You are considering a position as the director of finance in a company listed on the...

You are considering a position as the director of finance in a company listed on the Lusaka Securities Exchange Plc. Since the firm is still new, the salary is not that great but your package will include call options on 5,000 shares of the company. The shares are currently selling for K5 per share. The call options granted to you if you accept the job have an exercise price of K5 and expire in three years. The call options cannot be exercised before maturity. The stock volatility is 28% and the three-year risk free rate is 3.6%. A call with a strike price of K30 costs K3. Required:Calculate the value of the call option.

Homework Answers

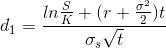

Call Option is valued with the help of either binomial option model or Black-Scholes option model. We can use Black_scholes model to value the option. Following is the formula for Call option value under Black-Scholes model.

Where

Now,

St= 5

K=5

r=3.6%

t=3

d1=0.65716; d2= -0.46867

N(d1)= 0.7446: N(d2)= 0.31965

Hence, C= 2.2849

Add Answer to:

You are considering a position as the director of finance in a

company listed on the...

The common shares of Twitter, Inc. (TWTR) recently traded on the NYSE for $20.10 per share. You have employee stock opti...

The common shares of Twitter, Inc. (TWTR) recently traded on the NYSE for $20.10 per share. You have employee stock options to purchase 1,000 TWTR shares for $18.4 per share. The options expire in three years. Assume that the annualized volatility of TWTR stock is 87.0 percent and that the interest rate is 3.3 percent. (Assume the options are European options that may only be exercised at the maturity date.) a. Is this option a call or a put? Call...

The common shares of Twitter, Inc. (TWTR) recently traded on the NYSE for $21.70 per share....

The common shares of Twitter, Inc. (TWTR) recently traded on the NYSE for $21.70 per share. You have employee stock options to purchase 1,000 TWTR shares for $20.8 per share. The options expire in three years. Assume that the annualized volatility of TWTR stock is 88.6 percent and that the interest rate is 2.6 percent. (Assume the options are European options that may only be exercised at the maturity date.) a. Is this option a call or a put? Call...

The market price of Loblaw Corporation stock has been very volatile and you think this volatility...

The market price of Loblaw Corporation stock has been very volatile and you think this volatility will continue for a few weeks. Thus, you decide to purchase a 1-month call option contract with a strike price of $47 and an option price of $1.93. You also purchase a 1-month put option contract on the stock with a strike price of $47 and an option price of $1.28. What will be your total profit or loss on all the transactions related...

The common shares of Twitter, Inc. (TWTR) recently traded on the NYSE for $20.70 per share....

The common shares of Twitter, Inc. (TWTR) recently traded on the NYSE for $20.70 per share. You have employee stock options to purchase 1,000 TWTR shares for $19.3 per share. The options expire in three years. Assume that the annualized volatility of TWTR stock is 87.6 percent and that the interest rate is 2.1 percent. (Assume the options are European options that may only be exercised at the maturity date.) a. Is this option a call or a put? •...

Please answer D, E, and F. Interpreting Disclosure on Employee Stock Options Intel Corporation reported the following...

Please answer D, E, and F.

Interpreting Disclosure on Employee Stock Options Intel Corporation reported the following in its 2015 10-K report. Share-Based Compensation Share-based compensation recognized in 2015 was $1.3 billion ($1.1 billion in 2014 and $1.1 billion in 2013) During 2015, the tax benefit that we realized for the tax deduction from share-based awards totaled $533 million ($555 million in 2014 and $385 million in 2013)... We use the Black-Scholes option pricing model to estimate the fair value...

Please answer D, E, and F.

Interpreting Disclosure on Employee Stock Options Intel Corporation reported the following in its 2015 10-K report. Share-Based Compensation Share-based compensation recognized in 2015 was $1.3 billion ($1.1 billion in 2014 and $1.1 billion in 2013) During 2015, the tax benefit that we realized for the tax deduction from share-based awards totaled $533 million ($555 million in 2014 and $385 million in 2013)... We use the Black-Scholes option pricing model to estimate the fair value...

Shares of XYZ are currently trading at $19.29 per share. You open a butterfly spread position...

Shares of XYZ are currently trading at $19.29 per share. You open a butterfly spread position because you believe the stock price will remain stable for the next month. You long a $3.40 call option with a strike price of $16.00. You short two $0.92 call options with a strike price of $19.00. You long a $0.09 call option with a strike price of $22.00. If at maturity, XYZ shares are trading at $17.00 per share, what is the final...

Shares of XYZ are currently trading at $19.29 per share. You open a butterfly spread position because you believe the stock price will remain stable for the next month. You long a $3.40 call option with a strike price of $16.00. You short two $0.92 call options with a strike price of $19.00. You long a $0.09 call option with a strike price of $22.00. If at maturity, XYZ shares are trading at $17.00 per share, what is the final...

Shares of XYZ are currently trading at $19.29 per share. You open a long straddle position...

Shares of XYZ are currently trading at $19.29 per share. You open a long straddle position to capture any potential volatility from the upcoming earning announcement. You long a $0.92 call option with a strike price of $19.00. You long a $0.62 put option with a strike price of $19.00. If at maturity, XYZ shares are trading at $15.00 per share, what is the final value of your long straddle position (on a per share basis)?

Shares of XYZ are currently trading at $19.29 per share. You open a long straddle position to capture any potential volatility from the upcoming earning announcement. You long a $0.92 call option with a strike price of $19.00. You long a $0.62 put option with a strike price of $19.00. If at maturity, XYZ shares are trading at $15.00 per share, what is the final value of your long straddle position (on a per share basis)?

This is the entire question, there were no tables or any other information given. You just...

This is the entire question, there were no tables or any other

information given.

You just sold an at-the-money European Call option on a stock that pays no dividends. The size of this option contract is 100, the current stock price is $50, and the volatility and interest rate parameters are o = 25% and r = 5%. You decide to Delta-Gamma hedge your portfolio. That is, you plan to buy and sell shares of the stock and other options...

This is the entire question, there were no tables or any other

information given.

You just sold an at-the-money European Call option on a stock that pays no dividends. The size of this option contract is 100, the current stock price is $50, and the volatility and interest rate parameters are o = 25% and r = 5%. You decide to Delta-Gamma hedge your portfolio. That is, you plan to buy and sell shares of the stock and other options...

On January 1, 2021, M Company granted 96,000 stock options to certain executives. The options are...

On January 1, 2021, M Company granted 96,000 stock options to certain executives. The options are exercisable no sooner than December 31, 2023, and expire on January 1, 2027. Each option can be exercised to acquire one share of $1 par common stock for $9. An option-pricing model estimates the fair value of the options to be $3 on the date of grant. What amount should M recognize as compensation expense for 2021? ---- On January 1, 2021, M Company...

The following price quotations are for exchange-listed options on Primo Corporation common stock. Company Strike Expiration...

The following price quotations are for exchange-listed options on Primo Corporation common stock. Company Strike Expiration Call Put Primo 61.12 56 Feb 7.23 0.49 With transaction costs ignored, how much would a buyer have to pay for one call option contract. Assume each contract is for 100 shares. Amount for one call option $

Please answer D, E, and F.

Interpreting Disclosure on Employee Stock Options Intel Corporation reported the following in its 2015 10-K report. Share-Based Compensation Share-based compensation recognized in 2015 was $1.3 billion ($1.1 billion in 2014 and $1.1 billion in 2013) During 2015, the tax benefit that we realized for the tax deduction from share-based awards totaled $533 million ($555 million in 2014 and $385 million in 2013)... We use the Black-Scholes option pricing model to estimate the fair value...

Please answer D, E, and F.

Interpreting Disclosure on Employee Stock Options Intel Corporation reported the following in its 2015 10-K report. Share-Based Compensation Share-based compensation recognized in 2015 was $1.3 billion ($1.1 billion in 2014 and $1.1 billion in 2013) During 2015, the tax benefit that we realized for the tax deduction from share-based awards totaled $533 million ($555 million in 2014 and $385 million in 2013)... We use the Black-Scholes option pricing model to estimate the fair value...

Shares of XYZ are currently trading at $19.29 per share. You open a butterfly spread position because you believe the stock price will remain stable for the next month. You long a $3.40 call option with a strike price of $16.00. You short two $0.92 call options with a strike price of $19.00. You long a $0.09 call option with a strike price of $22.00. If at maturity, XYZ shares are trading at $17.00 per share, what is the final...

Shares of XYZ are currently trading at $19.29 per share. You open a butterfly spread position because you believe the stock price will remain stable for the next month. You long a $3.40 call option with a strike price of $16.00. You short two $0.92 call options with a strike price of $19.00. You long a $0.09 call option with a strike price of $22.00. If at maturity, XYZ shares are trading at $17.00 per share, what is the final...

Shares of XYZ are currently trading at $19.29 per share. You open a long straddle position to capture any potential volatility from the upcoming earning announcement. You long a $0.92 call option with a strike price of $19.00. You long a $0.62 put option with a strike price of $19.00. If at maturity, XYZ shares are trading at $15.00 per share, what is the final value of your long straddle position (on a per share basis)?

Shares of XYZ are currently trading at $19.29 per share. You open a long straddle position to capture any potential volatility from the upcoming earning announcement. You long a $0.92 call option with a strike price of $19.00. You long a $0.62 put option with a strike price of $19.00. If at maturity, XYZ shares are trading at $15.00 per share, what is the final value of your long straddle position (on a per share basis)?

This is the entire question, there were no tables or any other

information given.

You just sold an at-the-money European Call option on a stock that pays no dividends. The size of this option contract is 100, the current stock price is $50, and the volatility and interest rate parameters are o = 25% and r = 5%. You decide to Delta-Gamma hedge your portfolio. That is, you plan to buy and sell shares of the stock and other options...

This is the entire question, there were no tables or any other

information given.

You just sold an at-the-money European Call option on a stock that pays no dividends. The size of this option contract is 100, the current stock price is $50, and the volatility and interest rate parameters are o = 25% and r = 5%. You decide to Delta-Gamma hedge your portfolio. That is, you plan to buy and sell shares of the stock and other options...

Most questions answered within 3 hours.

-

) Raw materials are studied for contamination. Suppose that

the number of particles of contamination per...

asked 7 minutes ago -

After running a regression analysis we calculated an F test and

the significance level was 0.15....

asked 3 minutes ago -

----Can someone please help me solve this one using JAVA

----I thank you in advance

Create...

asked 8 minutes ago -

1. What force primarily attracts the potassium ion to

the nitrate ion?

a. London forces...

asked 10 minutes ago -

What are the negative effects of abruptly stopping the use of

all fossil fuels? Give at...

asked 16 minutes ago -

Given that many conflict are the result of different parties having

different interests, is it possible...

asked 21 minutes ago -

A 750 g block can slide uniformly along the horizontal track

when a string attached to...

asked 24 minutes ago -

In 2017, Juan entered into a contract to write a book. The

publisher advanced Juan $50,000,...

asked 38 minutes ago -

Determine the number of kinds of protons in each molecule (w/

respect to NMR spectroscopy). Drawing...

asked 48 minutes ago -

A jeweler whose near point is 68 cm from his eye uses a

magnifying glass as...

asked 46 minutes ago -

A company wants to determine how many units of each of two

products, A and B,...

asked 50 minutes ago -

The blood pressure of a person changes throughout the day.

Suppose the systolic blood pressure of...

asked 59 minutes ago