(Appendix 4B) Support Department Cost Allocation: Comparison of Methods of Allocation

Objective 6Bender Automotive

Works Inc. manufactures a variety of front-end assemblies for

automobiles. A front-end assembly is the unified front of an

automobile that includes the headlamps, fender, and surrounding

metal/plastic. Bender has two producing departments: Drilling and

Assembly. Usually, the front-end assemblies are ordered in batches

of 100.

Objective 6Bender Automotive

Works Inc. manufactures a variety of front-end assemblies for

automobiles. A front-end assembly is the unified front of an

automobile that includes the headlamps, fender, and surrounding

metal/plastic. Bender has two producing departments: Drilling and

Assembly. Usually, the front-end assemblies are ordered in batches

of 100.

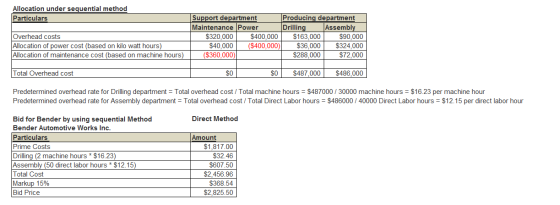

Two support departments provide support for Bender's producing departments: Maintenance and Power. Budgeted data for the coming quarter follow. The company does not separate fixed and variable costs.

| Support Departments | Producing Departments | ||||

|---|---|---|---|---|---|

| Maintenance | Power | Drilling | Assembly | ||

| Overhead costs | $320,000 | $400,000 | $163,000 | $90,000 | |

| Machine hours | — | 22,500 | 30,000 | 7,500 | |

| Kilowatt-hours | 40,000 | — | 36,000 | 324,000 | |

| Direct labor hours | — | — | 5,000 | 40,000 | |

The predetermined overhead rate for Drilling is computed on the basis of machine hours. Direct labor hours are used for Assembly.

Recently, a truck manufacturer requested a bid on a 3-year contract that would supply front-end assemblies to a nearby factory. The prime costs for a batch of 100 front-end assemblies are $1,817. It takes two machine hours to produce a batch in the drilling department and 50 direct labor hours to assemble the 100 front-end assemblies in the assembly department.

Bender's policy is to bid full manufacturing cost, plus 15%. (Note: Round allocation ratios to four decimal places, allocated support department cost to the nearest dollar, and the job cost components to the nearest cent.)

Required:

-

Prepare bids for Bender by using each of the following allocation methods: (a) direct method and (b) sequential method, allocating power costs first. (Note: Round allocation ratios to four decimal places, allocated support department cost to the nearest dollar, and the job cost components to the nearest cent.)

Homework Answers

Answer A

Answer B

Add Answer to:

(Appendix 4B) Support Department Cost Allocation:

Comparison of Methods of Allocation

Objective 6Bender Automotive

Works Inc....

(Appendix 4B) Sequential Method of Support Department Cost Allocation Stevenson Company is divided into two operating...

(Appendix 4B) Sequential Method of Support Department Cost Allocation Stevenson Company is divided into two operating divisions: Battery and Small Motors. The company allocates power and general factory costs to each operating division using the sequential method. General Factory is allocated first in the sequential method for the company. Support department cost allocations using the sequential method are based on the following data: Support Departments Operating Divisions Power General Factory Battery Small Motors Overhead costs $160,000 $430,000 $163,000 $84,600 Machine...

(Appendix 4B) Direct Method of Support Department Cost Allocation Stevenson Company is divided into two operating...

(Appendix 4B) Direct Method of Support Department Cost Allocation Stevenson Company is divided into two operating divisions: Battery and Small Motors. The company allocates power and general factory costs to each operating division using the direct method. Power costs are allocated on the basis of the number of machine hours and general factory costs on the basis of square footage. Support department cost allocations using the direct method are based on the following data: Support Departments Operating Divisions Power General...

(Appendix 4B) Sequential Method of Support Department Cost Allocation Stevenson Company is divided into two operating...

(Appendix 4B) Sequential Method of Support Department Cost Allocation Stevenson Company is divided into two operating divisions: Battery and Small Motors. The company allocates power and general factory costs to each operating division using the sequential method. General Factory is allocated first in the sequential method for the company. Support department cost allocations using the sequential method are based on the following data: Support Departments Operating Divisions General Factory Small Motors Power Battery Overhead costs $430,000 $84,600 $160,000 2,000 $163,000...

(Appendix 4B) Sequential Method of Support Department Cost Allocation Stevenson Company is divided into two operating divisions: Battery and Small Motors. The company allocates power and general factory costs to each operating division using the sequential method. General Factory is allocated first in the sequential method for the company. Support department cost allocations using the sequential method are based on the following data: Support Departments Operating Divisions General Factory Small Motors Power Battery Overhead costs $430,000 $84,600 $160,000 2,000 $163,000...

Direct Method of Support Department Cost Allocation Valron Company has two support departments, Human Resources an...

Direct Method of Support Department Cost Allocation Valron Company has two support departments, Human Resources and General Factory, and two producing departments, Fabricating and Assembly Support Departments Producing Departments Human Resources General Factory Fabricating Assembly Direct costs $160,000 $340,000 $114,600 $93,000 Normal activity: Number of employees 60 80 120 170 Square footage 1,000 5,700 13,300 The costs of the Human Resources Department are allocated on the basis of number of employees, and the costs of General Factory are allocated on...

Direct Method of Support Department Cost Allocation Valron Company has two support departments, Human Resources and General Factory, and two producing departments, Fabricating and Assembly Support Departments Producing Departments Human Resources General Factory Fabricating Assembly Direct costs $160,000 $340,000 $114,600 $93,000 Normal activity: Number of employees 60 80 120 170 Square footage 1,000 5,700 13,300 The costs of the Human Resources Department are allocated on the basis of number of employees, and the costs of General Factory are allocated on...

Direct Method of Support Department Cost Allocation Valron Company has two support departments, Human Resources and...

Direct Method of Support Department Cost Allocation Valron Company has two support departments, Human Resources and General Factory, and two producing departments, Fabricating and Assembly. Support Departments Producing Departments Human Resources General Factory Fabricating Assembly Direct costs $160,000 $340,000 $114,600 $93,000 Normal activity: Number of employees — 60 80 170 Square footage 1,000 — 5,700 13,300 The costs of the Human Resources Department are allocated on the basis of number of employees, and the costs of General Factory are allocated...

Direct Method of Support Department Cost Allocation Valron Company has two support departments, Human Resources and...

Direct Method of Support Department Cost Allocation Valron Company has two support departments, Human Resources and General Factory, and two producing departments, Fabricating and Assembly. Support Departments Producing Departments Human Resources General Factory Fabricating Assembly Direct costs $160,000 $340,000 $114,600 $93,000 Normal activity: Number of employees — 60 80 170 Square footage 1,000 — 5,700 13,300 The costs of the Human Resources Department are allocated on the basis of number of employees, and the costs of General Factory are allocated...

Direct Method of Support Department Cost Allocation Valron Company has two support departments, Human Resources and...

Direct Method of Support Department Cost Allocation Valron Company has two support departments, Human Resources and General Factory, and two producing departments, Fabricating and Assembly. Support Departments Producing Departments Human Resources General Factory Fabricating Assembly Direct costs $150,000 $330,000 $114,200 $94,000 Normal activity: Number of employees — 60 80 170 Square footage 1,000 — 5,700 13,300 The costs of the Human Resources Department are allocated on the basis of number of employees, and the costs of General Factory are allocated...

Comparison of Methods of Allocation Duweynie Pottery, Inc., is divided into two operating divisions: Pottery and...

Comparison of Methods of Allocation Duweynie Pottery, Inc., is divided into two operating divisions: Pottery and Retail. The company allocates Power and General Factory department costs to each operating division. Power costs are allocated on the basis of the number of machine hours and general factory costs on the basis of square footage. No effort is made to separate fixed and variable costs; however, only budgeted costs are allocated. Allocations for the coming year are based on the following data:...

Support department cost allocation—comparison Becker Tabletops has two support departments ( Janitorial and Cafeteria) a...

Support department cost allocation—comparison Becker Tabletops has two support departments ( Janitorial and Cafeteria) and two production departments (Cutting and Assembly). Relevant details for these departments are as follows: Support Department Cost Driver Janitorial Department Square footage to be serviced Cafeteria Department Number of employees Janitorial Department Cafeteria Department Cutting Department Assembly Department Department costs $310,000 $169,000 $1,504,000 $680,000 Square feet 50 5,000 1,000 4,000 Number of employees 10 3 30 10 Allocated the support department costs to the production...

(Appendix 4B) Support Department Cost Allocation MedServices Inc. is divided into two operating departments: Laboratory and...

(Appendix 4B) Support Department Cost Allocation MedServices Inc. is divided into two operating departments: Laboratory and Tissue Pathology. The company allocates delivery and accounting costs to each operating department. Delivery costs include the costs of a fleet of vans and drivers that drive throughout the state each day to clinics and doctors' offices to pick up samples and deliver them to the centrally located laboratory and tissue pathology offices. Delivery costs are allocated on the basis of number of samples....

(Appendix 4B) Support Department Cost Allocation MedServices Inc. is divided into two operating departments: Laboratory and Tissue Pathology. The company allocates delivery and accounting costs to each operating department. Delivery costs include the costs of a fleet of vans and drivers that drive throughout the state each day to clinics and doctors' offices to pick up samples and deliver them to the centrally located laboratory and tissue pathology offices. Delivery costs are allocated on the basis of number of samples....

(Appendix 4B) Sequential Method of Support Department Cost Allocation Stevenson Company is divided into two operating divisions: Battery and Small Motors. The company allocates power and general factory costs to each operating division using the sequential method. General Factory is allocated first in the sequential method for the company. Support department cost allocations using the sequential method are based on the following data: Support Departments Operating Divisions General Factory Small Motors Power Battery Overhead costs $430,000 $84,600 $160,000 2,000 $163,000...

(Appendix 4B) Sequential Method of Support Department Cost Allocation Stevenson Company is divided into two operating divisions: Battery and Small Motors. The company allocates power and general factory costs to each operating division using the sequential method. General Factory is allocated first in the sequential method for the company. Support department cost allocations using the sequential method are based on the following data: Support Departments Operating Divisions General Factory Small Motors Power Battery Overhead costs $430,000 $84,600 $160,000 2,000 $163,000...

Direct Method of Support Department Cost Allocation Valron Company has two support departments, Human Resources and General Factory, and two producing departments, Fabricating and Assembly Support Departments Producing Departments Human Resources General Factory Fabricating Assembly Direct costs $160,000 $340,000 $114,600 $93,000 Normal activity: Number of employees 60 80 120 170 Square footage 1,000 5,700 13,300 The costs of the Human Resources Department are allocated on the basis of number of employees, and the costs of General Factory are allocated on...

Direct Method of Support Department Cost Allocation Valron Company has two support departments, Human Resources and General Factory, and two producing departments, Fabricating and Assembly Support Departments Producing Departments Human Resources General Factory Fabricating Assembly Direct costs $160,000 $340,000 $114,600 $93,000 Normal activity: Number of employees 60 80 120 170 Square footage 1,000 5,700 13,300 The costs of the Human Resources Department are allocated on the basis of number of employees, and the costs of General Factory are allocated on...

(Appendix 4B) Support Department Cost Allocation MedServices Inc. is divided into two operating departments: Laboratory and Tissue Pathology. The company allocates delivery and accounting costs to each operating department. Delivery costs include the costs of a fleet of vans and drivers that drive throughout the state each day to clinics and doctors' offices to pick up samples and deliver them to the centrally located laboratory and tissue pathology offices. Delivery costs are allocated on the basis of number of samples....

(Appendix 4B) Support Department Cost Allocation MedServices Inc. is divided into two operating departments: Laboratory and Tissue Pathology. The company allocates delivery and accounting costs to each operating department. Delivery costs include the costs of a fleet of vans and drivers that drive throughout the state each day to clinics and doctors' offices to pick up samples and deliver them to the centrally located laboratory and tissue pathology offices. Delivery costs are allocated on the basis of number of samples....

Most questions answered within 3 hours.

-

The average length of time between arrivals at a turnpike

toll-booth is 26 seconds. What is...

asked 30 minutes ago -

(a) A piston at 6.1 atm contains a gas that occupies a volume of

3.5 L....

asked 1 hour ago -

Please answer true or false. Words

cannot be changed or added in to make it true...

asked 1 hour ago -

An empty test tube weighs 15.923 grams. Then,

MgCl2•6H2O is added into the test tube. After...

asked 1 hour ago -

Assume memory access is 10 units of time and disk access is

10000 units of time....

asked 2 hours ago -

1. Are all good samples random?

2. Magazines often report surveys giving statistics such as “63%...

asked 2 hours ago -

Under all the various types of market structures, firms

must eventually earn some economic profits for...

asked 2 hours ago -

Consider the following fitness regime for a single locus trait

with two co-dominant alleles: w11 =...

asked 2 hours ago -

A large cable company reports the following.

80% of its customers subscribe to its cable TV...

asked 2 hours ago -

Please answer the question in brief.

Discuss the role of ERP in organizations. Are ERP tools...

asked 2 hours ago -

Discuss the pros and cons of collaborative software such

as SameTime. Does it increase productivity? What...

asked 2 hours ago -

Buying your in-laws a gift because it’s expected is

due to the ____________ motive of gift-giving....

asked 2 hours ago