The Energy Policy Act of 2005 and the Energy Independence and Security Act of 2007 mandated...

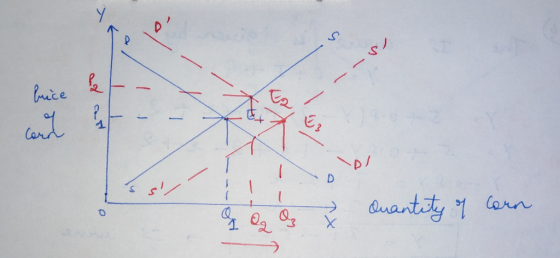

The Energy Policy Act of 2005 and the Energy Independence and Security Act of 2007 mandated enormous increases in ethanol consumption in the US. Most ethanol in the US is made from corn. Assuming that corn production takes place in a perfectly competitive market, explain what would happen to the price of corn in the global market as a result of these two laws? Use economic theory to explain what would happen to the number of corn farmers and production of corn in the long run in this market. Also, what should happen to prices in the long run? Explain your analysis using graphs and a few sentences.

Homework Answers

The initial equilibrium in the corn market occurs at point E1 where market demand and market supply curve intersects. The above two laws will increase the demand for corn in the corn market and thus shift the demand curve for corn rightwards to D'D' and new short run equilibrium occurs at point E2 where price level has risen to OP2 and quantity of corn has increased to OQ2. This increase in the price of corn will make it profitable for corn farmers and producers to produce corn and they will be earning supernormal profits. This will attract the entry of new firms in the market in the long and thus the supply curve of corn will shift rightwards to S'S' until prices fall to the initial price level at OP1 and thus new long run equilibrium occurs at point E3 where prices have fallen to OP1 and quantity of corn produced and sold has increased to OQ3.

Add Answer to:

The Energy Policy Act of 2005 and the Energy Independence and

Security Act of 2007 mandated...

what do you expect to happen in the long Suppose that the price of corn, a...

what do you expect to happen in the long

Suppose that the price of corn, a crop produced in a perfectly (or purely) competitive industry, increased 208 % last year as demand for corn based ethanol fuel increased. What do you expect to happen in the long run for the corn industry given this recent success? Suppose the firms in the market for bacon, also a perfectly (or purely) competitive industry, experienced losses last quarter the to people becoming increasingly...

what do you expect to happen in the long

Suppose that the price of corn, a crop produced in a perfectly (or purely) competitive industry, increased 208 % last year as demand for corn based ethanol fuel increased. What do you expect to happen in the long run for the corn industry given this recent success? Suppose the firms in the market for bacon, also a perfectly (or purely) competitive industry, experienced losses last quarter the to people becoming increasingly...

Assume that the perfectly competitive market for ethanol is in long-run equilibrium. Now suppose that the...

Assume that the perfectly competitive market for ethanol is in long-run equilibrium. Now suppose that the price of gasoline, a substitute for ethanol, increases. Explain what will happen in the market for ethanol. 1) Describe how this change will affect short-run economic profits. 2) What will happen to the number of firms producing ethanol in the long run? 3) How will price and output in this industry adjust in the long run?

Suppose that the price of corn, a crop produced in a perfectly (or purely) competitive industry,...

Suppose that the price of corn, a crop produced in a perfectly (or purely) competitive industry, increased 208% last year as demand for corn based ethanol fuel increased. What do you expect to happen in the long run for the corn industry given this recent success? The price per bushel of corn will continue to increase, yielding higher profits. Thus more firms will enter the market indefinitely. Profits will become negative due to over farming, which will result in the...

Suppose that the price of corn, a crop produced in a perfectly (or purely) competitive industry, increased 208% last year as demand for corn based ethanol fuel increased. What do you expect to happen in the long run for the corn industry given this recent success? The price per bushel of corn will continue to increase, yielding higher profits. Thus more firms will enter the market indefinitely. Profits will become negative due to over farming, which will result in the...

Problem 1. (13 points) Markets: Perfect Competition. Assume that a perfectly competitive, constant cost industry is...

Problem 1. (13 points) Markets: Perfect Competition. Assume that a perfectly competitive, constant cost industry is in a long run equilibrium with 35 firms. Each firm is producing 90 units of output which it sells at the price of $39 per unit; out of this amount each firm is paying $5 tax per unit of the output. The government decides to decrease the tax, so the firms will be paying $3 tax per unit. a) Explain what would happen in...

1. Draw two graphs. On the first, show the short-run profit maximizing output of an individual...

1. Draw two graphs. On the first, show the short-run profit maximizing output of an individual firm earning an economic profit, including MR, MC, AVC, and ATC. On the second, show the short-run market equilibrium price and quantity. Explain how the industry supply curve and the market equilibrium price and quantity are determined. 2. What is the relationship between the price on the two graphs? Why does this relationship exist? 3. Explain why a firm in a perfectly competitive industry...

Question 2: Suppose a market is having positive economic profit in the short run, what do you think will most like...

Question 2: Suppose a market is having positive economic profit in the short run, what do you think will most likely happen in the long run? 2.1 2.2 run? Explain in detail. Based on the lecture in the class, why would a firm choose to operate at a loss in the short When do firms decide to shut down production in the short run? Explain. 2.3. Question 3: For each of the following, is the business a price-taking producer? Explain...

Question 2: Suppose a market is having positive economic profit in the short run, what do you think will most likely happen in the long run? 2.1 2.2 run? Explain in detail. Based on the lecture in the class, why would a firm choose to operate at a loss in the short When do firms decide to shut down production in the short run? Explain. 2.3. Question 3: For each of the following, is the business a price-taking producer? Explain...

3 to 5 sentances each 1. Distinguish economies and diseconomies of scale. How can the extent...

3 to 5 sentances each

1. Distinguish economies and diseconomies of scale. How can the extent to which economies and one scale explain the size and number of real world firms in an industry? 2. Distinguish the short run from the long run Generally, what causes costs of production to vary with output in the short ruan? What generally causes costs of production to vary in the long run? 3. What is the difference between economic and accounting profit? Why...

3 to 5 sentances each

1. Distinguish economies and diseconomies of scale. How can the extent to which economies and one scale explain the size and number of real world firms in an industry? 2. Distinguish the short run from the long run Generally, what causes costs of production to vary with output in the short ruan? What generally causes costs of production to vary in the long run? 3. What is the difference between economic and accounting profit? Why...

Explain why a firm that is a monopoly may be beneficial for society. (10 marks) Paragraph...

Explain why a firm that is a monopoly may be beneficial for society. (10 marks) Paragraph B IDEE C2 Are the following markets perfectly competitive? Explain your answers. a) Potato farmers selling in a local market. (3 marks) b) Nancy Ajram, the famous Lebanese singer, concerts. (3 marks) c) SUVs (Sport Utility Vehicle). (4 marks) Pragraph B IDEE P 2 I a) What factors lead to an increase in Aggregate Demand?(4 marks) b) If aggregate demand increased with no change...

Explain why a firm that is a monopoly may be beneficial for society. (10 marks) Paragraph B IDEE C2 Are the following markets perfectly competitive? Explain your answers. a) Potato farmers selling in a local market. (3 marks) b) Nancy Ajram, the famous Lebanese singer, concerts. (3 marks) c) SUVs (Sport Utility Vehicle). (4 marks) Pragraph B IDEE P 2 I a) What factors lead to an increase in Aggregate Demand?(4 marks) b) If aggregate demand increased with no change...

Consider a small firm in a perfectly competitive industry. The firm is worth $600,000 and the...

Consider a small firm in a perfectly competitive industry. The firm is worth $600,000 and the return on investment elsewhere in the economy is 5.25 percent. Suppose the firm’s revenue in a year is $1.2 million and its operating expenses are $768,000. a. What is the firm’s accounting and economic profits in this case? b. Explain what would happen in this market in the long-run. What conditions are necessary for this to happen?

1. Suppose that a perfectly competitive industry is at a long-run equilibrium (each individual firm producing...

1. Suppose that a perfectly competitive industry is at a long-run equilibrium (each individual firm producing a quantity corresponding with minimum average cost). This implies that the following condition holds P = MC = AC. Assume that all firms have identical cost structures and the cost of inputs used in production (such as labor, raw material, intermediate goods, etc.) stays the same as the industry expands or contracts (i.e. constant-cost industry). a. Show with graphs and explain with words what...

1. Suppose that a perfectly competitive industry is at a long-run equilibrium (each individual firm producing a quantity corresponding with minimum average cost). This implies that the following condition holds P = MC = AC. Assume that all firms have identical cost structures and the cost of inputs used in production (such as labor, raw material, intermediate goods, etc.) stays the same as the industry expands or contracts (i.e. constant-cost industry). a. Show with graphs and explain with words what...

what do you expect to happen in the long

Suppose that the price of corn, a crop produced in a perfectly (or purely) competitive industry, increased 208 % last year as demand for corn based ethanol fuel increased. What do you expect to happen in the long run for the corn industry given this recent success? Suppose the firms in the market for bacon, also a perfectly (or purely) competitive industry, experienced losses last quarter the to people becoming increasingly...

what do you expect to happen in the long

Suppose that the price of corn, a crop produced in a perfectly (or purely) competitive industry, increased 208 % last year as demand for corn based ethanol fuel increased. What do you expect to happen in the long run for the corn industry given this recent success? Suppose the firms in the market for bacon, also a perfectly (or purely) competitive industry, experienced losses last quarter the to people becoming increasingly...

Suppose that the price of corn, a crop produced in a perfectly (or purely) competitive industry, increased 208% last year as demand for corn based ethanol fuel increased. What do you expect to happen in the long run for the corn industry given this recent success? The price per bushel of corn will continue to increase, yielding higher profits. Thus more firms will enter the market indefinitely. Profits will become negative due to over farming, which will result in the...

Suppose that the price of corn, a crop produced in a perfectly (or purely) competitive industry, increased 208% last year as demand for corn based ethanol fuel increased. What do you expect to happen in the long run for the corn industry given this recent success? The price per bushel of corn will continue to increase, yielding higher profits. Thus more firms will enter the market indefinitely. Profits will become negative due to over farming, which will result in the...

Question 2: Suppose a market is having positive economic profit in the short run, what do you think will most likely happen in the long run? 2.1 2.2 run? Explain in detail. Based on the lecture in the class, why would a firm choose to operate at a loss in the short When do firms decide to shut down production in the short run? Explain. 2.3. Question 3: For each of the following, is the business a price-taking producer? Explain...

Question 2: Suppose a market is having positive economic profit in the short run, what do you think will most likely happen in the long run? 2.1 2.2 run? Explain in detail. Based on the lecture in the class, why would a firm choose to operate at a loss in the short When do firms decide to shut down production in the short run? Explain. 2.3. Question 3: For each of the following, is the business a price-taking producer? Explain...

3 to 5 sentances each

1. Distinguish economies and diseconomies of scale. How can the extent to which economies and one scale explain the size and number of real world firms in an industry? 2. Distinguish the short run from the long run Generally, what causes costs of production to vary with output in the short ruan? What generally causes costs of production to vary in the long run? 3. What is the difference between economic and accounting profit? Why...

3 to 5 sentances each

1. Distinguish economies and diseconomies of scale. How can the extent to which economies and one scale explain the size and number of real world firms in an industry? 2. Distinguish the short run from the long run Generally, what causes costs of production to vary with output in the short ruan? What generally causes costs of production to vary in the long run? 3. What is the difference between economic and accounting profit? Why...

Explain why a firm that is a monopoly may be beneficial for society. (10 marks) Paragraph B IDEE C2 Are the following markets perfectly competitive? Explain your answers. a) Potato farmers selling in a local market. (3 marks) b) Nancy Ajram, the famous Lebanese singer, concerts. (3 marks) c) SUVs (Sport Utility Vehicle). (4 marks) Pragraph B IDEE P 2 I a) What factors lead to an increase in Aggregate Demand?(4 marks) b) If aggregate demand increased with no change...

Explain why a firm that is a monopoly may be beneficial for society. (10 marks) Paragraph B IDEE C2 Are the following markets perfectly competitive? Explain your answers. a) Potato farmers selling in a local market. (3 marks) b) Nancy Ajram, the famous Lebanese singer, concerts. (3 marks) c) SUVs (Sport Utility Vehicle). (4 marks) Pragraph B IDEE P 2 I a) What factors lead to an increase in Aggregate Demand?(4 marks) b) If aggregate demand increased with no change...

1. Suppose that a perfectly competitive industry is at a long-run equilibrium (each individual firm producing a quantity corresponding with minimum average cost). This implies that the following condition holds P = MC = AC. Assume that all firms have identical cost structures and the cost of inputs used in production (such as labor, raw material, intermediate goods, etc.) stays the same as the industry expands or contracts (i.e. constant-cost industry). a. Show with graphs and explain with words what...

1. Suppose that a perfectly competitive industry is at a long-run equilibrium (each individual firm producing a quantity corresponding with minimum average cost). This implies that the following condition holds P = MC = AC. Assume that all firms have identical cost structures and the cost of inputs used in production (such as labor, raw material, intermediate goods, etc.) stays the same as the industry expands or contracts (i.e. constant-cost industry). a. Show with graphs and explain with words what...

Most questions answered within 3 hours.

-

Calculate the pH of each of the following solutions.

0.50 M HBr

3.1×10−4 M KOH

4.2×10−5...

asked 3 hours ago -

For the year ended December 31, Depot Max’s cost of merchandise

sold was $85,600. Inventory at the...

asked 3 hours ago -

Week 10 - Professional Memo Assignment

Professional Memo Assignment

Your mission for this week, should you...

asked 3 hours ago -

Write a Python program that stores the data for each

player on the team, and it...

asked 3 hours ago -

In

the last 3 months, mike never knows when he is going to get his

allowance...

asked 3 hours ago -

Is Ca(OH)2 a Bronsted base, Lewis base, or both? Why?

asked 3 hours ago -

1A- Why don’t voters complain about U.S. tariffs on imported

sugar?

Because sugar is only a...

asked 3 hours ago -

Cash Payback Period

Primera Banco is evaluating two capital investment proposals for

a drive-up ATM kiosk,...

asked 3 hours ago -

Create a button in Swift (Xcode) that will create a charge,

create a charge using Stripe's...

asked 3 hours ago -

The reaction rate of CO and NO2 in the reaction

CO(g) + NO2(g) → CO2(g) +...

asked 3 hours ago -

Imagine that a chemist puts 6.40 mol each of

C3H8 and O2 in a 1.00-L container...

asked 4 hours ago -

How much money should be invested today in order to have $8340

at the end of...

asked 4 hours ago