Homework Answers

Please do rate me and mention doubts in the comments section

Add Answer to:

QUESTION # 10 Consider an option on a non-dividend paying stock when the stock price is...

Consider an option on a non-dividend paying stock when the stock price is $90

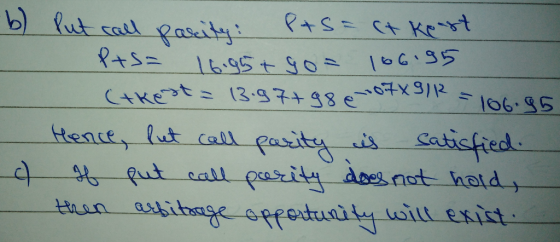

Consider an option on a non-dividend paying stock when the stock price is $90, the exercise price is $98 the risk-free rate is 7% per annum, the volatility is 49% per annum, and the time to maturity is 9-months. a. Compute the prices of Call and Put option on the stock using Black & Scholes formula. b. Using above information, does put-call parity hold? Why?c. What happens if put-call parity does not hold?

Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price...

Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 25% per annum, and the time to maturity is four months. Use the Black-Scholes-Merton formula. What is the price of the option if it is a European call? What is the price of the option if it is an American call? What is the price of the option if it is...

6) Consider an option on a non-dividend paying stock when the stock price is $38, the exercise price is $40, the risk-free interest rate is 6% per annum, the volatility is 30% per annum, and the time...

6) Consider an option on a non-dividend paying stock when the stock price is $38, the exercise price is $40, the risk-free interest rate is 6% per annum, the volatility is 30% per annum, and the time to maturity is six months. Using Black-Scholes Model, calculating manually, a. What is the price of the option if it is a European call? b. What is the price of the option if it is a European put? c. Show that the put-call...

Consider a European put option on a non-dividend-paying stock. The current stock price is $69, the...

Consider a European put option on a non-dividend-paying stock. The current stock price is $69, the strike price is $70, the risk-free interest rate is 5% per annum, the volatility is 35% per annum and the time to maturity is 6 months. a. Use the Black-Scholes model to calculate the put price. b. Calculate the corresponding call option using the put-call parity relation. Use the Option Calculator Spreadsheet to verify your result.

Problem 4.2 (15.30 in Hull) Consider an option on a non-dividend-paying stock when the stock price...

Problem 4.2 (15.30 in Hull) Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5%, the volatility is 25% per annum, and the time to maturity is 4 months. (a) what is the price of the option is it is a European call? (b) what is the price of the option if it is an American call? (c) what is the price of the option if...

Problem 4.2 (15.30 in Hull) Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5%, the volatility is 25% per annum, and the time to maturity is 4 months. (a) what is the price of the option is it is a European call? (b) what is the price of the option if it is an American call? (c) what is the price of the option if...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Consider an option on a non-dividend-paying stock when the stock price is $67

Consider an option on a non-dividend-paying stock when the stock price is $67, the exercise price is $61, the risk-free rate is 0.5%, the market volatility is 30% and the time to maturity is 6 months. Using the Black-Scholes Model when necessary:Given: Two dividend payments $1.75 and $2.75, two months and five months from now.(v) Compute the price of the option if it is an American Call (In Excel & show formulas).

(a) State the Black-Scholes formulas for the prices at time 0 of a European call and put options on a non-dividend-paying stock ABC

2. (a) State the Black-Scholes formulas for the prices at time 0 of a European call and put options on a non-dividend-paying stock ABC.(b) Consider an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 20% per annum, and the time to maturity is 5 months. What is the price of the option if it is a European call?

10. Use DerivaGem to complete this problem where you have an option on a non-dividend paying...

10. Use DerivaGem to complete this problem where you have an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 25% per annum, and the time to maturity is four months: a. What is the price of the option if it is a European call? b. What is the price of the option if it is an American call? c. What...

10. Use DerivaGem to complete this problem where you have an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 25% per annum, and the time to maturity is four months: a. What is the price of the option if it is a European call? b. What is the price of the option if it is an American call? c. What...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Problem 4.2 (15.30 in Hull) Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5%, the volatility is 25% per annum, and the time to maturity is 4 months. (a) what is the price of the option is it is a European call? (b) what is the price of the option if it is an American call? (c) what is the price of the option if...

Problem 4.2 (15.30 in Hull) Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5%, the volatility is 25% per annum, and the time to maturity is 4 months. (a) what is the price of the option is it is a European call? (b) what is the price of the option if it is an American call? (c) what is the price of the option if...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

10. Use DerivaGem to complete this problem where you have an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 25% per annum, and the time to maturity is four months: a. What is the price of the option if it is a European call? b. What is the price of the option if it is an American call? c. What...

10. Use DerivaGem to complete this problem where you have an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 25% per annum, and the time to maturity is four months: a. What is the price of the option if it is a European call? b. What is the price of the option if it is an American call? c. What...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Most questions answered within 3 hours.

-

Le Terroir Winery is considering an expansion project to produce

fine wines. The trial expansion will...

asked 1 minute ago -

The Bahraini public budget experiences deficit in the last

seven years, what are procedures are taken...

asked 8 minutes ago -

You invested $30,000 in a mutual fund at the beginning of the

year when the NAV...

asked 12 minutes ago -

Would you expect the price elasticity of supply for guitars to

be more inelastic in the...

asked 14 minutes ago -

A snowmobile is originally at the point with position vector

30.1 m at 95.0° counterclockwise from...

asked 13 minutes ago -

MAN3240 Organizational Behavior

In one to two paragraphs

6.) How can understanding emotions make me more...

asked 22 minutes ago -

Identify one individual who, in your opinion, is an excellent

leader. List the qualities that this...

asked 19 minutes ago -

For the data set shown below, complete parts (a) through (d)

below. x 3 4 5...

asked 25 minutes ago -

A university administrator working in student housing wants to

determine if the percentage of students residing...

asked 39 minutes ago -

3). Describe human population growth that has occurred in the

past 400 years. Use terms learned...

asked 36 minutes ago -

A

projectile is blue at a target. The distance from the point of

impact to the...

asked 1 hour ago -

Given a 32 bit processor, with 2 MB of physical RAM split into 512

frames. What...

asked 51 minutes ago