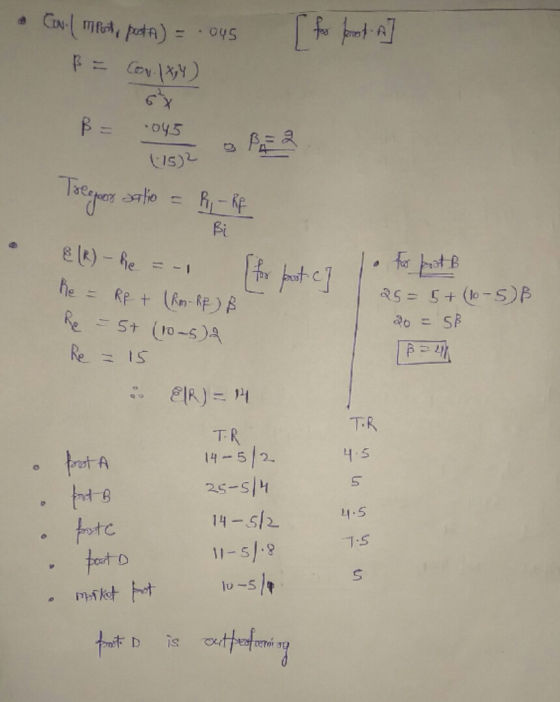

According to the Treynor meassure. Which of the following portfolios are outperforming the market portfolio? The...

According to the Treynor meassure. Which of the following portfolios are outperforming the market portfolio? The risk free rate of interest is 5%

Portfolio A: Standard deviation: 20%, Expected return: 14%. The covariance between the portfolio and the market portfolio is 0,045

Portfolio B: Expected return: 25% (according to CAPM)

Portfolio C: Alpha: -1%: Beta: 2

Portfolio D: Expected return: 11%: Beta 0,8

The market portfolio: Standard deviation: 15%, Expected return: 10%,

Select one:

a. Portfolio A

b. Portfolio C

c. Portfolio D

d. The market portfolio

e. Portfolio B

Homework Answers

Add Answer to:

According to the Treynor meassure. Which of the following

portfolios are outperforming the market portfolio? The...

Expected Portfolio Return Beta 22 0.8 A Market 173 1.0 D) Expected Portfolio Return Beta 30.28 1.8 A Market 198 1.0 If...

Expected Portfolio Return Beta 22 0.8 A Market 173 1.0 D) Expected Portfolio Return Beta 30.28 1.8 A Market 198 1.0 If the simple CAPM is valid and all portfolios are priced correctly, which of the situations below is possible? Consider each situation independently, and assume the risk-free rate is 5% A) Expected Portfolio Return Beta 198 0.8 Market 198 1.0 B) Expected Standard Return Deviation Portfolio 228 88 A Market 17B 168

Expected Portfolio Return Beta 22 0.8 A Market 173 1.0 D) Expected Portfolio Return Beta 30.28 1.8 A Market 198 1.0 If the simple CAPM is valid and all portfolios are priced correctly, which of the situations below is possible? Consider each situation independently, and assume the risk-free rate is 5% A) Expected Portfolio Return Beta 198 0.8 Market 198 1.0 B) Expected Standard Return Deviation Portfolio 228 88 A Market 17B 168

There are three assets, A, B and C, where A is the market portfolio and C...

There are three assets, A, B and C, where A is the market portfolio and C is the risk-free asset. The return on the market has a mean of 12% and a standard deviation of 20%. The risk-free asset yields a return of 4%. Asset B is a risky asset whose return has a standard deviation of 40% and a market beta of 1. Assume that the CAPM holds. Compute the expected return of asset B and its covariances with...

15. Estimate the Sharpe, Treynor and Alpha Jensen's performance analyses fort the three portfolios below. Use...

15. Estimate the Sharpe, Treynor and Alpha Jensen's performance analyses fort the three portfolios below. Use the data below to complete the table. Portfolio Sharpe Treynor Jensen's Return 0.07 0.085 0.11 SD 0.15 0.12 0.095 Beta 0.8 1.05 1.4 Z 0.075 Market Risk Free 0.075 0.025 a. If you were to choose one portfolio, which one would it be? Why?

15. Estimate the Sharpe, Treynor and Alpha Jensen's performance analyses fort the three portfolios below. Use the data below to complete the table. Portfolio Sharpe Treynor Jensen's Return 0.07 0.085 0.11 SD 0.15 0.12 0.095 Beta 0.8 1.05 1.4 Z 0.075 Market Risk Free 0.075 0.025 a. If you were to choose one portfolio, which one would it be? Why?

Consider the following information Expected Standard Portfolio Return Deviation Risk-free 10% 1.0 Market 18 A 16...

Consider the following information Expected Standard Portfolio Return Deviation Risk-free 10% 1.0 Market 18 A 16 1.5 a. Calculate the return predicted by CAPM for a portfolio with a beta of 1.5 Return b. What is the alpha of portfolio A. (Negatlve value should be Indicated by a minus sign.) Alpha c. If the simple CAPM is valid, is the situation above possible? O Yes O No

Consider the following information Expected Standard Portfolio Return Deviation Risk-free 10% 1.0 Market 18 A 16 1.5 a. Calculate the return predicted by CAPM for a portfolio with a beta of 1.5 Return b. What is the alpha of portfolio A. (Negatlve value should be Indicated by a minus sign.) Alpha c. If the simple CAPM is valid, is the situation above possible? O Yes O No

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset:...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio RP σP βP X 13.0 % 30 % 1.30 Y 12.0 25 1.10 Z 7.0 15 0.75 Market 10.1 20 1.00 Risk-free 5.0 0 0 What are the Sharpe ratio, Treynor ratio, and Jensen’s alpha for each portfolio?

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset:...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio RP 13.0% 12.0 7.0 10.1 5.0 op 30% 25 15 20 Bp 1.30 1.10 0.75 1.00 Market Risk-free 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicated by a minus sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Round your ratio answers...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio RP 13.0% 12.0 7.0 10.1 5.0 op 30% 25 15 20 Bp 1.30 1.10 0.75 1.00 Market Risk-free 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicated by a minus sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Round your ratio answers...

Parker has a portfolio with a beta of 1.0 and an a porttolio with a beta...

Parker has a portfolio with a beta of 1.0 and an a porttolio with a beta of 1.0 and an alpha of 0. Based on the CAPM, the return for the portfolio is a. 10% b. Greater than Rm. C. Equal to the Rm. d. Less than Rm but greater than R. ne TOKO Fund earns 11.2% during the year while the risk-free rate is 3.1%. The Yoko Fund has a beta of 1.20 and a standard deviation of 17.5%....

Parker has a portfolio with a beta of 1.0 and an a porttolio with a beta of 1.0 and an alpha of 0. Based on the CAPM, the return for the portfolio is a. 10% b. Greater than Rm. C. Equal to the Rm. d. Less than Rm but greater than R. ne TOKO Fund earns 11.2% during the year while the risk-free rate is 3.1%. The Yoko Fund has a beta of 1.20 and a standard deviation of 17.5%....

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk premium is 0.07, and the market risk premium has a standard...

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk premium is 0.07, and the market risk premium has a standard deviation of 25%, then what is asset B's expected return under the CAPM?

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk...

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk premium is 0.07, and the market risk premium has a standard deviation of 25%, then what is asset B's expected return under the CAPM?

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk...

ALLLLL 23. You are given the following information concerning three portfolios, the market portfolio, and the...

ALLLLL 23. You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio Rp Qe Bp 12.0% 33% 1.95 11.0 28 1.25 7.3 18 0.60 Market 11.4 1.00 Risk-free 6. 8 0 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio?

ALLLLL 23. You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio Rp Qe Bp 12.0% 33% 1.95 11.0 28 1.25 7.3 18 0.60 Market 11.4 1.00 Risk-free 6. 8 0 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio?

Question 3 (0.4 points) The following data are available for three portfolios and the market for...

Question 3 (0.4 points) The following data are available for three portfolios and the market for a recent 10-year period. Which portfolio has highest Jensen's alpha conditioning on CAPM risk-adjusted return? Portfolio Return (%) Std.Dev. (%) Beta 1 14 21 1.15 2 16 24 1.00 3 20 28 1.25 S&P 500 12 20 Risk-free rate 4 3 O2 S&P 500 1

Question 3 (0.4 points) The following data are available for three portfolios and the market for a recent 10-year period. Which portfolio has highest Jensen's alpha conditioning on CAPM risk-adjusted return? Portfolio Return (%) Std.Dev. (%) Beta 1 14 21 1.15 2 16 24 1.00 3 20 28 1.25 S&P 500 12 20 Risk-free rate 4 3 O2 S&P 500 1

Expected Portfolio Return Beta 22 0.8 A Market 173 1.0 D) Expected Portfolio Return Beta 30.28 1.8 A Market 198 1.0 If the simple CAPM is valid and all portfolios are priced correctly, which of the situations below is possible? Consider each situation independently, and assume the risk-free rate is 5% A) Expected Portfolio Return Beta 198 0.8 Market 198 1.0 B) Expected Standard Return Deviation Portfolio 228 88 A Market 17B 168

Expected Portfolio Return Beta 22 0.8 A Market 173 1.0 D) Expected Portfolio Return Beta 30.28 1.8 A Market 198 1.0 If the simple CAPM is valid and all portfolios are priced correctly, which of the situations below is possible? Consider each situation independently, and assume the risk-free rate is 5% A) Expected Portfolio Return Beta 198 0.8 Market 198 1.0 B) Expected Standard Return Deviation Portfolio 228 88 A Market 17B 168

15. Estimate the Sharpe, Treynor and Alpha Jensen's performance analyses fort the three portfolios below. Use the data below to complete the table. Portfolio Sharpe Treynor Jensen's Return 0.07 0.085 0.11 SD 0.15 0.12 0.095 Beta 0.8 1.05 1.4 Z 0.075 Market Risk Free 0.075 0.025 a. If you were to choose one portfolio, which one would it be? Why?

15. Estimate the Sharpe, Treynor and Alpha Jensen's performance analyses fort the three portfolios below. Use the data below to complete the table. Portfolio Sharpe Treynor Jensen's Return 0.07 0.085 0.11 SD 0.15 0.12 0.095 Beta 0.8 1.05 1.4 Z 0.075 Market Risk Free 0.075 0.025 a. If you were to choose one portfolio, which one would it be? Why?

Consider the following information Expected Standard Portfolio Return Deviation Risk-free 10% 1.0 Market 18 A 16 1.5 a. Calculate the return predicted by CAPM for a portfolio with a beta of 1.5 Return b. What is the alpha of portfolio A. (Negatlve value should be Indicated by a minus sign.) Alpha c. If the simple CAPM is valid, is the situation above possible? O Yes O No

Consider the following information Expected Standard Portfolio Return Deviation Risk-free 10% 1.0 Market 18 A 16 1.5 a. Calculate the return predicted by CAPM for a portfolio with a beta of 1.5 Return b. What is the alpha of portfolio A. (Negatlve value should be Indicated by a minus sign.) Alpha c. If the simple CAPM is valid, is the situation above possible? O Yes O No

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio RP 13.0% 12.0 7.0 10.1 5.0 op 30% 25 15 20 Bp 1.30 1.10 0.75 1.00 Market Risk-free 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicated by a minus sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Round your ratio answers...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio RP 13.0% 12.0 7.0 10.1 5.0 op 30% 25 15 20 Bp 1.30 1.10 0.75 1.00 Market Risk-free 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicated by a minus sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Round your ratio answers...

Parker has a portfolio with a beta of 1.0 and an a porttolio with a beta of 1.0 and an alpha of 0. Based on the CAPM, the return for the portfolio is a. 10% b. Greater than Rm. C. Equal to the Rm. d. Less than Rm but greater than R. ne TOKO Fund earns 11.2% during the year while the risk-free rate is 3.1%. The Yoko Fund has a beta of 1.20 and a standard deviation of 17.5%....

Parker has a portfolio with a beta of 1.0 and an a porttolio with a beta of 1.0 and an alpha of 0. Based on the CAPM, the return for the portfolio is a. 10% b. Greater than Rm. C. Equal to the Rm. d. Less than Rm but greater than R. ne TOKO Fund earns 11.2% during the year while the risk-free rate is 3.1%. The Yoko Fund has a beta of 1.20 and a standard deviation of 17.5%....

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk premium is 0.07, and the market risk premium has a standard deviation of 25%, then what is asset B's expected return under the CAPM?

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk...

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk premium is 0.07, and the market risk premium has a standard deviation of 25%, then what is asset B's expected return under the CAPM?

Asset A has a CAPM beta of 1.5. The covariance between asset A and asset B is 0.13. If the risk-free rate is 0.05, the expected market risk...

ALLLLL 23. You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio Rp Qe Bp 12.0% 33% 1.95 11.0 28 1.25 7.3 18 0.60 Market 11.4 1.00 Risk-free 6. 8 0 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio?

ALLLLL 23. You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio Rp Qe Bp 12.0% 33% 1.95 11.0 28 1.25 7.3 18 0.60 Market 11.4 1.00 Risk-free 6. 8 0 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio?

Question 3 (0.4 points) The following data are available for three portfolios and the market for a recent 10-year period. Which portfolio has highest Jensen's alpha conditioning on CAPM risk-adjusted return? Portfolio Return (%) Std.Dev. (%) Beta 1 14 21 1.15 2 16 24 1.00 3 20 28 1.25 S&P 500 12 20 Risk-free rate 4 3 O2 S&P 500 1

Question 3 (0.4 points) The following data are available for three portfolios and the market for a recent 10-year period. Which portfolio has highest Jensen's alpha conditioning on CAPM risk-adjusted return? Portfolio Return (%) Std.Dev. (%) Beta 1 14 21 1.15 2 16 24 1.00 3 20 28 1.25 S&P 500 12 20 Risk-free rate 4 3 O2 S&P 500 1

Most questions answered within 3 hours.

-

Let X be a continuous random variable whose PDF is Let X be a

continuous random...

asked 17 minutes ago -

Martinez Company’s relevant range of production is 7,500 units

to 12,500 units. When it produces and...

asked 15 minutes ago -

A football with a mass of 1.2 kg is kicked from ground level to

a height...

asked 21 minutes ago -

Remember: Changes in supply determinants shift supply, and

changes in demand determinants shift demand. We say...

asked 19 minutes ago -

Why is the answer b), for this question? I came up with C) for

my incorrect...

asked 25 minutes ago -

Suppose that you know that in the population of full-time

employees in the United States, the...

asked 47 minutes ago -

This experiment was designed originally to sample various meat and carcass quality

aspects of Ontario pigs...

asked 48 minutes ago -

Dopamine Hydrochloride: draw the structure And Show the

functional groups in different colors and label the...

asked 40 minutes ago -

A rope supports a 10 kg dumbbell hanging from it. What is the

tension in the...

asked 39 minutes ago -

) Raw materials are studied for contamination. Suppose that

the number of particles of contamination per...

asked 1 hour ago -

After running a regression analysis we calculated an F test and

the significance level was 0.15....

asked 58 minutes ago -

----Can someone please help me solve this one using JAVA

----I thank you in advance

Create...

asked 1 hour ago