[Para. 4-a-10]Invoices for some of goods and services ordered in transaction 4-a-3 were received and vouchered...

[Para. 4-a-10]Invoices for some of goods and services ordered in transaction 4-a-3 were received and vouchered for later payment. (Select “Elimination” in the drop down [Transaction Description] menu in the Detail Journal):

Actual Estimated

General Government $ 395,940 $ 394,060

Public Safety 1,086,650 1,088,600

Public Works 922,300 927,620

Health and Welfare 661,200 663,600

Culture and Recreation 593,750 597,000

Miscellaneous 138,000 138,000

Totals $3,797,840 $3,808,880

Required: Record the receipt of these goods and the related vouchers payable in both the General Fund and governmental activities journals. At the government-wide level, you should assume the city uses the periodic inventory method. Thus, the invoiced amounts above should be recorded as expenses of the appropriate functions, except for $72,500 of playground equipment ordered by Culture and Recreation. The equipment meets the city’s threshold for capitalization (debit Equipment for this item at the government-wide level). Expenditures charged to the miscellaneous appropriation should be recorded in this case as General Government expenses at the government-wide level.

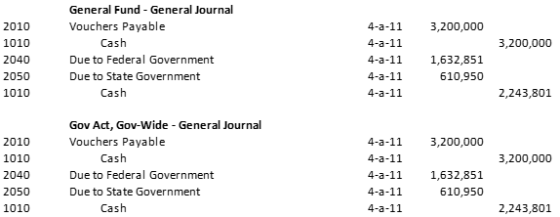

[Para. 4-a-11] The General Fund paid vouchers during the year in the amount of $3,200,000 as well as its liabilities for employees’ federal and state income taxes withheld and payroll taxes.

Required: Record the payment of these items in both the General Fund and governmental activities general journals.

[Para. 4-a-12] The General Fund transferred $50,000 to the debt service fund so the debt service fund could make a bond interest payment.

Required: Record this transaction in the General Fund only. The transaction has no effect at the government-wide level since it occurs between two governmental activities. (Do not record this transaction in the debt service fund until instructed to do so in Chapter 6 of this case.)

[Para. 4-a-13]Tax anticipation notes issued by the General Fund were paid at maturity at the face amount plus interest of $10,000.

Required: Record the payment of these items in both the General Fund and governmental activities general journals. For the General Fund charge Miscellaneous for the interest expenditure. At the government-wide level, debit Expenses—Interest on Tax Anticipation Notes.

Homework Answers

General Fund

Note: Use of ACCT 7010 will open the detail journal for encumbrances where you will enter the estimated amounts by function. Use of ACCT 6010 will open the detail journal for expenditures where you will enter the actual amounts by function and use goods received in the pull down menu. (You will have to populate the goods received in the pull down menu each time you enter the expenditure).

Gov Wide

Assume the city uses the periodic inventory method. The invoiced amounts above should be recorded as expenses of the appropriate functions, except for $72,500 of playground equipment ordered by Culture and Recreation. The equipment meets the city’s threshold for capitalization (debit Equipment for this item at the government-wide level). The amount attributable to Culture and Recreation is $72,500 for the equipment and $521,250 for expenses totaling to $593,750

Para 4-a-11

Para 4-a-12

Para 4-a-13

Add Answer to:

[Para. 4-a-10]Invoices for some of

goods and services ordered in transaction 4-a-3

were received and vouchered...

the question just about 5a-15 to 5a-18, I know the answer about 5a-1 to 5a-14 Para....

the question just about 5a-15 to 5a-18, I know the answer about 5a-1 to 5a-14 Para. 5a-1] On the first day of the 2020 fiscal year (January 1, 2020), the bond issue was sold at 101. Cash in the face amount of the bonds, $7,500,000, was deposited in the City Hall Annex Construction Fund; the premium was deposited in the debt service fund, as required by state law. Required: Record these transactions in the City Hall Annex Construction Fund...

Need help with the journal entry for both general fund and governmental activities not sure what...

Need help with the journal entry for both general fund and governmental activities not sure what to do with the vehicle 5. Invoices for some of the goods recorded as encumbrances in transaction 4-a-2 were received and vouchered for payment, as listed below. Related encumbrances were canceled in the amounts listed below Expenditures Encumbrances General Government $ 94,776 $ 94,752 Public Safety 175,406 175,620 Public Works 194,408 194,512 Culture and Recreation 108,187 108,150 ...

The City of Troy collects its annual property taxes late in its fiscal year. Consequently, each...

The City of Troy collects its annual property taxes late in its fiscal year. Consequently, each year it must finance part of its operating budget using tax anticipation notes. The notes are repaid upon collection of property taxes. On April 1, the city estimated that it will require $2,500,000 to finance governmental activities for the remainder of the fiscal year. On that date, it had $770,000 of cash on hand and $830,000 of current liabilities. Collections for the remainder of...

The City of Troy collects its annual property taxes late in its fiscal year. Consequently, each year it must finance part of its operating budget using tax anticipation notes. The notes are repaid upon collection of property taxes. On April 1, the city estimated that it will require $2,500,000 to finance governmental activities for the remainder of the fiscal year. On that date, it had $770,000 of cash on hand and $830,000 of current liabilities. Collections for the remainder of...

Post according to Governmental Accounting please [Para. 4-a-10] The city’s budget for 2017 was legally amended...

Post according to Governmental Accounting please [Para. 4-a-10] The city’s budget for 2017 was legally amended as follows: Estimated Revenues: Decreases Increases Charges for Services $ 5,000 Total $ 5,000 $0 Appropriations: Public Safety $11,000 Public Works $1,600 Culture and Recreation 37,500 $11,000 $39,100 Note: These amendments decrease the balance of the Budgetary Fund Balance account by $33,100. Required: Record the budget amendments in the General Fund general journal only. Budgetary items do not affect the government-wide accounting...

[Para. 4-a-7] During FY 2020, the City of Smithville received notification that the state government would...

[Para. 4-a-7] During FY 2020, the City of Smithville received notification that the state government would send $150,000 to it at the beginning of the next fiscal year. Based on the city’s definition of “available for use,” the city considers the funds available to use for Public Safety’s operating activities in the current reporting period. The budget for the current year included this amount as “Intergovernmental Revenue.” Required: Record this transaction as a receivable and revenue in the General Fund and...

10. [Para. 4-a-10] Interest and penalties receivable on delinquent taxes was increased by $40,500; $3,248 of...

10. [Para. 4-a-10] Interest and penalties receivable on delinquent taxes was increased by $40,500; $3,248 of this was estimated as uncollectible and $8,910 was considered unavailable for use in the current fiscal year. Required: Record this transaction in the General Fund and governmental activities journals as a revenue transaction. The $8,910 classified as unavailable for use is recorded as deferred inflows of resources in the General Fund journal and as revenue in the governmental activities journal. Post all journal entries...

10. [Para. 4-a-10] Interest and penalties receivable on delinquent taxes was increased by $40,500; $3,248 of this was estimated as uncollectible and $8,910 was considered unavailable for use in the current fiscal year. Required: Record this transaction in the General Fund and governmental activities journals as a revenue transaction. The $8,910 classified as unavailable for use is recorded as deferred inflows of resources in the General Fund journal and as revenue in the governmental activities journal. Post all journal entries...

Required information [The following information applies to the questions displayed below.] The following transactions occurred during...

Required information [The following information applies to the questions displayed below.] The following transactions occurred during the 2020 fiscal year for the City of Evergreen. For budgetary purposes, the city reports encumbrances in the Expenditures section of its budgetary comparison schedule for the General Fund but excludes expenditures chargeable to a prior year's appropriation. 1. The budget prepared for the fiscal year 2020 was as follows: Estimated Revenues: $1,943,000 372,000 397,000 62,000 Тахes Licenses and permits Intergovernmental revenue Miscellaneous revenues...

Required information [The following information applies to the questions displayed below.] The following transactions occurred during the 2020 fiscal year for the City of Evergreen. For budgetary purposes, the city reports encumbrances in the Expenditures section of its budgetary comparison schedule for the General Fund but excludes expenditures chargeable to a prior year's appropriation. 1. The budget prepared for the fiscal year 2020 was as follows: Estimated Revenues: $1,943,000 372,000 397,000 62,000 Тахes Licenses and permits Intergovernmental revenue Miscellaneous revenues...

[Para. 4-a-13] Delinquent taxes receivable in the amount of $17,150 were written off as uncollectible. Interest...

[Para. 4-a-13] Delinquent taxes receivable in the amount of $17,150 were written off as uncollectible. Interest and penalties already recorded as receivable on these taxes, amounting to $3,087, were also written off. Additional interest on these taxes that had legally accrued was not recorded since it was deemed uncollectible in its entirety. Required: Record this transaction in the General Fund and governmental activities journals.

[Para. 4-a-13] Delinquent taxes receivable in the amount of $17,150 were written off as uncollectible. Interest and penalties already recorded as receivable on these taxes, amounting to $3,087, were also written off. Additional interest on these taxes that had legally accrued was not recorded since it was deemed uncollectible in its entirety. Required: Record this transaction in the General Fund and governmental activities journals.

can you post the journal entries and how you got them. thank you 2. Rowan City...

can you post the journal entries and how you got them. thank

you

2. Rowan City applied for and received a grant of $10,000 from the State to purchase computers for the public library. Record this transaction in the city's journals from the perspective of government-wide governmental activities and the perspective of the General Fund. For governmental activities: Date Account Name Debit Credit For the General Fund: Account Name Date Debit Credit 3. On the last day of the calendar...

can you post the journal entries and how you got them. thank

you

2. Rowan City applied for and received a grant of $10,000 from the State to purchase computers for the public library. Record this transaction in the city's journals from the perspective of government-wide governmental activities and the perspective of the General Fund. For governmental activities: Date Account Name Debit Credit For the General Fund: Account Name Date Debit Credit 3. On the last day of the calendar...

The City of Troy collects its annual property taxes late in its fiscal year. Consequently, each...

The City of Troy collects its annual property taxes late in its fiscal year. Consequently, each year it must finance part of its operating budget using tax anticipation notes. The notes are repaid upon collection of property taxes. On April 1, the city estimated that it will require $2,000,000 to finance governmental activities for the remainder of the fiscal year. On that date, it had $720,000 of cash on hand and $780,000 of current liabilities. Collections for the remainder of...

The City of Troy collects its annual property taxes late in its fiscal year. Consequently, each year it must finance part of its operating budget using tax anticipation notes. The notes are repaid upon collection of property taxes. On April 1, the city estimated that it will require $2,500,000 to finance governmental activities for the remainder of the fiscal year. On that date, it had $770,000 of cash on hand and $830,000 of current liabilities. Collections for the remainder of...

The City of Troy collects its annual property taxes late in its fiscal year. Consequently, each year it must finance part of its operating budget using tax anticipation notes. The notes are repaid upon collection of property taxes. On April 1, the city estimated that it will require $2,500,000 to finance governmental activities for the remainder of the fiscal year. On that date, it had $770,000 of cash on hand and $830,000 of current liabilities. Collections for the remainder of...

10. [Para. 4-a-10] Interest and penalties receivable on delinquent taxes was increased by $40,500; $3,248 of this was estimated as uncollectible and $8,910 was considered unavailable for use in the current fiscal year. Required: Record this transaction in the General Fund and governmental activities journals as a revenue transaction. The $8,910 classified as unavailable for use is recorded as deferred inflows of resources in the General Fund journal and as revenue in the governmental activities journal. Post all journal entries...

10. [Para. 4-a-10] Interest and penalties receivable on delinquent taxes was increased by $40,500; $3,248 of this was estimated as uncollectible and $8,910 was considered unavailable for use in the current fiscal year. Required: Record this transaction in the General Fund and governmental activities journals as a revenue transaction. The $8,910 classified as unavailable for use is recorded as deferred inflows of resources in the General Fund journal and as revenue in the governmental activities journal. Post all journal entries...

Required information [The following information applies to the questions displayed below.] The following transactions occurred during the 2020 fiscal year for the City of Evergreen. For budgetary purposes, the city reports encumbrances in the Expenditures section of its budgetary comparison schedule for the General Fund but excludes expenditures chargeable to a prior year's appropriation. 1. The budget prepared for the fiscal year 2020 was as follows: Estimated Revenues: $1,943,000 372,000 397,000 62,000 Тахes Licenses and permits Intergovernmental revenue Miscellaneous revenues...

Required information [The following information applies to the questions displayed below.] The following transactions occurred during the 2020 fiscal year for the City of Evergreen. For budgetary purposes, the city reports encumbrances in the Expenditures section of its budgetary comparison schedule for the General Fund but excludes expenditures chargeable to a prior year's appropriation. 1. The budget prepared for the fiscal year 2020 was as follows: Estimated Revenues: $1,943,000 372,000 397,000 62,000 Тахes Licenses and permits Intergovernmental revenue Miscellaneous revenues...

[Para. 4-a-13] Delinquent taxes receivable in the amount of $17,150 were written off as uncollectible. Interest and penalties already recorded as receivable on these taxes, amounting to $3,087, were also written off. Additional interest on these taxes that had legally accrued was not recorded since it was deemed uncollectible in its entirety. Required: Record this transaction in the General Fund and governmental activities journals.

[Para. 4-a-13] Delinquent taxes receivable in the amount of $17,150 were written off as uncollectible. Interest and penalties already recorded as receivable on these taxes, amounting to $3,087, were also written off. Additional interest on these taxes that had legally accrued was not recorded since it was deemed uncollectible in its entirety. Required: Record this transaction in the General Fund and governmental activities journals.

can you post the journal entries and how you got them. thank

you

2. Rowan City applied for and received a grant of $10,000 from the State to purchase computers for the public library. Record this transaction in the city's journals from the perspective of government-wide governmental activities and the perspective of the General Fund. For governmental activities: Date Account Name Debit Credit For the General Fund: Account Name Date Debit Credit 3. On the last day of the calendar...

can you post the journal entries and how you got them. thank

you

2. Rowan City applied for and received a grant of $10,000 from the State to purchase computers for the public library. Record this transaction in the city's journals from the perspective of government-wide governmental activities and the perspective of the General Fund. For governmental activities: Date Account Name Debit Credit For the General Fund: Account Name Date Debit Credit 3. On the last day of the calendar...

Most questions answered within 3 hours.

-

Why do organizations decline? What steps can top

management take to halt, decline, and restore organizational...

asked 6 minutes ago -

Under the influence of its drive force, a snowmobile is moving

at a constant velocity along...

asked 20 minutes ago -

What mechanisms Drive speciation??

(I.e. what was Dawins theory on the orgin of species, and how...

asked 1 hour ago -

The manager at a car assembly plant believes that the mean

assembly time for a car...

asked 2 hours ago -

Which of the following is true of electron capture?

A) It decreases the nuclide's mass number...

asked 4 hours ago -

Assuming an efficiency of 43.10%, calculate the actual yield of

magnesium nitrate formed from 114.9 g...

asked 4 hours ago -

The highly pathogenic bacterium Clostridium

perfringens causes gangrene, a disease that results in the

destruction of...

asked 6 hours ago -

In the context of situation analysis, which of the following is

a category for analysis in...

asked 6 hours ago -

In a study of the gas phase decomposition of sulfuryl chloride

at 600 K SO2Cl2(g)SO2(g) +...

asked 6 hours ago -

75 g of 2-propanol (C3H8O) and 25 g of pentane are mixed in a

200 mL...

asked 6 hours ago -

The 2800-turn coil in a dc motor has an area per turn of 1.1 ×

10-2...

asked 6 hours ago -

Draw a combinational logic circuit diagram with a symbol inside

the box for two I/P of...

asked 6 hours ago