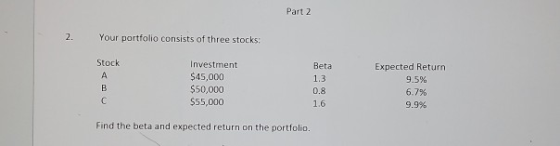

Complete showing all work (formulas, calc key strokes) for question #2

Homework Answers

| Stock | Investment | Beta | Expected return |

| A | 45000 | 1.3 | 9.5% |

| B | 50000 | 0.8 | 6.7% |

| C | 55000 | 1.6 | 9.9% |

Total amount invested in the portfolio = $45000 + 50000 + 55000 = $150000

Stock A

Weight of A = WA = Amount invested in A/Total amount invested in portfolio = 45000/150000 = 0.3

Beta of A = βA = 1.3

Return on A = RA = 9.5%

Stock B

Weight of B = WB = Amount invested in B/Total amount invested in portfolio = 50000/150000 = 10/30

Beta of B = βB = 0.8

Return on B = RB = 6.7%

Stock C

Weight of C = WC = Amount invested in C/Total amount invested in portfolio = 55000/150000 = 11/30

Beta of C = βC = 1.6

Return on C = RC = 9.9%

Portfolio

Beta of the portfolio is calculated using the formula:

Beta of portfolio = βP = WA*βA+WB*βB+WC*βC = 0.3*1.3 + ((10/30)*0.8) + ((11/30)*1.6) = 1.2433333

Expected return on the portfolio is calculated using the formula:

E[RP] = WA*RA+WB*RB+WC*RC = (0.3*9.5%) + ((10/30)*6.7%) + ((11/30)*9.9%) = 8.71333333%

Answers

Beta of the portfolio = 1.243333

Expected return on the portfolio = 8.713333%

Add Answer to:

Complete showing all work (formulas, calc key strokes)

for question #2

Part 2 2. Your portfolio...

Complete showing all work (formulas, calc key strokes) for question #3 3. Assume that the risk-free...

Complete showing all work (formulas, calc key strokes)

for question #3

3. Assume that the risk-free rate is 4 percent and that the market return is currently 7.5% a. Draw the SML b. Calculate and label the MRP. C. Given the data above, calculate the required return on Asset A with a beta of 1.3. d. Indicate Asset A on your graph

Complete showing all work (formulas, calc key strokes)

for question #3

3. Assume that the risk-free rate is 4 percent and that the market return is currently 7.5% a. Draw the SML b. Calculate and label the MRP. C. Given the data above, calculate the required return on Asset A with a beta of 1.3. d. Indicate Asset A on your graph

QUESTION 54 Your portfolio consists of $50,000 invested in Stock X and $50,000 invested in Stock ...

please assist with excel function or calculator

QUESTION 54 Your portfolio consists of $50,000 invested in Stock X and $50,000 invested in Stock Y. Both stocks have return of 15%, betas of 1.6, and standard deviations of 30%-The returns ofthe two stocks are independent correlation coefficient between them, xy, is zero. Which of the following statements best describes the cl your 2-stock portfolio? Your portfolio has a beta greater than 1.6, and its expected return is greater than 15% Your...

please assist with excel function or calculator

QUESTION 54 Your portfolio consists of $50,000 invested in Stock X and $50,000 invested in Stock Y. Both stocks have return of 15%, betas of 1.6, and standard deviations of 30%-The returns ofthe two stocks are independent correlation coefficient between them, xy, is zero. Which of the following statements best describes the cl your 2-stock portfolio? Your portfolio has a beta greater than 1.6, and its expected return is greater than 15% Your...

Portfolio X consists of 4 stocks which are A, B, C, and D. The information pertaining...

Portfolio X consists of 4 stocks which are A, B, C, and D. The information pertaining to the stocks, the portfolio and the market are given below: Stock Investment Beta A $25,000 0.8 B $25,000 1.2 C $25,000 Not Available D $25,000 Not Available Portfolio X $100,000 1 Expected return of the market = 10% Risk-free rate = 4% (a) Calculate the beta of Portfolio Y that is equally invested in stock A and stock B. b) Compute the beta...

Please show work/equations. Risk and Return Porfolio Weights and the Security Market Line Do not round...

Please show

work/equations.

Risk and Return Porfolio Weights and the Security Market Line Do not round any calculations From the Topic "Application of the SML"pp. 240-242 An investor wants to build a 2-stock portfolio of the following stocks: Stock Beta 1.3 0.85 Expected Return 7.80% 5.80% 14 If the investor wants the Portfolio Beta to be 1.1, what should the weights of each stock be in the portfolio? 16 sub-calc area Desired Portfolio beta: Weight of Stock A: Weight of...

Please show

work/equations.

Risk and Return Porfolio Weights and the Security Market Line Do not round any calculations From the Topic "Application of the SML"pp. 240-242 An investor wants to build a 2-stock portfolio of the following stocks: Stock Beta 1.3 0.85 Expected Return 7.80% 5.80% 14 If the investor wants the Portfolio Beta to be 1.1, what should the weights of each stock be in the portfolio? 16 sub-calc area Desired Portfolio beta: Weight of Stock A: Weight of...

Please solve for green boxes and please show excel formulas. Risk and Return Porfolio Weights and...

Please solve for green boxes and please show excel

formulas.

Risk and Return Porfolio Weights and the Security Market Line Do not round any calculations From the Topic "Application of the SML" pp. 240-242 An investor wants to build a 2-stock portfolio of the following stocks: Stock Beta 1.3 0.85 Expected Return 7.80% 5.80% If the investor wants the Portfolio Beta to be 1.1, what should the weights of each stock be in the portfolio? Desired Portfolio beta: Weight of...

Please solve for green boxes and please show excel

formulas.

Risk and Return Porfolio Weights and the Security Market Line Do not round any calculations From the Topic "Application of the SML" pp. 240-242 An investor wants to build a 2-stock portfolio of the following stocks: Stock Beta 1.3 0.85 Expected Return 7.80% 5.80% If the investor wants the Portfolio Beta to be 1.1, what should the weights of each stock be in the portfolio? Desired Portfolio beta: Weight of...

Please show all work using formulas, not a financial calculator. 2. You currently own a portfolio...

Please show all work using formulas, not a financial

calculator.

2. You currently own a portfolio of two stocks. JH Chemical has an expected return of 11% with a standard deviation of 15% while AAC Agriculture has an expected return of 15% with a standard deviation of 20%. The correlation coefficient between these two stocks is 0.30. a. (10 points) If you invest $14,000 in JH and $6,000 in AAC, what is the expected return and standard deviation of the...

Please show all work using formulas, not a financial

calculator.

2. You currently own a portfolio of two stocks. JH Chemical has an expected return of 11% with a standard deviation of 15% while AAC Agriculture has an expected return of 15% with a standard deviation of 20%. The correlation coefficient between these two stocks is 0.30. a. (10 points) If you invest $14,000 in JH and $6,000 in AAC, what is the expected return and standard deviation of the...

Please asnwer all the question 1) Your portfolio consists of $3,000 in ABC stock, $4,500 of...

Please asnwer all the question 1) Your portfolio consists of $3,000 in ABC stock, $4,500 of DEF stock and $2,500 of GHI stock. Expected rates of return are ABC 5%, DEF 12%, and GHI 16%. What is the portfolio expected rate of return? A) 10.9% B) 12.0% C) 11.4% D) 16.0% 2) You are considering investing in a portfolio consisting of 40% Electric General and 60% Buckstar. If the expected rate of return on Electric General is 16% and the...

Complete showing all work for question #1 FIN 202 Chapter 8 Homework Problems Part 1 Problems: SHOW ALL WORK. A corr...

Complete showing all work for question #1

FIN 202 Chapter 8 Homework Problems Part 1 Problems: SHOW ALL WORK. A correct answer without formulas, calculator keystrokes or work will receive ZERO credit. 1. State of Economy Rate of Return Probability of State of Economy Boom Normal Recession 20% 7096 10% 21% 13% -9% Find the expected return, standard deviation, and the coefficient of variation for the information provided above Part 2

Complete showing all work for question #1

FIN 202 Chapter 8 Homework Problems Part 1 Problems: SHOW ALL WORK. A correct answer without formulas, calculator keystrokes or work will receive ZERO credit. 1. State of Economy Rate of Return Probability of State of Economy Boom Normal Recession 20% 7096 10% 21% 13% -9% Find the expected return, standard deviation, and the coefficient of variation for the information provided above Part 2

Please show all work. Thanks! An optimal risky portfolio has been developed with investments in stocks...

Please show all work. Thanks!

An optimal risky portfolio has been developed with investments in stocks and bonds This optimal portfolio has 24% invested in bonds and the remainder invested in stocks The optimal portfolio mean return is 12.05% and its standard deviation is 18.45% The t-bill rate is 4.75%; what is the mean of the complete portfolio if 33% is invested in the optimal portfolio and theremainder is invested in T-bills? a What is the resulting allocation to stocks...

Please show all work. Thanks!

An optimal risky portfolio has been developed with investments in stocks and bonds This optimal portfolio has 24% invested in bonds and the remainder invested in stocks The optimal portfolio mean return is 12.05% and its standard deviation is 18.45% The t-bill rate is 4.75%; what is the mean of the complete portfolio if 33% is invested in the optimal portfolio and theremainder is invested in T-bills? a What is the resulting allocation to stocks...

please work all parts. 2. Stock A has expected return of 14% and volatility 30%. Stock...

please work all parts.

2. Stock A has expected return of 14% and volatility 30%. Stock B has expected return of 8% and volatility 19%. The correlation between two stocks is -0.2. The risk free interest rate is 4% (a) Find the expected returns, volatilities, and Sharpe ratios of portfolios that maintain 100.0% investment in Stock A and 100(1-x)% in Stock B, where x is given in the following table. Volatility Expected return Sharpe ratio 0.8 0.9 1.0 (b) How...

please work all parts.

2. Stock A has expected return of 14% and volatility 30%. Stock B has expected return of 8% and volatility 19%. The correlation between two stocks is -0.2. The risk free interest rate is 4% (a) Find the expected returns, volatilities, and Sharpe ratios of portfolios that maintain 100.0% investment in Stock A and 100(1-x)% in Stock B, where x is given in the following table. Volatility Expected return Sharpe ratio 0.8 0.9 1.0 (b) How...

Complete showing all work (formulas, calc key strokes)

for question #3

3. Assume that the risk-free rate is 4 percent and that the market return is currently 7.5% a. Draw the SML b. Calculate and label the MRP. C. Given the data above, calculate the required return on Asset A with a beta of 1.3. d. Indicate Asset A on your graph

Complete showing all work (formulas, calc key strokes)

for question #3

3. Assume that the risk-free rate is 4 percent and that the market return is currently 7.5% a. Draw the SML b. Calculate and label the MRP. C. Given the data above, calculate the required return on Asset A with a beta of 1.3. d. Indicate Asset A on your graph

please assist with excel function or calculator

QUESTION 54 Your portfolio consists of $50,000 invested in Stock X and $50,000 invested in Stock Y. Both stocks have return of 15%, betas of 1.6, and standard deviations of 30%-The returns ofthe two stocks are independent correlation coefficient between them, xy, is zero. Which of the following statements best describes the cl your 2-stock portfolio? Your portfolio has a beta greater than 1.6, and its expected return is greater than 15% Your...

please assist with excel function or calculator

QUESTION 54 Your portfolio consists of $50,000 invested in Stock X and $50,000 invested in Stock Y. Both stocks have return of 15%, betas of 1.6, and standard deviations of 30%-The returns ofthe two stocks are independent correlation coefficient between them, xy, is zero. Which of the following statements best describes the cl your 2-stock portfolio? Your portfolio has a beta greater than 1.6, and its expected return is greater than 15% Your...

Please show

work/equations.

Risk and Return Porfolio Weights and the Security Market Line Do not round any calculations From the Topic "Application of the SML"pp. 240-242 An investor wants to build a 2-stock portfolio of the following stocks: Stock Beta 1.3 0.85 Expected Return 7.80% 5.80% 14 If the investor wants the Portfolio Beta to be 1.1, what should the weights of each stock be in the portfolio? 16 sub-calc area Desired Portfolio beta: Weight of Stock A: Weight of...

Please show

work/equations.

Risk and Return Porfolio Weights and the Security Market Line Do not round any calculations From the Topic "Application of the SML"pp. 240-242 An investor wants to build a 2-stock portfolio of the following stocks: Stock Beta 1.3 0.85 Expected Return 7.80% 5.80% 14 If the investor wants the Portfolio Beta to be 1.1, what should the weights of each stock be in the portfolio? 16 sub-calc area Desired Portfolio beta: Weight of Stock A: Weight of...

Please solve for green boxes and please show excel

formulas.

Risk and Return Porfolio Weights and the Security Market Line Do not round any calculations From the Topic "Application of the SML" pp. 240-242 An investor wants to build a 2-stock portfolio of the following stocks: Stock Beta 1.3 0.85 Expected Return 7.80% 5.80% If the investor wants the Portfolio Beta to be 1.1, what should the weights of each stock be in the portfolio? Desired Portfolio beta: Weight of...

Please solve for green boxes and please show excel

formulas.

Risk and Return Porfolio Weights and the Security Market Line Do not round any calculations From the Topic "Application of the SML" pp. 240-242 An investor wants to build a 2-stock portfolio of the following stocks: Stock Beta 1.3 0.85 Expected Return 7.80% 5.80% If the investor wants the Portfolio Beta to be 1.1, what should the weights of each stock be in the portfolio? Desired Portfolio beta: Weight of...

Please show all work using formulas, not a financial

calculator.

2. You currently own a portfolio of two stocks. JH Chemical has an expected return of 11% with a standard deviation of 15% while AAC Agriculture has an expected return of 15% with a standard deviation of 20%. The correlation coefficient between these two stocks is 0.30. a. (10 points) If you invest $14,000 in JH and $6,000 in AAC, what is the expected return and standard deviation of the...

Please show all work using formulas, not a financial

calculator.

2. You currently own a portfolio of two stocks. JH Chemical has an expected return of 11% with a standard deviation of 15% while AAC Agriculture has an expected return of 15% with a standard deviation of 20%. The correlation coefficient between these two stocks is 0.30. a. (10 points) If you invest $14,000 in JH and $6,000 in AAC, what is the expected return and standard deviation of the...

Complete showing all work for question #1

FIN 202 Chapter 8 Homework Problems Part 1 Problems: SHOW ALL WORK. A correct answer without formulas, calculator keystrokes or work will receive ZERO credit. 1. State of Economy Rate of Return Probability of State of Economy Boom Normal Recession 20% 7096 10% 21% 13% -9% Find the expected return, standard deviation, and the coefficient of variation for the information provided above Part 2

Complete showing all work for question #1

FIN 202 Chapter 8 Homework Problems Part 1 Problems: SHOW ALL WORK. A correct answer without formulas, calculator keystrokes or work will receive ZERO credit. 1. State of Economy Rate of Return Probability of State of Economy Boom Normal Recession 20% 7096 10% 21% 13% -9% Find the expected return, standard deviation, and the coefficient of variation for the information provided above Part 2

Please show all work. Thanks!

An optimal risky portfolio has been developed with investments in stocks and bonds This optimal portfolio has 24% invested in bonds and the remainder invested in stocks The optimal portfolio mean return is 12.05% and its standard deviation is 18.45% The t-bill rate is 4.75%; what is the mean of the complete portfolio if 33% is invested in the optimal portfolio and theremainder is invested in T-bills? a What is the resulting allocation to stocks...

Please show all work. Thanks!

An optimal risky portfolio has been developed with investments in stocks and bonds This optimal portfolio has 24% invested in bonds and the remainder invested in stocks The optimal portfolio mean return is 12.05% and its standard deviation is 18.45% The t-bill rate is 4.75%; what is the mean of the complete portfolio if 33% is invested in the optimal portfolio and theremainder is invested in T-bills? a What is the resulting allocation to stocks...

please work all parts.

2. Stock A has expected return of 14% and volatility 30%. Stock B has expected return of 8% and volatility 19%. The correlation between two stocks is -0.2. The risk free interest rate is 4% (a) Find the expected returns, volatilities, and Sharpe ratios of portfolios that maintain 100.0% investment in Stock A and 100(1-x)% in Stock B, where x is given in the following table. Volatility Expected return Sharpe ratio 0.8 0.9 1.0 (b) How...

please work all parts.

2. Stock A has expected return of 14% and volatility 30%. Stock B has expected return of 8% and volatility 19%. The correlation between two stocks is -0.2. The risk free interest rate is 4% (a) Find the expected returns, volatilities, and Sharpe ratios of portfolios that maintain 100.0% investment in Stock A and 100(1-x)% in Stock B, where x is given in the following table. Volatility Expected return Sharpe ratio 0.8 0.9 1.0 (b) How...

Most questions answered within 3 hours.

-

What's the streaming business's problem on the

horizon?

asked 39 minutes ago -

I need help with writing the conclusion for this online lab

report

Abstract

By testing the...

asked 52 minutes ago -

For the reaction 1N2+3H2-----> 2NH3, would the reaction rate

trend be: delta[NH3]/ delta t = -2...

asked 1 hour ago -

Within your current/past organization, identify a problem/issue

and format a design to address same. You may...

asked 1 hour ago -

A sock stuck to the side of a clothes-dryer barrel has a

centripetal acceleration of 24...

asked 2 hours ago -

A perfect gas undergoes an isentropic process such that its

volume doubles. If the ratio of...

asked 2 hours ago -

list the elements in groups 3A to 6A in the same order as in the

periodic...

asked 2 hours ago -

Estimating effect size. Peng and Chen (2014)

evaluated effect size estimates for various tests. In their...

asked 2 hours ago -

Write a script in MySQL that creates and calls a stored

procedure name test. This procedure...

asked 2 hours ago -

If we test the following: H0: μ = 17

vs. H1: μ ≠ 17 and the...

asked 3 hours ago -

in the past year TVG had revenues of 3 million, cost

of goods sold of $25...

asked 3 hours ago -

4) In a polypeptide, which bond cannot rotate because of its

partial double bond character?

The...

asked 3 hours ago