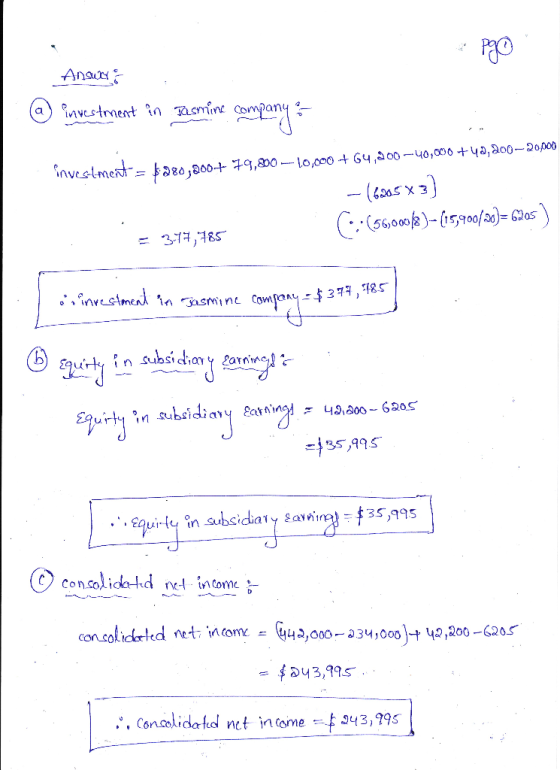

Tyler Company acquired all of Jasmine Company’s outstanding stock on January 1, 2016, for $280,200 in...

Tyler Company acquired all of Jasmine Company’s outstanding stock on January 1, 2016, for $280,200 in cash. Jasmine had a book value of only $199,400 on that date. However, equipment (having an eight-year remaining life) was undervalued by $56,000 on Jasmine’s financial records. A building with a 20-year remaining life was overvalued by $15,900. Subsequent to the acquisition, Jasmine reported the following:

| Net Income | Dividends Declared | |||||

| 2016 | $ | 79,800 | $ | 10,000 | ||

| 2017 | 64,200 | 40,000 | ||||

| 2018 | 42,200 | 20,000 | ||||

In accounting for this investment, Tyler has used the equity

method. Selected accounts taken from the financial records of these

two companies as of December 31, 2018, follow:

| Tyler Company | Jasmine Company | ||||||

| Revenues—operating | $ | (442,000 | ) | $ | (167,000 | ) | |

| Expenses | 234,000 | 124,800 | |||||

| Equipment (net) | 398,000 | 57,000 | |||||

| Buildings (net) | 286,000 | 70,500 | |||||

| Common stock | (290,000 | ) | (57,600 | ) | |||

| Retained earnings, 12/31/18 | (586,000 | ) | (226,000 | ) | |||

Determine the following account balances as of December 31, 2018:

| a. | Investment in Jasmine Company | |

| b. | Equity in Subsidiary Earnings | |

| c. | Consolidated Net Income | |

| d. | Consolidated Equipment (net) | |

| e. | Consolidated Buildings (net) | |

| f. | Consolidated Goodwill (net) | |

| g. | Consolidated Common Stock | |

| h. | Consolidated Retained Earnings, 12/31/18 |

Homework Answers

Add Answer to:

Tyler Company acquired all of Jasmine Company’s outstanding

stock on January 1, 2016, for $280,200 in...

Tyler Company acquired all of Jasmine Company’s outstanding stock on January 1, 2016, for $206,000 in...

Tyler Company acquired all of Jasmine Company’s outstanding stock on January 1, 2016, for $206,000 in cash. Jasmine had a book value of only $140,000 on that date. However, equipment (having an eight-year remaining life) was undervalued by $54,400 on Jasmine’s financial records. A building with a 20-year remaining life was overvalued by $10,000. Subsequent to the acquisition, Jasmine reported the following:In accounting for this investment, Tyler has used the equity method. Selected accounts taken from the financial records of...

Tyler Company acquired all of Jasmine Company’s outstanding stock on January 1, 2016, for $206,000 in cash. Jasmine had a book value of only $140,000 on that date. However, equipment (having an eight-year remaining life) was undervalued by $54,400 on Jasmine’s financial records. A building with a 20-year remaining life was overvalued by $10,000. Subsequent to the acquisition, Jasmine reported the following:In accounting for this investment, Tyler has used the equity method. Selected accounts taken from the financial records of...

Tyler Company acquired all of Jasmine Company's outstanding stock on January 1, 2016, for $269,500 in...

Tyler Company acquired all of Jasmine Company's outstanding stock on January 1, 2016, for $269,500 in cash. Jasmine had a book value of only $188,500 on that date. However, equipment (having an eight-year remaining life) was undervalued by $56,800 on Jasmine's financial records. A building with a 20-year remaining life was overvalued by $13,600. Subsequent to the acquisition, Jasmine reported the following: Dividends Net Income Declared 2016 2017 2018 $75,300 64,500 34,800 $10,000 40,000 20,000 In accounting for this investment,...

Tyler Company acquired all of Jasmine Company's outstanding stock on January 1, 2016, for $269,500 in cash. Jasmine had a book value of only $188,500 on that date. However, equipment (having an eight-year remaining life) was undervalued by $56,800 on Jasmine's financial records. A building with a 20-year remaining life was overvalued by $13,600. Subsequent to the acquisition, Jasmine reported the following: Dividends Net Income Declared 2016 2017 2018 $75,300 64,500 34,800 $10,000 40,000 20,000 In accounting for this investment,...

Problem 3-36 (LO 3-3a) Tyler Company acquired all of Jasmine Company’s outstanding stock on January 1,...

Problem 3-36 (LO 3-3a) Tyler Company acquired all of Jasmine Company’s outstanding stock on January 1, 2016, for $258,100 in cash. Jasmine had a book value of only $189,500 on that date. However, equipment (having an eight-year remaining life) was undervalued by $68,000 on Jasmine’s financial records. A building with a 20-year remaining life was overvalued by $15,000. Subsequent to the acquisition, Jasmine reported the following: Net Income Dividends Declared 2016 $ 65,400 $ 10,000 2017 80,500 40,000 2018 33,000...

Foxx Corporation acquired all of Greenburg Company’s outstanding stock on January 1, 2016, for $771,000 cash....

Foxx Corporation acquired all of Greenburg Company’s outstanding stock on January 1, 2016, for $771,000 cash. Greenburg’s accounting records showed net assets on that date of $542,000, although equipment with a 10-year life was undervalued on the records by $168,000. Any recognized goodwill is considered to have an indefinite life. Greenburg reports net income in 2016 of $112,000 and $135,000 in 2017. The subsidiary declared dividends of $20,000 in each of these two years. Account balances for the year ending...

Foxx Corporation acquired all of Greenburg Company’s outstanding stock on January 1, 2016, for $646,000 cash....

Foxx Corporation acquired all of Greenburg Company’s outstanding stock on January 1, 2016, for $646,000 cash. Greenburg’s accounting records showed net assets on that date of $497,000, although equipment with a 10-year life was undervalued on the records by $66,000. Any recognized goodwill is considered to have an indefinite life. Greenburg reports net income in 2016 of $119,000 and $100,500 in 2017. The subsidiary declared dividends of $20,000 in each of these two years. Account balances for the year ending...

Miller Company acquired an 80 percent interest in Taylor Company on January 1, 2016. Miller paid...

Miller Company acquired an 80 percent interest in Taylor Company on January 1, 2016. Miller paid $800,000 in cash to the owners of Taylor to acquire these shares. In addition, the remaining 20 percent of Taylor shares continued to trade at a total value of $200,000 both before and after Miller’s acquisition. On January 1, 2016, Taylor reported a book value of $674,000 (Common Stock = $337,000; Additional Paid-In Capital = $101,100; Retained Earnings = $235,900). Several of Taylor’s buildings...

Miller Company acquired an 80 percent interest in Taylor Company on January 1, 2016. Miller paid...

Miller Company acquired an 80 percent interest in Taylor Company on January 1, 2016. Miller paid $888,000 in cash to the owners of Taylor to acquire these shares. In addition, the remaining 20 percent of Taylor shares continued to trade at a total value of $222,000 both before and after Miller’s acquisition. On January 1, 2016, Taylor reported a book value of $634,000 (Common Stock = $317,000; Additional Paid-In Capital = $95,100; Retained Earnings = $221,900). Several of Taylor’s buildings...

Miller Company acquired an 80 percent interest in Taylor Company on January 1, 2016. Miller paid...

Miller Company acquired an 80 percent interest in Taylor Company on January 1, 2016. Miller paid $784,000 in cash to the owners of Taylor to acquire these shares. In addition, the remaining 20 percent of Taylor shares continued to trade at a total value of $196,000 both before and after Miller's acquisition. On January 1, 2016, Taylor reported a book value of $768,000 (Common Stock = $384,000; Additional Paid-In Capital = $115,200; Retained Earnings = $268,800). Several of Taylor's buildings...

Miller Company acquired an 80 percent interest in Taylor Company on January 1, 2016. Miller paid $784,000 in cash to the owners of Taylor to acquire these shares. In addition, the remaining 20 percent of Taylor shares continued to trade at a total value of $196,000 both before and after Miller's acquisition. On January 1, 2016, Taylor reported a book value of $768,000 (Common Stock = $384,000; Additional Paid-In Capital = $115,200; Retained Earnings = $268,800). Several of Taylor's buildings...

Pitino acquired 90 percent of Brey's outstanding shares on January 1, 2016, in exchange for $423,000...

Pitino acquired 90 percent of Brey's outstanding shares on

January 1, 2016, in exchange for $423,000 in cash. The subsidiary's

stockholders' equity accounts totaled $407,000 and the

noncontrolling interest had a fair value of $47,000 on that day.

However, a building (with a ten-year remaining life) in Brey's

accounting records was undervalued by $31,000. Pitino assigned the

rest of the excess fair value over book value to Brey's patented

technology (four-year remaining life).

Brey reported net income from its own...

Pitino acquired 90 percent of Brey's outstanding shares on

January 1, 2016, in exchange for $423,000 in cash. The subsidiary's

stockholders' equity accounts totaled $407,000 and the

noncontrolling interest had a fair value of $47,000 on that day.

However, a building (with a ten-year remaining life) in Brey's

accounting records was undervalued by $31,000. Pitino assigned the

rest of the excess fair value over book value to Brey's patented

technology (four-year remaining life).

Brey reported net income from its own...

On January 1, 2016, Monica Company acquired 80 percent of Young Company’s outstanding common stock for...

On January 1, 2016, Monica Company acquired 80 percent of Young Company’s outstanding common stock for $760,000. The fair value of the noncontrolling interest at the acquisition date was $190,000. Young reported stockholders’ equity accounts on that date as follows: Common stock—$10 par value $ 200,000 Additional paid-in capital 50,000 Retained earnings 470,000 In establishing the acquisition value, Monica appraised Young's assets and ascertained that the accounting records undervalued a building (with a five-year remaining life) by $50,000. Any remaining...

Tyler Company acquired all of Jasmine Company’s outstanding stock on January 1, 2016, for $206,000 in cash. Jasmine had a book value of only $140,000 on that date. However, equipment (having an eight-year remaining life) was undervalued by $54,400 on Jasmine’s financial records. A building with a 20-year remaining life was overvalued by $10,000. Subsequent to the acquisition, Jasmine reported the following:In accounting for this investment, Tyler has used the equity method. Selected accounts taken from the financial records of...

Tyler Company acquired all of Jasmine Company’s outstanding stock on January 1, 2016, for $206,000 in cash. Jasmine had a book value of only $140,000 on that date. However, equipment (having an eight-year remaining life) was undervalued by $54,400 on Jasmine’s financial records. A building with a 20-year remaining life was overvalued by $10,000. Subsequent to the acquisition, Jasmine reported the following:In accounting for this investment, Tyler has used the equity method. Selected accounts taken from the financial records of...

Tyler Company acquired all of Jasmine Company's outstanding stock on January 1, 2016, for $269,500 in cash. Jasmine had a book value of only $188,500 on that date. However, equipment (having an eight-year remaining life) was undervalued by $56,800 on Jasmine's financial records. A building with a 20-year remaining life was overvalued by $13,600. Subsequent to the acquisition, Jasmine reported the following: Dividends Net Income Declared 2016 2017 2018 $75,300 64,500 34,800 $10,000 40,000 20,000 In accounting for this investment,...

Tyler Company acquired all of Jasmine Company's outstanding stock on January 1, 2016, for $269,500 in cash. Jasmine had a book value of only $188,500 on that date. However, equipment (having an eight-year remaining life) was undervalued by $56,800 on Jasmine's financial records. A building with a 20-year remaining life was overvalued by $13,600. Subsequent to the acquisition, Jasmine reported the following: Dividends Net Income Declared 2016 2017 2018 $75,300 64,500 34,800 $10,000 40,000 20,000 In accounting for this investment,...

Miller Company acquired an 80 percent interest in Taylor Company on January 1, 2016. Miller paid $784,000 in cash to the owners of Taylor to acquire these shares. In addition, the remaining 20 percent of Taylor shares continued to trade at a total value of $196,000 both before and after Miller's acquisition. On January 1, 2016, Taylor reported a book value of $768,000 (Common Stock = $384,000; Additional Paid-In Capital = $115,200; Retained Earnings = $268,800). Several of Taylor's buildings...

Miller Company acquired an 80 percent interest in Taylor Company on January 1, 2016. Miller paid $784,000 in cash to the owners of Taylor to acquire these shares. In addition, the remaining 20 percent of Taylor shares continued to trade at a total value of $196,000 both before and after Miller's acquisition. On January 1, 2016, Taylor reported a book value of $768,000 (Common Stock = $384,000; Additional Paid-In Capital = $115,200; Retained Earnings = $268,800). Several of Taylor's buildings...

Pitino acquired 90 percent of Brey's outstanding shares on

January 1, 2016, in exchange for $423,000 in cash. The subsidiary's

stockholders' equity accounts totaled $407,000 and the

noncontrolling interest had a fair value of $47,000 on that day.

However, a building (with a ten-year remaining life) in Brey's

accounting records was undervalued by $31,000. Pitino assigned the

rest of the excess fair value over book value to Brey's patented

technology (four-year remaining life).

Brey reported net income from its own...

Pitino acquired 90 percent of Brey's outstanding shares on

January 1, 2016, in exchange for $423,000 in cash. The subsidiary's

stockholders' equity accounts totaled $407,000 and the

noncontrolling interest had a fair value of $47,000 on that day.

However, a building (with a ten-year remaining life) in Brey's

accounting records was undervalued by $31,000. Pitino assigned the

rest of the excess fair value over book value to Brey's patented

technology (four-year remaining life).

Brey reported net income from its own...

Most questions answered within 3 hours.

-

A 8.15- g bullet from a 9-mm pistol has a velocity of 366.0 m/s.

It strikes...

asked 32 minutes ago -

The outstanding bonds of Alpha Extracts have a yield to maturity

of 7.4 percent and a...

asked 29 minutes ago -

The Problem: The Case of the Harmonizing Vacations

Your CEO is exploring partnering with a European...

asked 1 hour ago -

A chemical equation is balanced by adding coefficients in front

of some formulas so that the...

asked 1 hour ago -

From the literature (reference your sources): What are the

lattice parameters of calcite and aragonite? Why...

asked 2 hours ago -

Your system is rejecting the question am asking which is

preceded by a case study. It...

asked 2 hours ago -

3. On January 2, 2000, Larry creates a trust with himself as

trustee. Larry as trustee...

asked 2 hours ago -

A member of the volleyball team spikes the ball. During this

process, she changes the velocity...

asked 2 hours ago -

Are adult gamers less likely to use a gaming console (Xbox,

PlayStation, Wii, etc...) than teen...

asked 3 hours ago -

The University of

Texas recently reported that 43% of college students aged 18-24

would spend their...

asked 3 hours ago -

The length of stay at a specific emergency department in

Phoenix, Arizona, in 2009 had a...

asked 3 hours ago -

. Please give the mechanism for this type of problem. Step by

Step

The toxin that...

asked 3 hours ago