Create a four-period binominal price tree and find the fair value of an European call and...

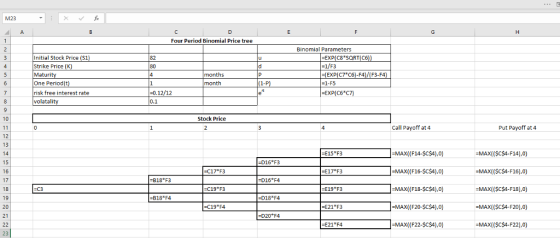

Create a four-period binominal price tree and find the fair value of an European call and put options and an American put option on a nondividend-paying stock if the initial stock price is 82 PLN, the strike price of 80 PLN is expiring at the end of the fourth month, the compound risk-free interest rate is 12% per annum, and σ=0.1.

Homework Answers

Parameters of Option Binomial Model –

There are three parameters of Option Binomial Pricing Model

- up factor (u)

- down factor (d)

- probability (P)

up factor and down factor used to calculate rise in price and fall in price of underlying assets in one period. Probability is measure probability of rise in price and (1-P) is probability of price fall.

Cox-Rox-Rubinstein has suggested following formula to calculate these factors,

Where,

r = risk free interest rate

t = one period time

= risk

Please refer to below spreadsheets for calculations -

Formula reference -

formula reference-

Thus, Value of European call is 9.14 and Value of European Put is 4.0

formula reference-

Thus, Value of American Put is 4.23 at 0 period.

American Put can be exercised early.

Add Answer to:

Create a four-period binominal price tree and find the fair

value of an European call and...

Create a four-period binominal price tree and find the fair value of an European call and...

Create a four-period binominal price tree and find the fair value of an European call and put options and an American put option on a nondividend-paying stock if the initial stock price is 82 PLN, the strike price of 80 PLN is expiring at the end of the fourth month, the compound risk-free interest rate is 12% per annum, and σ= 0.1 .

Create a four-period binominal price tree and find the fair value of an European call and...

Create a four-period binominal price tree and find the fair value of an European call and put options and an American put option on a nondividend-paying stock if the initial stock price is 82 PLN, the strike price of 80 PLN is expiring at the end of the fourth month, the compound risk-free interest rate is 12% per annum, and σ= 0.1 . Please solve in details.

Find the fair value of an European call option and an American put option using the...

Find the fair value of an European call option and an American put option using the incoherent and coherent binomial option tree if the underlying asset pays dividend of 4 PLN in one and half month. The initial stock price is 60 PLN, the strike price of 58 PLN is expiring at the end of the third month, the continuously compounded risk-free interest rate is 10% per annum, and the stock volatility is 20%.

(b) A 6-month European call option on a non-dividend paying stock is cur- rently selling for $3. The stock price is...

(b) A 6-month European call option on a non-dividend paying stock is cur- rently selling for $3. The stock price is $50, the strike price is $55, and the risk-free interest rate is 6% per annum continuously compounded. The price for 6-months European put option with same strike, underlying and maturity is 82. What opportunities are there for an arbitrageur? Describe the strategy and compute the gain.

(b) A 6-month European call option on a non-dividend paying stock is cur- rently selling for $3. The stock price is $50, the strike price is $55, and the risk-free interest rate is 6% per annum continuously compounded. The price for 6-months European put option with same strike, underlying and maturity is 82. What opportunities are there for an arbitrageur? Describe the strategy and compute the gain.

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

A 1-year European call option is modeled with a 1-period binomial tree with u = 1.2, d = 0.7.

A 1-year European call option is modeled with a 1-period binomial tree with u = 1.2, d = 0.7. The stock price is 50. The strike price is 55. The stock pays no dividends. The call premium is 3.10. σ = 0.25.Determine the risk-free rate

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annu...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

The price of a European call option on a non-dividend-paying stock with a strike price of...

The price of a European call option on a non-dividend-paying stock with a strike price of $50 is $6. The stock price is $51, the continuously compounded risk-free rate (all maturities) is 6% and the time to maturity is one year. What is the price of a one-year European put option on the stock with a strike price of $50? $2.09 $7.52 $3.58 $9.91

What is the price of a European call option according to the Black-Sholes formula on a...

What is the price of a European call option according to the Black-Sholes formula on a non-dividend-paying stock when the stock price is $45, the strike price is $50, the risk-free interest rate is 12% per annum, the volatility is 25% per annum, and the time to maturity is six months? Show your work in details.

(b) A 6-month European call option on a non-dividend paying stock is cur- rently selling for $3. The stock price is $50, the strike price is $55, and the risk-free interest rate is 6% per annum continuously compounded. The price for 6-months European put option with same strike, underlying and maturity is 82. What opportunities are there for an arbitrageur? Describe the strategy and compute the gain.

(b) A 6-month European call option on a non-dividend paying stock is cur- rently selling for $3. The stock price is $50, the strike price is $55, and the risk-free interest rate is 6% per annum continuously compounded. The price for 6-months European put option with same strike, underlying and maturity is 82. What opportunities are there for an arbitrageur? Describe the strategy and compute the gain.

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Most questions answered within 3 hours.

-

At the start of a CD it is spinning at a rate of 525 rpm

(revolutions...

asked 12 minutes ago -

4. Without doing any calculations, predict whether the observed

∆T would increase, decrease or remain the...

asked 1 hour ago -

Based on the range, which of the following sets of scores has

the greatest variability? 3,...

asked 2 hours ago -

Ripples in a pond travel at a velocity of 3 m/s with one peak

passing a...

asked 2 hours ago -

A man stands on the roof of a building of height 13.0 mm and

throws a...

asked 2 hours ago -

The extent to which assets are financed by borrowed funds and

other liabilities is indicated by:...

asked 3 hours ago -

Explain in detail

Germany is the fifth largest economy

explain what goods and services Germany specializes...

asked 3 hours ago -

The density of platinum is 21.45 g/mL. If a cube of platinum

with a mass of...

asked 3 hours ago -

Accounts Receivable

Sales

A/R Posting

Extended Sales Invoice

Packing Slip

Compare invoice to packing slip 2...

asked 3 hours ago -

Michaella, age 23, is a full-time law student and is claimed by

her parents as a...

asked 3 hours ago -

Why are polymers not typically casted into products?

asked 4 hours ago -

When rolling a die 129 times, what is the probability of rolling

a 6 no more...

asked 4 hours ago