1) Record the entry for credit losses.

2)Record the entry for fair value adjustment

Homework Answers

| Below answer based on IFRS 9 - Financial Instrument and treatment in | |||

| Income Statement as well as OCI , Along with fair value adjustment | |||

| As per Question , LED Corporation owns $1950000- Pharma Bonds | |||

| the market price of the Branch Bonds feel by $ 1400000 | |||

| due to companies principal drug | |||

| $ 100000- decline in value already included in OCI as temporary Unorganized | |||

| loss in prior period | |||

| $960,000 out of $ 1400,000 loss relates to Credit LOSS | |||

| $440,000 AS Non credit losses | |||

| Journal Entry | |||

| Deatils | Debit($) | Credit($) | |

| Oter than Temporary Impairment Loss ( Income /Statement) | 9,60,000 | ||

| Discount on Bond Investment ) Amortized) | 9,60,000 | ||

| LED to recognised the $960,0000 represents Credit Loss == need to | |||

| routed thourgh Income Statement | |||

| Balance

Non Credit Loss amount to $ 440000 routed through OCI and Fair

value adjustment |

|||

| Oter than Temporary Impairment Loss == OCI | 4,40,000 | ||

| Fair value Adjustment | 4,40,000 | ||

| Fair value Adjustment | 1,00,000 | ||

| Net Unrealized gain & losses | 1,00,000 | ||

| ( As

explained above , amount already included uner OCI as temporary

unrecognised loss relates to prior period |

|||

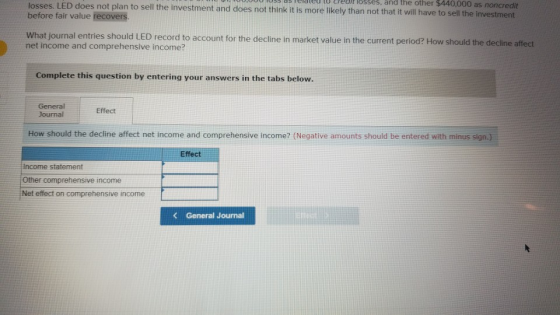

| Disclosure on Financial Statement | Amnt($) | ||

| Income Statement | -9,60,000 | ||

| Other Comprehensive Income | 3,40,000 | ||

| ($440,000-$100,000 | |||

| Net Effect on Comprehensibe Income | 13,00,000 | ||

| $960,000+$340,000 | |||

Add Answer to:

1) Record the entry for credit losses.

2)Record the entry for fair value adjustment

market price...

1. record entry for credit loss 2. record entry for fair value adjustment Help Save LED...

1. record entry for credit loss

2. record entry for fair value adjustment

Help Save LED Corporation owns $1.950,000 of Branch Pharmaceuticals bonds and classifies its investment as securities available for sale. The market price of Branch's bonds fell by $1,400,000, due to concerns about one of the company's principal drugs. The concerns were justified when the FDA banned the drug. $100,000 of that decline in value already had been included in Ocl as a temporary unrealized loss in a...

1. record entry for credit loss

2. record entry for fair value adjustment

Help Save LED Corporation owns $1.950,000 of Branch Pharmaceuticals bonds and classifies its investment as securities available for sale. The market price of Branch's bonds fell by $1,400,000, due to concerns about one of the company's principal drugs. The concerns were justified when the FDA banned the drug. $100,000 of that decline in value already had been included in Ocl as a temporary unrealized loss in a...

LED Corporation owns $1,050,000 of Branch Pharmaceuticals bonds and classifies its investment as securities available-for-sale. The...

LED Corporation owns $1,050,000 of Branch Pharmaceuticals bonds and classifies its investment as securities available-for-sale. The market price of Branch's bonds fell by $500,000, due to concerns about one of the company's principal drugs. The concerns were justified when the FDA banned the drug. $100,000 of that decline in value already had been included in OCI as a temporary unrealized loss in a prior period. LED views $240,000 of the $500,000 loss as related to credit losses, and the other...

LED Corporation owns $1,050,000 of Branch Pharmaceuticals bonds and classifies its investment as securities available-for-sale. The market price of Branch's bonds fell by $500,000, due to concerns about one of the company's principal drugs. The concerns were justified when the FDA banned the drug. $100,000 of that decline in value already had been included in OCI as a temporary unrealized loss in a prior period. LED views $240,000 of the $500,000 loss as related to credit losses, and the other...

LED Corporation owns $1,750,000 of Branch Pharmaceuticals bonds and classifies its investment as securities available-for-sale. The...

LED Corporation owns $1,750,000 of Branch Pharmaceuticals bonds and classifies its investment as securities available-for-sale. The market price of Branch’s bonds fell by $1,200,000, due to concerns about one of the company’s principal drugs. The concerns were justified when the FDA banned the drug. $100,000 of that decline in value already had been included in OCI as a temporary unrealized loss in a prior period. LED views $800,000 of the $1,200,000 loss as related to credit losses, and the other...

1) Record the entry for fair value adjustment of December 31, 2021. 2)Record the entry to...

1) Record the entry for fair value adjustment of

December 31, 2021.

2)Record the entry to adjust to fair value on the date

of sale

3) Record the entry to reverse the previous fair value

adjustment.

4) Record the entry for sale of investment in Coca

Cola bonds.

S&L Financial buys and sells securities which it classifies as available for sale. On December 27 2021. S&L purchased Coca-Cola bonds at par for $885,000 and sold the bonds on January 3,...

1) Record the entry for fair value adjustment of

December 31, 2021.

2)Record the entry to adjust to fair value on the date

of sale

3) Record the entry to reverse the previous fair value

adjustment.

4) Record the entry for sale of investment in Coca

Cola bonds.

S&L Financial buys and sells securities which it classifies as available for sale. On December 27 2021. S&L purchased Coca-Cola bonds at par for $885,000 and sold the bonds on January 3,...

Exercise 12-3 Bloom Corporation purchased $1,900,000 of Taylor Company 5% bonds at par and classifies their investm...

Exercise 12-3 Bloom Corporation purchased $1,900,000 of Taylor Company 5% bonds at par and classifies their investment as AFS, Unfortunately, a combination of problems at Taylor Company and in the debt market caused the fair value of the Taylor investment to decline to $1,320,000 during 2018. Consider each of the following as independent situation. 1. Bloom now believes it is more likely than not that it will have to sell the Taylor bonds before the bonds have a chance to...

Exercise 12-3 Bloom Corporation purchased $1,900,000 of Taylor Company 5% bonds at par and classifies their investment as AFS, Unfortunately, a combination of problems at Taylor Company and in the debt market caused the fair value of the Taylor investment to decline to $1,320,000 during 2018. Consider each of the following as independent situation. 1. Bloom now believes it is more likely than not that it will have to sell the Taylor bonds before the bonds have a chance to...

1. Record the investment 2. Record the investment revenue realized. 3. Record the fair value adjustment....

1. Record the investment

2. Record the investment revenue realized.

3. Record the fair value adjustment.

He Turner Company purchased 35% of the outstanding stock of ICA Company for $11,800,000 on January 2, 2021. Turner elects the fair value option to account for the investment. During 2021, ICA reports $930,000 of net income and on December 30 pays a dividend of $680,000. On December 31, 2021, the fair value of Turner's investment has increased to $15,100,000. Prepare the journal entries...

1. Record the investment

2. Record the investment revenue realized.

3. Record the fair value adjustment.

He Turner Company purchased 35% of the outstanding stock of ICA Company for $11,800,000 on January 2, 2021. Turner elects the fair value option to account for the investment. During 2021, ICA reports $930,000 of net income and on December 30 pays a dividend of $680,000. On December 31, 2021, the fair value of Turner's investment has increased to $15,100,000. Prepare the journal entries...

Exercise 12-30 Held-to-maturity securities; impairments (Appendix 128) [LO12-2, 12-8] Bloom Corporation purchased $1.200,000 of Taylor Company...

Exercise 12-30 Held-to-maturity securities; impairments (Appendix 128) [LO12-2, 12-8] Bloom Corporation purchased $1.200,000 of Taylor Company 5% bonds at par with the intent and ability to hold the bonds until they matured in 2025, so Bloom Classifies their investment as HTM. Unfortunately, a combination of problems at Taylor Company and in the debt market caused the fair value of the Taylor investment to decline to $760,000 during 2018. Consider each of the following as an Independent situation 1. Bloom now...

Exercise 12-30 Held-to-maturity securities; impairments (Appendix 128) [LO12-2, 12-8] Bloom Corporation purchased $1.200,000 of Taylor Company 5% bonds at par with the intent and ability to hold the bonds until they matured in 2025, so Bloom Classifies their investment as HTM. Unfortunately, a combination of problems at Taylor Company and in the debt market caused the fair value of the Taylor investment to decline to $760,000 during 2018. Consider each of the following as an Independent situation 1. Bloom now...

2 Part 2 Homework i Seved Bloom Corporation purchased $1,000,000 of Taylor Company 5% bonds at...

2 Part 2 Homework i Seved Bloom Corporation purchased $1,000,000 of Taylor Company 5% bonds at their face amount, with the intent and ability to hold the bonds until they matured in 2025, so Bloom classifies its investment as HTM. Unfortunately, a combination of problems at Taylor Company and in the debt securities market caused the fair value of the Taylor investment to decline to $600,000 during 2021 The following are the two alternative scenarios that should be analyzed independent...

2 Part 2 Homework i Seved Bloom Corporation purchased $1,000,000 of Taylor Company 5% bonds at their face amount, with the intent and ability to hold the bonds until they matured in 2025, so Bloom classifies its investment as HTM. Unfortunately, a combination of problems at Taylor Company and in the debt securities market caused the fair value of the Taylor investment to decline to $600,000 during 2021 The following are the two alternative scenarios that should be analyzed independent...

Question #2 The following are the cost and fair value for a debt investment (Available to...

Question #2 The following are the cost and fair value for a debt investment (Available to December 31, 2020. of investment Available for Sale) on Fair Value Debt Investment - Available for Sale Cost 10,000,000 $ $ 9,000,000 Assume the company had Net Income of $620,000 at the end of 2020 Required: 1) Calculate the Unrealized Holding Gains and Losses. 2) Does the Unrealized Holding Gains and Losses affect the Income Statement or Balance Sheet 3) Prepare the journal entry...

Question #2 The following are the cost and fair value for a debt investment (Available to December 31, 2020. of investment Available for Sale) on Fair Value Debt Investment - Available for Sale Cost 10,000,000 $ $ 9,000,000 Assume the company had Net Income of $620,000 at the end of 2020 Required: 1) Calculate the Unrealized Holding Gains and Losses. 2) Does the Unrealized Holding Gains and Losses affect the Income Statement or Balance Sheet 3) Prepare the journal entry...

Bloom Corporation purchased $1,750,000 of Taylor Company 5% bonds, at their face amount, with the intent...

Bloom Corporation purchased $1,750,000 of Taylor Company 5% bonds, at their face amount, with the intent and ability to hold the bonds until they matured in 2025, so Bloom classifies its investment as AFS. Unfortunately, a combination of problems at Taylor Company and in the debt securities market caused the fair value of the Taylor investment to decline to $1,200,000 during 2021. The following are the two alternative scenarios that should be analyzed independent of each other. 1. Bloom now...

Bloom Corporation purchased $1,750,000 of Taylor Company 5% bonds, at their face amount, with the intent and ability to hold the bonds until they matured in 2025, so Bloom classifies its investment as AFS. Unfortunately, a combination of problems at Taylor Company and in the debt securities market caused the fair value of the Taylor investment to decline to $1,200,000 during 2021. The following are the two alternative scenarios that should be analyzed independent of each other. 1. Bloom now...

1. record entry for credit loss

2. record entry for fair value adjustment

Help Save LED Corporation owns $1.950,000 of Branch Pharmaceuticals bonds and classifies its investment as securities available for sale. The market price of Branch's bonds fell by $1,400,000, due to concerns about one of the company's principal drugs. The concerns were justified when the FDA banned the drug. $100,000 of that decline in value already had been included in Ocl as a temporary unrealized loss in a...

1. record entry for credit loss

2. record entry for fair value adjustment

Help Save LED Corporation owns $1.950,000 of Branch Pharmaceuticals bonds and classifies its investment as securities available for sale. The market price of Branch's bonds fell by $1,400,000, due to concerns about one of the company's principal drugs. The concerns were justified when the FDA banned the drug. $100,000 of that decline in value already had been included in Ocl as a temporary unrealized loss in a...

LED Corporation owns $1,050,000 of Branch Pharmaceuticals bonds and classifies its investment as securities available-for-sale. The market price of Branch's bonds fell by $500,000, due to concerns about one of the company's principal drugs. The concerns were justified when the FDA banned the drug. $100,000 of that decline in value already had been included in OCI as a temporary unrealized loss in a prior period. LED views $240,000 of the $500,000 loss as related to credit losses, and the other...

LED Corporation owns $1,050,000 of Branch Pharmaceuticals bonds and classifies its investment as securities available-for-sale. The market price of Branch's bonds fell by $500,000, due to concerns about one of the company's principal drugs. The concerns were justified when the FDA banned the drug. $100,000 of that decline in value already had been included in OCI as a temporary unrealized loss in a prior period. LED views $240,000 of the $500,000 loss as related to credit losses, and the other...

1) Record the entry for fair value adjustment of

December 31, 2021.

2)Record the entry to adjust to fair value on the date

of sale

3) Record the entry to reverse the previous fair value

adjustment.

4) Record the entry for sale of investment in Coca

Cola bonds.

S&L Financial buys and sells securities which it classifies as available for sale. On December 27 2021. S&L purchased Coca-Cola bonds at par for $885,000 and sold the bonds on January 3,...

1) Record the entry for fair value adjustment of

December 31, 2021.

2)Record the entry to adjust to fair value on the date

of sale

3) Record the entry to reverse the previous fair value

adjustment.

4) Record the entry for sale of investment in Coca

Cola bonds.

S&L Financial buys and sells securities which it classifies as available for sale. On December 27 2021. S&L purchased Coca-Cola bonds at par for $885,000 and sold the bonds on January 3,...

Exercise 12-3 Bloom Corporation purchased $1,900,000 of Taylor Company 5% bonds at par and classifies their investment as AFS, Unfortunately, a combination of problems at Taylor Company and in the debt market caused the fair value of the Taylor investment to decline to $1,320,000 during 2018. Consider each of the following as independent situation. 1. Bloom now believes it is more likely than not that it will have to sell the Taylor bonds before the bonds have a chance to...

Exercise 12-3 Bloom Corporation purchased $1,900,000 of Taylor Company 5% bonds at par and classifies their investment as AFS, Unfortunately, a combination of problems at Taylor Company and in the debt market caused the fair value of the Taylor investment to decline to $1,320,000 during 2018. Consider each of the following as independent situation. 1. Bloom now believes it is more likely than not that it will have to sell the Taylor bonds before the bonds have a chance to...

1. Record the investment

2. Record the investment revenue realized.

3. Record the fair value adjustment.

He Turner Company purchased 35% of the outstanding stock of ICA Company for $11,800,000 on January 2, 2021. Turner elects the fair value option to account for the investment. During 2021, ICA reports $930,000 of net income and on December 30 pays a dividend of $680,000. On December 31, 2021, the fair value of Turner's investment has increased to $15,100,000. Prepare the journal entries...

1. Record the investment

2. Record the investment revenue realized.

3. Record the fair value adjustment.

He Turner Company purchased 35% of the outstanding stock of ICA Company for $11,800,000 on January 2, 2021. Turner elects the fair value option to account for the investment. During 2021, ICA reports $930,000 of net income and on December 30 pays a dividend of $680,000. On December 31, 2021, the fair value of Turner's investment has increased to $15,100,000. Prepare the journal entries...

Exercise 12-30 Held-to-maturity securities; impairments (Appendix 128) [LO12-2, 12-8] Bloom Corporation purchased $1.200,000 of Taylor Company 5% bonds at par with the intent and ability to hold the bonds until they matured in 2025, so Bloom Classifies their investment as HTM. Unfortunately, a combination of problems at Taylor Company and in the debt market caused the fair value of the Taylor investment to decline to $760,000 during 2018. Consider each of the following as an Independent situation 1. Bloom now...

Exercise 12-30 Held-to-maturity securities; impairments (Appendix 128) [LO12-2, 12-8] Bloom Corporation purchased $1.200,000 of Taylor Company 5% bonds at par with the intent and ability to hold the bonds until they matured in 2025, so Bloom Classifies their investment as HTM. Unfortunately, a combination of problems at Taylor Company and in the debt market caused the fair value of the Taylor investment to decline to $760,000 during 2018. Consider each of the following as an Independent situation 1. Bloom now...

2 Part 2 Homework i Seved Bloom Corporation purchased $1,000,000 of Taylor Company 5% bonds at their face amount, with the intent and ability to hold the bonds until they matured in 2025, so Bloom classifies its investment as HTM. Unfortunately, a combination of problems at Taylor Company and in the debt securities market caused the fair value of the Taylor investment to decline to $600,000 during 2021 The following are the two alternative scenarios that should be analyzed independent...

2 Part 2 Homework i Seved Bloom Corporation purchased $1,000,000 of Taylor Company 5% bonds at their face amount, with the intent and ability to hold the bonds until they matured in 2025, so Bloom classifies its investment as HTM. Unfortunately, a combination of problems at Taylor Company and in the debt securities market caused the fair value of the Taylor investment to decline to $600,000 during 2021 The following are the two alternative scenarios that should be analyzed independent...

Question #2 The following are the cost and fair value for a debt investment (Available to December 31, 2020. of investment Available for Sale) on Fair Value Debt Investment - Available for Sale Cost 10,000,000 $ $ 9,000,000 Assume the company had Net Income of $620,000 at the end of 2020 Required: 1) Calculate the Unrealized Holding Gains and Losses. 2) Does the Unrealized Holding Gains and Losses affect the Income Statement or Balance Sheet 3) Prepare the journal entry...

Question #2 The following are the cost and fair value for a debt investment (Available to December 31, 2020. of investment Available for Sale) on Fair Value Debt Investment - Available for Sale Cost 10,000,000 $ $ 9,000,000 Assume the company had Net Income of $620,000 at the end of 2020 Required: 1) Calculate the Unrealized Holding Gains and Losses. 2) Does the Unrealized Holding Gains and Losses affect the Income Statement or Balance Sheet 3) Prepare the journal entry...

Bloom Corporation purchased $1,750,000 of Taylor Company 5% bonds, at their face amount, with the intent and ability to hold the bonds until they matured in 2025, so Bloom classifies its investment as AFS. Unfortunately, a combination of problems at Taylor Company and in the debt securities market caused the fair value of the Taylor investment to decline to $1,200,000 during 2021. The following are the two alternative scenarios that should be analyzed independent of each other. 1. Bloom now...

Bloom Corporation purchased $1,750,000 of Taylor Company 5% bonds, at their face amount, with the intent and ability to hold the bonds until they matured in 2025, so Bloom classifies its investment as AFS. Unfortunately, a combination of problems at Taylor Company and in the debt securities market caused the fair value of the Taylor investment to decline to $1,200,000 during 2021. The following are the two alternative scenarios that should be analyzed independent of each other. 1. Bloom now...

Most questions answered within 3 hours.

-

Humans have used horses for transportation for millions of

years. Therefore, they will use horses for...

asked 18 minutes ago -

The following are the Jensen Corporation's unit costs of making

and selling an item at a...

asked 53 minutes ago -

Does direct Medicare reimbursement of Advanced practice nurses

increase access to their services?

asked 1 hour ago -

List and explain why a company would choose to use a

published

compensation survey vs. creating...

asked 1 hour ago -

A discrete random variable X can take values from 1 to 10. Find

the variance of...

asked 2 hours ago -

The primary financial goal of a corporation is to maximize:

shareholders wealth.

earnings per share.

stock...

asked 2 hours ago -

determine whether the vectors u=(1,2,3,), v=(-2,1,0) and

w=(1,0,1) are linearly dependent or independent.

asked 2 hours ago -

python

Define a function called print_values which takes a dictionary

object as a parameter. The function...

asked 3 hours ago -

In Chapter 1 you created a program named Triangle in

which you displayed a seven-line triangle...

asked 3 hours ago -

Research question: What are the differences between separately

stated and non separately stated transactions in an...

asked 3 hours ago -

By using Arduino write a code that connects two LEDs to two

push-buttons. Each button controls...

asked 4 hours ago -

Bank of America has bonds that pay a coupon interest rate of 5.5

percent and mature...

asked 5 hours ago