Homework Answers

Add Answer to:

a firm in perfectly competitive market sells all its products

Q at constant price p

(1)A...

the firm faces a constant price (P) of $60 A firm in a perfectly competitive market...

the

firm faces a constant price (P) of $60

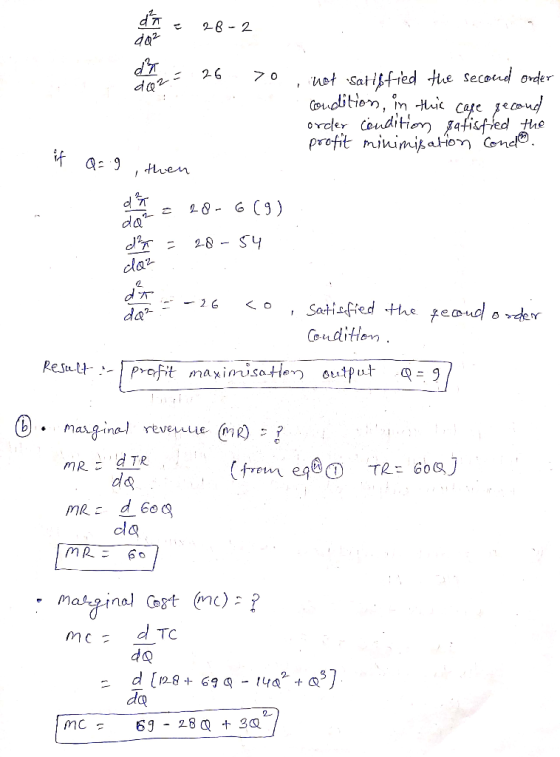

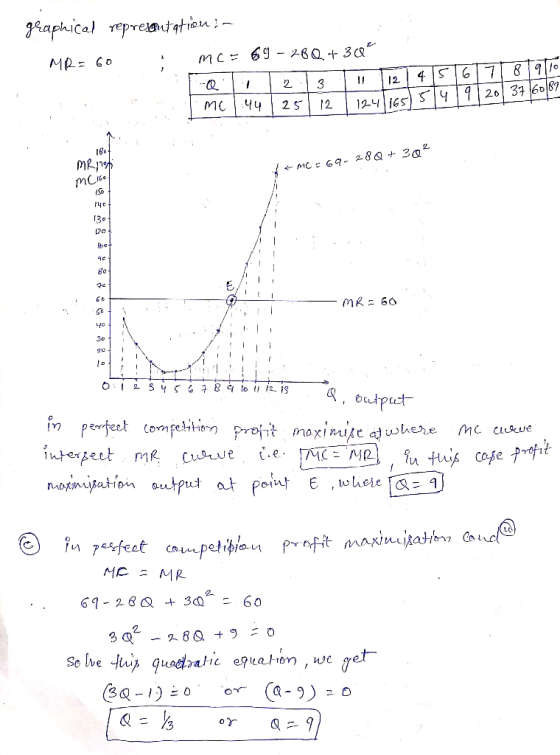

A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 TC(Q) = 128 + 69Q - 140 + Q (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at this...

the

firm faces a constant price (P) of $60

A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 TC(Q) = 128 + 69Q - 140 + Q (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at this...

Can you label each one please . (1)A firm in a perfectly competitive market sells all...

Can you label each one please .

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 TC(Q) 128+ 690-14Q + Q (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at this level of output. (b)Derive the marginal...

Can you label each one please .

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 TC(Q) 128+ 690-14Q + Q (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at this level of output. (b)Derive the marginal...

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price...

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 Q TC(Q) = 128 +690-140 (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at this level of output. (b)Derive the marginal revenue (MR) and the marginal cost(MC). Graph...

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 Q TC(Q) = 128 +690-140 (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at this level of output. (b)Derive the marginal revenue (MR) and the marginal cost(MC). Graph...

please answer all of the following questions since theyre all related (1)A firm in a perfectly...

please answer all of the following questions since theyre all

related

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 TC(Q) = 128 +69Q - 140 + Q (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at...

please answer all of the following questions since theyre all

related

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 TC(Q) = 128 +69Q - 140 + Q (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at...

please answer all of the following questions since theyre all related (1)A firm in a perfectly...

please answer all of the following questions since theyre all

related

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 TC(Q) = 128 +69Q - 140 + Q (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at...

please answer all of the following questions since theyre all

related

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 TC(Q) = 128 +69Q - 140 + Q (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at...

1) A perfectly competitive firm faces the following Total revenue, Total cost and Marginal cost functions:...

1) A perfectly competitive firm faces the following Total revenue, Total cost and Marginal cost functions: TR = 10Q TC = 2 + 2Q + Q2 MC = 2 + 2Q At the level of output maximizing profit , the above firm's level of economic profit is A) $0 B) $4 C) $6 D) $8 *Additional information after I did the math: The price this firm charges for its product is $10, the level of output maximizing profit is 4...

The market price is p=50 3. Consider a competitive firm with total costs given by TC(q)...

The market price is p=50

3. Consider a competitive firm with total costs given by TC(q) = 100 + 10q+q? (e) Graph the ATC, AVC, MC, and MR curves in a single graph, and indicate the profit maximizing level of output. If there are profits, shade the region corre- sponding to profit and label it. (f) If fixed costs increase from 100 to 500, what happens to the profit maximizing level of output, TR, TC, and a? (g) If fixed...

The market price is p=50

3. Consider a competitive firm with total costs given by TC(q) = 100 + 10q+q? (e) Graph the ATC, AVC, MC, and MR curves in a single graph, and indicate the profit maximizing level of output. If there are profits, shade the region corre- sponding to profit and label it. (f) If fixed costs increase from 100 to 500, what happens to the profit maximizing level of output, TR, TC, and a? (g) If fixed...

A price-taking firm in a perfectly competitive market faces a market price of $4. The firm's...

A price-taking firm in a perfectly competitive market faces a market price of $4. The firm's marginal cost function is MC(Q) = 2 + aQ, where "a" is a positive number. As "a" increases, the firm's profit-maximizing quantity increases, decreases, or does not change?

Consider a competitive firm with total costs given by TC(q) = 100 + 10q + q...

Consider a competitive firm with total costs given by TC(q) = 100 + 10q + q 2 The firm faces a market price p = 50. (d) Find the profit-maximizing level of output q^*. At this level of output, what are TR, TC, ATC, and π? (e) Graph the ATC, AVC, MC, and MR curves in a single graph, and indicate the profit-maximizing level of output. If there are profits, shade the region corresponding to profit and label it.

15. Use the following figure for a firm in a perfectly competitive market. a What is the output that maximizes...

15. Use the following figure for a firm in a perfectly competitive market. a What is the output that maximizes the firm's profit? b. At the profit-maximizing output, calculate total revenue and total cost. C. If the firm maximizes profit, how much profit does it earn? d. What will likely happen to market demand or market supply in the long run? e. What will likely happen to the market price in the long run? Price (s) d = P =...

15. Use the following figure for a firm in a perfectly competitive market. a What is the output that maximizes the firm's profit? b. At the profit-maximizing output, calculate total revenue and total cost. C. If the firm maximizes profit, how much profit does it earn? d. What will likely happen to market demand or market supply in the long run? e. What will likely happen to the market price in the long run? Price (s) d = P =...

the

firm faces a constant price (P) of $60

A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 TC(Q) = 128 + 69Q - 140 + Q (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at this...

the

firm faces a constant price (P) of $60

A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 TC(Q) = 128 + 69Q - 140 + Q (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at this...

Can you label each one please .

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 TC(Q) 128+ 690-14Q + Q (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at this level of output. (b)Derive the marginal...

Can you label each one please .

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 TC(Q) 128+ 690-14Q + Q (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at this level of output. (b)Derive the marginal...

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 Q TC(Q) = 128 +690-140 (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at this level of output. (b)Derive the marginal revenue (MR) and the marginal cost(MC). Graph...

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 Q TC(Q) = 128 +690-140 (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at this level of output. (b)Derive the marginal revenue (MR) and the marginal cost(MC). Graph...

please answer all of the following questions since theyre all

related

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 TC(Q) = 128 +69Q - 140 + Q (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at...

please answer all of the following questions since theyre all

related

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 TC(Q) = 128 +69Q - 140 + Q (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at...

please answer all of the following questions since theyre all

related

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 TC(Q) = 128 +69Q - 140 + Q (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at...

please answer all of the following questions since theyre all

related

(1)A firm in a perfectly competitive market sells all its product (Q) at a constant price (P) of $60. Suppose the total cost function (TC) for this firm is described by the following equation: 2 3 TC(Q) = 128 +69Q - 140 + Q (a)Form the profit function and determine the output that maximizes the firm's profit. Evaluate the second order condition to assure that profit is maximized at...

The market price is p=50

3. Consider a competitive firm with total costs given by TC(q) = 100 + 10q+q? (e) Graph the ATC, AVC, MC, and MR curves in a single graph, and indicate the profit maximizing level of output. If there are profits, shade the region corre- sponding to profit and label it. (f) If fixed costs increase from 100 to 500, what happens to the profit maximizing level of output, TR, TC, and a? (g) If fixed...

The market price is p=50

3. Consider a competitive firm with total costs given by TC(q) = 100 + 10q+q? (e) Graph the ATC, AVC, MC, and MR curves in a single graph, and indicate the profit maximizing level of output. If there are profits, shade the region corre- sponding to profit and label it. (f) If fixed costs increase from 100 to 500, what happens to the profit maximizing level of output, TR, TC, and a? (g) If fixed...

15. Use the following figure for a firm in a perfectly competitive market. a What is the output that maximizes the firm's profit? b. At the profit-maximizing output, calculate total revenue and total cost. C. If the firm maximizes profit, how much profit does it earn? d. What will likely happen to market demand or market supply in the long run? e. What will likely happen to the market price in the long run? Price (s) d = P =...

15. Use the following figure for a firm in a perfectly competitive market. a What is the output that maximizes the firm's profit? b. At the profit-maximizing output, calculate total revenue and total cost. C. If the firm maximizes profit, how much profit does it earn? d. What will likely happen to market demand or market supply in the long run? e. What will likely happen to the market price in the long run? Price (s) d = P =...

Most questions answered within 3 hours.

-

The blues made its way into many kinds of music. Eric Clapton,

The Beatles, and Elvis...

asked 1 hour ago -

8. A wave in a string has a wave function given by: y (x, t) =...

asked 1 hour ago -

If you’re standing at the bottom of a hill and asked to evaluate

it while being...

asked 2 hours ago -

1. Which region has taken the lead in the world of

e-waste handling?

a) European Union...

asked 2 hours ago -

A 8.15- g bullet from a 9-mm pistol has a velocity of 366.0 m/s.

It strikes...

asked 4 hours ago -

The outstanding bonds of Alpha Extracts have a yield to maturity

of 7.4 percent and a...

asked 4 hours ago -

The Problem: The Case of the Harmonizing Vacations

Your CEO is exploring partnering with a European...

asked 5 hours ago -

A chemical equation is balanced by adding coefficients in front

of some formulas so that the...

asked 5 hours ago -

From the literature (reference your sources): What are the

lattice parameters of calcite and aragonite? Why...

asked 6 hours ago -

Your system is rejecting the question am asking which is

preceded by a case study. It...

asked 6 hours ago -

3. On January 2, 2000, Larry creates a trust with himself as

trustee. Larry as trustee...

asked 6 hours ago -

A member of the volleyball team spikes the ball. During this

process, she changes the velocity...

asked 6 hours ago