The table below gives today’s prices of six-month European put and call options written on a...

- The table below gives today’s prices of six-month European put and call options written on a share of ABC stock at different strike prices. The stock does not pay a dividend and the risk-free interest rate is 0% per annum.

|

Call Price ($) |

Strike Price ($) |

Put Price ($) |

|

13.1 |

105 |

8.2 |

|

9.7 |

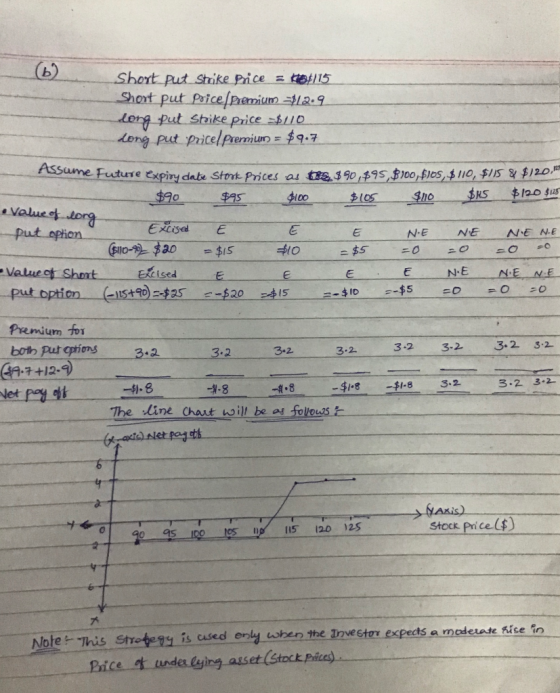

110 |

9.7 |

|

7.9 |

115 |

12.9 |

- Using call options with strike prices of 105 and 110, create a bear spread and show in a table the profit of the spread at maturity as a function of the then stock price. Give the range of stock prices at maturity for which this portfolio of options is profitable.

- Using put options with strike prices of 110 and 115, create a bull spread and show in a table the profit of the spread at maturity as a function of the then stock price. Give the range of stock prices at maturity for which this portfolio of options is profitable.

Homework Answers

Add Answer to:

The table below gives today’s prices of six-month European put

and call options written on a...

the cash price of a one year treasury bill is 95 per 100 of face value....

the

cash price of a one year treasury bill is 95 per 100 of face value.

a 2 year bond with a face value of 100usd that pays annual coupons

of

8. The table below gives today's prices of six-month European put and call options written on a share of ABC stock at different strike prices. The stock does not pay a dividend and the risk-free interest rate is 0% per annum. Put Price (S) Call Price (S) 13.1 9.7...

the

cash price of a one year treasury bill is 95 per 100 of face value.

a 2 year bond with a face value of 100usd that pays annual coupons

of

8. The table below gives today's prices of six-month European put and call options written on a share of ABC stock at different strike prices. The stock does not pay a dividend and the risk-free interest rate is 0% per annum. Put Price (S) Call Price (S) 13.1 9.7...

6. The following table shows the premiums of European call and put options having the same...

6. The following table shows the premiums of European call and put options having the same underlying stock, the same time to expiration but different strike prices: StrikeCall Premium Put Premium $20 $23 $25 $3.59 $2.45 $1.89 $2.64 $4.36 $5.70 You use the above call and put options to construct an asymmetric butterfly spread with the following characteristics (i) The maximum payoff of 6 is attained when the stock price at expiration is 23 (ii) The payoff is strictly positive...

6. The following table shows the premiums of European call and put options having the same underlying stock, the same time to expiration but different strike prices: StrikeCall Premium Put Premium $20 $23 $25 $3.59 $2.45 $1.89 $2.64 $4.36 $5.70 You use the above call and put options to construct an asymmetric butterfly spread with the following characteristics (i) The maximum payoff of 6 is attained when the stock price at expiration is 23 (ii) The payoff is strictly positive...

Suppose that call options on a stock with strike prices $25 and $35 cost $7 and...

Suppose that call options on a stock with strike prices $25 and $35 cost $7 and $2, respectively. How can the options be used to create (a) a bull spread and (b) a bear spread? Construct a table that shows the profit and payo↵ for both spreads.

Three-month European put options with strike prices of $50, $55, and $60 cost $2, $4, and...

Three-month European put options with strike prices of $50, $55, and $60 cost $2, $4, and $7, respectively. 1) How can one create a butterfly spread using these options? 2) Please draw the payoff and profit diagrams of this butterfly strategy. 3) What are the maximum gain and maximum loss of the butterfly spread created using these put options? 4) For which two values of ST does the holder of the butterfly spread break even (with a profit of zero),...

A trader creates a long butterfly spread from put options with strike prices of $90, $100,...

A trader creates a long butterfly spread from put options with strike prices of $90, $100, and $110 per share by trading a total of 40 option contracts (buy 10 contracts struck at $90, sell 20 contracts struck at $100 and buy 10 contracts struck at $110). Each contract is written on 100 shares of stock. The options are worth $18, $24, and $32 per share of stock. What is the value of the butterfly spread at maturity as a...

Suppose the prices of 3-month European call options with strike prices of $40, $45 and $50 are $6.08, $2.70, and $0.86, respectively.

Suppose the prices of 3-month European call options with strike prices of $40, $45 and $50 are $6.08, $2.70, and $0.86, respectively. a) Explain how a trader can create a butterfly spread using these options. b) What is the profit when the price of the underlying asset in three months is $40 c) What is the profit when the price of the underlying asset in three months is $43 d) What is the profit when the price of the underlying...

ABC, a non-dividend paying stock Details of European option prices follows on are as Option type...

ABC, a non-dividend paying stock Details of European option prices follows on are as Option type Exercise price Option premium Call on Stock ABC $17.50 $20 $5.50 $3.50 Required: Create a call ratio spread by using the above options. A call ratio spread consists of taking a long position in a bull spread and selling another call on the same stock with the strike price of $20. Draw the profit and loss diagram (on the following page) of the call...

ABC, a non-dividend paying stock Details of European option prices follows on are as Option type Exercise price Option premium Call on Stock ABC $17.50 $20 $5.50 $3.50 Required: Create a call ratio spread by using the above options. A call ratio spread consists of taking a long position in a bull spread and selling another call on the same stock with the strike price of $20. Draw the profit and loss diagram (on the following page) of the call...

10. Use the options prices for Spotify in the EXCEL FILE to create a bear spread...

10. Use the options prices for Spotify in the EXCEL FILE to create a bear spread using the puts with strike prices 170 and 175. Be sure to use the appropriate bid and ask prices. a. What will be your cash flow per share when you set up the position? Show all cash flows: inflows, outflows, and net flow. Inflow Outflow Net Flow b. The maximum profit on the put bear spread is c. The minimum profit on the put...

10. Use the options prices for Spotify in the EXCEL FILE to create a bear spread using the puts with strike prices 170 and 175. Be sure to use the appropriate bid and ask prices. a. What will be your cash flow per share when you set up the position? Show all cash flows: inflows, outflows, and net flow. Inflow Outflow Net Flow b. The maximum profit on the put bear spread is c. The minimum profit on the put...

The prices of European call and put options on a dividend-paying stock with 6 months to...

The prices of European call and put options on a dividend-paying stock with 6 months to maturity and a strike price of $125 are $20 and $5, respectively. If the current stock price is $140, what is the implied annual continuously compounded risk-free rate? Assume the present value of dividend to be paid out over the next 6 months is $3.

5.8. The prices of European call and put options on a non-dividend-paying stock with 15 months to...

5.8. The prices of European call and put options on a non-dividend-paying stock with 15 months to maturity, a strike price of $118, and an expiration date in 15 months are $21 and $5, respectively. The current stock price is $125. What is the implied risk-free rate?

the

cash price of a one year treasury bill is 95 per 100 of face value.

a 2 year bond with a face value of 100usd that pays annual coupons

of

8. The table below gives today's prices of six-month European put and call options written on a share of ABC stock at different strike prices. The stock does not pay a dividend and the risk-free interest rate is 0% per annum. Put Price (S) Call Price (S) 13.1 9.7...

the

cash price of a one year treasury bill is 95 per 100 of face value.

a 2 year bond with a face value of 100usd that pays annual coupons

of

8. The table below gives today's prices of six-month European put and call options written on a share of ABC stock at different strike prices. The stock does not pay a dividend and the risk-free interest rate is 0% per annum. Put Price (S) Call Price (S) 13.1 9.7...

6. The following table shows the premiums of European call and put options having the same underlying stock, the same time to expiration but different strike prices: StrikeCall Premium Put Premium $20 $23 $25 $3.59 $2.45 $1.89 $2.64 $4.36 $5.70 You use the above call and put options to construct an asymmetric butterfly spread with the following characteristics (i) The maximum payoff of 6 is attained when the stock price at expiration is 23 (ii) The payoff is strictly positive...

6. The following table shows the premiums of European call and put options having the same underlying stock, the same time to expiration but different strike prices: StrikeCall Premium Put Premium $20 $23 $25 $3.59 $2.45 $1.89 $2.64 $4.36 $5.70 You use the above call and put options to construct an asymmetric butterfly spread with the following characteristics (i) The maximum payoff of 6 is attained when the stock price at expiration is 23 (ii) The payoff is strictly positive...

ABC, a non-dividend paying stock Details of European option prices follows on are as Option type Exercise price Option premium Call on Stock ABC $17.50 $20 $5.50 $3.50 Required: Create a call ratio spread by using the above options. A call ratio spread consists of taking a long position in a bull spread and selling another call on the same stock with the strike price of $20. Draw the profit and loss diagram (on the following page) of the call...

ABC, a non-dividend paying stock Details of European option prices follows on are as Option type Exercise price Option premium Call on Stock ABC $17.50 $20 $5.50 $3.50 Required: Create a call ratio spread by using the above options. A call ratio spread consists of taking a long position in a bull spread and selling another call on the same stock with the strike price of $20. Draw the profit and loss diagram (on the following page) of the call...

10. Use the options prices for Spotify in the EXCEL FILE to create a bear spread using the puts with strike prices 170 and 175. Be sure to use the appropriate bid and ask prices. a. What will be your cash flow per share when you set up the position? Show all cash flows: inflows, outflows, and net flow. Inflow Outflow Net Flow b. The maximum profit on the put bear spread is c. The minimum profit on the put...

10. Use the options prices for Spotify in the EXCEL FILE to create a bear spread using the puts with strike prices 170 and 175. Be sure to use the appropriate bid and ask prices. a. What will be your cash flow per share when you set up the position? Show all cash flows: inflows, outflows, and net flow. Inflow Outflow Net Flow b. The maximum profit on the put bear spread is c. The minimum profit on the put...

Most questions answered within 3 hours.

-

2. Describe market equilibrium in terms of the following

characteristics

d.

How supply and demand interactions...

asked 3 minutes ago -

1a. Create a class named Computer

- Separate declaration from implementation (i.e. Header and CPP

files)...

asked 18 minutes ago -

Which of the following does NOT add to US GDP? A. Saudi Arabia

buys fighter jets...

asked 21 minutes ago -

A medical researcher

believes that a drug changes the body's temperature. Seven test

subjects are randomly...

asked 47 minutes ago -

A call option on Project Cash Flow Consulting Inc.'s stock (PCF)

has a market price of...

asked 48 minutes ago -

A study on the latest fad diet claimed that the amounts of

weight lost by all...

asked 1 hour ago -

give examples of how gene expression is inherited to the next

generation?

asked 59 minutes ago -

If a project has _________ IRR(s), we should __________ . Assume

this project is competing with...

asked 1 hour ago -

In the figure, a sound of wavelength 0.700 m is emitted

isotropically by point source S....

asked 1 hour ago -

1) Stock X has a beta of 1.6. If the risk free rate is 3.4

percent...

asked 1 hour ago -

Gallium is produced by the electrolysis of a solution obtained

by dissolving gallium oxide in concentrated...

asked 1 hour ago -

A small company that manufactures juggling equipment makes 19

different types of clubs. The company wants...

asked 1 hour ago