Problem 1. (13 points) Markets: Perfect Competition. Assume that a perfectly competitive, constant cost industry is...

Problem 1. (13 points) Markets: Perfect Competition.

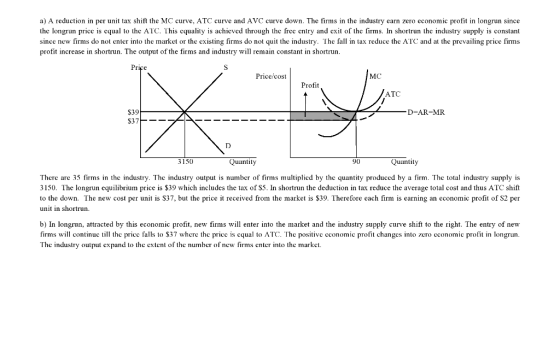

Assume that a perfectly competitive, constant cost industry is in a long run equilibrium with 35 firms. Each firm is producing 90 units of output which it sells at the price of $39 per unit; out of this amount each firm is paying $5 tax per unit of the output. The government decides to decrease the tax, so the firms will be paying $3 tax per unit.

-

a) Explain what would happen in the short run to the equilibrium price and industry output; number of firms in the industry; output and profit of each firm. Illustrate on diagrams for the market and a particular firm.

-

b) Explain what would happen in the long run to the equilibrium price and industry output; number of firms in the industry; output and profit of each firm. Illustrate on diagrams for the market and a particular firm. Compare to the initial long run equilibrium and to the short run equilibrium found in a).

Your answer to this question should include graphs and explanations in words; please use complete sentences (not dot points). Please note that the numbers are provided for convenience; you should indicate them on graphs, but you are not expected to do any calculations.

Homework Answers

Add Answer to:

Problem 1. (13 points) Markets: Perfect Competition.

Assume that a perfectly competitive, constant cost industry is...

The first picture below depicts the cost curves for a representative firm in this perfectly competitive industry. Initia...

The first picture below depicts the cost curves for a

representative firm in this perfectly competitive industry.

Initially, there are 100 firms. The second picture depicts market

demand.

A) Suppose that the firm produces 300 units of output, how much

are their total costs?

B) What is the short-run equilibrium price?

C) At the short-run equilibrium price, what is the quantity

produced by each firm?

D) At the short-run equilibrium price, what is per-firm

profit?

E) In the long-run,...

The first picture below depicts the cost curves for a

representative firm in this perfectly competitive industry.

Initially, there are 100 firms. The second picture depicts market

demand.

A) Suppose that the firm produces 300 units of output, how much

are their total costs?

B) What is the short-run equilibrium price?

C) At the short-run equilibrium price, what is the quantity

produced by each firm?

D) At the short-run equilibrium price, what is per-firm

profit?

E) In the long-run,...

1. (20p) Suppose that, in a perfectly competitive industry, the technology for making the product (by...

1. (20p) Suppose that, in a perfectly competitive industry, the technology for making the product (by any single firm) has the total cost function c(q) = 200 + 4q+ Barriers to entry and exit the market are low and an unlimited number of firms could enter this industry, all with the same total cost function. (a) Compute the long-run equilibrium price in this industry, as well as the amount of output each firm would produce at this price. Explain the...

1. (20p) Suppose that, in a perfectly competitive industry, the technology for making the product (by any single firm) has the total cost function c(q) = 200 + 4q+ Barriers to entry and exit the market are low and an unlimited number of firms could enter this industry, all with the same total cost function. (a) Compute the long-run equilibrium price in this industry, as well as the amount of output each firm would produce at this price. Explain the...

Assume that pistachios are produced in a perfectly competitive constant-cost industry. *****I JUST NEED part C...

Assume that pistachios are produced in a perfectly competitive constant-cost industry. *****I JUST NEED part C AND D ANSWERED NOT A AND B, JUST INCLUDED FOR REFERENCE TO PROBLEM****** a. The market for pistachios is in a full long-run equilibrium state. Use side-by-side diagrams for the market and a typical firm to illustrate the equilibrium, being sure to include price, market output, the output of the typical firm and relevant cost curves.. b. Now assume that there is an increase...

4. (8 points) A competitive industry is in long-run equilibrium. An excise tax is then placed...

4. (8 points) A competitive industry is in long-run equilibrium. An excise tax is then placed on all firms in the industry a. Explain what you expect to happen to the price of the product, the number of firms in the industry, and the output of each firm in the short run: b. Explain what you expect to happen in the long run to the price of the product, the number of firms in the industry, and the output of...

4. (8 points) A competitive industry is in long-run equilibrium. An excise tax is then placed on all firms in the industry a. Explain what you expect to happen to the price of the product, the number of firms in the industry, and the output of each firm in the short run: b. Explain what you expect to happen in the long run to the price of the product, the number of firms in the industry, and the output of...

14. (Perfect Competition) Apples are produced in a perfectly competitive industry. As- sume that there are...

14. (Perfect Competition) Apples are produced in a perfectly competitive industry. As- sume that there are 100 identical firms in this industry. Below are graphs for the market supply and demand as well as the cost curves of these firms 6 MC ATC AVC 2 0 0 0 100 200 300 400 500 600 0 1 23 4 5 6 Q(kg) q(kg) (a) Draw the market supply curve for apples (b) What are the market price and quantity for apples?...

14. (Perfect Competition) Apples are produced in a perfectly competitive industry. As- sume that there are 100 identical firms in this industry. Below are graphs for the market supply and demand as well as the cost curves of these firms 6 MC ATC AVC 2 0 0 0 100 200 300 400 500 600 0 1 23 4 5 6 Q(kg) q(kg) (a) Draw the market supply curve for apples (b) What are the market price and quantity for apples?...

3. Perfect Competition Market (Total 8 points) a. For a perfectly competitive firm, illustrate a case...

3. Perfect Competition Market (Total 8 points) a. For a perfectly competitive firm, illustrate a case where the firm is facing PMC SRATC LRATC by using yin the following diagram. In this diagram, you should include demand curve (d), marginal cost curve (MC), short run average total cost curve (SRATC), and long run average total cost curve (LRATC). Remember to label all axes. (2 points) pves vwerase totail cost curve (SRATC,aushould include demandcun b. Does the firm exhibit productive efficiency?...

3. Perfect Competition Market (Total 8 points) a. For a perfectly competitive firm, illustrate a case where the firm is facing PMC SRATC LRATC by using yin the following diagram. In this diagram, you should include demand curve (d), marginal cost curve (MC), short run average total cost curve (SRATC), and long run average total cost curve (LRATC). Remember to label all axes. (2 points) pves vwerase totail cost curve (SRATC,aushould include demandcun b. Does the firm exhibit productive efficiency?...

a) Using both market and firm graphs for a perfectly competitive industry, show the effect of...

a) Using both market and firm graphs for a perfectly competitive industry, show the effect of an increase in consumers’ income taxes. Assume the representative firm and market begin in long run equilibrium. Illustrate the short run effect on price, output, and profits, assuming this firm does not shut down. Label your graphs and explain your answer. b) Assuming the representative firm does not withdraw from the market, show the long run effect on price, output, and profits. Label your...

Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and...

Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and have the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. Assume also that it does not matter how many firms are in the industry Tool Tip: Place the mouse cursor over orange square points on the MC curve to see coordinates. COST PER UNIT IDollars per pound) 10 MC ATC AVC 0 5...

Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and have the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. Assume also that it does not matter how many firms are in the industry Tool Tip: Place the mouse cursor over orange square points on the MC curve to see coordinates. COST PER UNIT IDollars per pound) 10 MC ATC AVC 0 5...

The market for cashews is perfectly competitive and comprised of fifty (50) firms with identical cost...

The market for cashews is perfectly competitive and comprised of fifty (50) firms with identical cost structures and U-shaped ATC curves. The market demand curve for cashews is downward-sloping. The industry is initially in long run equilibrium at the following market price and quantity P* = $4/pound Q* = 50 pounds of cashews In TWO, well-labeled graphs (side by side), depict this long run equilibrium for both the cashew market and for the individual cashew firm. Be sure to calculate...

The market for cashews is perfectly competitive and comprised of fifty (50) firms with identical cost structures and U-shaped ATC curves. The market demand curve for cashews is downward-sloping. The industry is initially in long run equilibrium at the following market price and quantity P* = $4/pound Q* = 50 pounds of cashews In TWO, well-labeled graphs (side by side), depict this long run equilibrium for both the cashew market and for the individual cashew firm. Be sure to calculate...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

The first picture below depicts the cost curves for a

representative firm in this perfectly competitive industry.

Initially, there are 100 firms. The second picture depicts market

demand.

A) Suppose that the firm produces 300 units of output, how much

are their total costs?

B) What is the short-run equilibrium price?

C) At the short-run equilibrium price, what is the quantity

produced by each firm?

D) At the short-run equilibrium price, what is per-firm

profit?

E) In the long-run,...

The first picture below depicts the cost curves for a

representative firm in this perfectly competitive industry.

Initially, there are 100 firms. The second picture depicts market

demand.

A) Suppose that the firm produces 300 units of output, how much

are their total costs?

B) What is the short-run equilibrium price?

C) At the short-run equilibrium price, what is the quantity

produced by each firm?

D) At the short-run equilibrium price, what is per-firm

profit?

E) In the long-run,...

1. (20p) Suppose that, in a perfectly competitive industry, the technology for making the product (by any single firm) has the total cost function c(q) = 200 + 4q+ Barriers to entry and exit the market are low and an unlimited number of firms could enter this industry, all with the same total cost function. (a) Compute the long-run equilibrium price in this industry, as well as the amount of output each firm would produce at this price. Explain the...

1. (20p) Suppose that, in a perfectly competitive industry, the technology for making the product (by any single firm) has the total cost function c(q) = 200 + 4q+ Barriers to entry and exit the market are low and an unlimited number of firms could enter this industry, all with the same total cost function. (a) Compute the long-run equilibrium price in this industry, as well as the amount of output each firm would produce at this price. Explain the...

4. (8 points) A competitive industry is in long-run equilibrium. An excise tax is then placed on all firms in the industry a. Explain what you expect to happen to the price of the product, the number of firms in the industry, and the output of each firm in the short run: b. Explain what you expect to happen in the long run to the price of the product, the number of firms in the industry, and the output of...

4. (8 points) A competitive industry is in long-run equilibrium. An excise tax is then placed on all firms in the industry a. Explain what you expect to happen to the price of the product, the number of firms in the industry, and the output of each firm in the short run: b. Explain what you expect to happen in the long run to the price of the product, the number of firms in the industry, and the output of...

14. (Perfect Competition) Apples are produced in a perfectly competitive industry. As- sume that there are 100 identical firms in this industry. Below are graphs for the market supply and demand as well as the cost curves of these firms 6 MC ATC AVC 2 0 0 0 100 200 300 400 500 600 0 1 23 4 5 6 Q(kg) q(kg) (a) Draw the market supply curve for apples (b) What are the market price and quantity for apples?...

14. (Perfect Competition) Apples are produced in a perfectly competitive industry. As- sume that there are 100 identical firms in this industry. Below are graphs for the market supply and demand as well as the cost curves of these firms 6 MC ATC AVC 2 0 0 0 100 200 300 400 500 600 0 1 23 4 5 6 Q(kg) q(kg) (a) Draw the market supply curve for apples (b) What are the market price and quantity for apples?...

3. Perfect Competition Market (Total 8 points) a. For a perfectly competitive firm, illustrate a case where the firm is facing PMC SRATC LRATC by using yin the following diagram. In this diagram, you should include demand curve (d), marginal cost curve (MC), short run average total cost curve (SRATC), and long run average total cost curve (LRATC). Remember to label all axes. (2 points) pves vwerase totail cost curve (SRATC,aushould include demandcun b. Does the firm exhibit productive efficiency?...

3. Perfect Competition Market (Total 8 points) a. For a perfectly competitive firm, illustrate a case where the firm is facing PMC SRATC LRATC by using yin the following diagram. In this diagram, you should include demand curve (d), marginal cost curve (MC), short run average total cost curve (SRATC), and long run average total cost curve (LRATC). Remember to label all axes. (2 points) pves vwerase totail cost curve (SRATC,aushould include demandcun b. Does the firm exhibit productive efficiency?...

Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and have the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. Assume also that it does not matter how many firms are in the industry Tool Tip: Place the mouse cursor over orange square points on the MC curve to see coordinates. COST PER UNIT IDollars per pound) 10 MC ATC AVC 0 5...

Consider a perfectly competitive market for titanium. Assume that all firms in the industry are identical and have the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. Assume also that it does not matter how many firms are in the industry Tool Tip: Place the mouse cursor over orange square points on the MC curve to see coordinates. COST PER UNIT IDollars per pound) 10 MC ATC AVC 0 5...

The market for cashews is perfectly competitive and comprised of fifty (50) firms with identical cost structures and U-shaped ATC curves. The market demand curve for cashews is downward-sloping. The industry is initially in long run equilibrium at the following market price and quantity P* = $4/pound Q* = 50 pounds of cashews In TWO, well-labeled graphs (side by side), depict this long run equilibrium for both the cashew market and for the individual cashew firm. Be sure to calculate...

The market for cashews is perfectly competitive and comprised of fifty (50) firms with identical cost structures and U-shaped ATC curves. The market demand curve for cashews is downward-sloping. The industry is initially in long run equilibrium at the following market price and quantity P* = $4/pound Q* = 50 pounds of cashews In TWO, well-labeled graphs (side by side), depict this long run equilibrium for both the cashew market and for the individual cashew firm. Be sure to calculate...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

Most questions answered within 3 hours.

-

Suppose that you are an official with Mexico's economic

development agency. Write a one-page memo detailing...

asked 27 minutes ago -

If you were an international firm, why would you support the

concept of global free trade?...

asked 42 minutes ago -

Cisco packet tracer

Q1) Do you get any changes of IP address when packet is

traversing...

asked 1 hour ago -

What is the pressure inside a 33.0 L container holding 106.4 kg

of argon gas at...

asked 2 hours ago -

Question no 2

A housekeeping support department budgets its costs at

SR 40,000 per month plus...

asked 2 hours ago -

A 1400Kg sports car accelerates from rest to 90km/h in 7.0s.

What is the average power...

asked 2 hours ago -

For the following reaction, 0.128 moles of

potassium hydrogen sulfateare mixed with

0.504 moles of potassium...

asked 6 hours ago -

1. What is the present value of $400, three years in the future

if the interest...

asked 6 hours ago -

The labor force minus the number of employed equals the number

of unemployed.

a. True

b....

asked 9 hours ago -

Determine the mass in units of grams [g] of 0.49 moles [mol]

of a new fictitious...

asked 9 hours ago -

A horizontal mass of M=5kg is on a spring and stretched to

x=0.5m when released from...

asked 10 hours ago -

26 of 50

"I have worked at the Arizona Humane Society for ten years, and

have...

asked 11 hours ago