E19-1. (One Temporary Difference, Future Taxable Amounts, One Rate, No Beginning Deferred Taxes) 2 5 South...

| E19-1. |

(One Temporary Difference, Future Taxable Amounts, One Rate, No Beginning Deferred Taxes)

Instructions

|

Homework Answers

Tax is the amount of a compulsory monetary charge or any other levy imposed on a person liable to pay it by government to fund various expenditures and welfare schemes of the government. Tax is a major revenue source of the government. The income statement consists of both income tax and deferred tax.

An Income tax expense is a tax on the income of the individual or entities who are liable to pay tax. Income tax varies with the amount of income earned by an assessed. Income tax increases with increase in income and various deductions are also permissible to taxpayers while calculating income.

Deferred income tax is a virtual asset or liability created to reflect the difference in calculation of income and tax as per assesses books of account and as per taxation laws prevailing in its jurisdiction. Deferred tax is calculated based on the temporary timing differences which are capable of reversal in the subsequent time periods.

The following terms are relevant for understanding the concept of income tax and deferred tax:

• Taxable income: Taxable income is the income on which an individual’s or a company’s income tax is calculated as per government tax laws.

• Accounting income: Accounting income is the income which is calculated by a company from its accounting records maintained.

• Temporary differences: Temporary differences are the differences between book income and taxable income due to certain items of income and expenses that are recognized in one period for calculating taxable income and in a different period in the books for calculating accounting income.

• Permanent differences: Permanent differences are those differences that are recognized in the books but are disallowed in taxation laws, that is, they are the items of income/ expense which are to be excluded in the calculation of taxable income.

Deferred tax is the result of temporary differences and permanent differences are completely ignored for calculation of deferred tax due to their incapacity of reversal in the subsequent time periods.

The items causing temporary differences are added/ subtracted from accounting income to arrive at taxable income. Examples of temporary difference includes methods of charging depreciation, quantum of deduction allowable to taxpayer etc.

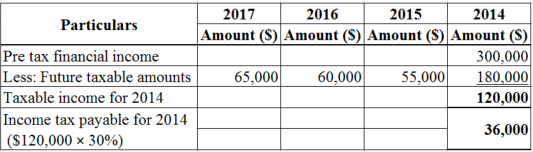

Compute taxable income and income taxes payable for 2014 as follows:

[Part a]

Part a

Part a

Compute the deferred tax liability as follows:

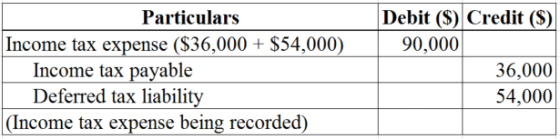

Pass the journal entry to record the income tax expense, deferred income taxes and income tax payable for 2014 as follows:

[Part b]

Part b

Part b

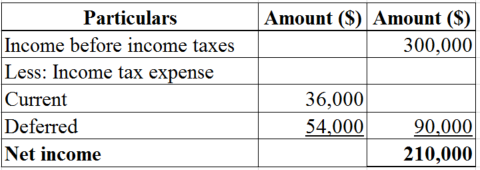

Prepare the income tax section of the income statement for 2014 as follows:

[Part c]

Part c

Part c

Ans: Part aThe taxable income and income taxes payable for 2014 are $120,000 and $36,000 respectively.

Part bPass the journal entry to record the income tax expense, deferred income taxes and income tax payable for 2014 as follows:

Therefore, the net income for the year 2014 as per income statement is $210,000.

Add Answer to:

E19-1.

(One Temporary Difference, Future Taxable Amounts, One Rate, No

Beginning Deferred Taxes)

2

5

South...

E19.1 (LO1,2) (One temporary difference, Future Taxable Amounts, One Rate, No Beginning Differed Taxes) South Carolina...

E19.1 (LO1,2) (One temporary difference, Future Taxable Amounts, One Rate, No Beginning Differed Taxes) South Carolina Corporation has one temporary difference at the end of 2020 that will reverse and cause taxable amounts of $55,000 in 2021, $60,000 in 2022, and $65,000 in 2023. South Carolina’s pretax financial income for 2020 is $300,000, and the tax rate is 30% for all years. There are no deferred taxes at the beginning of 2020. Instructions Prepare the journal entry to record income...

E19.3, (LO 1, 2) Excel (One Temporary Difference, Future Taxable Amounts, One Rate, beginning Deferred Taxes)...

E19.3, (LO 1, 2) Excel (One Temporary Difference, Future Taxable Amounts, One Rate, beginning Deferred Taxes) Bandung Corporation began 2020 with a $46,000 balance in the Deferred Tax Liability account. At the end of 2020, the related cumulative temporary difference amounts to $350,000, and it will reverse evenly over the next 2 vears. Pretax accounting income for 2020 is $325,000. the tax rate for all years is 20%, and taxable income for 2020 is $405,000. Instructions a. Compute income taxes...

E19.3, (LO 1, 2) Excel (One Temporary Difference, Future Taxable Amounts, One Rate, beginning Deferred Taxes) Bandung Corporation began 2020 with a $46,000 balance in the Deferred Tax Liability account. At the end of 2020, the related cumulative temporary difference amounts to $350,000, and it will reverse evenly over the next 2 vears. Pretax accounting income for 2020 is $325,000. the tax rate for all years is 20%, and taxable income for 2020 is $405,000. Instructions a. Compute income taxes...

E19.3 (LOI,2) (One Temporary Difference, Future Taxable Amounts, One Rate, Beginning Deferred Taxes) Brennan Corporation began...

E19.3 (LOI,2) (One Temporary Difference, Future Taxable Amounts, One Rate, Beginning Deferred Taxes) Brennan Corporation began 2019 with a $90,000 balance in the Deferred Tax Liabil- ity account. At the end of 2019, the related cumulative temporary difference amounts to $350,000, and it will reverse evenly over the next 2 years. Pretax accounting income for 2019 is $525,000, the tax rate for all years is 40%, and taxable income for 2019 is $400,000. Instructions a. Compute income taxes payable for...

E19.3 (LOI,2) (One Temporary Difference, Future Taxable Amounts, One Rate, Beginning Deferred Taxes) Brennan Corporation began 2019 with a $90,000 balance in the Deferred Tax Liabil- ity account. At the end of 2019, the related cumulative temporary difference amounts to $350,000, and it will reverse evenly over the next 2 years. Pretax accounting income for 2019 is $525,000, the tax rate for all years is 40%, and taxable income for 2019 is $400,000. Instructions a. Compute income taxes payable for...

E19-17B (Two Temporary Differences, Tracked through 3 Years, Multiple Rates) Taxable income and pretax financial income...

E19-17B (Two Temporary Differences, Tracked through 3 Years, Multiple Rates) Taxable income and pretax financial income would be identical for Ursula Co. except for its depreciation on equipment pur- chased in 2014 for $500,000 and estimated costs of warranties. The following income computations have been prepared. Taxable income 2014 2015 2016 Excess of revenues over expenses (excluding two temporary differences) Tax Depreciation Expenditures for warranties Taxable income $265,000 (125,000) (10,000) $ 130,000 $ 630,000 (200,000) (50,000) $ 380,000 $ 250,000...

E19-17B (Two Temporary Differences, Tracked through 3 Years, Multiple Rates) Taxable income and pretax financial income would be identical for Ursula Co. except for its depreciation on equipment pur- chased in 2014 for $500,000 and estimated costs of warranties. The following income computations have been prepared. Taxable income 2014 2015 2016 Excess of revenues over expenses (excluding two temporary differences) Tax Depreciation Expenditures for warranties Taxable income $265,000 (125,000) (10,000) $ 130,000 $ 630,000 (200,000) (50,000) $ 380,000 $ 250,000...

POLOOOOOOOOOOO E19.5 (LO 1, 2) (Two Temporary Differences, One Rate, Beginning Deferred Taxes) The fol- lowing...

POLOOOOOOOOOOO E19.5 (LO 1, 2) (Two Temporary Differences, One Rate, Beginning Deferred Taxes) The fol- lowing facts relate to Krung Thep Corporation. 1. Deferred tax liability, January 1, 2020, $20,000. 2. Deferred tax asset, January 1, 2020, $0. 3. Taxable income for 2020, $95,000. 4. Pretax financial income for 2020, $200,000. 5. Cumulative temporary difference at December 31, 2020, giving rise to future taxable amounts, $240,000. 6. Cumulative temporary difference at December 31, 2020, giving rise to future deductible amounts,...

POLOOOOOOOOOOO E19.5 (LO 1, 2) (Two Temporary Differences, One Rate, Beginning Deferred Taxes) The fol- lowing facts relate to Krung Thep Corporation. 1. Deferred tax liability, January 1, 2020, $20,000. 2. Deferred tax asset, January 1, 2020, $0. 3. Taxable income for 2020, $95,000. 4. Pretax financial income for 2020, $200,000. 5. Cumulative temporary difference at December 31, 2020, giving rise to future taxable amounts, $240,000. 6. Cumulative temporary difference at December 31, 2020, giving rise to future deductible amounts,...

Crane Corporation has one temporary difference at the end of 2020 that will reverse and cause...

Crane Corporation has one temporary difference at the end of 2020 that will reverse and cause taxable amounts of $56,200 in 2021, $61,000 in 2022, and $66,500 in 2023. Crane’s pretax financial income for 2020 is $285,200, and the tax rate is 30% for all years. There are no deferred taxes at the beginning of 2020. Compute taxable income and income taxes payable for 2020. Prepare the journal entry to record income tax expense, deferred income taxes, and income taxes...

I years is 40%. ne le manner in which deferred taxes should be presented on Belmont...

I years is 40%. ne le manner in which deferred taxes should be presented on Belmont Company's December 31, 2016, balance sheet. E19-10 (L01,2) (Two Temporary Differences, One Rate, Beginning Deferred Taxes, Compute Pretax Financial Income) The following facts relate to Duncan Corporation. 1. Deferred tax liability, January 1, 2017, 560,000. 2. Deferred tax asset, January 1, 2017, $20,000. 3. Taxable income for 2017, S105,000. 4. Cumulative temporary difference at December 31, 2017, giving rise to future taxable amounts, $230,000...

I years is 40%. ne le manner in which deferred taxes should be presented on Belmont Company's December 31, 2016, balance sheet. E19-10 (L01,2) (Two Temporary Differences, One Rate, Beginning Deferred Taxes, Compute Pretax Financial Income) The following facts relate to Duncan Corporation. 1. Deferred tax liability, January 1, 2017, 560,000. 2. Deferred tax asset, January 1, 2017, $20,000. 3. Taxable income for 2017, S105,000. 4. Cumulative temporary difference at December 31, 2017, giving rise to future taxable amounts, $230,000...

Pharoah Corporation has one temporary difference at the end of 2020 that will reverse and cause...

Pharoah Corporation has one temporary

difference at the end of 2020 that will reverse and cause taxable

amounts of $58,600 in 2021, $64,100 in 2022, and $69,000 in 2023.

Pharoah’s pretax financial income for 2020 is $289,500, and the tax

rate is 30% for all years. There are no deferred taxes at the

beginning of 2020.

Pharoah Corporation has one temporary difference at the end of 2020 that will reverse and cause taxable amounts of $58,600 in 2021. $64.100 in...

Pharoah Corporation has one temporary

difference at the end of 2020 that will reverse and cause taxable

amounts of $58,600 in 2021, $64,100 in 2022, and $69,000 in 2023.

Pharoah’s pretax financial income for 2020 is $289,500, and the tax

rate is 30% for all years. There are no deferred taxes at the

beginning of 2020.

Pharoah Corporation has one temporary difference at the end of 2020 that will reverse and cause taxable amounts of $58,600 in 2021. $64.100 in...

Exercise 19-1 Headland Corporation has one temporary difference at the end of 2017 that will reverse...

Exercise 19-1 Headland Corporation has one temporary difference at the end of 2017 that will reverse and cause taxable amounts of $53,900 in 2018, $58,600 in 2019, and $63,900 in 2020. Headland's pretax financial income for 2017 is $304,500, and the tax rate is 40% for all years. There are no deferred taxes at the beginning of 2017 Compute taxable income and income taxes payable for 2017. Taxable income Income taxes payable $ Prepare the journal entry to record income...

Exercise 19-1 Headland Corporation has one temporary difference at the end of 2017 that will reverse and cause taxable amounts of $53,900 in 2018, $58,600 in 2019, and $63,900 in 2020. Headland's pretax financial income for 2017 is $304,500, and the tax rate is 40% for all years. There are no deferred taxes at the beginning of 2017 Compute taxable income and income taxes payable for 2017. Taxable income Income taxes payable $ Prepare the journal entry to record income...

6:31 @ . Indigo Corporation has one temporary difference at the end of 2020 that will...

6:31 @ . Indigo Corporation has one temporary difference at the end of 2020 that will reverse and cause taxable amounts of $49.800 in 2021. $54.700 in 2022, and $59,300 in 2023. Indigo's pretax financial income for 2020 is $285,000, and the tax rate is 30% for all years There are no deferred taxes at the beginning of 2020 Compute taxable income and income taxes payable for 2020 Prepare the journal entry to record income tax expense, deferred income taxes,...

6:31 @ . Indigo Corporation has one temporary difference at the end of 2020 that will reverse and cause taxable amounts of $49.800 in 2021. $54.700 in 2022, and $59,300 in 2023. Indigo's pretax financial income for 2020 is $285,000, and the tax rate is 30% for all years There are no deferred taxes at the beginning of 2020 Compute taxable income and income taxes payable for 2020 Prepare the journal entry to record income tax expense, deferred income taxes,...

E19.3, (LO 1, 2) Excel (One Temporary Difference, Future Taxable Amounts, One Rate, beginning Deferred Taxes) Bandung Corporation began 2020 with a $46,000 balance in the Deferred Tax Liability account. At the end of 2020, the related cumulative temporary difference amounts to $350,000, and it will reverse evenly over the next 2 vears. Pretax accounting income for 2020 is $325,000. the tax rate for all years is 20%, and taxable income for 2020 is $405,000. Instructions a. Compute income taxes...

E19.3, (LO 1, 2) Excel (One Temporary Difference, Future Taxable Amounts, One Rate, beginning Deferred Taxes) Bandung Corporation began 2020 with a $46,000 balance in the Deferred Tax Liability account. At the end of 2020, the related cumulative temporary difference amounts to $350,000, and it will reverse evenly over the next 2 vears. Pretax accounting income for 2020 is $325,000. the tax rate for all years is 20%, and taxable income for 2020 is $405,000. Instructions a. Compute income taxes...

E19.3 (LOI,2) (One Temporary Difference, Future Taxable Amounts, One Rate, Beginning Deferred Taxes) Brennan Corporation began 2019 with a $90,000 balance in the Deferred Tax Liabil- ity account. At the end of 2019, the related cumulative temporary difference amounts to $350,000, and it will reverse evenly over the next 2 years. Pretax accounting income for 2019 is $525,000, the tax rate for all years is 40%, and taxable income for 2019 is $400,000. Instructions a. Compute income taxes payable for...

E19.3 (LOI,2) (One Temporary Difference, Future Taxable Amounts, One Rate, Beginning Deferred Taxes) Brennan Corporation began 2019 with a $90,000 balance in the Deferred Tax Liabil- ity account. At the end of 2019, the related cumulative temporary difference amounts to $350,000, and it will reverse evenly over the next 2 years. Pretax accounting income for 2019 is $525,000, the tax rate for all years is 40%, and taxable income for 2019 is $400,000. Instructions a. Compute income taxes payable for...

E19-17B (Two Temporary Differences, Tracked through 3 Years, Multiple Rates) Taxable income and pretax financial income would be identical for Ursula Co. except for its depreciation on equipment pur- chased in 2014 for $500,000 and estimated costs of warranties. The following income computations have been prepared. Taxable income 2014 2015 2016 Excess of revenues over expenses (excluding two temporary differences) Tax Depreciation Expenditures for warranties Taxable income $265,000 (125,000) (10,000) $ 130,000 $ 630,000 (200,000) (50,000) $ 380,000 $ 250,000...

E19-17B (Two Temporary Differences, Tracked through 3 Years, Multiple Rates) Taxable income and pretax financial income would be identical for Ursula Co. except for its depreciation on equipment pur- chased in 2014 for $500,000 and estimated costs of warranties. The following income computations have been prepared. Taxable income 2014 2015 2016 Excess of revenues over expenses (excluding two temporary differences) Tax Depreciation Expenditures for warranties Taxable income $265,000 (125,000) (10,000) $ 130,000 $ 630,000 (200,000) (50,000) $ 380,000 $ 250,000...

POLOOOOOOOOOOO E19.5 (LO 1, 2) (Two Temporary Differences, One Rate, Beginning Deferred Taxes) The fol- lowing facts relate to Krung Thep Corporation. 1. Deferred tax liability, January 1, 2020, $20,000. 2. Deferred tax asset, January 1, 2020, $0. 3. Taxable income for 2020, $95,000. 4. Pretax financial income for 2020, $200,000. 5. Cumulative temporary difference at December 31, 2020, giving rise to future taxable amounts, $240,000. 6. Cumulative temporary difference at December 31, 2020, giving rise to future deductible amounts,...

POLOOOOOOOOOOO E19.5 (LO 1, 2) (Two Temporary Differences, One Rate, Beginning Deferred Taxes) The fol- lowing facts relate to Krung Thep Corporation. 1. Deferred tax liability, January 1, 2020, $20,000. 2. Deferred tax asset, January 1, 2020, $0. 3. Taxable income for 2020, $95,000. 4. Pretax financial income for 2020, $200,000. 5. Cumulative temporary difference at December 31, 2020, giving rise to future taxable amounts, $240,000. 6. Cumulative temporary difference at December 31, 2020, giving rise to future deductible amounts,...

I years is 40%. ne le manner in which deferred taxes should be presented on Belmont Company's December 31, 2016, balance sheet. E19-10 (L01,2) (Two Temporary Differences, One Rate, Beginning Deferred Taxes, Compute Pretax Financial Income) The following facts relate to Duncan Corporation. 1. Deferred tax liability, January 1, 2017, 560,000. 2. Deferred tax asset, January 1, 2017, $20,000. 3. Taxable income for 2017, S105,000. 4. Cumulative temporary difference at December 31, 2017, giving rise to future taxable amounts, $230,000...

I years is 40%. ne le manner in which deferred taxes should be presented on Belmont Company's December 31, 2016, balance sheet. E19-10 (L01,2) (Two Temporary Differences, One Rate, Beginning Deferred Taxes, Compute Pretax Financial Income) The following facts relate to Duncan Corporation. 1. Deferred tax liability, January 1, 2017, 560,000. 2. Deferred tax asset, January 1, 2017, $20,000. 3. Taxable income for 2017, S105,000. 4. Cumulative temporary difference at December 31, 2017, giving rise to future taxable amounts, $230,000...

Pharoah Corporation has one temporary

difference at the end of 2020 that will reverse and cause taxable

amounts of $58,600 in 2021, $64,100 in 2022, and $69,000 in 2023.

Pharoah’s pretax financial income for 2020 is $289,500, and the tax

rate is 30% for all years. There are no deferred taxes at the

beginning of 2020.

Pharoah Corporation has one temporary difference at the end of 2020 that will reverse and cause taxable amounts of $58,600 in 2021. $64.100 in...

Pharoah Corporation has one temporary

difference at the end of 2020 that will reverse and cause taxable

amounts of $58,600 in 2021, $64,100 in 2022, and $69,000 in 2023.

Pharoah’s pretax financial income for 2020 is $289,500, and the tax

rate is 30% for all years. There are no deferred taxes at the

beginning of 2020.

Pharoah Corporation has one temporary difference at the end of 2020 that will reverse and cause taxable amounts of $58,600 in 2021. $64.100 in...

Exercise 19-1 Headland Corporation has one temporary difference at the end of 2017 that will reverse and cause taxable amounts of $53,900 in 2018, $58,600 in 2019, and $63,900 in 2020. Headland's pretax financial income for 2017 is $304,500, and the tax rate is 40% for all years. There are no deferred taxes at the beginning of 2017 Compute taxable income and income taxes payable for 2017. Taxable income Income taxes payable $ Prepare the journal entry to record income...

Exercise 19-1 Headland Corporation has one temporary difference at the end of 2017 that will reverse and cause taxable amounts of $53,900 in 2018, $58,600 in 2019, and $63,900 in 2020. Headland's pretax financial income for 2017 is $304,500, and the tax rate is 40% for all years. There are no deferred taxes at the beginning of 2017 Compute taxable income and income taxes payable for 2017. Taxable income Income taxes payable $ Prepare the journal entry to record income...

6:31 @ . Indigo Corporation has one temporary difference at the end of 2020 that will reverse and cause taxable amounts of $49.800 in 2021. $54.700 in 2022, and $59,300 in 2023. Indigo's pretax financial income for 2020 is $285,000, and the tax rate is 30% for all years There are no deferred taxes at the beginning of 2020 Compute taxable income and income taxes payable for 2020 Prepare the journal entry to record income tax expense, deferred income taxes,...

6:31 @ . Indigo Corporation has one temporary difference at the end of 2020 that will reverse and cause taxable amounts of $49.800 in 2021. $54.700 in 2022, and $59,300 in 2023. Indigo's pretax financial income for 2020 is $285,000, and the tax rate is 30% for all years There are no deferred taxes at the beginning of 2020 Compute taxable income and income taxes payable for 2020 Prepare the journal entry to record income tax expense, deferred income taxes,...

Most questions answered within 3 hours.

-

A hot-air balloon is descending with a velocity of (−2.00m/s)y^.

A champagne bottle is opened to...

asked 7 minutes ago -

1. When a nearsighted person looks at an object that is in the

distance with their...

asked 1 hour ago -

QUESTION 8

Both of these statements will store the same value in the

variable $number

$number...

asked 1 hour ago -

The price of 1 lb of potatoes is $1.75. If all the potatoes sold

today at...

asked 2 hours ago -

Garcia Company issues 20.00%, 15-year bonds with a par value of

$470,000 and semiannual interest payments....

asked 2 hours ago -

In C++ Programming, Try using loops only.

This lab demonstrates the use of the While Loop...

asked 3 hours ago -

Effect of DCMU and sodium azide on Chlamydomonas? We did an

experiment where we had Chlamydomonas...

asked 4 hours ago -

1a) According to the ideal gas law, _______________.

a. a gas has infinite volume at absolute...

asked 5 hours ago -

Oakdale Fashions, Inc. had $245,000 in 2018 taxable income.

Using the tax schedule in Table 2.3...

asked 6 hours ago -

The marketing class at CSUS had an average score of 150. An

educational analyst determined that...

asked 7 hours ago -

Justin Case has purchased a $250 000 home by putting 20 % down

and taking out...

asked 7 hours ago -

1. In a labor market, marginal cost for a firm is

____________.

a. recruiting cost

b....

asked 8 hours ago