Homework Answers

Add Answer to:

(b) A 6-month European call option on a non-dividend paying stock is cur- rently selling for $3. The stock price is...

Question 3 (30 Points) (a) Assume that So 10 EUR and r price of a 9-months...

Question 3 (30 Points) (a) Assume that So 10 EUR and r price of a 9-months European put option with strike K 8 EUR is 2 EUR Compute the price of a 9-months European call option with same strike and same underlying. Which relation did you use? (b) A 6-month European call option on a non-dividend-paying stock is cur- rently selling for $3. The stock price is $50, the strike price is $55, and the risk-free interest rate is 6...

Question 3 (30 Points) (a) Assume that So 10 EUR and r price of a 9-months European put option with strike K 8 EUR is 2 EUR Compute the price of a 9-months European call option with same strike and same underlying. Which relation did you use? (b) A 6-month European call option on a non-dividend-paying stock is cur- rently selling for $3. The stock price is $50, the strike price is $55, and the risk-free interest rate is 6...

Question 3 - (30 Points) (a) Assume that So = 10 EUR and r = 3%...

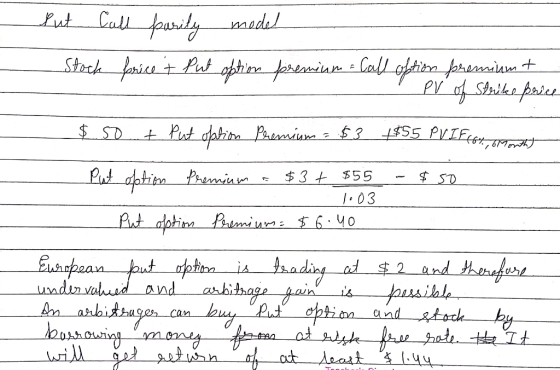

Question 3 - (30 Points) (a) Assume that So = 10 EUR and r = 3% continuously compounded. The price of a 9-months European put option with strike K = 8 EUR is 2 EUR. Compute the price of a 9-months European call option with same strike and same underlying. Which relation did you use? (b) A 6-month European call option on a non-dividend-paying stock is cur- rently selling for $3. The stock price is $50, the strike price is...

Question 3 - (30 Points) (a) Assume that So = 10 EUR and r = 3% continuously compounded. The price of a 9-months European put option with strike K = 8 EUR is 2 EUR. Compute the price of a 9-months European call option with same strike and same underlying. Which relation did you use? (b) A 6-month European call option on a non-dividend-paying stock is cur- rently selling for $3. The stock price is $50, the strike price is...

A six-month European call option on a non-dividend-paying stock is currently selling for $6. The stock...

A six-month European call option on a non-dividend-paying stock is currently selling for $6. The stock price is$64, the strike price is S60. The risk-free interest rate is 12% per annum for all maturities. what opportunities are there for an arbitrageur? (2 points) 1. a. What should be the minimum price of the call option? Does an arbitrage opportunity exist? b. How would you form an arbitrage? What is the arbitrage profit at Time 0? Complete the following table. c....

A six-month European call option on a non-dividend-paying stock is currently selling for $6. The stock price is$64, the strike price is S60. The risk-free interest rate is 12% per annum for all maturities. what opportunities are there for an arbitrageur? (2 points) 1. a. What should be the minimum price of the call option? Does an arbitrage opportunity exist? b. How would you form an arbitrage? What is the arbitrage profit at Time 0? Complete the following table. c....

The price of a European call option on a non-dividend-paying stock with a strike price of...

The price of a European call option on a non-dividend-paying stock with a strike price of $50 is $6. The stock price is $51, the continuously compounded risk-free rate (all maturities) is 6% and the time to maturity is one year. What is the price of a one-year European put option on the stock with a strike price of $50? $2.09 $7.52 $3.58 $9.91

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Consider a European put option on a non-dividend-paying stock. The current stock price is $69, the...

Consider a European put option on a non-dividend-paying stock. The current stock price is $69, the strike price is $70, the risk-free interest rate is 5% per annum, the volatility is 35% per annum and the time to maturity is 6 months. a. Use the Black-Scholes model to calculate the put price. b. Calculate the corresponding call option using the put-call parity relation. Use the Option Calculator Spreadsheet to verify your result.

What is the price of a European put option on a non-dividend-paying stock when the stock...

What is the price of a European put option on a non-dividend-paying stock when the stock price is $69, the strike price is $70, the risk-free interest rate is 5% per annum, the volatility is 35% per annum, and the time to maturity is six months?

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

What is the price of a European put option on a non-dividend paying stock when the...

What is the price of a European put option on a non-dividend paying stock when the stock price is $69, the strike price is $70, the risk-free interest rate is 5% per annum, the volatility is 35%per annum, and the time to maturity is six months? Please give me step by step by step instructions.

A 10-month European call option on a stock is currently selling for $5. The stock price...

A 10-month European call option on a stock is currently selling for $5. The stock price is $64, the strike price is $60. The continuously-compounded risk-free interest rate is 5% per annum for all maturities. a) Suppose that the stock pays no dividend in the next ten months, and that the price of a 10-month European put with a strike price of $60 on the same stock is trading at $1. Is there an arbitrage opportunity? If yes, how can...

Question 3 (30 Points) (a) Assume that So 10 EUR and r price of a 9-months European put option with strike K 8 EUR is 2 EUR Compute the price of a 9-months European call option with same strike and same underlying. Which relation did you use? (b) A 6-month European call option on a non-dividend-paying stock is cur- rently selling for $3. The stock price is $50, the strike price is $55, and the risk-free interest rate is 6...

Question 3 (30 Points) (a) Assume that So 10 EUR and r price of a 9-months European put option with strike K 8 EUR is 2 EUR Compute the price of a 9-months European call option with same strike and same underlying. Which relation did you use? (b) A 6-month European call option on a non-dividend-paying stock is cur- rently selling for $3. The stock price is $50, the strike price is $55, and the risk-free interest rate is 6...

Question 3 - (30 Points) (a) Assume that So = 10 EUR and r = 3% continuously compounded. The price of a 9-months European put option with strike K = 8 EUR is 2 EUR. Compute the price of a 9-months European call option with same strike and same underlying. Which relation did you use? (b) A 6-month European call option on a non-dividend-paying stock is cur- rently selling for $3. The stock price is $50, the strike price is...

Question 3 - (30 Points) (a) Assume that So = 10 EUR and r = 3% continuously compounded. The price of a 9-months European put option with strike K = 8 EUR is 2 EUR. Compute the price of a 9-months European call option with same strike and same underlying. Which relation did you use? (b) A 6-month European call option on a non-dividend-paying stock is cur- rently selling for $3. The stock price is $50, the strike price is...

A six-month European call option on a non-dividend-paying stock is currently selling for $6. The stock price is$64, the strike price is S60. The risk-free interest rate is 12% per annum for all maturities. what opportunities are there for an arbitrageur? (2 points) 1. a. What should be the minimum price of the call option? Does an arbitrage opportunity exist? b. How would you form an arbitrage? What is the arbitrage profit at Time 0? Complete the following table. c....

A six-month European call option on a non-dividend-paying stock is currently selling for $6. The stock price is$64, the strike price is S60. The risk-free interest rate is 12% per annum for all maturities. what opportunities are there for an arbitrageur? (2 points) 1. a. What should be the minimum price of the call option? Does an arbitrage opportunity exist? b. How would you form an arbitrage? What is the arbitrage profit at Time 0? Complete the following table. c....

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Most questions answered within 3 hours.

-

Write a Java program that reads words from a text file and

displays all the non-duplicate...

asked 12 seconds ago -

Assume that you have an outstanding 100M loan with your bank

under which you pay 5%...

asked 1 minute ago -

A 62-kg woman in an elevator is accelerating downward at a rate

of 1.6 m/s2. What...

asked 14 minutes ago -

Darlene owns 500 shares of Sandmayor, Inc., common stock that

she purchased several years ago for...

asked 19 minutes ago -

Photosynthesis

and Chloroplasts

You will read that

only plants, algae, and some bacteria are photosynthetic. There...

asked 26 minutes ago -

Mark has a choice to play a game and pay $80 with a probability

of 40%...

asked 27 minutes ago -

Critical Thinking

In today’s highly competitive, extremely variable and

really dynamic environment, many firms are seeking...

asked 34 minutes ago -

Systems Engineering with Economics, Probability, and Statistics:

Second Edition - Por C. Jotin Khisty, Jamshid Mohammadi,...

asked 43 minutes ago -

After exposure to a bioaccumulating toxin for a long period of

time, which type of organism...

asked 50 minutes ago -

please help asap

in c++, you dont have to do everything but at least give me...

asked 52 minutes ago -

1.ABP pizza produces three different items for their customers:

pizza, calzone and lahmacun. In order to...

asked 1 hour ago -

A non-spontaneous reaction may be driven by coupling it to a

reaction that is spontaneous. The...

asked 1 hour ago