Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price...

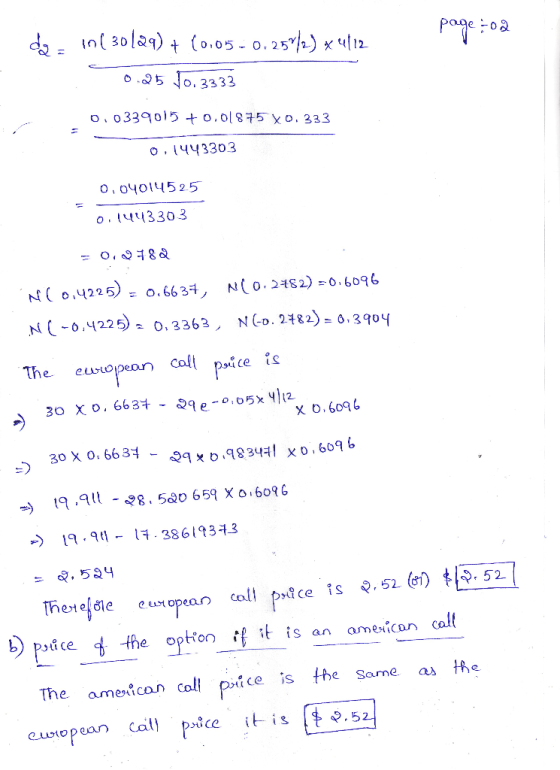

Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 25% per annum, and the time to maturity is four months. Use the Black-Scholes-Merton formula.

- What is the price of the option if it is a European call?

- What is the price of the option if it is an American call?

- What is the price of the option if it is a European put?

- Verify that put–call parity holds.

Homework Answers

The present value of the dividend must be subtracted from the stock price.

Add Answer to:

Consider an option on a

non-dividend-paying stock when the stock price is $30, the exercise

price...

Problem 4.2 (15.30 in Hull) Consider an option on a non-dividend-paying stock when the stock price...

Problem 4.2 (15.30 in Hull) Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5%, the volatility is 25% per annum, and the time to maturity is 4 months. (a) what is the price of the option is it is a European call? (b) what is the price of the option if it is an American call? (c) what is the price of the option if...

Problem 4.2 (15.30 in Hull) Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5%, the volatility is 25% per annum, and the time to maturity is 4 months. (a) what is the price of the option is it is a European call? (b) what is the price of the option if it is an American call? (c) what is the price of the option if...

6) Consider an option on a non-dividend paying stock when the stock price is $38, the exercise price is $40, the risk-free interest rate is 6% per annum, the volatility is 30% per annum, and the time...

6) Consider an option on a non-dividend paying stock when the stock price is $38, the exercise price is $40, the risk-free interest rate is 6% per annum, the volatility is 30% per annum, and the time to maturity is six months. Using Black-Scholes Model, calculating manually, a. What is the price of the option if it is a European call? b. What is the price of the option if it is a European put? c. Show that the put-call...

Consider an option on a non-dividend paying stock when the stock price is $90

Consider an option on a non-dividend paying stock when the stock price is $90, the exercise price is $98 the risk-free rate is 7% per annum, the volatility is 49% per annum, and the time to maturity is 9-months. a. Compute the prices of Call and Put option on the stock using Black & Scholes formula. b. Using above information, does put-call parity hold? Why?c. What happens if put-call parity does not hold?

Consider a European put option on a non-dividend-paying stock. The current stock price is $69, the...

Consider a European put option on a non-dividend-paying stock. The current stock price is $69, the strike price is $70, the risk-free interest rate is 5% per annum, the volatility is 35% per annum and the time to maturity is 6 months. a. Use the Black-Scholes model to calculate the put price. b. Calculate the corresponding call option using the put-call parity relation. Use the Option Calculator Spreadsheet to verify your result.

10. Use DerivaGem to complete this problem where you have an option on a non-dividend paying...

10. Use DerivaGem to complete this problem where you have an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 25% per annum, and the time to maturity is four months: a. What is the price of the option if it is a European call? b. What is the price of the option if it is an American call? c. What...

10. Use DerivaGem to complete this problem where you have an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 25% per annum, and the time to maturity is four months: a. What is the price of the option if it is a European call? b. What is the price of the option if it is an American call? c. What...

QUESTION # 10 Consider an option on a non-dividend paying stock when the stock price is...

QUESTION # 10 Consider an option on a non-dividend paying stock when the stock price is $90, the exercise price is $98 the risk-free rate is 7% per annum, the volatility is 49% per annum, and the time to maturity is 9-months. a. Compute the prices of Call and Put option on the stock using Black & Scholes formula. b. Using above information, does put-call parity hold? Why?-dNCa) c. What happens if put-call parity does not hold? [Max. Marks =...

QUESTION # 10 Consider an option on a non-dividend paying stock when the stock price is $90, the exercise price is $98 the risk-free rate is 7% per annum, the volatility is 49% per annum, and the time to maturity is 9-months. a. Compute the prices of Call and Put option on the stock using Black & Scholes formula. b. Using above information, does put-call parity hold? Why?-dNCa) c. What happens if put-call parity does not hold? [Max. Marks =...

Problem 1. 1. Calculate the price of a six-month European put option on a non-dividend-paying stock...

Problem 1. 1. Calculate the price of a six-month European put option on a non-dividend-paying stock with an exercise price of $90 when the current stock price is $100, the annualized riskless rate of interest is 3%, and the volatility is 40% per year. 2. Calculate the price of a six-month European call option with an exercise price on this same stock a non-dividend-paying stock with an exercise price of $90. Problem 2. Re-calculate the put and call option prices...

(a) State the Black-Scholes formulas for the prices at time 0 of a European call and put options on a non-dividend-paying stock ABC

2. (a) State the Black-Scholes formulas for the prices at time 0 of a European call and put options on a non-dividend-paying stock ABC.(b) Consider an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 20% per annum, and the time to maturity is 5 months. What is the price of the option if it is a European call?

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Please shown in steps,thank you! QUESTION 16 Consider an option on a non-dividend paying stock when...

Please shown in steps,thank you!

QUESTION 16 Consider an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5%, the volatility is 25% per annum, and the time to maturity is four months. What is the price of the option if it is a European call? QUESTION 17 Use the same information as in the previous question. What is the price of the option if it is...

Please shown in steps,thank you!

QUESTION 16 Consider an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5%, the volatility is 25% per annum, and the time to maturity is four months. What is the price of the option if it is a European call? QUESTION 17 Use the same information as in the previous question. What is the price of the option if it is...

Problem 4.2 (15.30 in Hull) Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5%, the volatility is 25% per annum, and the time to maturity is 4 months. (a) what is the price of the option is it is a European call? (b) what is the price of the option if it is an American call? (c) what is the price of the option if...

Problem 4.2 (15.30 in Hull) Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5%, the volatility is 25% per annum, and the time to maturity is 4 months. (a) what is the price of the option is it is a European call? (b) what is the price of the option if it is an American call? (c) what is the price of the option if...

10. Use DerivaGem to complete this problem where you have an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 25% per annum, and the time to maturity is four months: a. What is the price of the option if it is a European call? b. What is the price of the option if it is an American call? c. What...

10. Use DerivaGem to complete this problem where you have an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 25% per annum, and the time to maturity is four months: a. What is the price of the option if it is a European call? b. What is the price of the option if it is an American call? c. What...

QUESTION # 10 Consider an option on a non-dividend paying stock when the stock price is $90, the exercise price is $98 the risk-free rate is 7% per annum, the volatility is 49% per annum, and the time to maturity is 9-months. a. Compute the prices of Call and Put option on the stock using Black & Scholes formula. b. Using above information, does put-call parity hold? Why?-dNCa) c. What happens if put-call parity does not hold? [Max. Marks =...

QUESTION # 10 Consider an option on a non-dividend paying stock when the stock price is $90, the exercise price is $98 the risk-free rate is 7% per annum, the volatility is 49% per annum, and the time to maturity is 9-months. a. Compute the prices of Call and Put option on the stock using Black & Scholes formula. b. Using above information, does put-call parity hold? Why?-dNCa) c. What happens if put-call parity does not hold? [Max. Marks =...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Please shown in steps,thank you!

QUESTION 16 Consider an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5%, the volatility is 25% per annum, and the time to maturity is four months. What is the price of the option if it is a European call? QUESTION 17 Use the same information as in the previous question. What is the price of the option if it is...

Please shown in steps,thank you!

QUESTION 16 Consider an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5%, the volatility is 25% per annum, and the time to maturity is four months. What is the price of the option if it is a European call? QUESTION 17 Use the same information as in the previous question. What is the price of the option if it is...

Most questions answered within 3 hours.

-

Please explain steps:

An 80 kg swimmer steps off a platform 10 m above the water...

asked 5 minutes ago -

A lottery exists where balls numbered 1 to 17 are placed in an

urn. To win,...

asked 8 minutes ago -

26) Briefly describe, using words or simple diagrams, the

chemiosmotic theory for coupling oxidation to phosphorylation...

asked 2 hours ago -

Suppose that XX is a random variable with mean 16 and standard

deviation 5 . Also...

asked 2 hours ago -

Calculate the number density of argon gas at a temperature of

24C and a pressure of...

asked 6 hours ago -

Alternative

Classification

How to Estimate

Probabilities from Data? ( For continuous Attributes)

And How to generate...

asked 6 hours ago -

An explosion breaks a 20.0-kg object into three parts. The

object is initially moving at a...

asked 6 hours ago -

Calculate the approximate number of residues of Rubisco, which

is involved in carbon fixation in plants,...

asked 7 hours ago -

Other decisions about scientific claims can have a much broader

impact.ENERGYarrow-10x10.png, environment, health, security - all...

asked 8 hours ago -

I need to write a research paper and work cited about this

topic: The United States...

asked 9 hours ago -

Hello! I was wondering if I could have some help?

If the vapor pressure of carvone...

asked 9 hours ago -

An economist wants to estimate the mean per capita income (in

thousands of dollars) for a...

asked 9 hours ago