Homework Answers

Add Answer to:

3. There are two types of firms in an industry. Type 1 firms have the costs...

3. There are two types of firms in an industry. Type 1 firms have the costs...

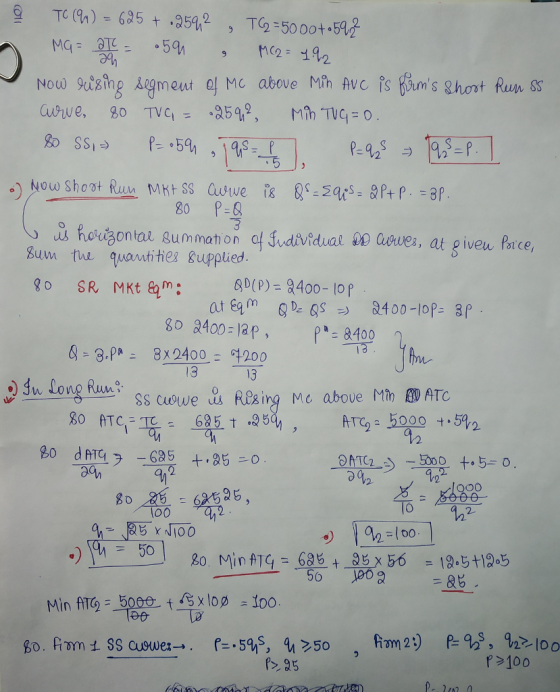

3. There are two types of firms in an industry. Type 1 firms have the costs TC(n) = 625+ 0.25qi and type 2 firms have costs TC(2) 50000.52 The fixed costs for both types of firms are NOT sunk. (a) Derive each firm's ATC(g), AVC() and MC() functions and plot the curves on separate diagrams (b) Derive each firm's supply function q(p) and show the corresponding curves in the diagrams (c Suppose that there are 10 firms of each type....

3. There are two types of firms in an industry. Type 1 firms have the costs TC(n) = 625+ 0.25qi and type 2 firms have costs TC(2) 50000.52 The fixed costs for both types of firms are NOT sunk. (a) Derive each firm's ATC(g), AVC() and MC() functions and plot the curves on separate diagrams (b) Derive each firm's supply function q(p) and show the corresponding curves in the diagrams (c Suppose that there are 10 firms of each type....

2. A competitive industry has 12 identical firms, each one has a total variable cost function...

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

1. Suppose firms in a perfectly competitive, constant cost (i.e., flat LR supply curve), industry face...

1. Suppose firms in a perfectly competitive, constant cost (i.e., flat LR supply curve), industry face monthly demand given by Qp = 1000 - P and have access to a production technology that yields a cost function TC(Q:) = 40? + 100Qi + 100 where Q denotes units produced per month. Assume the only difference between short-run and long-run costs is T C(0) = 100 in the short run and TC(O) = 0 in the long run (which is consistent...

1. Suppose firms in a perfectly competitive, constant cost (i.e., flat LR supply curve), industry face monthly demand given by Qp = 1000 - P and have access to a production technology that yields a cost function TC(Q:) = 40? + 100Qi + 100 where Q denotes units produced per month. Assume the only difference between short-run and long-run costs is T C(0) = 100 in the short run and TC(O) = 0 in the long run (which is consistent...

Question 2 The tortilla industry commissions you to examine the outlook for firms selling tortillas. There...

Question 2 The tortilla industry commissions you to examine the outlook for firms selling tortillas. There are currently twenty, identical price-taking firms in this perfectly competitive market. Each firm has a short-run cost function of STC(Q) = 9+ 2Q + . When the price is P, the total quantity demanded is given by Q(P) = 100 – 2P . (a) Assuming all fixed costs are sunk, find the short-run supply curve for a typical firm. (b) In the short run,...

Question 2 The tortilla industry commissions you to examine the outlook for firms selling tortillas. There are currently twenty, identical price-taking firms in this perfectly competitive market. Each firm has a short-run cost function of STC(Q) = 9+ 2Q + . When the price is P, the total quantity demanded is given by Q(P) = 100 – 2P . (a) Assuming all fixed costs are sunk, find the short-run supply curve for a typical firm. (b) In the short run,...

Suppose gizmos are produced in a perfectly competitive industry where two types of managers oversee the...

Suppose gizmos are produced in a perfectly competitive industry where two types of managers oversee the production. One type of the managers are called as alpha-type and the other as omega- type. There are only 100 alpha managers, whereas there is unlimited supply of omega managers Both types of managers are willing to work for a salary of $144,000 per year. The long-run total cost of a firm with an alpha manager at this salary is: TCAlpha (9)=144+q2 if q=0...

Suppose gizmos are produced in a perfectly competitive industry where two types of managers oversee the production. One type of the managers are called as alpha-type and the other as omega- type. There are only 100 alpha managers, whereas there is unlimited supply of omega managers Both types of managers are willing to work for a salary of $144,000 per year. The long-run total cost of a firm with an alpha manager at this salary is: TCAlpha (9)=144+q2 if q=0...

1. The bolt-making industry has 20 identical firms, each one has a short-run total cost function...

1. The bolt-making industry has 20 identical firms, each one has a short-run total cost function TC(q) 16 + q2 (a) What is the short-run supply of each firm? (b) The market demand is QD(p) = 110-p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's profit. (c) Suppose that the number of firms increases to 25. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's profit

1. The bolt-making industry has 20 identical firms, each one has a short-run total cost function TC(q) 16 + q2 (a) What is the short-run supply of each firm? (b) The market demand is QD(p) = 110-p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's profit. (c) Suppose that the number of firms increases to 25. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's profit

4. A competitive industry consists of six type A firms and four type B firms. Each...

4. A competitive industry consists of six type A firms and four type B firms. Each firm of type A operates with the supply curve: 1-10+ p 9A = if P >10 0 p510 Each firm of type B operates with the supply curve: 9B = 2 p if p> 0 The market demand is Q” = 108–10p. a) Draw the industry supply curve. b) What quantity is a type-A firm is producing at the market equilibrium? How about a...

4. A competitive industry consists of six type A firms and four type B firms. Each firm of type A operates with the supply curve: 1-10+ p 9A = if P >10 0 p510 Each firm of type B operates with the supply curve: 9B = 2 p if p> 0 The market demand is Q” = 108–10p. a) Draw the industry supply curve. b) What quantity is a type-A firm is producing at the market equilibrium? How about a...

For a constant cost industry in which all firms the same cost functions, their long-run average...

For a constant cost industry in which all firms the same cost functions, their long-run average cost is minimized at $10 per unit output and 20 units (i.e. q = 20). Market demand is given by QD=DP=1,500-50P. Find the long-run market supply function Find the long-run equilibrium price (P*), market quantity (Q*), firm output (q*), number of firms (n), and each firm’s profit. The short-run total cost function associated with each firm’s long-run costs is SCq=0.5q2-10q+200. Calculate the short-run average...

Suppose that each firm in a competitive industry has the following costs: Total Cost: TC =...

Suppose that each firm in a competitive industry has the following costs:Total Cost: TC=50+1/2 q2Marginal Cost: MC=qwhere q is an individual firm's quantity produced.The market demand curve for this product is:Demand QD=160-4 Pwhere P is the price and Q is the total quantity of the good.Each firm's fixed cost is $_______ What is each firm's variable cost?1/2 q50+1/2 q1/2 q^{2}qWhich of the following represents the equation for each firm's average total cost?50/q+1/2 q50+1/2 q50/q1/2 qComplete the following table by computing the...

Suppose that each firm in a competitive industry has the following costs:Total Cost: TC=50+1/2 q2Marginal Cost: MC=qwhere q is an individual firm's quantity produced.The market demand curve for this product is:Demand QD=160-4 Pwhere P is the price and Q is the total quantity of the good.Each firm's fixed cost is $_______ What is each firm's variable cost?1/2 q50+1/2 q1/2 q^{2}qWhich of the following represents the equation for each firm's average total cost?50/q+1/2 q50+1/2 q50/q1/2 qComplete the following table by computing the...

3. There are two types of firms in an industry. Type 1 firms have the costs TC(n) = 625+ 0.25qi and type 2 firms have costs TC(2) 50000.52 The fixed costs for both types of firms are NOT sunk. (a) Derive each firm's ATC(g), AVC() and MC() functions and plot the curves on separate diagrams (b) Derive each firm's supply function q(p) and show the corresponding curves in the diagrams (c Suppose that there are 10 firms of each type....

3. There are two types of firms in an industry. Type 1 firms have the costs TC(n) = 625+ 0.25qi and type 2 firms have costs TC(2) 50000.52 The fixed costs for both types of firms are NOT sunk. (a) Derive each firm's ATC(g), AVC() and MC() functions and plot the curves on separate diagrams (b) Derive each firm's supply function q(p) and show the corresponding curves in the diagrams (c Suppose that there are 10 firms of each type....

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

1. Suppose firms in a perfectly competitive, constant cost (i.e., flat LR supply curve), industry face monthly demand given by Qp = 1000 - P and have access to a production technology that yields a cost function TC(Q:) = 40? + 100Qi + 100 where Q denotes units produced per month. Assume the only difference between short-run and long-run costs is T C(0) = 100 in the short run and TC(O) = 0 in the long run (which is consistent...

1. Suppose firms in a perfectly competitive, constant cost (i.e., flat LR supply curve), industry face monthly demand given by Qp = 1000 - P and have access to a production technology that yields a cost function TC(Q:) = 40? + 100Qi + 100 where Q denotes units produced per month. Assume the only difference between short-run and long-run costs is T C(0) = 100 in the short run and TC(O) = 0 in the long run (which is consistent...

Question 2 The tortilla industry commissions you to examine the outlook for firms selling tortillas. There are currently twenty, identical price-taking firms in this perfectly competitive market. Each firm has a short-run cost function of STC(Q) = 9+ 2Q + . When the price is P, the total quantity demanded is given by Q(P) = 100 – 2P . (a) Assuming all fixed costs are sunk, find the short-run supply curve for a typical firm. (b) In the short run,...

Question 2 The tortilla industry commissions you to examine the outlook for firms selling tortillas. There are currently twenty, identical price-taking firms in this perfectly competitive market. Each firm has a short-run cost function of STC(Q) = 9+ 2Q + . When the price is P, the total quantity demanded is given by Q(P) = 100 – 2P . (a) Assuming all fixed costs are sunk, find the short-run supply curve for a typical firm. (b) In the short run,...

Suppose gizmos are produced in a perfectly competitive industry where two types of managers oversee the production. One type of the managers are called as alpha-type and the other as omega- type. There are only 100 alpha managers, whereas there is unlimited supply of omega managers Both types of managers are willing to work for a salary of $144,000 per year. The long-run total cost of a firm with an alpha manager at this salary is: TCAlpha (9)=144+q2 if q=0...

Suppose gizmos are produced in a perfectly competitive industry where two types of managers oversee the production. One type of the managers are called as alpha-type and the other as omega- type. There are only 100 alpha managers, whereas there is unlimited supply of omega managers Both types of managers are willing to work for a salary of $144,000 per year. The long-run total cost of a firm with an alpha manager at this salary is: TCAlpha (9)=144+q2 if q=0...

1. The bolt-making industry has 20 identical firms, each one has a short-run total cost function TC(q) 16 + q2 (a) What is the short-run supply of each firm? (b) The market demand is QD(p) = 110-p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's profit. (c) Suppose that the number of firms increases to 25. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's profit

1. The bolt-making industry has 20 identical firms, each one has a short-run total cost function TC(q) 16 + q2 (a) What is the short-run supply of each firm? (b) The market demand is QD(p) = 110-p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's profit. (c) Suppose that the number of firms increases to 25. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's profit

4. A competitive industry consists of six type A firms and four type B firms. Each firm of type A operates with the supply curve: 1-10+ p 9A = if P >10 0 p510 Each firm of type B operates with the supply curve: 9B = 2 p if p> 0 The market demand is Q” = 108–10p. a) Draw the industry supply curve. b) What quantity is a type-A firm is producing at the market equilibrium? How about a...

4. A competitive industry consists of six type A firms and four type B firms. Each firm of type A operates with the supply curve: 1-10+ p 9A = if P >10 0 p510 Each firm of type B operates with the supply curve: 9B = 2 p if p> 0 The market demand is Q” = 108–10p. a) Draw the industry supply curve. b) What quantity is a type-A firm is producing at the market equilibrium? How about a...

Most questions answered within 3 hours.

-

(EPS with

Convertible Bonds) On June 1, 2012, Bluhm Company and

Amanar Company merged to form...

asked 18 seconds ago -

The velocity field of a flow is given by V = (2+1) x

y2 i +...

asked 2 minutes ago -

2. Discuss why the study exemplifies one that agrees with The

American Psychological Association’s (APA) Ethical...

asked 4 minutes ago -

Without considering the following capital gains and losses,

Charlene, who is single, has a taxable income...

asked 11 minutes ago -

1a. The __________ functional group often triggers our sense of

smell.

1b. The geometry around a...

asked 24 minutes ago -

A uniform plank of length 2.00 m and mass 34.0 kg is supported

by three ropes,...

asked 25 minutes ago -

Suppose a floor on a hospital has 12 physicians at any given

time. You are brought...

asked 39 minutes ago -

Compartmentalization

in eukaryotic cells facilitates chemical reactions happening faster

due to... Select all

Substrates needed for...

asked 26 minutes ago -

The deltaH for the solution process when solid sodium

hydroxide dissolves in water is 44.4 kJ/mol....

asked 29 minutes ago -

a. Discuss the reciprocal/opposite “hormonal” regulation of the

most highly regulated steps of these two pathways....

asked 47 minutes ago -

Members of unions had mounted campaigns to persuade customers

not to shop at a company because...

asked 48 minutes ago -

Why is the alpha carboxyl group pka value 2 ?

And why is an alpha amino...

asked 57 minutes ago