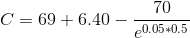

Consider a European put option on a non-dividend-paying stock. The current stock price is $69, the...

Consider a European put option on a non-dividend-paying stock. The

current stock

price is $69, the strike price is $70, the risk-free interest rate

is 5% per annum, the

volatility is 35% per annum and the time to maturity is 6

months.

a. Use the Black-Scholes model to calculate the put price.

b. Calculate the corresponding call option using the put-call

parity relation. Use the

Option Calculator Spreadsheet to verify your result.

Homework Answers

a. Value of Put using Black-Scholes model:

Please refer to below spreadsheet for calculation and answer. Cell reference also provided.

Cell reference -

b. Corresponding Call price using the Put-call parity

Where,

E = Exercise Price

S = Current underlying asset price

P = Put Premium

C = Call Premium

r = risk free rate

T =Time to maturity

putting the values

Hope this will help, please do comment if you need any further explanation. Your feedback would be highly appreciated.

Add Answer to:

Consider a European put option on a non-dividend-paying stock. The

current stock

price is $69, the...

Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price...

Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 25% per annum, and the time to maturity is four months. Use the Black-Scholes-Merton formula. What is the price of the option if it is a European call? What is the price of the option if it is an American call? What is the price of the option if it is...

What is the price of a European put option on a non-dividend-paying stock when the stock...

What is the price of a European put option on a non-dividend-paying stock when the stock price is $69, the strike price is $70, the risk-free interest rate is 5% per annum, the volatility is 35% per annum, and the time to maturity is six months?

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Consider an option on a non-dividend paying stock when the stock price is $90

Consider an option on a non-dividend paying stock when the stock price is $90, the exercise price is $98 the risk-free rate is 7% per annum, the volatility is 49% per annum, and the time to maturity is 9-months. a. Compute the prices of Call and Put option on the stock using Black & Scholes formula. b. Using above information, does put-call parity hold? Why?c. What happens if put-call parity does not hold?

What is the price of a European put option on a non-dividend paying stock when the...

What is the price of a European put option on a non-dividend paying stock when the stock price is $69, the strike price is $70, the risk-free interest rate is 5% per annum, the volatility is 35%per annum, and the time to maturity is six months? Please give me step by step by step instructions.

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Problem 1. 1. Calculate the price of a six-month European put option on a non-dividend-paying stock...

Problem 1. 1. Calculate the price of a six-month European put option on a non-dividend-paying stock with an exercise price of $90 when the current stock price is $100, the annualized riskless rate of interest is 3%, and the volatility is 40% per year. 2. Calculate the price of a six-month European call option with an exercise price on this same stock a non-dividend-paying stock with an exercise price of $90. Problem 2. Re-calculate the put and call option prices...

6) Consider an option on a non-dividend paying stock when the stock price is $38, the exercise price is $40, the risk-free interest rate is 6% per annum, the volatility is 30% per annum, and the time...

6) Consider an option on a non-dividend paying stock when the stock price is $38, the exercise price is $40, the risk-free interest rate is 6% per annum, the volatility is 30% per annum, and the time to maturity is six months. Using Black-Scholes Model, calculating manually, a. What is the price of the option if it is a European call? b. What is the price of the option if it is a European put? c. Show that the put-call...

(a) State the Black-Scholes formulas for the prices at time 0 of a European call and put options on a non-dividend-paying stock ABC

2. (a) State the Black-Scholes formulas for the prices at time 0 of a European call and put options on a non-dividend-paying stock ABC.(b) Consider an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 20% per annum, and the time to maturity is 5 months. What is the price of the option if it is a European call?

QUESTION # 10 Consider an option on a non-dividend paying stock when the stock price is...

QUESTION # 10 Consider an option on a non-dividend paying stock when the stock price is $90, the exercise price is $98 the risk-free rate is 7% per annum, the volatility is 49% per annum, and the time to maturity is 9-months. a. Compute the prices of Call and Put option on the stock using Black & Scholes formula. b. Using above information, does put-call parity hold? Why?-dNCa) c. What happens if put-call parity does not hold? [Max. Marks =...

QUESTION # 10 Consider an option on a non-dividend paying stock when the stock price is $90, the exercise price is $98 the risk-free rate is 7% per annum, the volatility is 49% per annum, and the time to maturity is 9-months. a. Compute the prices of Call and Put option on the stock using Black & Scholes formula. b. Using above information, does put-call parity hold? Why?-dNCa) c. What happens if put-call parity does not hold? [Max. Marks =...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

QUESTION # 10 Consider an option on a non-dividend paying stock when the stock price is $90, the exercise price is $98 the risk-free rate is 7% per annum, the volatility is 49% per annum, and the time to maturity is 9-months. a. Compute the prices of Call and Put option on the stock using Black & Scholes formula. b. Using above information, does put-call parity hold? Why?-dNCa) c. What happens if put-call parity does not hold? [Max. Marks =...

QUESTION # 10 Consider an option on a non-dividend paying stock when the stock price is $90, the exercise price is $98 the risk-free rate is 7% per annum, the volatility is 49% per annum, and the time to maturity is 9-months. a. Compute the prices of Call and Put option on the stock using Black & Scholes formula. b. Using above information, does put-call parity hold? Why?-dNCa) c. What happens if put-call parity does not hold? [Max. Marks =...

Most questions answered within 3 hours.

-

When an airplane is flying 200 mph at 5000-ft altitude in a

standard atmosphere, the air...

asked 6 minutes ago -

Consider the economy of Freeland, whose overall actual price

index and actual output are P and...

asked 20 minutes ago -

Your car is worth considerably less money than you owe.

This is an example of the...

asked 18 minutes ago -

Which Asian police agency discussed in class does not have a

citizenship requirement for police officers?...

asked 11 minutes ago -

A test tube with a suspension of cells that was diluted to 1:100

(DF 1/100). You...

asked 6 minutes ago -

Explore some of the new database technology including: NoSQL,

Hadoop, and IMDB. Discuss each item. Include...

asked 11 minutes ago -

Raleigh Department

Store uses the conventional retail method for the year ended

December 31, 2016. Available...

asked 17 minutes ago -

Calculate the entropy change for the hypothetical process in

which 0.5 g of ice at 0°C...

asked 18 minutes ago -

Suppose that the production function takes the form Q=L-0.7L^2.

In addition, marginal revenue is $10 and...

asked 26 minutes ago -

If you were in charge of the selection and purchase of a display

system for the...

asked 26 minutes ago -

I just took a final for chemistry 2. There were alot of

questions on cell potential....

asked 31 minutes ago -

In which region of the country did Methodists and

Baptists have the largest following?

a. The...

asked 31 minutes ago