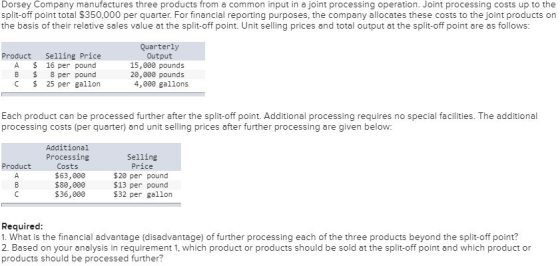

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $350,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows:

| Product | Selling Price | Quarterly Output |

||||

| A | $ | 16 | per pound | 15,000 | pounds | |

| B | $ | 8 | per pound | 20,000 | pounds | |

| C | $ | 25 | per gallon | 4,000 | gallons | |

Each product can be processed further after the split-off point. Additional processing requires no special facilities. The additional processing costs (per quarter) and unit selling prices after further processing are given below:

| Product | Additional Processing Costs |

Selling Price |

|||

| A | $ | 63,000 | $ | 20 | per pound |

| B | $ | 80,000 | $ | 13 | per pound |

| C | $ | 36,000 | $ | 32 | per gallon |

Required:

1. What is the financial advantage (disadvantage) of further processing each of the three products beyond the split-off point?

2. Based on your analysis in requirement 1, which product or products should be sold at the split-off point and which product or products should be processed further?

Homework Answers

1.allocate joint cost

| a | b | c | Total | |

| sales | 15000 | 20000 | 4000 | |

| sell price $ | 16 | 8 | 25 | |

| Total sales value | 240000 | 160000 | 100000 | 500000 |

| joint cost allocation | 168000[350000/500000]*240000 | 112000[350000/500000]*160000 | 70000[350000/500000]*100000 | 350000 |

Comparision between sold at split off and further processing

| A | B | C | |||||

| Sale at split off | 240000 | 160000 | 100000 | ||||

| Less: joint cost allocated | (168000) | (112000) | (70000) | ||||

| income A | 72000 | 48000 | 30000 | ||||

| further process | |||||||

| sales | 300000[15000*20] | 260000[20000*13] | 128000[4000*32] | ||||

| less: joint cost allocated | (168000) | (112000) | (70000) | ||||

| less: further processing cost | (63000) | (80000) | (36000) | ||||

| Net Income B | 69000 | 68000 | 22000 | ||||

|

Net financial advantage(disadvantage) B-A |

(3000) [69000-72000] |

20000 [68000-48000] |

(8000) [22000-30000] |

ANSWER 1 | |||

| FURTHER PROCESS OR SELL AT SPLIT OFF | SELL AT SPLIT OFF | Further process | SELL AT SPLIT OFF |

IF THER IS FINANCIAL DISADVANTAGE PRODUCT SHOULD NOT BE FURTHER PROCEESED.

Add Answer to:

Dorsey Company manufactures three products from a common input

in a joint processing operation. Joint processing...

Dorsey company... Dorsey Company manufactures three products from a common input in a joint processing operation....

Dorsey company...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $360,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: points Product A Selling Price $ 22.00 per pound $ 16.00 per pound $...

Dorsey company...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $360,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: points Product A Selling Price $ 22.00 per pound $ 16.00 per pound $...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $355,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product A B C Selling Price $ 21.00 per pound $ 15.00 per pound $ 27.00...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $355,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product A B C Selling Price $ 21.00 per pound $ 15.00 per pound $ 27.00...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing...

Dorsey Company manufactures three products from a common input in a

joint processing operation. Joint processing costs up to the

split-off point total $330,000 per quarter. For financial reporting

purposes, the company allocates these costs to the joint products

on the basis of their relative sales value at the split-off point.

Unit selling peices and total output at the split-off point are as

follows:

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing...

Dorsey Company manufactures three products from a common input in a

joint processing operation. Joint processing costs up to the

split-off point total $330,000 per quarter. For financial reporting

purposes, the company allocates these costs to the joint products

on the basis of their relative sales value at the split-off point.

Unit selling peices and total output at the split-off point are as

follows:

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $360,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product Selling Price 22.00 per pound $ 16.00 per pound $ 28.00 per gallon Quarterly Output...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $360,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product Selling Price 22.00 per pound $ 16.00 per pound $ 28.00 per gallon Quarterly Output...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $310,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product Selling Price $ 12.00 per pound $ 6.00 per pound $ 18.00 per gallon Quarterly...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $310,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product Selling Price $ 12.00 per pound $ 6.00 per pound $ 18.00 per gallon Quarterly...

Dorsey Company manufactures three products from a common Input In a joint processing operation. Joint processing...

Dorsey Company manufactures three products from a common Input In a joint processing operation. Joint processing costs up to the split-off point total $370,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product A B C Selling Price $ 24.00 per pound $ 18.00 per pound $ 30.00...

Dorsey Company manufactures three products from a common Input In a joint processing operation. Joint processing costs up to the split-off point total $370,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product A B C Selling Price $ 24.00 per pound $ 18.00 per pound $ 30.00...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $315,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Quarterly Output 11,600 pounds 18,200 pounds 2,800 gallons Selling Price 13.00 per pound $ 7.00 per...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $315,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Quarterly Output 11,600 pounds 18,200 pounds 2,800 gallons Selling Price 13.00 per pound $ 7.00 per...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $370,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Quarterly Output 13,800 pounds 21,500 pounds Product Selling Price A 24.00 per pound s 18.00 per...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $370,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Quarterly Output 13,800 pounds 21,500 pounds Product Selling Price A 24.00 per pound s 18.00 per...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $320,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product Selling Price Quarterly Output A $ 14.00 per pound 11,800 pounds B $ 8.00 per...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $350,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product Selling Price $ 16 per pound B $ 8 per pound C $ 25 per...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $350,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product Selling Price $ 16 per pound B $ 8 per pound C $ 25 per...

Dorsey company...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $360,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: points Product A Selling Price $ 22.00 per pound $ 16.00 per pound $...

Dorsey company...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $360,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: points Product A Selling Price $ 22.00 per pound $ 16.00 per pound $...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $355,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product A B C Selling Price $ 21.00 per pound $ 15.00 per pound $ 27.00...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $355,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product A B C Selling Price $ 21.00 per pound $ 15.00 per pound $ 27.00...

Dorsey Company manufactures three products from a common input in a

joint processing operation. Joint processing costs up to the

split-off point total $330,000 per quarter. For financial reporting

purposes, the company allocates these costs to the joint products

on the basis of their relative sales value at the split-off point.

Unit selling peices and total output at the split-off point are as

follows:

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing...

Dorsey Company manufactures three products from a common input in a

joint processing operation. Joint processing costs up to the

split-off point total $330,000 per quarter. For financial reporting

purposes, the company allocates these costs to the joint products

on the basis of their relative sales value at the split-off point.

Unit selling peices and total output at the split-off point are as

follows:

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $360,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product Selling Price 22.00 per pound $ 16.00 per pound $ 28.00 per gallon Quarterly Output...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $360,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product Selling Price 22.00 per pound $ 16.00 per pound $ 28.00 per gallon Quarterly Output...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $310,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product Selling Price $ 12.00 per pound $ 6.00 per pound $ 18.00 per gallon Quarterly...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $310,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product Selling Price $ 12.00 per pound $ 6.00 per pound $ 18.00 per gallon Quarterly...

Dorsey Company manufactures three products from a common Input In a joint processing operation. Joint processing costs up to the split-off point total $370,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product A B C Selling Price $ 24.00 per pound $ 18.00 per pound $ 30.00...

Dorsey Company manufactures three products from a common Input In a joint processing operation. Joint processing costs up to the split-off point total $370,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product A B C Selling Price $ 24.00 per pound $ 18.00 per pound $ 30.00...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $315,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Quarterly Output 11,600 pounds 18,200 pounds 2,800 gallons Selling Price 13.00 per pound $ 7.00 per...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $315,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Quarterly Output 11,600 pounds 18,200 pounds 2,800 gallons Selling Price 13.00 per pound $ 7.00 per...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $370,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Quarterly Output 13,800 pounds 21,500 pounds Product Selling Price A 24.00 per pound s 18.00 per...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $370,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Quarterly Output 13,800 pounds 21,500 pounds Product Selling Price A 24.00 per pound s 18.00 per...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $350,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product Selling Price $ 16 per pound B $ 8 per pound C $ 25 per...

Dorsey Company manufactures three products from a common input in a joint processing operation. Joint processing costs up to the split-off point total $350,000 per quarter. For financial reporting purposes, the company allocates these costs to the joint products on the basis of their relative sales value at the split-off point. Unit selling prices and total output at the split-off point are as follows: Product Selling Price $ 16 per pound B $ 8 per pound C $ 25 per...

Most questions answered within 3 hours.

-

On January 1, 2017, Nicks Corporation issued $250 million of

floating-rate debt. The debt carries a...

asked 32 minutes ago -

If Mark is unable to see objects clearly when they are placed

beyond 0.5m away, (a)...

asked 29 minutes ago -

Where there is no course of performance, usage of trade, or

course of dealing, and where...

asked 30 minutes ago -

A piece of charcoal (essentially 100% carbon) from an

archaeological site in Egypt is subjected to...

asked 46 minutes ago -

7) A) Balance the following reaction:

__H2SO4 + __NaOH __Na2SO4 + __H2O

b) Classify the...

asked 48 minutes ago -

Planets X, Y, and Z have circular orbits around a Star, which is

similar to our...

asked 57 minutes ago -

Use case analysis is used to ____

a) communicate system requirements

b) implement the system

c)...

asked 55 minutes ago -

What is the equilibrium constant for the reaction below, given

the listed concentrations at equilibrium? Report...

asked 58 minutes ago -

The following account appears in the ledger prior to recognizing

the jobs completed in August:

Work...

asked 59 minutes ago -

Air contained in a piston-cylinder undergoes two processes in

series. In the first the air expands...

asked 1 hour ago -

Propose a circuit that has an effective resistance of 6666ohms.

Include drawing.

asked 1 hour ago -

Starting with a given fatty acid: C22:6 w-3 go through the

process of beta oxidation. begin...

asked 1 hour ago