can someone please explain the illustration 16-1 and

illustration 16-1A to me. I have to understand this before the exam

tomorrow.

(I provided extra info if u need it)

Homework Answers

Solution 16-1 & 16-1A :-

Before explaining the question we need to understand the basic concept related to accounting for taxes on income -

Tax liability, in general is calculated on the taxable income as per income tax law. In comparison to accounting principles adopted in the financial statements, the tax laws allow quicker write off of assets and disallowance of certain expenses. As per MATCHING PRINCIPLE expenses are recognized in the in the profit and loss account based upon corresponding revenue generated by asset thereby. In simple terms Tax expense (Current tax plus Deferred tax) should be accounted for in the period in which the revenue is accounted.

A. Accounting income (loss) is the net profit or loss for a period, as reported in the statement of profit and loss, before deducting income tax expense or adding income tax saving.

B. Taxable income (tax loss) is the the amount of the income (loss) for a period, determined in accordance with the tax laws, based upon which tax payable (recoverable) is determined.

C. Tax expense (tax saving) is the aggregate of current tax and deferred tax charged or credited to the statement of profit and loss for the period. It is the amount expected to be paid using applicable tax rates.

D. Current Tax is the amount of income tax determined to be payable (recoverable) in respect of the taxable income (tax loss) for a period.

E. Deferred Tax is the tax effect of TIMING DIFFERENCES.

F. Timing Differences are the differences between taxable income and accounting income for a period that originate in one period and are capable of reversal in one or more subsequent periods.

G. Permanent Differences are the differences between taxable income and accounting income for a period that originate in one one period and do not reverse subsequently.

As explained above Tax expense is the aggregate of Current Tax and Deferred Tax.

Deferred Tax is the difference between tax expense and tax liability as per income tax law. It is measured as amount payable as per tax laws that have been force at the balance sheet date. Two differences (permanent differences and Temporary differences explained above) arises between accounting income and taxable income.

Deferred Tax liability is accounted in the books of accounts in following two situations where -

(i). Accounting income is greater than taxable income, and/or

(ii). Profit as per accounts but loss as per income tax law

Both the above stated situations leads to SAVE TAX NOW, PAY LATER. i.e. postponement of tax liability resulting in creation of deferred tax liability. In both the situations we will charge/Debit Profit & Loss Account thereby increasing income tax expense and credit Deferred Tax Liability.

In the year of reversing timing difference, Deferred tax liability is written back to Profit and Loss account. i.e. Debit deferred Tax liability and credit Profit and Loss account thereby reducing income tax expense.

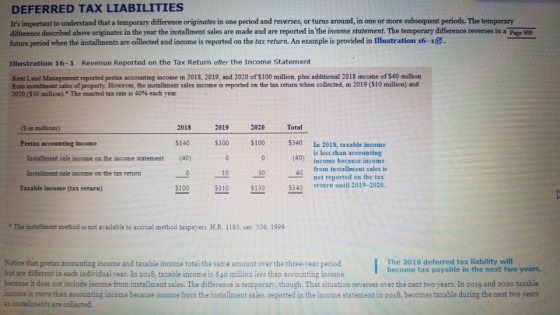

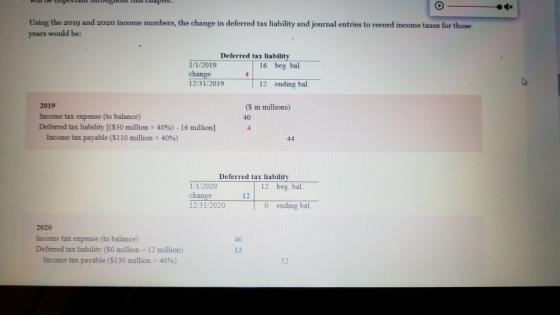

In the light of the above statement it is very much clear that pretax accounting income of 2018 is $140 which is greater than taxable return income of $100. Postponement of tax liability (save now & pay later). Hence, we will Debit Profit and Loss account by $16 thereby increasing income tax expense and credit Deferred Tax Liability of $16 (40% income tax rate of $40 which is a temporary difference created in 2018 and reversed in 2019 and 2020).

Income Tax Expense (Profit and Loss account) Dr. 56 (Balancing Figure)

To Deferred Tax Liability 16

To Income Tax Payable 40

Closing balance of Deferred tax Liability in 2018 - $16.

In the year 2019, where $10 is reversed on account of installment sale income on tax return. Hence, we will Debit Deferred Tax Liability of $4 (40% income tax rate of $10) and credit Profit and Loss account by $4 thereby reducing income tax expense by $4.

Income Tax Expense (Profit and Loss account) Dr. 40 (Balancing Figure)

Deferred Tax Liability Dr. 4

To Income Tax Payable 44

Closing balance of Deferred tax Liability in 2019 - $12 ($16-$4).

In the year 2020, where $30 is reversed on account of installment sale income on tax return. Hence, we will Debit Deferred Tax Liability of $12 (40% income tax rate of $30) and credit Profit and Loss account by $12 thereby reducing income tax expense by $12.

Income Tax Expense (Profit and Loss account) Dr. 40 (Balancing Figure)

Deferred Tax Liability Dr. 12

To Income Tax Payable 52

Closing balance of Deferred tax Liability in 2020 - $0 ($12-$12).

Add Answer to:

can someone please explain the illustration 16-1 and

illustration 16-1A to me. I have to understand...

please explain this illustration 16-A this is due tomorrow. what is happening here in this illustration?...

please explain this illustration 16-A

this is due tomorrow.

what is happening here in this illustration?

I need to know this before tomorrow.

Because tax laws permit the company to delay reporting this income as part of taxable the tax on that income. As shown in Illustration 16-iAC, that tax is not avoided, just deferred. income, the company is able to defer paying Illustration 16-1A Determining and Recording Income Taxes-2018 Future Taxable Amounts Current Year 2018 Future Taxable Amounts (total)...

please explain this illustration 16-A

this is due tomorrow.

what is happening here in this illustration?

I need to know this before tomorrow.

Because tax laws permit the company to delay reporting this income as part of taxable the tax on that income. As shown in Illustration 16-iAC, that tax is not avoided, just deferred. income, the company is able to defer paying Illustration 16-1A Determining and Recording Income Taxes-2018 Future Taxable Amounts Current Year 2018 Future Taxable Amounts (total)...

I don't understand why end 2019 is not $13 and why end of 2020 is not...

I don't understand why end 2019 is not $13

and why end of 2020 is not $5.

Ayres Services acquired an asset for $106 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: Pretax...

I don't understand why end 2019 is not $13

and why end of 2020 is not $5.

Ayres Services acquired an asset for $106 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: Pretax...

I really just need the journal entries and how income tax payable and expense are calculated...

I really just need the journal entries and

how income tax payable and expense are calculated for the entries

each year. Thank you

Ayres Services acquired an asset for $116 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020,...

I really just need the journal entries and

how income tax payable and expense are calculated for the entries

each year. Thank you

Ayres Services acquired an asset for $116 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020,...

Required Information Problem 16-8 Multiple differences; taxable income given; two years; balance sheet classification; change in...

Required Information Problem 16-8 Multiple differences; taxable income given; two years; balance sheet classification; change in tax rate (L016-4, 16-6, 16-8] [The following Information applies to the questions displayed below.] Arndt, Inc., reported the following for 2018 and 2019 ($ in millions): Revenues Expenses Pretax accounting income (income statement) Taxable income (tax return) Tax rate: 40% 2018 2019 $ 913 $988 770810 $ 143 $ 178 $ 135 $ 200 a. Expenses each year Include $30 million from a two-year...

Required Information Problem 16-8 Multiple differences; taxable income given; two years; balance sheet classification; change in tax rate (L016-4, 16-6, 16-8] [The following Information applies to the questions displayed below.] Arndt, Inc., reported the following for 2018 and 2019 ($ in millions): Revenues Expenses Pretax accounting income (income statement) Taxable income (tax return) Tax rate: 40% 2018 2019 $ 913 $988 770810 $ 143 $ 178 $ 135 $ 200 a. Expenses each year Include $30 million from a two-year...

Ayres Services acquired an asset for $88 million in 2018. The asset is depreciated for financial...

Ayres Services acquired an

asset for $88 million in 2018. The asset is depreciated for

financial reporting purposes over four years on a straight-line

basis (no residual value). For tax purposes the asset’s cost is

depreciated by MACRS. The enacted tax rate is 40%. Amounts for

pretax accounting income, depreciation, and taxable income in 2018,

2019, 2020, and 2021 are as follows:

Ayres Services acquired an asset for $88 million in 2018. The asset is depreciated for financial reporting purposes...

Ayres Services acquired an

asset for $88 million in 2018. The asset is depreciated for

financial reporting purposes over four years on a straight-line

basis (no residual value). For tax purposes the asset’s cost is

depreciated by MACRS. The enacted tax rate is 40%. Amounts for

pretax accounting income, depreciation, and taxable income in 2018,

2019, 2020, and 2021 are as follows:

Ayres Services acquired an asset for $88 million in 2018. The asset is depreciated for financial reporting purposes...

Ayres Services acquired an asset for $100 million in 2018. The asset is depreciated for financial...

Ayres Services acquired an asset for $100 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: Pretax accounting income Depreciation on the income statement Depreciation on the tax return Taxable income 2018 $ 380...

Ayres Services acquired an asset for $100 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: Pretax accounting income Depreciation on the income statement Depreciation on the tax return Taxable income 2018 $ 380...

r 16 Homework Assignmenti Saved Help Check my wor Ayres Services acquired an asset for $106...

r 16 Homework Assignmenti Saved Help Check my wor Ayres Services acquired an asset for $106 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-ine basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: (s in millions) 2018 2019 2020 2021 s 395...

r 16 Homework Assignmenti Saved Help Check my wor Ayres Services acquired an asset for $106 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-ine basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: (s in millions) 2018 2019 2020 2021 s 395...

Check my work Ayres Services acquired an asset for $104 million in 2018. The asset is...

Check my work Ayres Services acquired an asset for $104 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: points (8 04:07:01 Pretax accounting income Depreciation on the income statement Depreciation on the tax...

Check my work Ayres Services acquired an asset for $104 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: points (8 04:07:01 Pretax accounting income Depreciation on the income statement Depreciation on the tax...

Required information [The following information applies to the questions displayed below.] Arndt, Inc., reported the following...

Required information [The following information applies to the questions displayed below.] Arndt, Inc., reported the following for 2018 and 2019 ($ in millions): 2018 2019 $ 983 $ 888 Revenues Expenses Pretax accounting income (income statement) Taxable income (tax return) 760 800 $ 128 $ 120 $ 183 $ 200 Tax rate: 40% a. Expenses each year include $30 million from a two-year casualty insurance policy purchased in 2018 for $60 million. The cost is tax deductible in 2018. b....

Required information [The following information applies to the questions displayed below.] Arndt, Inc., reported the following for 2018 and 2019 ($ in millions): 2018 2019 $ 983 $ 888 Revenues Expenses Pretax accounting income (income statement) Taxable income (tax return) 760 800 $ 128 $ 120 $ 183 $ 200 Tax rate: 40% a. Expenses each year include $30 million from a two-year casualty insurance policy purchased in 2018 for $60 million. The cost is tax deductible in 2018. b....

R.S. reported pre-tax accounting income in 2017, 2018, and 2019 of $80 million, plus an additional...

R.S. reported pre-tax accounting income in 2017, 2018, and 2019 of $80 million, plus an additional 2018 income of $50 million from installment sales of property. However, the installment sales income is reported on the tax return when collected, in 2018 ($20 million) and 2019 ($30 million). The enacted tax rate is 40% each yr. Prepare the table calculating the annual tax payable for each yr. Prepare the journal entry for each yr. ............................. ..................... Current yr ..................Future Taxable amounts...

please explain this illustration 16-A

this is due tomorrow.

what is happening here in this illustration?

I need to know this before tomorrow.

Because tax laws permit the company to delay reporting this income as part of taxable the tax on that income. As shown in Illustration 16-iAC, that tax is not avoided, just deferred. income, the company is able to defer paying Illustration 16-1A Determining and Recording Income Taxes-2018 Future Taxable Amounts Current Year 2018 Future Taxable Amounts (total)...

please explain this illustration 16-A

this is due tomorrow.

what is happening here in this illustration?

I need to know this before tomorrow.

Because tax laws permit the company to delay reporting this income as part of taxable the tax on that income. As shown in Illustration 16-iAC, that tax is not avoided, just deferred. income, the company is able to defer paying Illustration 16-1A Determining and Recording Income Taxes-2018 Future Taxable Amounts Current Year 2018 Future Taxable Amounts (total)...

I don't understand why end 2019 is not $13

and why end of 2020 is not $5.

Ayres Services acquired an asset for $106 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: Pretax...

I don't understand why end 2019 is not $13

and why end of 2020 is not $5.

Ayres Services acquired an asset for $106 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: Pretax...

I really just need the journal entries and

how income tax payable and expense are calculated for the entries

each year. Thank you

Ayres Services acquired an asset for $116 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020,...

I really just need the journal entries and

how income tax payable and expense are calculated for the entries

each year. Thank you

Ayres Services acquired an asset for $116 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020,...

Required Information Problem 16-8 Multiple differences; taxable income given; two years; balance sheet classification; change in tax rate (L016-4, 16-6, 16-8] [The following Information applies to the questions displayed below.] Arndt, Inc., reported the following for 2018 and 2019 ($ in millions): Revenues Expenses Pretax accounting income (income statement) Taxable income (tax return) Tax rate: 40% 2018 2019 $ 913 $988 770810 $ 143 $ 178 $ 135 $ 200 a. Expenses each year Include $30 million from a two-year...

Required Information Problem 16-8 Multiple differences; taxable income given; two years; balance sheet classification; change in tax rate (L016-4, 16-6, 16-8] [The following Information applies to the questions displayed below.] Arndt, Inc., reported the following for 2018 and 2019 ($ in millions): Revenues Expenses Pretax accounting income (income statement) Taxable income (tax return) Tax rate: 40% 2018 2019 $ 913 $988 770810 $ 143 $ 178 $ 135 $ 200 a. Expenses each year Include $30 million from a two-year...

Ayres Services acquired an

asset for $88 million in 2018. The asset is depreciated for

financial reporting purposes over four years on a straight-line

basis (no residual value). For tax purposes the asset’s cost is

depreciated by MACRS. The enacted tax rate is 40%. Amounts for

pretax accounting income, depreciation, and taxable income in 2018,

2019, 2020, and 2021 are as follows:

Ayres Services acquired an asset for $88 million in 2018. The asset is depreciated for financial reporting purposes...

Ayres Services acquired an

asset for $88 million in 2018. The asset is depreciated for

financial reporting purposes over four years on a straight-line

basis (no residual value). For tax purposes the asset’s cost is

depreciated by MACRS. The enacted tax rate is 40%. Amounts for

pretax accounting income, depreciation, and taxable income in 2018,

2019, 2020, and 2021 are as follows:

Ayres Services acquired an asset for $88 million in 2018. The asset is depreciated for financial reporting purposes...

Ayres Services acquired an asset for $100 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: Pretax accounting income Depreciation on the income statement Depreciation on the tax return Taxable income 2018 $ 380...

Ayres Services acquired an asset for $100 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: Pretax accounting income Depreciation on the income statement Depreciation on the tax return Taxable income 2018 $ 380...

r 16 Homework Assignmenti Saved Help Check my wor Ayres Services acquired an asset for $106 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-ine basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: (s in millions) 2018 2019 2020 2021 s 395...

r 16 Homework Assignmenti Saved Help Check my wor Ayres Services acquired an asset for $106 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-ine basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: (s in millions) 2018 2019 2020 2021 s 395...

Check my work Ayres Services acquired an asset for $104 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: points (8 04:07:01 Pretax accounting income Depreciation on the income statement Depreciation on the tax...

Check my work Ayres Services acquired an asset for $104 million in 2018. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset's cost is depreciated by MACRS. The enacted tax rate is 40%. Amounts for pretax accounting income, depreciation, and taxable income in 2018, 2019, 2020, and 2021 are as follows: points (8 04:07:01 Pretax accounting income Depreciation on the income statement Depreciation on the tax...

Required information [The following information applies to the questions displayed below.] Arndt, Inc., reported the following for 2018 and 2019 ($ in millions): 2018 2019 $ 983 $ 888 Revenues Expenses Pretax accounting income (income statement) Taxable income (tax return) 760 800 $ 128 $ 120 $ 183 $ 200 Tax rate: 40% a. Expenses each year include $30 million from a two-year casualty insurance policy purchased in 2018 for $60 million. The cost is tax deductible in 2018. b....

Required information [The following information applies to the questions displayed below.] Arndt, Inc., reported the following for 2018 and 2019 ($ in millions): 2018 2019 $ 983 $ 888 Revenues Expenses Pretax accounting income (income statement) Taxable income (tax return) 760 800 $ 128 $ 120 $ 183 $ 200 Tax rate: 40% a. Expenses each year include $30 million from a two-year casualty insurance policy purchased in 2018 for $60 million. The cost is tax deductible in 2018. b....

Most questions answered within 3 hours.

-

A certain genetic characteristic of a particular plant can

appear in one of three forms (phenotypes)....

asked 11 minutes ago -

summarize Robert s. McNamara and the evolution of modern

management and the key point.

asked 10 minutes ago -

how many double bond equivalents are contained in a compound

with a molecular formula of C6H2F3I

asked 17 minutes ago -

A sample of pond sediment was diluted by placing a 0.1 g into

9.9 ml of...

asked 17 minutes ago -

A student performed an experiment using the same setup as the

one used in the lab...

asked 31 minutes ago -

predict the major product of nitration of bromobenzene, followed by

SnCl2 reduction

asked 40 minutes ago -

A standing wave with five antinodes is excited in a string of

length 2.5 m where...

asked 34 minutes ago -

An apnea monitor for adults consists of a flexible coil that

wraps around the chest, When...

asked 34 minutes ago -

Suppose the method of tree ring dating gave the following dates

A.D. for an archaeological excavation...

asked 1 hour ago -

Network security

1. explain succinctly how a Denial of Service attack may occur

on an implementation...

asked 54 minutes ago -

Name two of the basic guidelines for business dress that women

should follow in cultures other...

asked 55 minutes ago -

How can organizations create value by implementing an advanced

information system solution paired with the appropriate...

asked 56 minutes ago