Option #2: Applying Activity Based Costing #5-8.

Homework Answers

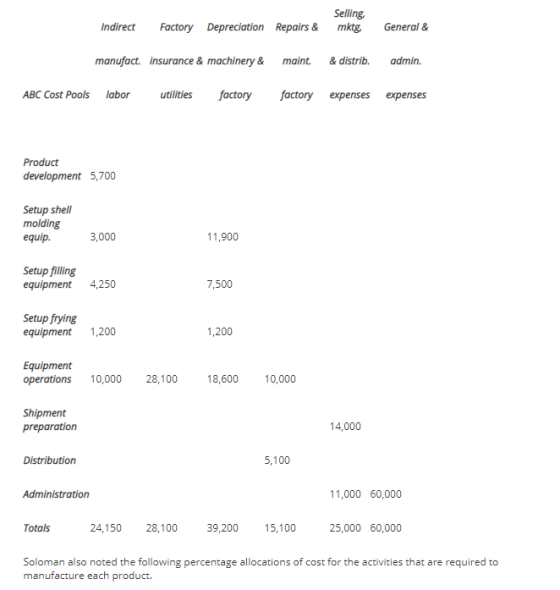

| ABC allocation: | ||||

| Cost | Total Amount | Bean&Cheese | Shredded Beef | |

| Prod Devel | 5700 | 1140 | 4560 | |

| Setup shell mol | 14900 | 8940 | 5960 | |

| Setup filling eq | 11750 | 5875 | 5875 | |

| Setup frying eq | 2400 | 1200 | 1200 | |

| Eq. operation | 66700 | 50025 | 16675 | |

| Shipment prep. | 14000 | 9800 | 4200 | |

| Distri. | 5100 | 3315 | 1785 | |

| Admin. | 71000 | 35500 | 35500 | |

| Total overhead | 191550 | 115795 | 75755 | |

| Traditional Method of allocation: | ||||

| Selling Price | 1.95 | 2.99 | ||

| Less:Direct Vari cost: | 0.75 | 1.25 | ||

| Contribution per unit | 1.2 | 1.74 | ||

| Volume of sale | 300000 | 200000 | ||

| total Contribution | 360000 | 348000 | ||

| Less: Allocated cost | 95775 | 95775 | ||

| Net Profit | 264225 | 252225 | ||

| Profitability | Higher | |||

| ABC Method of allocation: | ||||

| Selling Price | 1.95 | 2.99 | ||

| Less:Direct Vari cost: | 0.75 | 1.25 | ||

| Contribution per unit | 1.2 | 1.74 | ||

| Volume of sale | 300000 | 200000 | ||

| total Contribution | 360000 | 348000 | ||

| Less: Allocated cost | 115795 | 75755 | ||

| Net Profit | 244205 | 272245 | ||

| Profitability | Higher | |||

| Bean&Cheese | Shredded Beef | |||

| 5) Unit cost under ABC: | ||||

| Direct cost | 0.75 | 1.25 | ||

| Allocated OH | 0.39 | 0.38 | ||

| Total Unit cost | 1.14 | 1.63 | ||

| Bean&Cheese | Shredded Beef | |||

| 6) | ||||

| Selling Price | 1.95 | 2.99 | ||

| Less:Direct Vari cost: | 0.75 | 1.25 | ||

| Contribution per unit | 1.2 | 1.74 | ||

| Volume of sale | 300000 | 200000 | ||

| total Contribution | 360000 | 348000 | ||

| Less: Allocated cost | 115795 | 75755 | ||

| Net Profit | 244205 | 272245 | ||

| 7) Net Profit: | ||||

| As per Traditional | 264225 | 252225 | ||

| As per ABC | 244205 | 272245 | ||

| Difference | 20020 | -20020 | ||

| Under, the traditional method of allocation, the Bean & Cheese | ||||

| have the higher Net Profit whereas in the ABC method of allocation | ||||

| the Shredded Beef carries the higher Net Profit because as per | ||||

| micro allocation of overhead under ABC method, Shredded Beef | ||||

| is consuming less overhead to Bean & Cheese. | ||||

| 8) Soloman had delivered to management because Shredded Beef | ||||

| has been consuming less overhead to Bean & Cheese, which has | ||||

| not being recognised in the Traditional method of overhead allocation, | ||||

| where overhead is allocated on the number of hours devoted to each | ||||

| product ie. equally distributed. | ||||

| The bifercation of the overhead according to the activities and distributing | ||||

| it as per consumption of each activity by each product in production would | ||||

| allocate the cost properly between the products. Thus, the ABC method | ||||

| has been best choosen to allocate overhead to Traditional method of | ||||

| overhead allocation. | ||||

Add Answer to:

Option #2: Applying Activity Based Costing

#5-8.

Option #2: Applying Activity-Based Costing South of the Border's...

Activity Based Costing 1 Chapter 3: Applying Excel Fra formulato each of the cols marked when...

Activity Based Costing 1 Chapter 3: Applying Excel Fra formulato each of the cols marked when Review Problem. Activity Based Couting 6 Data Annual sales in units 9 Direct materials per unit 10 Direct labor hours per unit 2000 Tourist 10 000 $25 517 12 Direct labor rate 512 per DUH Overhead Expected Activity 16 Activities and Activity Measures 17 Labor-related (direct labor hours) 19 Machine setups (setups) 19 Production orders (orders) 20 General factory (machine hours) $ 80.000 150.000...

Activity Based Costing 1 Chapter 3: Applying Excel Fra formulato each of the cols marked when Review Problem. Activity Based Couting 6 Data Annual sales in units 9 Direct materials per unit 10 Direct labor hours per unit 2000 Tourist 10 000 $25 517 12 Direct labor rate 512 per DUH Overhead Expected Activity 16 Activities and Activity Measures 17 Labor-related (direct labor hours) 19 Machine setups (setups) 19 Production orders (orders) 20 General factory (machine hours) $ 80.000 150.000...

Mastery Problem: Activity-Based Costing (Advanced) Activity-Based Costing Traditionally, Overhead cost: Sometimes referred to as "factory overhead,"...

Mastery Problem: Activity-Based Costing (Advanced) Activity-Based Costing Traditionally, Overhead cost: Sometimes referred to as "factory overhead," this is an indirect cost that is not directly tied to the production of units, yet nonetheless must be built into product cost in order to appropriately price it. Examples are managerial salaries, rent expense, setup costs, and property taxes.overhead costs are assigned based arbitrarily on the rate of either Direct labor: This is a labor cost directly associated with the production of goods...

Lamer Corporation is a diversified manufacturer of industrial goods. The company's activity-based costing system contains the...

Lamer Corporation is a diversified manufacturer of industrial goods. The company's activity-based costing system contains the following six activity cost pools and activity rates activity cost Pool Labor related Machine-related Machine setups Production orders Shipments General factory Activity Rates $ 7.00 per direct labor-hour $ 3.00 per machine-hour $ 10.00 per setup $160.00 per order $120.00 per shipment 5 4.00 per direct labor-hour Cost and activity data have been supplied for the following products Direct materials cost per unit olrect...

Lamer Corporation is a diversified manufacturer of industrial goods. The company's activity-based costing system contains the following six activity cost pools and activity rates activity cost Pool Labor related Machine-related Machine setups Production orders Shipments General factory Activity Rates $ 7.00 per direct labor-hour $ 3.00 per machine-hour $ 10.00 per setup $160.00 per order $120.00 per shipment 5 4.00 per direct labor-hour Cost and activity data have been supplied for the following products Direct materials cost per unit olrect...

Problem 2 (Supplemental Problem #2) – Activity-based costing versus traditional costing Lovelace Company produces only two...

Problem 2 (Supplemental Problem #2) – Activity-based costing versus traditional costing Lovelace Company produces only two products: reading glasses and sunglasses. The company uses a normal cost system and overhead costs are currently allocated using a plant-wide overhead rate based on direct labor hours. Outside cost consultants have recommended that the company use activity-based costing to charge overhead to products. The company expects to produce 4,000 reading glasses and 8,000 sunglasses this year. Each pair of reading glasses requires two...

Pro blem 2 (Supplemental Problem #2)-Activity-based costing versus traditional costing sunglasses. The company uses a normal...

Pro blem 2 (Supplemental Problem #2)-Activity-based costing versus traditional costing sunglasses. The company uses a normal cos based on direct labor hours Lovelace Company produces only two products: reading glasses and sung system and overhead costs are currently allocated using a plant-wide overhead rate products. Itants have recommended that the company use activity-based costing to charge overhead to he company expects to produce 4,000 reading glasses and 8,000 sunglasses this year. Each pair of reading glasses requires two direct labor...

Pro blem 2 (Supplemental Problem #2)-Activity-based costing versus traditional costing sunglasses. The company uses a normal cos based on direct labor hours Lovelace Company produces only two products: reading glasses and sung system and overhead costs are currently allocated using a plant-wide overhead rate products. Itants have recommended that the company use activity-based costing to charge overhead to he company expects to produce 4,000 reading glasses and 8,000 sunglasses this year. Each pair of reading glasses requires two direct labor...

HELP Activity-Based Costing for a Service Business Sterling Hotel uses activity-based costing to determine the cost...

HELP

Activity-Based Costing for a Service Business Sterling Hotel uses activity-based costing to determine the cost of servicing customers. There are three activity pools: guest check-in, room cleaning, and meal service. The activity rates associated with each activity pool are $8.10 per quest check-in, $22.00 per room cleaning, and $5.00 per served meal (not induding food). Brian Campbell visited the hotel for a 4-night stay. Brian had 7 meals in the hotel during the visit Determine the total activity-based cost...

HELP

Activity-Based Costing for a Service Business Sterling Hotel uses activity-based costing to determine the cost of servicing customers. There are three activity pools: guest check-in, room cleaning, and meal service. The activity rates associated with each activity pool are $8.10 per quest check-in, $22.00 per room cleaning, and $5.00 per served meal (not induding food). Brian Campbell visited the hotel for a 4-night stay. Brian had 7 meals in the hotel during the visit Determine the total activity-based cost...

Klumper Corporation is a diversified manufacturer of industrial goods. The company's activity-based costing system contains the...

Klumper Corporation is a diversified manufacturer of industrial goods. The company's activity-based costing system contains the following six activity cost pools and activity rates: Activity Cost Pool Supporting di rect labor Machine processing Machine setups Activity Rates $ 6 per direct labor-hour 4 per machine-hour $ 50 per setup $ 90 per order 14 per shipment 840 per product Production orders Shipments Product sustain ing Activity data have been supplied for the following two products: Total Expected Activity м67 2,000...

Klumper Corporation is a diversified manufacturer of industrial goods. The company's activity-based costing system contains the following six activity cost pools and activity rates: Activity Cost Pool Supporting di rect labor Machine processing Machine setups Activity Rates $ 6 per direct labor-hour 4 per machine-hour $ 50 per setup $ 90 per order 14 per shipment 840 per product Production orders Shipments Product sustain ing Activity data have been supplied for the following two products: Total Expected Activity м67 2,000...

Exercise 4-5 Assigning Overhead to Products in ABC [LO4-2, L04-3) Sultan Company uses an activity-based costing...

Exercise 4-5 Assigning Overhead to Products in ABC [LO4-2, L04-3) Sultan Company uses an activity-based costing system At the beginning of the year, the company made the following estimates of cost and activity for its five activity cost pools: Activity Cost Pool Labor-related Purchase orders Parts management Board etching General factory Activity Measure Direct labor-hours Number of orders Number of part types Number of boards Machine-hours Expected Overhead Cost $311,500 $ 8,840 $ 71,280 $ 63,700 $ 148,eee Expected Activity...

Exercise 4-5 Assigning Overhead to Products in ABC [LO4-2, L04-3) Sultan Company uses an activity-based costing system At the beginning of the year, the company made the following estimates of cost and activity for its five activity cost pools: Activity Cost Pool Labor-related Purchase orders Parts management Board etching General factory Activity Measure Direct labor-hours Number of orders Number of part types Number of boards Machine-hours Expected Overhead Cost $311,500 $ 8,840 $ 71,280 $ 63,700 $ 148,eee Expected Activity...

Problem 4-17 Contrast Activity-Based Costing and Conventional Product Costing [LO4-2, LO4-3, LO4-4] [The following information applies...

Problem 4-17 Contrast Activity-Based Costing and Conventional Product Costing [LO4-2, LO4-3, LO4-4] [The following information applies to the questions displayed below.] Puget World, Inc., manufactures two models of television sets, the N 800 XL model and the N 500 model. Data regarding the two products follow: Direct Labor- Hours per Unit Annual Production Total Direct Labor-Hours Model N 800 XL 3.5 4,500 units 15,750 Model N 500 1.2 12,500 units 15,000 30,750 Additional information about the company follows: a. Model...

Fairbanks Corporation produces two types of cell phone electronic chargers: wall chargers and car chargers. The...

Fairbanks Corporation produces two types of cell phone electronic chargers: wall chargers and car chargers. The current traditional costing system allocates overhead costs using a plant-wide overhead rate based on direct labor hours. Since the two products are similar but require different parts and processes, the company controller believes that it might make sense to employ activity-based costing in order to get a better application of overhead expenses to the products produced. Production expectations for 2017 are 17,000 wall chargers...

Activity Based Costing 1 Chapter 3: Applying Excel Fra formulato each of the cols marked when Review Problem. Activity Based Couting 6 Data Annual sales in units 9 Direct materials per unit 10 Direct labor hours per unit 2000 Tourist 10 000 $25 517 12 Direct labor rate 512 per DUH Overhead Expected Activity 16 Activities and Activity Measures 17 Labor-related (direct labor hours) 19 Machine setups (setups) 19 Production orders (orders) 20 General factory (machine hours) $ 80.000 150.000...

Activity Based Costing 1 Chapter 3: Applying Excel Fra formulato each of the cols marked when Review Problem. Activity Based Couting 6 Data Annual sales in units 9 Direct materials per unit 10 Direct labor hours per unit 2000 Tourist 10 000 $25 517 12 Direct labor rate 512 per DUH Overhead Expected Activity 16 Activities and Activity Measures 17 Labor-related (direct labor hours) 19 Machine setups (setups) 19 Production orders (orders) 20 General factory (machine hours) $ 80.000 150.000...

Lamer Corporation is a diversified manufacturer of industrial goods. The company's activity-based costing system contains the following six activity cost pools and activity rates activity cost Pool Labor related Machine-related Machine setups Production orders Shipments General factory Activity Rates $ 7.00 per direct labor-hour $ 3.00 per machine-hour $ 10.00 per setup $160.00 per order $120.00 per shipment 5 4.00 per direct labor-hour Cost and activity data have been supplied for the following products Direct materials cost per unit olrect...

Lamer Corporation is a diversified manufacturer of industrial goods. The company's activity-based costing system contains the following six activity cost pools and activity rates activity cost Pool Labor related Machine-related Machine setups Production orders Shipments General factory Activity Rates $ 7.00 per direct labor-hour $ 3.00 per machine-hour $ 10.00 per setup $160.00 per order $120.00 per shipment 5 4.00 per direct labor-hour Cost and activity data have been supplied for the following products Direct materials cost per unit olrect...

Pro blem 2 (Supplemental Problem #2)-Activity-based costing versus traditional costing sunglasses. The company uses a normal cos based on direct labor hours Lovelace Company produces only two products: reading glasses and sung system and overhead costs are currently allocated using a plant-wide overhead rate products. Itants have recommended that the company use activity-based costing to charge overhead to he company expects to produce 4,000 reading glasses and 8,000 sunglasses this year. Each pair of reading glasses requires two direct labor...

Pro blem 2 (Supplemental Problem #2)-Activity-based costing versus traditional costing sunglasses. The company uses a normal cos based on direct labor hours Lovelace Company produces only two products: reading glasses and sung system and overhead costs are currently allocated using a plant-wide overhead rate products. Itants have recommended that the company use activity-based costing to charge overhead to he company expects to produce 4,000 reading glasses and 8,000 sunglasses this year. Each pair of reading glasses requires two direct labor...

HELP

Activity-Based Costing for a Service Business Sterling Hotel uses activity-based costing to determine the cost of servicing customers. There are three activity pools: guest check-in, room cleaning, and meal service. The activity rates associated with each activity pool are $8.10 per quest check-in, $22.00 per room cleaning, and $5.00 per served meal (not induding food). Brian Campbell visited the hotel for a 4-night stay. Brian had 7 meals in the hotel during the visit Determine the total activity-based cost...

HELP

Activity-Based Costing for a Service Business Sterling Hotel uses activity-based costing to determine the cost of servicing customers. There are three activity pools: guest check-in, room cleaning, and meal service. The activity rates associated with each activity pool are $8.10 per quest check-in, $22.00 per room cleaning, and $5.00 per served meal (not induding food). Brian Campbell visited the hotel for a 4-night stay. Brian had 7 meals in the hotel during the visit Determine the total activity-based cost...

Klumper Corporation is a diversified manufacturer of industrial goods. The company's activity-based costing system contains the following six activity cost pools and activity rates: Activity Cost Pool Supporting di rect labor Machine processing Machine setups Activity Rates $ 6 per direct labor-hour 4 per machine-hour $ 50 per setup $ 90 per order 14 per shipment 840 per product Production orders Shipments Product sustain ing Activity data have been supplied for the following two products: Total Expected Activity м67 2,000...

Klumper Corporation is a diversified manufacturer of industrial goods. The company's activity-based costing system contains the following six activity cost pools and activity rates: Activity Cost Pool Supporting di rect labor Machine processing Machine setups Activity Rates $ 6 per direct labor-hour 4 per machine-hour $ 50 per setup $ 90 per order 14 per shipment 840 per product Production orders Shipments Product sustain ing Activity data have been supplied for the following two products: Total Expected Activity м67 2,000...

Exercise 4-5 Assigning Overhead to Products in ABC [LO4-2, L04-3) Sultan Company uses an activity-based costing system At the beginning of the year, the company made the following estimates of cost and activity for its five activity cost pools: Activity Cost Pool Labor-related Purchase orders Parts management Board etching General factory Activity Measure Direct labor-hours Number of orders Number of part types Number of boards Machine-hours Expected Overhead Cost $311,500 $ 8,840 $ 71,280 $ 63,700 $ 148,eee Expected Activity...

Exercise 4-5 Assigning Overhead to Products in ABC [LO4-2, L04-3) Sultan Company uses an activity-based costing system At the beginning of the year, the company made the following estimates of cost and activity for its five activity cost pools: Activity Cost Pool Labor-related Purchase orders Parts management Board etching General factory Activity Measure Direct labor-hours Number of orders Number of part types Number of boards Machine-hours Expected Overhead Cost $311,500 $ 8,840 $ 71,280 $ 63,700 $ 148,eee Expected Activity...

Most questions answered within 3 hours.

-

what process occurs to form microspores and megaspores in flowering

plants?

asked 5 minutes ago -

C++

I need to use the function getData to put in all my data using

arrays....

asked 4 minutes ago -

A block is hung by a string from the inside roof of a van. When

the...

asked 11 minutes ago -

Do you think companies should not go for long term debt in their

capital structure to...

asked 19 minutes ago -

I create an address book where the user enters the name, phone

and email in the...

asked 25 minutes ago -

The production capacity for acrylonitrile

(C3H3N) in the United States exceeds 2

million pounds per year....

asked 33 minutes ago -

explain and comment out your answer

43. How many address lines are required to address a...

asked 39 minutes ago -

A sample of 45 observations is selected from a normal

population. The sample mean is 49,...

asked 54 minutes ago -

A construction company is planning to bid on a building

contract. The bid costs the company...

asked 51 minutes ago -

A firm operating in a purely competitive environment is faced

with a market price of $250....

asked 58 minutes ago -

•Let’s say someone claims the average population size is

600 feet squared and the housing authority...

asked 1 hour ago -

Cynaide is a deadly poison that blocks the last step in the

electron transport chain of...

asked 1 hour ago