Homework Answers

Please refer to below spreadsheet for calculation and answer. Cell reference also provided.

Cell reference -

Hope this will help, please do comment if you need any further explanation. Your feedback would be highly appreciated.

Add Answer to:

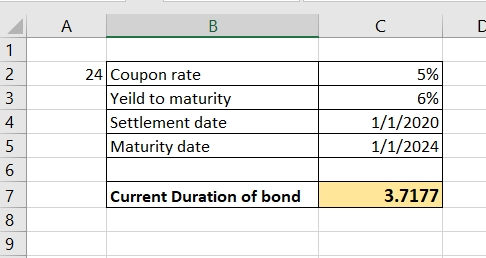

24. What is the current duration of a 4-period coupon bond with a periodic coupon rate...

Bond with: Par Value: $1,000 Maturity: 4 years Coupon Rate: 6% Current Annualized 6-month yield of...

Bond with: Par Value: $1,000 Maturity: 4 years Coupon Rate: 6% Current Annualized 6-month yield of 9%. Assume that coupon payments are made semiannually to bondholders and that the next coupon payment is expected in 6 months. 1.) What is the bond's duration (annualized)? Compare this with the approximate duration.

Find the duration of a 6% coupon bond making semiannually coupon payments if it has three...

Find the duration of a 6% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6%. What is the duration if the yield to maturity is 10%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) Duration 6% YTM years 10% YTM years

Find the duration of a 6% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6%. What is the duration if the yield to maturity is 10%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) Duration 6% YTM years 10% YTM years

Compute the duration of a bond with a face value of $1,000, a coupon rate of 7% (coupon is paid annually) and a maturity...

Compute the duration of a bond with a face value of $1,000, a coupon rate of 7% (coupon is paid annually) and a maturity of 10 years as the interest rate (or yield to maturity) on the bond changes from 2% to 12% (consider increments of 1% - so you need to compute the duration for various yields to maturity 2%, 3%, …, 12%) . What happens to duration as the interest rate increases?

Problem 16-5 Find the duration of a 4.0% coupon bond making semiannually coupon payments if it...

Problem 16-5 Find the duration of a 4.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) Years 6% YTM 8% YTM : Years

Problem 16-5 Find the duration of a 4.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) Years 6% YTM 8% YTM : Years

a. What is the difference between coupon rate and yield to maturity? How do you use...

a. What is the difference between coupon rate and yield to maturity? How do you use the coupon rate to calculate the periodic payment received from a bond? b. What is the price of a bond that is currently trading at a yield of 10% and has a face value of $1,000? This bond still has exactly 5 years to maturity. This bond pays semi-annual coupon at an annual rate of 8% (i.e., each coupon is 4%). Show how you...

You are considering a bond with a face value of $1 000 and a coupon rate...

You are considering a bond with a face value of $1 000 and a coupon rate of 2.0%. The bond has 16 year until maturity and coupon payments are paid semiannually. The yield to maturity on similar securities in the market is 8.3% Given the information provided, what is the per period coupon payment for this bond? What is the appropriate per period discount rate used to price this bond? What is the current price of this bond?

Find the duration of a 7.2% coupon bond making semiannually coupon payments if it has three...

Find the duration of a 7.2% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 10.0%? Note: The face value of the bond is $100. (Do not round Intermediate calculations. Round your answers to 4 decimal places.) 6% YTM 10% YTM

Find the duration of a 7.2% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 10.0%? Note: The face value of the bond is $100. (Do not round Intermediate calculations. Round your answers to 4 decimal places.) 6% YTM 10% YTM

Find the duration of a 7.4% coupon bond making semiannually coupon payments if it has three...

Find the duration of a 7.4% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 9.4%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM Years 9.4% YTM Years

Find the duration of a 7.4% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 9.4%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM Years 9.4% YTM Years

Find the duration of a 5.0% coupon bond making semiannually coupon payments if it has three...

Find the duration of a 5.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM Years 8% YTM Years

Find the duration of a 5.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM Years 8% YTM Years

Calculate the Duration and Modified Duration of each bond (already completed). Create a chart the shows...

Calculate the Duration and Modified Duration of each bond

(already completed). Create a chart the shows both measures

versus term to maturity. Does duration increase linearly

with term? If not, what relationship do you see?

А 2 Settlement Date 3 Maturity Date 4 Coupon Rate 5 Market Price 6 Face Value 7 Required Return 8 Frequency Bond A 2/15/2017 8/15/2027 4.00% 975.00 1,000.00 4.35% 2.00 Bond B 2/15/2017 5/15/2037 6.25% 1,062.00 1,000.00 5.50% 2.00 Bond C 2/15/2017 6/15/2047 7.40% 1,103.00...

Calculate the Duration and Modified Duration of each bond

(already completed). Create a chart the shows both measures

versus term to maturity. Does duration increase linearly

with term? If not, what relationship do you see?

А 2 Settlement Date 3 Maturity Date 4 Coupon Rate 5 Market Price 6 Face Value 7 Required Return 8 Frequency Bond A 2/15/2017 8/15/2027 4.00% 975.00 1,000.00 4.35% 2.00 Bond B 2/15/2017 5/15/2037 6.25% 1,062.00 1,000.00 5.50% 2.00 Bond C 2/15/2017 6/15/2047 7.40% 1,103.00...

Find the duration of a 6% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6%. What is the duration if the yield to maturity is 10%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) Duration 6% YTM years 10% YTM years

Find the duration of a 6% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6%. What is the duration if the yield to maturity is 10%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) Duration 6% YTM years 10% YTM years

Problem 16-5 Find the duration of a 4.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) Years 6% YTM 8% YTM : Years

Problem 16-5 Find the duration of a 4.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) Years 6% YTM 8% YTM : Years

Find the duration of a 7.2% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 10.0%? Note: The face value of the bond is $100. (Do not round Intermediate calculations. Round your answers to 4 decimal places.) 6% YTM 10% YTM

Find the duration of a 7.2% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 10.0%? Note: The face value of the bond is $100. (Do not round Intermediate calculations. Round your answers to 4 decimal places.) 6% YTM 10% YTM

Find the duration of a 7.4% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 9.4%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM Years 9.4% YTM Years

Find the duration of a 7.4% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 9.4%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM Years 9.4% YTM Years

Find the duration of a 5.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM Years 8% YTM Years

Find the duration of a 5.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM Years 8% YTM Years

Calculate the Duration and Modified Duration of each bond

(already completed). Create a chart the shows both measures

versus term to maturity. Does duration increase linearly

with term? If not, what relationship do you see?

А 2 Settlement Date 3 Maturity Date 4 Coupon Rate 5 Market Price 6 Face Value 7 Required Return 8 Frequency Bond A 2/15/2017 8/15/2027 4.00% 975.00 1,000.00 4.35% 2.00 Bond B 2/15/2017 5/15/2037 6.25% 1,062.00 1,000.00 5.50% 2.00 Bond C 2/15/2017 6/15/2047 7.40% 1,103.00...

Calculate the Duration and Modified Duration of each bond

(already completed). Create a chart the shows both measures

versus term to maturity. Does duration increase linearly

with term? If not, what relationship do you see?

А 2 Settlement Date 3 Maturity Date 4 Coupon Rate 5 Market Price 6 Face Value 7 Required Return 8 Frequency Bond A 2/15/2017 8/15/2027 4.00% 975.00 1,000.00 4.35% 2.00 Bond B 2/15/2017 5/15/2037 6.25% 1,062.00 1,000.00 5.50% 2.00 Bond C 2/15/2017 6/15/2047 7.40% 1,103.00...

Most questions answered within 3 hours.

-

Problem 1: Present entries to record the selected transactions

described below:

(a)

Issued $2,790,000 of 5-year,...

asked 2 minutes ago -

Using technology to support HR activities increases:

a.

the efficiency of the administrative HR functions.

b....

asked 2 minutes ago -

1. List the features used to classify leaf

types.

2. List some characteristics that are shared...

asked 7 minutes ago -

The three elements of Value Proposition, Key Customers, and

Capabilities operate within an environment. Which of...

asked 10 minutes ago -

Katelynn, a physician, earns $200,000 from her medical practice

in the current year. She receives $45,000...

asked 17 minutes ago -

Each row of the table below describes an aqueous solution at

25°C

.

The second column...

asked 22 minutes ago -

A horizontal wire is at y = 0. Current travels in the +x

direction. The magnetic...

asked 22 minutes ago -

Let X be a continuous random variable whose PDF is Let X be a

continuous random...

asked 43 minutes ago -

Martinez Company’s relevant range of production is 7,500 units

to 12,500 units. When it produces and...

asked 41 minutes ago -

A football with a mass of 1.2 kg is kicked from ground level to

a height...

asked 47 minutes ago -

Remember: Changes in supply determinants shift supply, and

changes in demand determinants shift demand. We say...

asked 46 minutes ago -

Why is the answer b), for this question? I came up with C) for

my incorrect...

asked 52 minutes ago