,000) $85,500 2016 2017 2018 $149,000 $83,200 Pretax financial income Excess of revenues...

Taxable income and pretax financial income would be identical for Bramble Co. except for its treatments of gross profit on installment sales and estimated costs of warranties. The following income computations have been prepared. 2016 2017 2018 Taxable income Excess of revenues over expenses (excluding two temporary differences) Installment gross profit collected Expenditures for warranties Taxable income $83,200 7,300 $149,000 7,300 (5,000) $151,300 $218,000 7,300 (5,000) $220,300 (5,000) $85,500 2016 2017 2018 $149,000 $83,200 Pretax financial income Excess of revenues...

Question 15 Taxable income and preta financial income would be computations have been prepared til for Grouper Co. except for its treatments of gross profit on installment Sales and estimated costs of warranties. The following income 2016 2017 2018 Taxable income Excess of revenues over expenses (excluding two temporary Terences) Installment gross profit collected Expenditures for warranties Taxable income 5166,000 7,500 (4,800) $168,700 200.000 7.500 92.900 7.500 (4,800 ) $205,700 (4.800) 995,600 2016 2017 2018 Pretax financial income Excess of...

Question 15 Taxable income and preta financial income would be computations have been prepared til for Grouper Co. except for its treatments of gross profit on installment Sales and estimated costs of warranties. The following income 2016 2017 2018 Taxable income Excess of revenues over expenses (excluding two temporary Terences) Installment gross profit collected Expenditures for warranties Taxable income 5166,000 7,500 (4,800) $168,700 200.000 7.500 92.900 7.500 (4,800 ) $205,700 (4.800) 995,600 2016 2017 2018 Pretax financial income Excess of...

E19-4 (L01,2) (Three Differences, Compute Taxable income, Entry for Taxes) Zurich Company reports pretax financial income of $70,000 for 2017. The following items cause taxable income to be different than pretax financial income. 1. Depreciation on the tax return is greater than depreciation on the income statement by $16,000. 2. Rent collected on the tax return is greater than rent recognized on the income stalement by $22,000. 3. Fines for pollution appear as an expense of $11,000 on the income...

E19-4 (L01,2) (Three Differences, Compute Taxable income, Entry for Taxes) Zurich Company reports pretax financial income of $70,000 for 2017. The following items cause taxable income to be different than pretax financial income. 1. Depreciation on the tax return is greater than depreciation on the income statement by $16,000. 2. Rent collected on the tax return is greater than rent recognized on the income stalement by $22,000. 3. Fines for pollution appear as an expense of $11,000 on the income...

E19-4 (L01,2) (Three Differences, Compute Taxable income, Entry for Taxes) Zurich Company reports pretax financial income of $70,000 for 2017. The following items cause taxable income to be different than pretax financial income. 1. Depreciation on the tax return is greater than depreciation on the income statement by $16,000. 2. Rent collected on the tax return is greater than rent recognized on the income stalement by $22,000. 3. Fines for pollution appear as an expense of $11,000 on the income...

E19-4 (L01,2) (Three Differences, Compute Taxable income, Entry for Taxes) Zurich Company reports pretax financial income of $70,000 for 2017. The following items cause taxable income to be different than pretax financial income. 1. Depreciation on the tax return is greater than depreciation on the income statement by $16,000. 2. Rent collected on the tax return is greater than rent recognized on the income stalement by $22,000. 3. Fines for pollution appear as an expense of $11,000 on the income...

E19-4 (LO1,2) (Three Differences, Compute Taxable Income, Entry for Taxes) Zurich Company reports pretax financial income of $70,000 for 2017. The following items cause taxable income to be different than pretax financial income. 1. Depreciation on the tax return is greater than depreciation on the income statement by $16,000. 2. Rent collected on the tax return is greater than rent recognized on the income sta.sment by $22,000. 3. Fines for pollution appear as an expense of $11,000 on the income...

E19-4 (LO1,2) (Three Differences, Compute Taxable Income, Entry for Taxes) Zurich Company reports pretax financial income of $70,000 for 2017. The following items cause taxable income to be different than pretax financial income. 1. Depreciation on the tax return is greater than depreciation on the income statement by $16,000. 2. Rent collected on the tax return is greater than rent recognized on the income sta.sment by $22,000. 3. Fines for pollution appear as an expense of $11,000 on the income...

Most questions answered within 3 hours.

-

A 747 has a cruising speed of 235 m/s at a height of 10,700

meters. The...

asked 4 minutes ago -

Part 3: Arrows

Write a python program that prompts the user for a number of

columns,...

asked 11 minutes ago -

Need help answering these questions!!

1. What economic concept do you find most interesting in

Macroeconomics?...

asked 15 minutes ago -

1. Nimbus, Inc. produces and sells brooms. This table shows the

relationship between the number of...

asked 19 minutes ago -

A gas occupies 200. mL in a piston. If the pressure of the

piston were decreased...

asked 35 minutes ago -

A fossil is found to have a 14C level of 71.0% compared to

living organisms. How...

asked 39 minutes ago -

Many communist or socialist countries have a department that

addresses public health as well as the...

asked 41 minutes ago -

the following questions are either true or false answers

1. The Central Limit Theorem allows one...

asked 41 minutes ago -

The patient recovery time from a particular surgical procedure

is normally distributed with a mean of...

asked 47 minutes ago -

Human relations refer to the way a company arranges people,

jobs, and communications so that work...

asked 1 hour ago -

Python Program: Design the logic for and implement a program

that merges the two files into...

asked 1 hour ago -

The specific radiocarbon activity of a sample of wood is 6.25

gms dpm/gm of carbon. The...

asked 1 hour ago