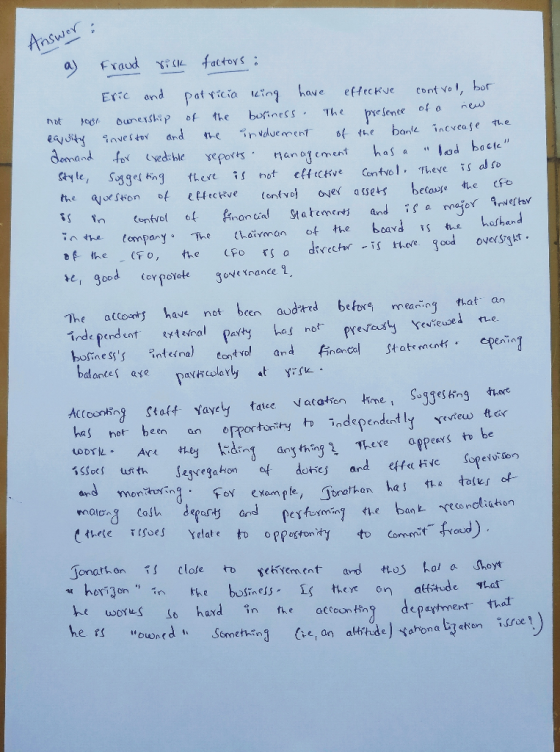

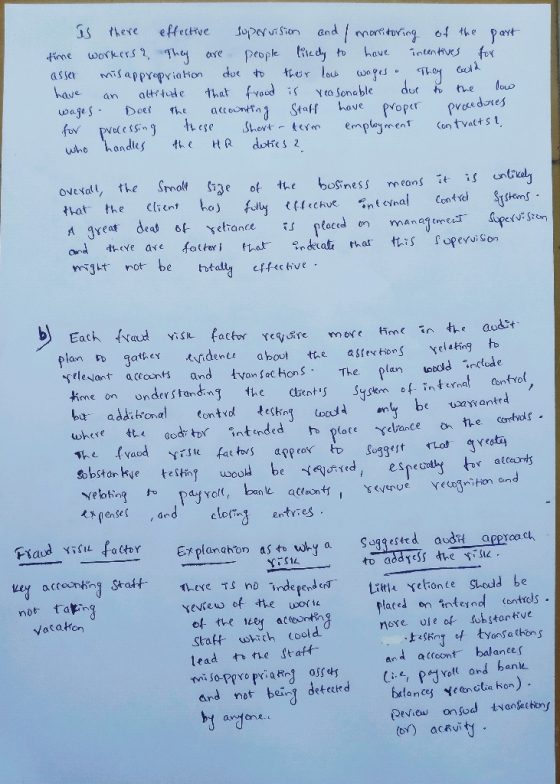

What are the fraud risk factors of KCI, why

are they risks, and how will the risk affect my approach to the

audit of KCI?

What are the fraud risk factors of KCI, why

are they risks, and how will the risk affect my approach to the

audit of KCI?

Homework Answers

Refer the below images for the above asked questions, in a detailed way of solution.

Add Answer to:

What are the fraud risk factors of KCI, why

are they risks, and how will the...

King Companies, Inc. (KCI) is a private company that owns five auto parts stores in urban...

King Companies, Inc. (KCI) is a private company that owns five auto parts stores in urban Los Angeles, California. KCI has expanded from two auto parts stores to five stores in the last three years, and it plans continued growth. Eric and Patricia King own the majority of the shares in KCI. Eric is the chairman of the board of directors and CEO of KCI, and Patricia is a director as well as the CFO. Shares not owned by Eric...

Which of the six risks should be considered a significant risk? Explain why they represent a...

Which of the six risks should be considered a significant risk? Explain why they represent a significant risk. For each risk that you identified as a significant risk, describe how you might address the risk to give it special audit consideration. For example, a valuation risk might be addressed by engaging a valuation specialist. Begin by determining which of the six risks should be considered a significant risk. Then, for each risk that has been identified as a significant risk,...

Auditing Related Party Transactions ABSTRACT As part of the risk assessment of a client firm, auditors...

Auditing Related Party Transactions ABSTRACT As part of the risk assessment of a client firm, auditors are required to evaluate the risks of material misstatement associated with related party transactions. Related party transactions may be evaluated at a higher risk of material misstatement as they may not occur under normal market settings or they may be motivated by an intent to perpetrate fraud. This case presents information about the related party transactions and other facts surrounding the audit of a...

Auditing Related Party Transactions ABSTRACT As part of the risk assessment of a client firm, auditors...

Auditing Related Party Transactions ABSTRACT As part of the risk assessment of a client firm, auditors are required to evaluate the risks of material misstatement associated with related party transactions. Related party transactions may be evaluated at a higher risk of material misstatement as they may not occur under normal market settings or they may be motivated by an intent to perpetrate fraud. This case presents information about the related party transactions and other facts surrounding the audit of a...

Fraud at Berry, CPA’s BERRY, CERTIFIED PUBLIC ACCOUNTANTS Brief History of the Firm In 1999, John...

Fraud at Berry, CPA’s BERRY, CERTIFIED PUBLIC ACCOUNTANTS Brief History of the Firm In 1999, John Berry graduated from college with an accounting degree. After 10 years at an international accounting firm, John decided to start his firm, Berry, CPA’s. The firm, located in Oakwood, caters to local clients; specifically, John and his staff of four professionals specialize in non-public companies. The majority of the services provided by Berry, CPA’s are tax planning and preparation; however, the firm also performs...

CASE 20 Enron: Not Accounting for the Future* INTRODUCTION Once upon a time, there was a...

CASE 20 Enron: Not Accounting for the Future* INTRODUCTION Once upon a time, there was a gleaming office tower in Houston, Texas. In front of that gleaming tower was a giant "E" slowly revolving, flashing in the hot Texas sun. But in 2001, the Enron Corporation, which once ranked among the top Fortune 500 companies, would collapse under a mountain of debt that had been concealed through a complex scheme of off-balance-sheet partnerships. Forced to declare bankruptcy, the energy firm...

CASE 20 Enron: Not Accounting for the Future* INTRODUCTION Once upon a time, there was a gleaming office tower in Houston, Texas. In front of that gleaming tower was a giant "E" slowly revolving, flashing in the hot Texas sun. But in 2001, the Enron Corporation, which once ranked among the top Fortune 500 companies, would collapse under a mountain of debt that had been concealed through a complex scheme of off-balance-sheet partnerships. Forced to declare bankruptcy, the energy firm...

CASE 20 Enron: Not Accounting for the Future* INTRODUCTION Once upon a time, there was a gleaming office tower in Houston, Texas. In front of that gleaming tower was a giant "E" slowly revolving, flashing in the hot Texas sun. But in 2001, the Enron Corporation, which once ranked among the top Fortune 500 companies, would collapse under a mountain of debt that had been concealed through a complex scheme of off-balance-sheet partnerships. Forced to declare bankruptcy, the energy firm...

CASE 20 Enron: Not Accounting for the Future* INTRODUCTION Once upon a time, there was a gleaming office tower in Houston, Texas. In front of that gleaming tower was a giant "E" slowly revolving, flashing in the hot Texas sun. But in 2001, the Enron Corporation, which once ranked among the top Fortune 500 companies, would collapse under a mountain of debt that had been concealed through a complex scheme of off-balance-sheet partnerships. Forced to declare bankruptcy, the energy firm...

Most questions answered within 3 hours.

-

Let X be a continuous random variable whose PDF is Let X be a

continuous random...

asked 6 minutes ago -

Martinez Company’s relevant range of production is 7,500 units

to 12,500 units. When it produces and...

asked 4 minutes ago -

A football with a mass of 1.2 kg is kicked from ground level to

a height...

asked 9 minutes ago -

Remember: Changes in supply determinants shift supply, and

changes in demand determinants shift demand. We say...

asked 8 minutes ago -

Why is the answer b), for this question? I came up with C) for

my incorrect...

asked 14 minutes ago -

Suppose that you know that in the population of full-time

employees in the United States, the...

asked 36 minutes ago -

This experiment was designed originally to sample various meat and carcass quality

aspects of Ontario pigs...

asked 37 minutes ago -

Dopamine Hydrochloride: draw the structure And Show the

functional groups in different colors and label the...

asked 29 minutes ago -

A rope supports a 10 kg dumbbell hanging from it. What is the

tension in the...

asked 28 minutes ago -

) Raw materials are studied for contamination. Suppose that

the number of particles of contamination per...

asked 51 minutes ago -

After running a regression analysis we calculated an F test and

the significance level was 0.15....

asked 47 minutes ago -

----Can someone please help me solve this one using JAVA

----I thank you in advance

Create...

asked 51 minutes ago