Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A,...

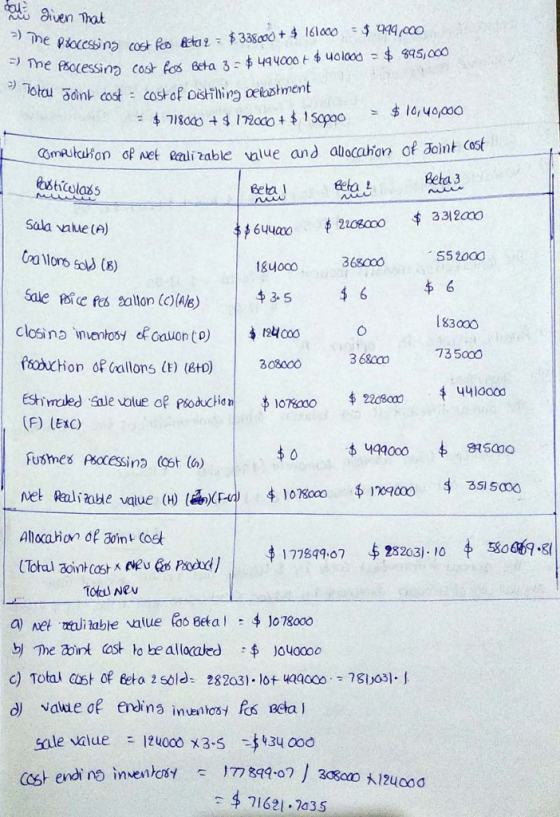

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta-1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing; it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified in Department C. Following is a summary of costs and other related data for the year ended November 30.

| Department | (1) Distilling | (2) Fusing | (3) Solidifying | ||||||

| Cost of Alpha-11 | $ | 718,000 | 0 | 0 | |||||

| Direct labor | 172,000 | $ | 338,000 | $ | 494,000 | ||||

| Manufacturing overhead | 150,000 | 161,000 | 401,000 | ||||||

| Products | Beta-1 | Beta-2 | Beta-3 | ||||||

| Gallons sold | 184,000 | 368,000 | 552,000 | ||||||

| Gallons on hand at year-end | 124,000 | 0 | 183,000 | ||||||

| Sales | $ | 644,000 | $ | 2,208,000 | $ | 3,312,000 | |||

Davenport had no beginning inventories on hand at December 1 and no Alpha-11 on hand at the end of the year on November 30. All gallons on hand on November 30 were complete as to processing. Davenport uses the net realizable value method to allocate joint costs.

Required:

Compute the following:

a. The net realizable value of Beta-1 for the year ended November 30.

net realizable value of beta-1

b. The joint costs for the year ended November 30 to be allocated.

joint costs

c. The cost of Beta-2 sold for the year ended November 30. (Do not round intermediate calculations.)

cost of beta-2 sold

d. The value of the ending inventory for Beta-1. (Do not round intermediate calculations.)

ending inventory for beta-1

Homework Answers

Add Answer to:

Davenport Company buys Alpha-11 for $6 a gallon. At the end of

distilling in Department A,...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A,...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta-1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing; it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified in Department C. Following is a summary of costs and other related data for the year ended November 30. Department (1) Distilling...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A,...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta-1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing; it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified in Department C. Following is a summary of costs and other related data for the year ended November 30. Department (1) Distilling...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A,...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta- 1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing, it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified In Department C. Following is a summary of costs and other related data for the year ended November 30. (1 )...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta- 1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing, it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified In Department C. Following is a summary of costs and other related data for the year ended November 30. (1 )...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A,...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta-1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing; it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified in Department C. Following is a summary of costs and other related data for the year ended November 30. Department (1) Distilling...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta-1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing; it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified in Department C. Following is a summary of costs and other related data for the year ended November 30. Department (1) Distilling...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A,...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta-1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing; it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified in Department C. Following is a summary of costs and other related data for the year ended November 30. Department (1) Distilling...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A,...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta- 1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing; it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified in Department C. Following is a summary of costs and other related data for the year ended November 30. (1) Distilling...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta- 1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing; it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified in Department C. Following is a summary of costs and other related data for the year ended November 30. (1) Distilling...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A,...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta- 1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing; it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified in Department C. Following is a summary of costs and other related data for the year ended November 30. 0.76 points...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta- 1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing; it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified in Department C. Following is a summary of costs and other related data for the year ended November 30. 0.76 points...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into production in Department X, and at the end of processing in this department, three products appear. Product A is sold at the split-off point with no further processing. Products B and C require further processing before they are sold. Product B is processed in Department Y, and product C is processed in Department Z. The company uses the estimated net realizable value method of...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into production in Department X, and at the end of processing in this department, three products appear. Product A is sold at the split-off point with no further processing. Products B and C require further processing before they are sold. Product B is processed in Department Y, and product C is processed in Department Z. The company uses the estimated net realizable value method of...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into production in Department X, and at the end of processing in this department, three products appear. Product A is sold at the split-off point with no further processing. Products B and C require further processing before they are sold. Product B is processed in Department Y, and product C is processed in Department Z. The company uses the estimated net realizable value method of...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into pr...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into production in Department X, and at the end of processing in this department, three products appear Product A is sold at the split-off point with no further processing. Products B and C require further processing before they are sold, Product B is processed in Department Y, and product C is processed in Department Z. The company uses the estimated net realizable value method of...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into production in Department X, and at the end of processing in this department, three products appear Product A is sold at the split-off point with no further processing. Products B and C require further processing before they are sold, Product B is processed in Department Y, and product C is processed in Department Z. The company uses the estimated net realizable value method of...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta- 1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing, it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified In Department C. Following is a summary of costs and other related data for the year ended November 30. (1 )...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta- 1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing, it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified In Department C. Following is a summary of costs and other related data for the year ended November 30. (1 )...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta-1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing; it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified in Department C. Following is a summary of costs and other related data for the year ended November 30. Department (1) Distilling...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta-1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing; it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified in Department C. Following is a summary of costs and other related data for the year ended November 30. Department (1) Distilling...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta- 1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing; it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified in Department C. Following is a summary of costs and other related data for the year ended November 30. (1) Distilling...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta- 1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing; it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified in Department C. Following is a summary of costs and other related data for the year ended November 30. (1) Distilling...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta- 1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing; it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified in Department C. Following is a summary of costs and other related data for the year ended November 30. 0.76 points...

Davenport Company buys Alpha-11 for $6 a gallon. At the end of distilling in Department A, Alpha-11 splits off into three products: Beta- 1, Beta-2, and Beta-3. Davenport sells Beta-1 at the split-off point, with no further processing; it processes Beta-2 and Beta-3 further before they can be sold. Beta-2 is fused in Department B, and Beta-3 is solidified in Department C. Following is a summary of costs and other related data for the year ended November 30. 0.76 points...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into production in Department X, and at the end of processing in this department, three products appear. Product A is sold at the split-off point with no further processing. Products B and C require further processing before they are sold. Product B is processed in Department Y, and product C is processed in Department Z. The company uses the estimated net realizable value method of...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into production in Department X, and at the end of processing in this department, three products appear. Product A is sold at the split-off point with no further processing. Products B and C require further processing before they are sold. Product B is processed in Department Y, and product C is processed in Department Z. The company uses the estimated net realizable value method of...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into production in Department X, and at the end of processing in this department, three products appear Product A is sold at the split-off point with no further processing. Products B and C require further processing before they are sold, Product B is processed in Department Y, and product C is processed in Department Z. The company uses the estimated net realizable value method of...

Fletcher Fabrication, Inc., produces three products by a joint production process. Raw materials are put into production in Department X, and at the end of processing in this department, three products appear Product A is sold at the split-off point with no further processing. Products B and C require further processing before they are sold, Product B is processed in Department Y, and product C is processed in Department Z. The company uses the estimated net realizable value method of...

Most questions answered within 3 hours.

-

2. What is the "great turnaround" with respect to offshore

labor?

asked 6 minutes ago -

Frost wedging breaks apart a large rock measuring 12 m

long by 12 m wide by...

asked 15 seconds from now -

Consider an 8 to 256 decoder built using 256 8-input AND

gates.

1. For the decimal...

asked 4 minutes ago -

A 0.510 m0.510 m aqueous solution of KBrKBr has a total mass of

71.0 g.71.0 g....

asked 8 minutes ago -

** use your own words, don't copy and paste, don't use

handwriting, please. i need your...

asked 12 minutes ago -

Calculate ΔHrxn for the following reaction: CH4 (g) + 4Cl2(g) →

CCl4(g) + 4HCl(g) Using the...

asked 14 minutes ago -

A.Consider the reaction when aqueous solutions of

chromium(II) sulfate and barium

acetate are combined. The net...

asked 28 minutes ago -

Two forces F1 =

-7.10i + 7.40j and

F2 = 6.80i +

3.40j are acting on...

asked 33 minutes ago -

Search the Internet regarding online Personal Health Records

(PHRs). Is an online personal health record different...

asked 44 minutes ago -

In a lottery game, a player picks 7 numbers from 1 to 43. How

many different...

asked 51 minutes ago -

How would transport and dispersion of pollutants from a coastal

stack be affected by the sea...

asked 52 minutes ago -

the

average length of a hospital stay is 4.8 days. if we assume the

lengths of...

asked 53 minutes ago